Doctor-Focused Mobile Healthcare Apps Enter Mid-Game: Practicality and Clinical Collaboration Emerge as Keys to Success

As the Internet increasingly permeates various industries, the world has begun to change. In the early stages, Internet healthcare enterprises were primarily health and medical web portals centered on PC-based services. They built market appeal by aggregating information and establishing platforms for health consultations, pathology queries, drug searches, databases of physicians and hospitals, as well as basic doctor-patient communication. After years of development, with the miniaturization of smart devices and the gradual maturation of Internet technologies, mobile Internet has emerged as a new growth driver for the Internet industry.

Whether on the patient side or the physician side, mobile health is becoming deeply integrated with medical services. For patients, mobile health platforms are building closed-loop service ecosystems and expanding into offline services. Meanwhile, mobile health apps for physicians are beginning to directly influence the delivery of medical care, becoming essential tools for clinicians.

Based on a survey of physicians’ usage of mobile health apps, this report provides an in-depth analysis of the application value and future development trends of physician-facing mobile health applications. Drawing on extensive interviews and analytical insights from the survey, we have prepared this industry research report on physician-oriented mobile apps, yielding the following key findings:

l Overall Trends in Physician-Facing Mobile Health Apps: From Information Dissemination to Workflow Assistance, and from Knowledge Services to Business Collaboration. This is specifically reflected in the shift of knowledge-enhancement apps toward more “practical” content, while tool-assistance apps feature increasingly granular functional modules tailored to specific clinical scenarios.

l The industry has entered a period of steady growth, with the market landscape becoming increasingly clear and business model innovations largely completed. This is specifically reflected in the significantly enhanced capital-raising capabilities of industry giants and a decline in overall industry financing scale. New entrants find it difficult to penetrate the market, as physician resources are concentrated in the hands of unicorns within several niche sectors.

l Knowledge-enhancement apps face low entry barriers, severe homogenization, and a nearing-saturation market, with social and utilitarian features determining their competitive differentiation. In contrast, tool-assistance apps are highly specialized, limited in variety, and not yet widely penetrated, indicating significant potential for future growth.

l Currently, the most urgent mobile health need among physicians is “out-of-hospital patient management,” with primary care physicians and junior doctors being the main sources of this demand. This also reflects the impact of tiered diagnosis and treatment on the industry. Out-of-hospital patient management and empowerment of primary care physicians may become the most valuable development direction for physician-facing mobile health apps.

l The profitability of physician-facing mobile health apps cannot rely solely on physicians themselves; it is essential to leverage physician resources through integration and connectivity to generate greater revenue. Currently, unicorns across various niche sectors are exploring how to utilize the physician resources on their platforms to expand their product lines.

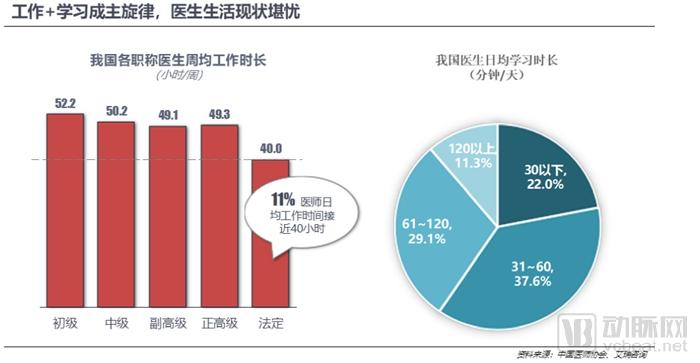

The White Paper on the Practice Status of Chinese Physicians, released by the Chinese Medical Doctor Association on January 9, 2018, reveals that physicians at all levels in China face considerable work pressure, with weekly working hours far exceeding the statutory 40-hour workweek. Among them, physicians with junior professional titles have the longest average weekly working hours, reaching 52 hours per week. Even associate senior physicians, who have the shortest working hours among the groups, still average 49.1 hours per week. Only 11% of physicians have weekly working hours close to 40 hours.

Unlike other professions, the quality of service provided by physicians is underpinned by their professional expertise, and the continuous updating of medical knowledge constitutes a critical component of career advancement for doctors. According to a report released by iResearch, nearly 80% of physicians spend more than half an hour on learning each day, with 11.3% dedicating over two hours daily to study.

We can imagine that after completing ten hours of high-pressure work per day, doctors still need to devote a significant portion of their rest time at home to studying. “Healthcare + Learning” has become the main theme of doctors’ lives.

Based on physicians’ needs, we categorize mobile health products for doctors into two major types: knowledge-enhancement products that meet their learning needs, and tool-assistance products that support the medical service delivery process.

Based on these two requirements from physicians, we categorize physician mobile apps into two major types:

Knowledge Enhancement Category: This category facilitates physicians’ knowledge advancement through education, live video streaming, and peer exchanges. Such mobile health products can be further subdivided into “Information Acquisition” and “Physician Social Networking.”

—Information Acquisition Category: Reflected in the enhancement of professional knowledge, primarily including news and literature, as well as education and training.

—Physician Social Networking: Reflects connectivity among physicians, primarily encompassing academic exchanges and topic discussions.

Tool-Assisted Category: Directly serving the medical process to enhance its convenience and immediacy. This type of mobile health product can be further subdivided into "Patient Management" and "Diagnostic and Therapeutic Assistance."

—Patient Management Category: Focused on connecting patients with providers, primarily including patient follow-up and mobile consultations.

— Auxiliary Diagnosis and Treatment Category: This involves empowering the diagnostic and treatment process with knowledge and tools, primarily including reference materials for diagnosis and treatment, medical calculation tools, etc.

In tool-assisted applications, we can also categorize them into mobile consultation apps and professional tool apps based on product characteristics. The value of the former is primarily tied to patients, while the latter’s value is mainly anchored in physicians.

Knowledge Enhancement Category: High product coverage and numerous profit opportunities, but significant homogenization.

Knowledge-enhancement platforms can be categorized into information-acquisition and physician-social networking types. Their product offerings include modules such as medical news, specialized medical knowledge, video courses, case libraries, drug information, and academic exchange. While these products suffer from significant homogenization, their monetization pathways are highly diversified due to the aggregation of the most core physician resources within the healthcare system.

Taking DXY as an example, founded in 2000, DXY is China's largest medical information and news platform as well as a professional communication platform for physicians, with a coverage rate exceeding 90% among healthcare professionals.

DXY can connect with the physician community and cover participants in the healthcare industry, including pharmaceutical companies, medical device manufacturers, and hospitals, by leveraging its platforms for drug and medical device advertising, online academic marketing, market research, procurement and investment promotion information dissemination, talent recruitment, conference services, and hospital branding services, thereby fully unlocking profit opportunities.

Tool-Assisted Category: High Growth Potential, Mostly Derived from Mobile Consultation

Tool-assisted applications primarily serve the medical service delivery process, with most products being physician-facing mobile consultation apps, such as the Haodaifu Online Doctor Edition and Ping An Good Doctor Doctor Edition. Additionally, there are products that approach patient management directly from the physician’s perspective, such as Xingshulin’s Medical Record Folder.

Compared with knowledge-enhancement products, tool-assisted products are more specialized and practical, with a more segmented user base.

Taking Xingshulin’s Medical Record Folder as an example, the app expands from patient medical records to clinical medical records. As a leading enterprise in tool-assisted applications, it has accumulated over 1 million registered users, accounting for approximately 35% of China’s 3 million licensed (assistant) physicians.

The scarcity of high-quality medical resources and the structural imbalance in their distribution are the primary factors constraining the enhancement of service capacity within China’s healthcare system. The fundamental approaches to addressing this issue generally stem from two strategies: increasing the supply of medical resources and optimizing the utilization of existing ones.

To expand the supply of medical resources, governments and healthcare institutions have primarily focused on building physician teams and enhancing both hardware and software infrastructure, aiming to improve physicians’ capabilities and availability, as well as the coverage and quality of technological infrastructure. However, this approach inevitably entails significant time and financial costs. On one hand, cultivating highly skilled physicians requires a training period spanning more than a decade; on the other hand, health information technology development demands substantial investment and prolonged periods for system integration and optimization.

Regarding resource allocation, the government primarily initiates efforts through policy implementation, advancing healthcare system reform. However, similar to “creating incremental healthcare capacity,” achieving resource allocation via policy remains a protracted process. During policy implementation, it is necessary to reconcile conflicting interests among various stakeholders and engage in continuous trial-and-error and corrective adjustments.

Overall, both the government and medical institutions are focusing on system construction to enhance the supply of medical resources and restructure the pathways for resource allocation. Although this is a fundamental solution to the problem, it requires significant time and cost, representing a long-term mechanism.

Meanwhile, mobile internet can drive systemic restructuring and even directly address certain issues of resource scarcity and unequal distribution. We believe that the benefits brought by mobile healthcare on the physician side include at least the following five points:

1. Promote tiered diagnosis and treatment, and leverage internet technology to allocate medical resources rationally

2. Achieved accessibility of medical services and improved service efficiency

3. Achieve efficient patient management by establishing electronic health records for patients

4. Fully leverage physicians' fragmented time to enhance their capabilities and efficiency

5. Reduce healthcare costs and save the nation substantial medical expenditures

Taking Hospital-Side Electronic Medical Records as an Example

Around the year 2000, China introduced electronic medical record (EMR) systems into hospital services. However, after two decades of development, domestic EMR products still lag significantly behind those in developed countries, particularly in terms of user-friendliness, granularity, and standardization.

Every day, physicians spend a significant amount of time entering patient medical record information. Discrepancies in electronic health record (EHR) standards across medical institutions hinder the circulation of medical records and prevent systematic research, reducing EHRs to mere digital archives of paper charts and significantly diminishing their utility. Furthermore, many healthcare organizations, particularly primary care institutions, cannot afford the substantial investment required for such extensive informatization infrastructure, resulting in a lack of systematic EHR solutions. Paper-based medical records suffer from even lower standardization, cumbersome retrieval processes, and limited potential for secondary use, making comparative analysis and research unfeasible. Consequently, physicians also devote considerable time to handwriting paper-based medical records.

Mobile Medical Record Management Apps: Built on mobile internet platforms, these applications standardize patient medical record templates, facilitating easier sharing, discussion, comparison, and research of case data. Furthermore, some apps leverage image and speech recognition technologies to streamline the entry of medical record information, thereby reducing tedious, low-value documentation tasks and enhancing the efficiency of medical services.

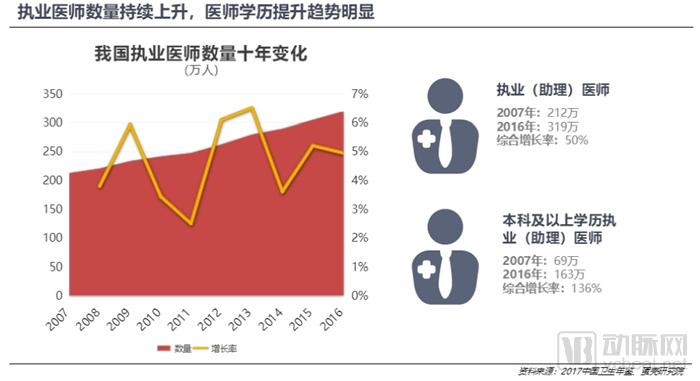

According to the latest data from the "2017 China Health Yearbook," the number of licensed (assistant) physicians in China reached 3.19 million in 2016, representing a 50% increase from 2.12 million a decade earlier. Compared with the overall growth in the physician workforce, structural changes in educational attainment among doctors are even more pronounced.

From 2007 to 2016, the number of licensed (assistant) physicians with a bachelor’s degree or higher increased from 690,000 in 2007 to 1.63 million in 2016, representing a cumulative growth rate of 136% and a net increase of 940,000. Given that the total net increase in the number of physicians was 1.07 million, it can be concluded that the growth in the physician workforce over the past decade was primarily driven by the increase in highly educated physicians.

For mobile health products designed for physicians, the continuous influx of young, highly educated doctors will steadily elevate the overall professionalism, thirst for knowledge, and acceptance of new technologies among the user base, thereby providing a stable demand foundation for the development of such physician-oriented mobile health solutions.

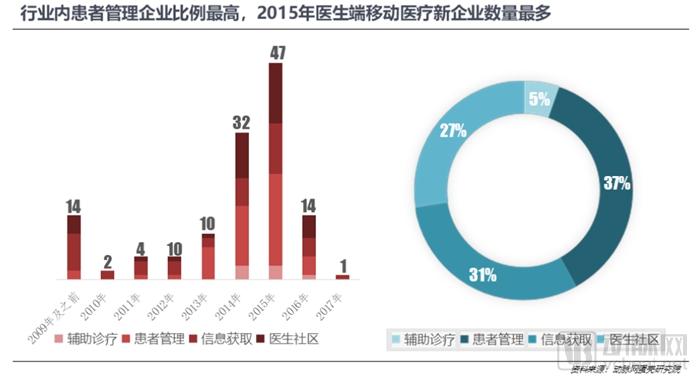

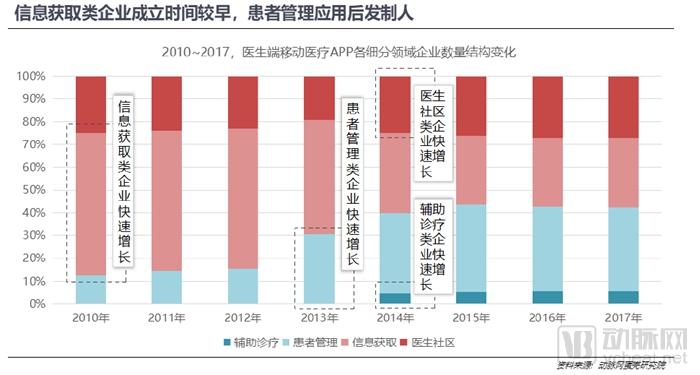

Since 2010, the number of participants in the physician-facing mobile health sector has continued to grow. In 2014, the number of newly established enterprises increased by 320% compared with 2013, driven primarily by the influx of capital and the widespread adoption of mobile internet. After 2015, the maturation of leading companies and the consolidation of the industry landscape made it increasingly difficult for new entrants to break into the market; whereas 47 new companies were added in 2015, only 14 new enterprises emerged in 2016.

Products designed for knowledge enhancement emerged earlier than those focused on tool-based assistance. Prior to 2013, the market was dominated by information-access products, including medical news platforms and medical literature databases. After 2013, with the rise of mobile consultation services and the evolution of product attributes, tool-assisted products—primarily patient management software—began to gain prominence. We believe that these differing development trajectories stem primarily from the distinct nature of the two product categories: products addressing knowledge-enhancement needs serve an informational integration role and have lower entry barriers, whereas those meeting medical assistance requirements must align with clinical service scenarios, entailing higher entry barriers and closer integration with the healthcare delivery process. Consequently, this developmental pattern reflects the trend in physician-facing mobile health products: evolving from information disseminators to workflow assistants, and from knowledge services to operational collaboration.

Prior to 2014, financing activity for physician-facing mobile health products remained relatively lukewarm, with the annual number of funding rounds consistently hovering around three.

In 2014, the heated discussion around “Internet + Healthcare” significantly boosted the fundraising capabilities of mobile health products, including those designed for physicians. The surge in financing interest in companies focused on information acquisition and patient management was the primary driver of overall industry funding growth.

In 2015, industry financing enthusiasm peaked, with a total of 28 financing events recorded, representing more than a two-fold increase compared to 2014. Of the incremental financing events that year, 68% were attributed to patient management products and physician community products, which saw increases of 6 and 9 financing events, respectively, compared to 2014.

In 2016, the growth in financing enthusiasm and scale stagnated. This was primarily due to the increasingly clear industrial landscape of patient management and physician communities, along with a significant decline in financing capabilities. However, professional tool-based companies, including Xingshulin, secured substantial funding, effectively mitigating the downturn in industry-wide financing enthusiasm.

The increasingly pronounced industry landscape has led to a significant decline in financing events across various subsectors. In particular, the information-access segment saw eight financing deals in 2016, which dropped to just two in 2017. Absent major external environmental shifts or wholly innovative business models, the physician-facing mobile health market is beginning to consolidate, with high-quality projects increasingly dominating the industry.

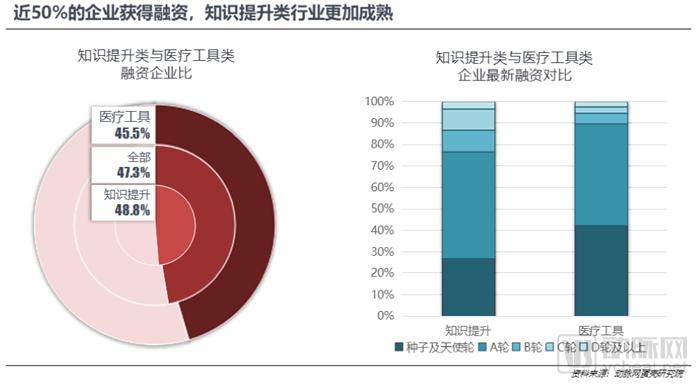

Currently, nearly 50% of companies in the industry have secured financing. The knowledge-enhancement segment exhibits a higher level of industry maturity compared to the tool-assistance segment. Among the funded companies, 75% of those in the former category have raised no more than Series A financing, whereas 90% of projects in the latter category remain at Series A or earlier stages, including seed and angel rounds.

Compared to tool-assisted solutions, knowledge-enhancement products emerged earlier. These products primarily focus on information aggregation and connecting with physicians, featuring lower entry barriers. In contrast, the latter requires integration into complex medical service processes and the establishment of deep collaborative relationships with physicians, resulting in higher entry barriers and a later emergence. Consequently, their financing rounds are more concentrated in early-stage projects.

Capital consolidation signifies the emergence of a distinct industry landscape. Currently, whether in knowledge-enhancement products or medical-assistance products, the industry structure is becoming increasingly clear, and business model innovation has largely been completed. This is specifically reflected in the significantly enhanced capital-raising capabilities of industry giants and the overall reduction in industry-wide financing scale. Among knowledge-enhancement enterprises, companies such as DXY and Medlinker have secured substantial financing amountsing to hundreds of millions of RMB. In the category of tool-based assistance products, apart from mobile consultation services, Xingshulin, which focuses on professional tools, has also raised $30 million. As time progresses, it is becoming increasingly difficult for new entrants to innovate their business models and challenge the industry giants that have already established significant advantages.

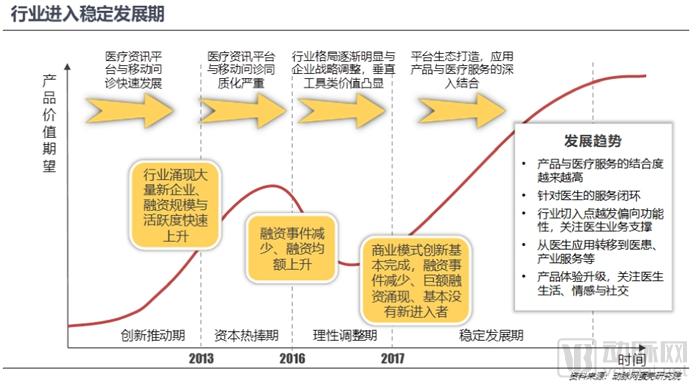

By analyzing the industry’s development trajectory and financing history, we can divide the evolution of the physician-facing mobile health sector into four stages: the Innovation-Driven Phase, the Capital Frenzy Phase, the Rational Adjustment Phase, and the Stable Growth Phase.

Exploration of business models by some companies in the industry can be traced back ten years. Before the rapid development of mobile internet, numerous physician-oriented vertical portals and forums had already emerged, exhibiting early-stage web-based prototypes with product positioning similar to information-acquisition platforms and physician communities. Meanwhile, there were also many online consultation platforms on the web, which later evolved into precursors of patient management tools for physicians. With the subsequent rise of mobile internet, these web-based products began migrating to mobile platforms, particularly those focused on knowledge enhancement, such as information acquisition and physician communities. Due to their low entry barriers and minimal migration costs, these types of products became the predominant form of mobile healthcare solutions targeted at physicians during that period.

Since 2013, the influx of capital has driven the rapid development of mobile health products for physicians, with patient management solutions being particularly prominent. Most patient management products evolved from physician-facing mobile consultation platforms. On the other hand, capital infusion led to a surge in low-barrier information and literature platforms, resulting in severe product homogenization and bottlenecks in business model innovation. Meanwhile, many physician-oriented clinical decision support apps also emerged during this period.

In 2016, the development of mobile health products for physicians cooled down. The number of newly established companies in this sector dropped to 14, significantly lower than the 47 recorded in 2015. Meanwhile, industry financing amounts declined for the first time. Capital markets began to concentrate on high-quality projects, signaling that the industry had entered a phase of rational adjustment, with its competitive landscape largely solidified.

After 2017, the industry entered a period of stable development, with the competitive landscape becoming increasingly distinct. This was specifically reflected in the virtual disappearance of new entrants and small-scale financing rounds, alongside a significant increase in the average financing amount. In 2017, all known investment deals in physician-focused mobile health projects exceeded RMB 10 million, with several large-scale financing rounds surpassing RMB 100 million; for example, Medlinker secured an investment of RMB 400 million in 2017.

In the future, whether in knowledge enhancement or tool-assisted categories, mobile medical products for physicians will face significant barriers to entry. As unicorns emerge across various niche sectors, the homogenization of product features will make it increasingly difficult for new entrants to disrupt the existing industry landscape. The competitive moats of high-quality projects will widen further as capital becomes more concentrated.

At the industry development level, as products and services gradually mature, product functionalities are becoming more refined. This is specifically reflected in the increasing support these products provide to physicians’ workflows and the deepening integration of products into medical processes. Therefore, medical professional tools that can most directly support and serve clinical workflows have broad prospects for growth. However, regardless of whether they are tool-assistance or knowledge-enhancement products, their future lies in providing comprehensive, all-around services to physicians, namely, the creation of a closed-loop service ecosystem.

In the course of this industry’s development, accurately grasping physicians’ pain points and gaining deep insights into their needs have become increasingly important.

To identify physicians’ key needs, VCBeat conducted a survey on their use of mobile health apps, aiming to understand both their product requirements and current usage patterns of mobile health products, thereby reflecting industry development trends.

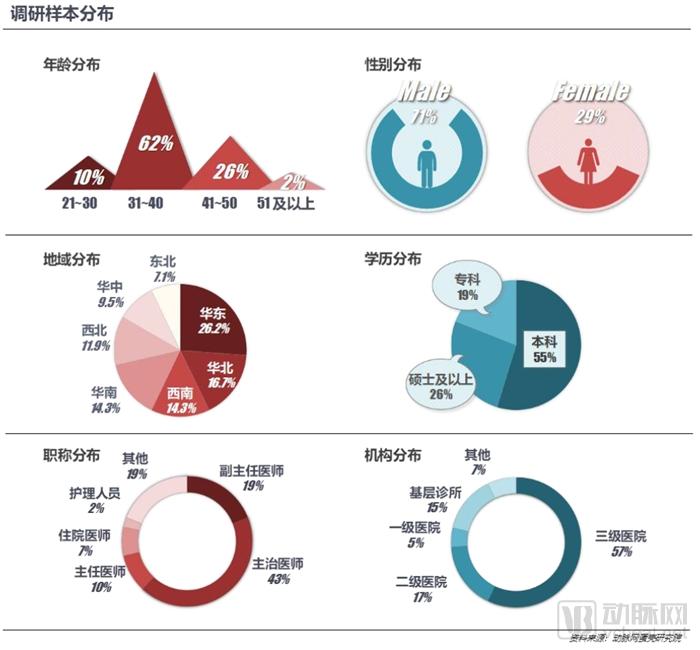

The survey was primarily conducted leveraging the physician resources available on the VCBeat platform. Questionnaires were distributed randomly, and the collected responses were analyzed to derive insights. Approximately 1,000 completed questionnaires were gathered from physician users, with samples covering a wide range of medical institutions across China, from tertiary hospitals to primary care facilities. This comprehensive coverage ensures that the sample sources are sufficiently dispersed. Therefore, although the data were obtained through sampling, the findings possess a certain degree of representativeness.

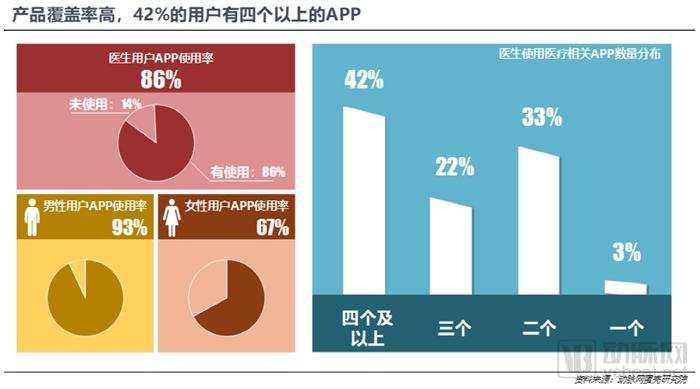

After several years of development, mobile healthcare products for physicians have reached 86% of the physician population in China. Among them, 97% of users have installed multiple mobile healthcare apps, with the majority having four or more; only 3% use a single app. This indicates that a single app currently fails to adequately meet physicians’ needs, requiring them to install multiple apps to fulfill their requirements.

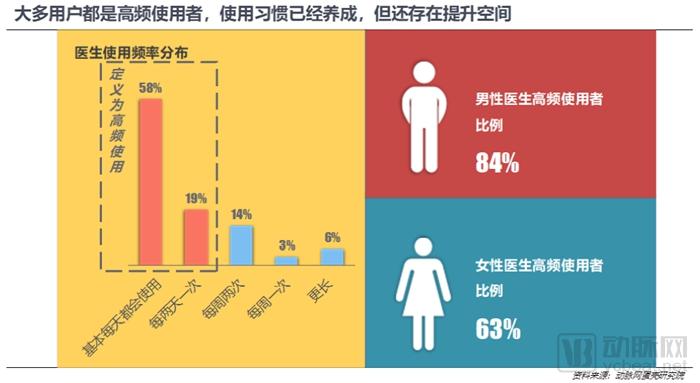

58% of physicians use mobile health apps on a daily basis. Defining users who access these apps more frequently than once every two days as high-frequency users, over 77% of the surveyed physicians fall into this category, indicating that user habits have been well established.

Although 86% of physicians have already installed mobile health products, and 77% of these users are high-frequency users, this does not mean that the physician-facing mobile health market has no room for incremental growth. On the contrary, we remain optimistic about the development trends of physician-facing mobile health products. This view is primarily based on three factors:

1. 42% of users have installed four or more apps, but 52% of users have no more than three apps, indicating a significant growth gap in the market

2. Among users who have installed mobile healthcare products, only 58% report using them “basically every day.” The increase in user frequency and duration of use is also a source of industry growth.

3. The integration of mobile health products with medical services is insufficient, indicating significant potential for further development

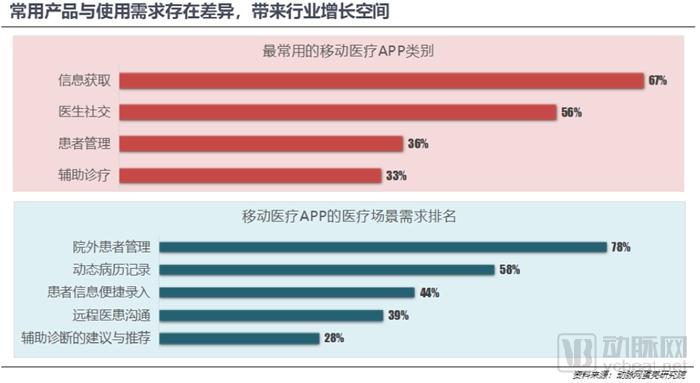

As previously stated, “the growing support of mobile health products for physicians’ work and their deepening integration into clinical workflows” represents the development trend of mobile health; products that most directly support and serve clinical processes have broader growth potential.

Survey results indicate that the clinical scenario in which physicians most desire assistance is “out-of-hospital patient management.” However, among the apps most frequently used by physicians, only 36% have chosen patient management applications corresponding to this need. This discrepancy is primarily because most current patient management software solutions are derived from the physician-facing versions of mobile diagnosis and treatment platforms. These products are mainly designed for patients on teleconsultation platforms, making them unsuitable for direct application in physicians’ daily workflow.

Most physicians are eager to receive support from mobile health apps across multiple dimensions, particularly at the practice management level. However, the mobile health apps currently in use often fail to meet these needs. For instance, while physicians seek tools to enhance consultation efficiency during patient encounters, the mobile health apps most frequently used by them are primarily medical news and information platforms.

In fact, similar products already exist in the market and have received positive user feedback for their effectiveness in supporting physicians’ clinical workflows. However, adoption rates among physicians remain low, likely due to insufficient promotion. Many physicians still perceive mobile health applications for providers merely as platforms for information dissemination and peer communication, unaware that certain apps can directly assist in clinical processes through a variety of functionalities. Regardless, bridging the gap between existing products and actual user needs represents a key direction for the future development of physician-facing mobile health solutions.

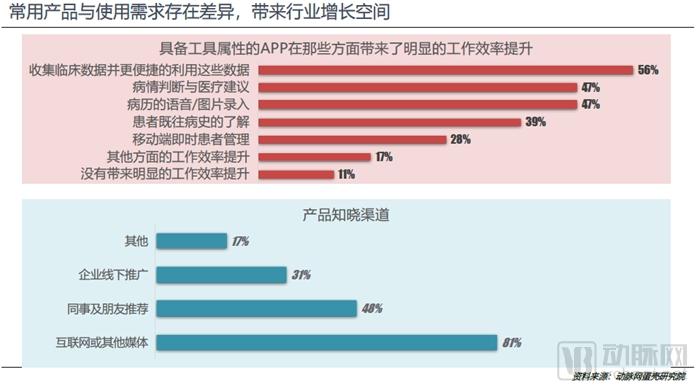

In our survey on how physicians learn about mobile health products, we found that “the Internet and other media” is the primary channel through which doctors become aware of these products. This indicates that “online promotion” is the main strategy enterprises use to market their offerings. “Recommendations from friends and colleagues” rank as the second most common source of awareness. Word-of-mouth has a significant impact on mobile health apps and serves as a crucial driver for their expansion. Physicians are willing to recommend only those apps that genuinely support their clinical workflows and enhance their professional capabilities, underscoring that practical utility is becoming key to boosting an app’s influence.

When examining whether tool-assisted products significantly enhance work efficiency, only 11% of users reported that medical utility apps do not help improve productivity. The majority of physicians believe that such tools have delivered tangible and notable efficiency gains in their work, particularly in three areas: clinical data collection, disease assessment, and automated medical record entry. Therefore, the reason why utility apps have not yet become the mainstream choice among physicians is that many doctors have not yet developed the habit of using them due to various factors.

We believe that utility-based mobile health apps can directly impact medical processes and enable physicians to perceive tangible benefits from these products; therefore, they are more “pragmatic” compared with knowledge-enhancement products.

In surveys, over 89% of physicians reported that tool-based mobile health apps significantly improved their work efficiency. However, compared with knowledge-enhancement apps, tool-assisted products entered the market later, face higher entry barriers, and currently suffer from lower brand awareness. Developers of tool-based mobile health solutions should continue to strengthen user education to help physicians understand the value of their products, thereby raising product visibility and cultivating habitual use of these apps. In the future, as tool-based mobile health apps gain deeper penetration among physicians, their influence will be progressively unlocked, becoming a key force in enhancing physician efficiency and liberating healthcare productivity.

Professional tool products represent a key direction for the deep integration of mobile health solutions and medical services, warranting dedicated research. How do such professional tools unlock medical productivity? How do physicians currently perceive and utilize these products? What is the current state of development for collaborative tool-based solutions? To address these questions, we must conduct an in-depth study of collaborative tool-based products.

Among work-assistance products, which include patient management products and clinical decision support (CDS) products, patient management offerings are primarily dominated by physician-side applications for mobile consultation services and do not constitute professional medical service tools. Therefore, we define patient management derivatives that incorporate mobile consultation features, along with CDS products, as professional tools—i.e., genuine medical tools.

Among these products, Xingshulin’s Medical Record Folder stands out as the most representative. Currently, Xingshulin has amassed over 1 million registered users, covering nearly one-third of China’s physician population. Therefore, we use Xingshulin’s operational data as the foundational dataset for studying physician-focused tool applications.

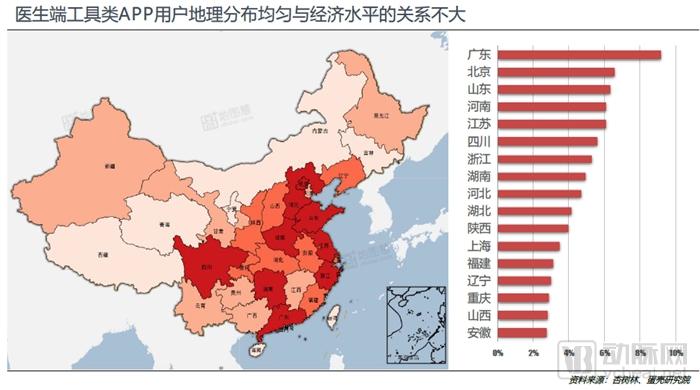

Due to the comprehensive development of mobile internet, the geographic distribution of users utilizing utility-based mobile health apps has become relatively balanced. Overall, however, physicians in economically developed regions demonstrate greater proactivity in adopting new tools. In certain central provinces, the large physician population combined with relatively low product penetration rates presents significant potential for industry growth. Among all regions, Guangdong ranks first in the geographic distribution of mobile health app users, accounting for 9.1% of the total user base.

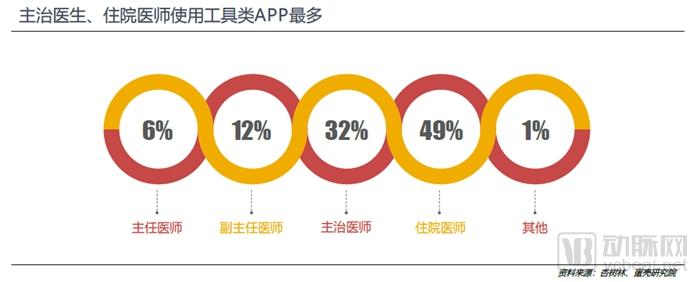

Attending physicians and resident physicians are the primary users of mobile health professional tool apps. These doctors are generally younger, more open to new technologies, and interact with a larger number of patients in their daily practice, making them the core audience for such applications. Junior physicians also entail lower user education costs.

Taking resident physicians as an example, this user group accounts for nearly 50% of the total user base of utility-oriented apps. In reality, however, resident physicians constitute only 35.1% of China’s licensed physician workforce.

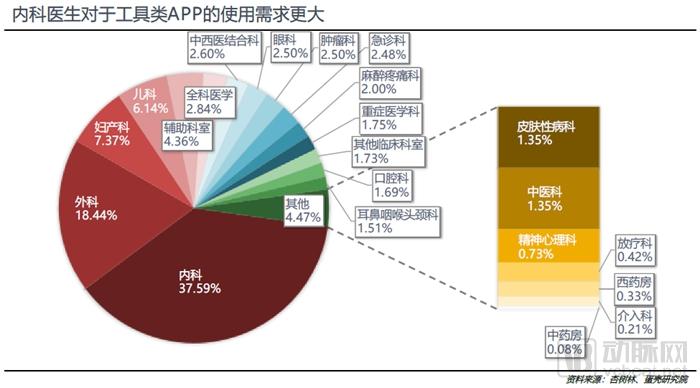

Among physicians using utility apps, internal medicine specialists demonstrate greater demand, accounting for 37.59% of physician users. In contrast, in 2016, internal medicine physicians comprised only 22.2% of licensed practitioners in China.

On the one hand, internal medicine encompasses dozens of subspecialties, including pulmonology, gastroenterology, and cardiology, resulting in a large base of physicians.

Furthermore, compared with surgeons, internists engage more frequently in tasks involving direct interaction with patients and medical records, such as ward rounds and outpatient consultations. These clinical settings often involve large volumes of disorganized patient information. The in-app tools can effectively assist physicians in organizing and structuring such data, thereby leading to greater demand for these tools among internists.

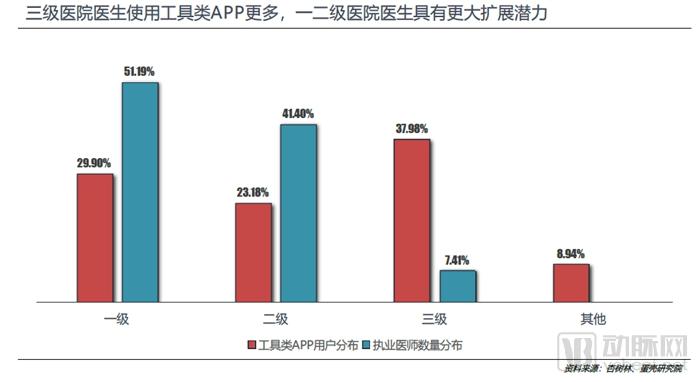

Among licensed physicians in China, the largest proportion practices in primary hospitals (Level I), accounting for over 51% of all licensed physicians, while the smallest proportion works in tertiary hospitals (Level III), with only 7% employed at this level. However, in terms of user distribution for physician utility apps, tertiary hospital doctors constitute the largest user base. Although they represent only 7.47% of all licensed physicians, they capture 37.89% of the market for physician utility apps.

There are two main reasons for this:

1. Physicians at tertiary hospitals often demonstrate stronger learning capabilities and a higher degree of receptiveness to new developments.

2. Physicians at tertiary hospitals work at a faster pace and under greater pressure, creating an urgent need for tool-based apps to assist them in their daily work. This further underscores the significant role that tool-based apps play for physicians.

Most Tier-1 medical institutions are primary care facilities. In China, the number of licensed physicians in Tier-2 medical institutions exceeds that in Tier-1 institutions, and their average educational attainment and learning capacity are higher than those in Tier-1 hospitals. However, when it comes to the adoption of utility-based mobile apps, physicians in primary care institutions are actually more active users.

This phenomenon arises from inadequate informatization infrastructure and insufficient clinical competency within primary healthcare institutions. On one hand, tool-based mobile applications can effectively compensate for deficiencies in grassroots medical informatization through features such as mobile electronic health records (EHRs). On the other hand, these applications facilitate connectivity with high-quality medical resources and provide professional support, thereby effectively offsetting limitations in physicians’ individual clinical capabilities.

It can be concluded that physician-facing utility apps in China have already achieved deep integration with medical service scenarios. Whether for physicians at tertiary hospitals or those at primary care institutions, these utility apps can effectively help them improve work efficiency and professional capabilities.

Furthermore, we believe that the discrepancy between the hospital distribution of physicians using utility apps and the overall hospital distribution of physicians in China indicates substantial untapped market potential for such apps, pointing to significant future growth. As user penetration deepens, these two distribution ratios will gradually converge.

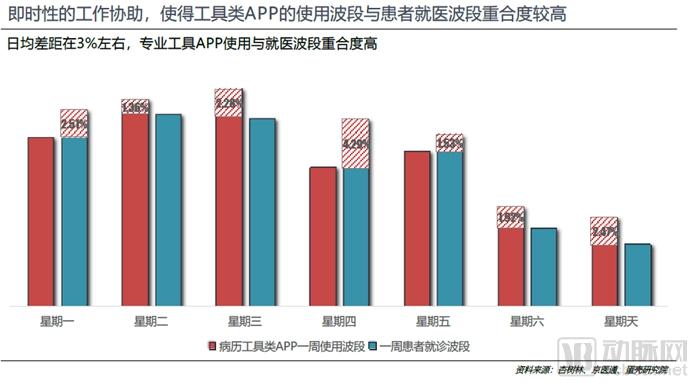

We analyzed the distribution of daily app access times by users of Xingshulin’s Medical Record Folder over the course of a week and compared it with the weekly distribution of patient healthcare-seeking times reported in the “2017 Jingyitong Healthcare Data Report.” We found that the two curves overlapped closely.

For example, on Xingshulin, user visits peak from Monday to Wednesday, accounting for 55% of the total weekly visits. Meanwhile, the “2017 Jingyi Tong Medical Care Data Report” shows that patient visits are also highest from Monday to Wednesday, representing 54% of the total weekly medical consultations.

This means that the greater the patient volume, the higher the utilization of utility-based apps. These apps effectively help physicians enhance the efficiency and capacity of patient care. Furthermore, owing to the benefits derived from these tools, physicians who have adopted them have developed a habit of sustained use.

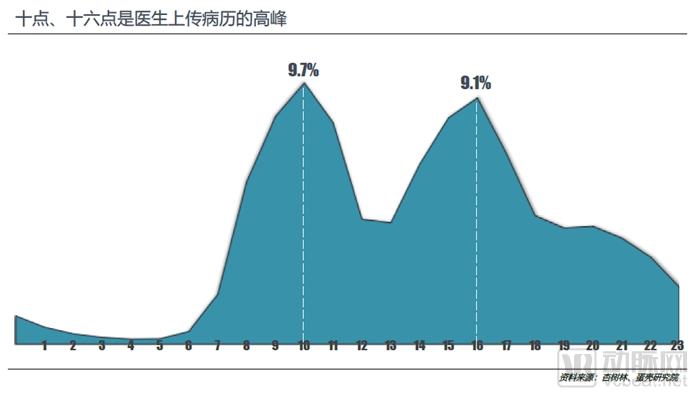

Medical record folders can upload medical record data in real time. The peak hours for doctors to upload medical record data are 10:00 and 16:00, accounting for 9.7% and 9.1% of the total daily medical records, respectively.

Although medical records uploaded between 8:00 AM and 6:00 PM account for 77% of the total daily uploads, the volume of uploads from 6:00 PM to midnight remains high. On one hand, many doctors work more than eight hours a day, which is a significant factor contributing to the sustained high upload volume. On the other hand, some doctors choose to continue organizing medical records after work, sometimes as late as midnight. This indicates that if a utility-based app can effectively assist doctors in improving their workflow, given that they devote most of their time to work and study, the user engagement time on such an app would likely see a substantial increase.

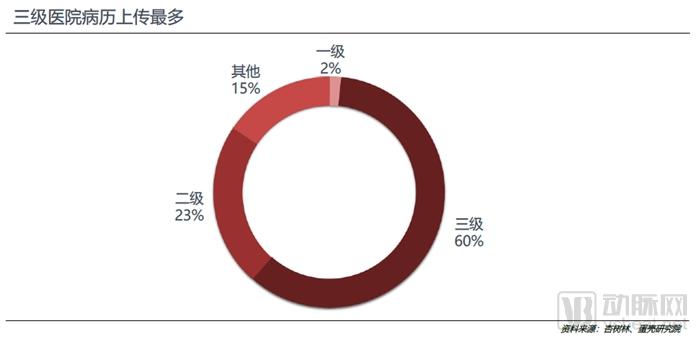

There is a significant discrepancy between the hospital sources of medical records and those of users. Medical records from tertiary hospitals account for 60% of the total case volume, whereas physicians from tertiary hospitals constitute only 38% of users of tool-based apps. In contrast, users from primary hospitals make up 30% of the user base, yet their medical records represent merely 2% of the total.

We believe that this disparity reflects the vast difference in patient volume between tertiary hospitals and primary care institutions, indirectly highlighting the imbalance in China’s healthcare resource allocation. Furthermore, physicians at primary care institutions have weaker awareness of patient record management, whereas physicians at tertiary hospitals possess higher professional competence and engage in more systematic work and learning practices, which are also significant factors contributing to this gap. How to stimulate the initiative of primary care physicians is key to determining how tool-based apps can effectively influence them.

Currently, mobile healthcare products for physicians are predominantly information-access oriented, with the number of tool-assistance products being significantly lower than that of knowledge-enhancement products.

However, in terms of specific product forms, some tool-assistance products offer functional sections such as medical knowledge, healthcare news, and online courses to enhance physicians’ expertise; meanwhile, some knowledge-enhancement products also provide functional modules, including medication assistants and clinical practice guidelines, to assist physicians in their daily work. We have compiled information on selected physician-facing mobile health products available in the market, as detailed below:

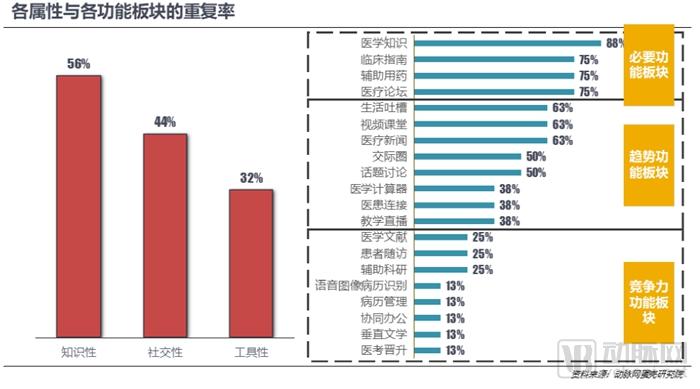

As is evident from the table above, mobile health products for physicians exhibit significant differences across many application modules. To further delineate these differences, we categorize the functionalities of mobile health into three attributes: “knowledge-based,” “social,” and “utility-based.” These three attributes encompass nearly all functionalities available in current mobile health products on the market. To better investigate how each functional module delivers services to physicians, we selected eight influential apps currently on the market and decomposed their application functionalities into 20 functional modules based on the knowledge-based, social, and utility-based attributes.

How to Evaluate the Homogenization of Various Products? We Believe It Can Be Assessed Based on the Repetition Rate of Each Functional Module, Namely:

Product knowledge sections suffer from severe homogenization, while social and utility features carry the product’s distinctive characteristics.

Among the eight representative products surveyed, knowledge-based features exhibited the highest redundancy rate, with a 56% overlap across various functional modules. This implies that each product on the market contains an average of 0.56 × 6 knowledge-based functional modules, indicating that:

1. Such features are low-cost to implement and are essential for mobile health products.

2. The pursuit of knowledge is the core need currently expressed by physicians. On average, physician-facing mobile health products on the market feature 3.36 functional modules, indicating that this need has been well met. In the future, products that merely satisfy physicians’ access to medical knowledge and consultations will struggle to capture market growth opportunities.

3. Information Overload: Currently, most physicians have multiple apps on their smartphones, with each app delivering knowledge through an average of 3.36 functional modules. Therefore, achieving rapid and efficient knowledge dissemination while enhancing the intrinsic value of information has become particularly critical. The core development focus for this attribute lies in strengthening its “pragmatic” dimension—specifically, by improving the practicality of knowledge content and optimizing product design and user experience.

Low social and instrumental coverage, in a sense, foreshadows the key to the product’s future success:

1. At the level of knowledge dissemination, while retaining the traditional unidirectional model of knowledge transmission, active topic discussions are leveraged to enable interactive knowledge acquisition and expression among users.

2. The product addresses users' social needs by providing modules such as social circles and lifestyle venting, thereby enhancing user engagement.

3. The “instrumental” attribute exhibits the lowest degree of functional module redundancy. Products can integrate selected functional modules under this attribute to enhance their utility and distinctiveness, thereby achieving deeper integration with medical services.

4. Professional utility apps centered on functionality exhibit lower homogeneity and stronger professionalism, offering more direct developmental advantages in the future.

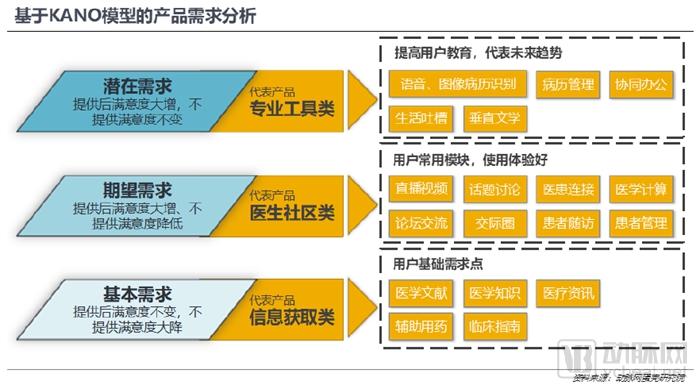

The Kano Model is frequently employed to analyze the classification and prioritization of user requirements. Based on how user needs impact satisfaction, this model illustrates the nonlinear relationship between product performance and user satisfaction. We developed a product requirement analysis framework based on the Kano Model, incorporating the recurrence rates of various functional modules and findings from our prior survey of physicians’ needs.

In the KANO model, requirements are categorized into five types: "Basic Needs," "Performance Needs," "Excitement Needs," "Indifferent Needs," and "Reverse Needs." The latter two are not applicable to the requirement analysis of mobile healthcare products for physicians and are therefore excluded.

Basic needs are taken for granted; if a product meets such a need, user satisfaction does not increase. Conversely, if a product fails to meet this need, users generally perceive it as functionally deficient. (The presence or absence of instrumental modules affects only professional tool-oriented products, not knowledge-acquisition products.)

Since the pursuit of knowledge is a fundamental user need, the presence or absence of a “knowledge” module will impact “knowledge-acquisition” and “professional tool” products.

It comprises five functional modules: medical literature, medical knowledge, healthcare information, adjunctive medication, and clinical guidelines. These modules constitute the core functionalities of physician-facing mobile health products, and vendors should provide relatively comprehensive coverage of each section.

Expected requirements refer to features that users desire, where their presence or absence directly increases or decreases user satisfaction. Representative features include live video streaming, topic discussions, doctor-patient connectivity, medical calculations, forum interactions, social circles, patient follow-ups, and patient management. These features represent key directions for current product upgrades.

The latent needs module refers to features that users are unaware of; if these features are not provided, users will not notice their absence, but their inclusion significantly enhances user satisfaction. These features include voice recognition, image-based medical record recognition, medical record management, collaborative office tools, lifestyle venting, and vertical-specific literature.

The above is part of the content of this report. To view the full version, please go to the Reports section to download it.