Rock Health Q3 2018 Digital Health Funding Report: $3.3B Raised Across 93 Deals, On-Demand Care Leads Investment

Rock Health, founded in 2010, primarily invests in startups operating in the digital health sector and provides them with capital, medical expertise, risk management, legal services, corporate partnerships, and office space.

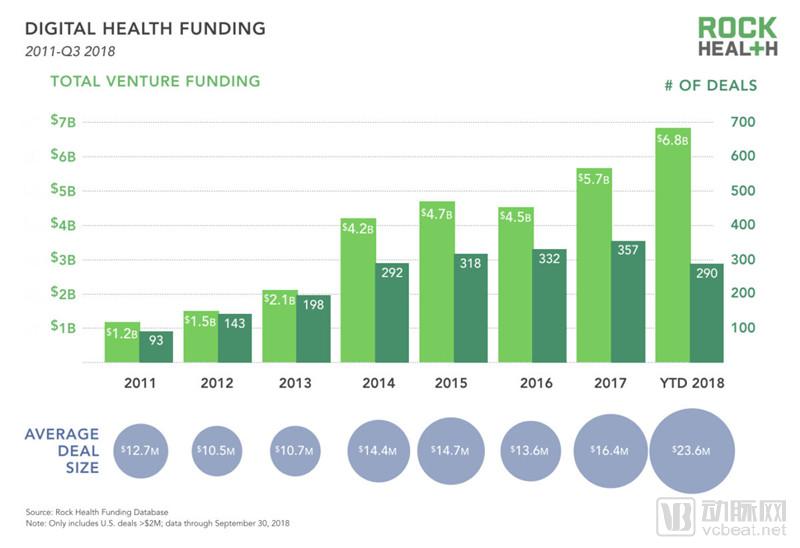

Rock Health’s recently released report on digital health industry financing for the third quarter of 2018 shows that capital interest in the digital health sector remained strong, with total funding reaching $3.3 billion in Q3 2018. This surge in quarterly funding brought the year-to-date total (as of September 30, 2018) to $6.8 billion, exceeding the full-year total from the previous year by more than $1 billion.

Below is Rock Health’s complete quarterly summary of the digital health investment market. VCBeat (WeChat ID: vcbeat) has compiled the main content of this report for you.

The third quarter of 2018 was the peak period for financing in the digital health sector. The pace of funding for individual startups indicates that this is a founder’s market, where entrepreneurs are securing larger rounds of financing with increasing frequency. The following are the highlights from the report:

1. As of 2018, 31 companies have received FDA digital health clearance;

2. Among the investors supporting digital health companies this year, the majority (59%) were repeat investors in the digital health sector;

3. There are currently more ongoing transactions than ever before, indicating that an increasing number of investors are allocating greater resources to digital health.

Q3 has surpassed 2017, making it the biggest year for venture capital investment in the digital health sector to date.

In the third quarter of 2018, digital health startups raised a total of $3.3 billion through 93 transactions, bringing the year-to-date funding total (as of September 30) to $6.8 billion. Even excluding the fourth quarter, the total funding amount for 2018 has already surpassed the $5.7 billion raised in 2017.

Notably, the average transaction value in 2018 surged to $23.6 million. Even after excluding six large transactions exceeding $200 million, the average deal size ($17.6 million) remained higher than the previous year’s $16.4 million.

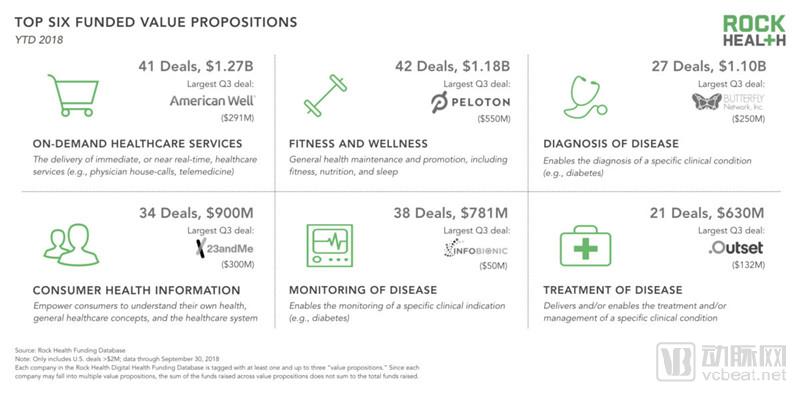

To date, ten companies have completed mega-deals exceeding $100 million in 2018: Livongo ($105 million), Collective Health ($110 million), Tempus ($110 million), Outset Medical ($132 million), Helix ($200 million), HeartFlow ($240 million), Butterfly Network ($250 million), American Well ($291 million), 23andMe ($300 million), and Peloton Interactive ($550 million).

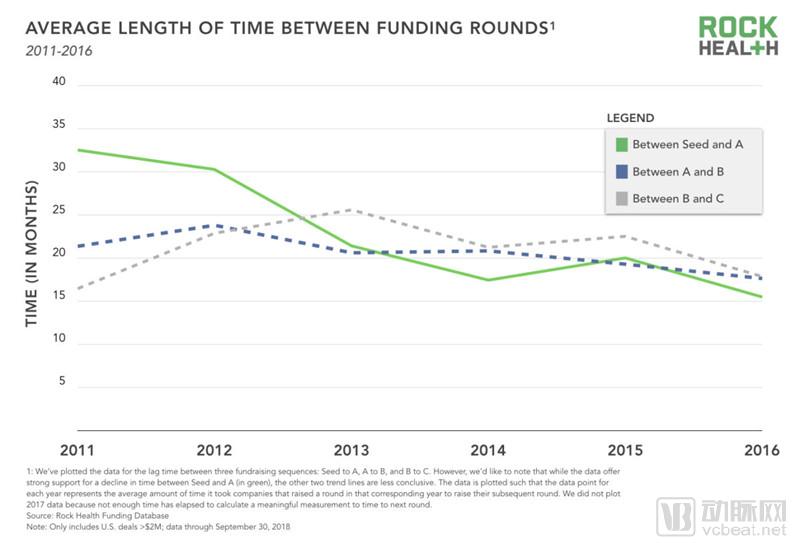

The average financing interval for corporate fundraising has steadily shortened.

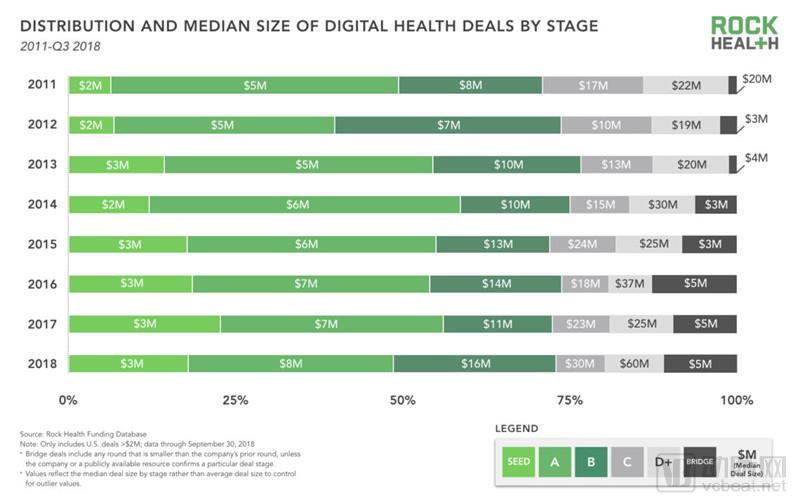

Currently, many signs indicate that the digital health market is in a strong funding position.

Digital health companies are not only raising more capital, but they are also securing consecutive rounds of funding at an unprecedented pace, particularly from seed to Series A. Over the past few years, the average interval between financing rounds has been steadily shortening. For instance, a company that began its seed round fundraising in 2013 took 21 months to close its Series A. In contrast, a company that raised its seed round in 2016 could complete its Series A within 15.5 months.

Investors Support China's Healthcare Reform

In the first three quarters of 2018, companies whose primary value proposition was on-demand medical services attracted the most financing. Among these, the largest deal in the third quarter was American Well ($291 million), which was one of the ten mega-deals year to date.

This category primarily comprises companies that deliver various real-time services through multiple channels. Examples include Doctor on Demand, a platform enabling patients to have video consultations with licensed physicians; Honor, an online platform for premium in-home elderly care; NowRx, which provides on-demand prescription delivery services; and Nurx, a telehealth platform offering remote prescriptions for contraception and HIV pre-exposure prophylaxis (PrEP), as well as at-home testing kits.

Digital therapy developers have also raised substantial funding this year, including Pear Therapeutics ($46 million), Click Therapeutics ($17 million), Akili Interactive Labs ($68 million), Virta Health ($45 million), Propeller Health ($20 million), and Hinge Health ($26 million).

Committed toCompanies Transforming Healthcare Service Delivery Models Raised the Most Funding, enabling patients to manage their health conditions at home. While consumers still require face-to-face physician-patient relationships, there is growing attention toward companies that connect patients (and patient data) with physicians and deliver care in a more continuous and convenient manner.

Investors are expanding strategic partnerships

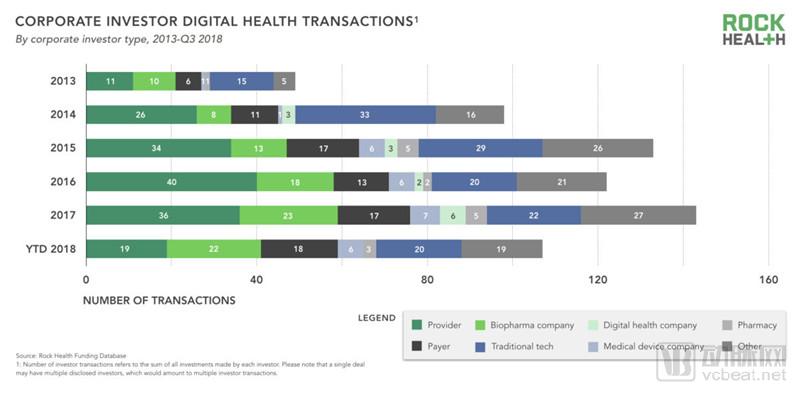

Independent venture capital funds remain the primary investors in the digital health sector, accounting for 63% of publicly disclosed investment deals in 2018. As part of broader collaborative strategies, many investment firms are investing in digital health companies. The following are some notable strategic investments made in 2018:

This July, GSK invested $300 million in 23andMe. In return, 23andMe granted GSK exclusive rights to mine its data for drug target identification. Of 23andMe’s 5 million users, approximately 80% have opted to share their data for research purposes. Their survey responses on health and lifestyle habits help elucidate potential gene-environment interactions, which may reveal novel drug targets. Both parties also identified Parkinson’s disease as a key area of focus.

Abbott and Bigfoot Biomedical began their partnership last year to integrate Abbott’s FreeStyle Libre continuous glucose monitor with Bigfoot Biomedical’s insulin delivery system. This year, Abbott participated in Bigfoot Biomedical’s $55 million Series B financing round, which will help the company build a diabetes management platform that connects insulin pens, insulin pumps, and glucose monitors to smartphones.

In 2017, Cigna led a $50 million investment round in Omada Health and expanded its commercial partnership in the third quarter of this year. It will provide Omada Health’s solutions to customers at higher risk for chronic conditions such as early-stage diabetes, heart disease, and hypertension.

OSF Ventures participated in a recent funding round for Level Ex, a company that provides applications enabling physicians to conduct remote diagnosis and treatment of patients. In addition to OSF clinicians who already utilize Level Ex’s existing applications, OSF aims to identify further opportunities for digital medical education and training.

Overall, venture capital investors completed a total of 102 deals by 2018. Biopharmaceutical companies and technology firms (such as the Amazon Alexa Fund, Baidu Ventures, GV, and Comcast Ventures) each accounted for nearly 20% of these transactions.

Major Tech Companies Continue to Expand into the Healthcare Sector

In the first half of this year, Amazon intensified its investment in its PBM strategy by acquiring PillPack, a move that sent shockwaves through the entire pharmaceutical industry. A few weeks ago, Apple announced the launch of the Apple Watch Series 4, which features fall detection and is equipped with an FDA-cleared sensor capable of performing electrocardiogram (ECG) readings and detecting atrial fibrillation.

However, Apple is not the only company exploring elderly monitoring; it is reported that Google is also considering how to provide home monitoring for the elderly population, and Amazon’s Alexa has similar applications.

It remains unclear how the strategies of large technology companies will affect startups operating in these niche markets. One of Apple’s products for detecting atrial fibrillation received FDA clearance in 2014. Following Apple’s announcement, the CEO of AliveCor pointed out that Apple was “doing what we have been doing for the past seven years.”

While startups rely on proprietary algorithms, competitive pricing, and other features to maintain differentiation, large tech companies entering the remote monitoring and home care sectors will still pose formidable competition. Furthermore, the attention that big tech brings to digital health may stimulate demand, educate consumers, and expand the investor market.

The following are some niche markets to watch in the short term:

On-Demand Pharmacy:Companies such as Blink Health, NowRx, Alto, Agile Pharmacy, and TelePharm may soon compete with Amazon, while Amazon’s acquisition of PillPack has also impacted direct competitors like CVS and Walgreens, whose stock prices declined following the announcement.

Prescription-Capable Telemedicine Companies:Companies like Roman, Hims, Nurx, and Lemonaid may find that Amazon is seeking to enter the on-demand prescription market.

Home Care:Every major tech company is competing in the smart home sector, but none has emerged as a leader in applying this technology for medical purposes. As they continue to evolve, these companies will compete with various home health solutions, including remote monitoring, patient medication adherence, telemedicine, and on-demand symptom checking and triage.

However, it may be premature to overinterpret these strategic moves. In 2016, Apple acquired Gliimpse, a platform that enables consumers to manage and share their medical records. Developments two years later suggested that this acquisition allowed Apple to advance its healthcare strategy, while digital health startups such as CareCloud, Modernizing Medicine, and drchrono continued to evolve.

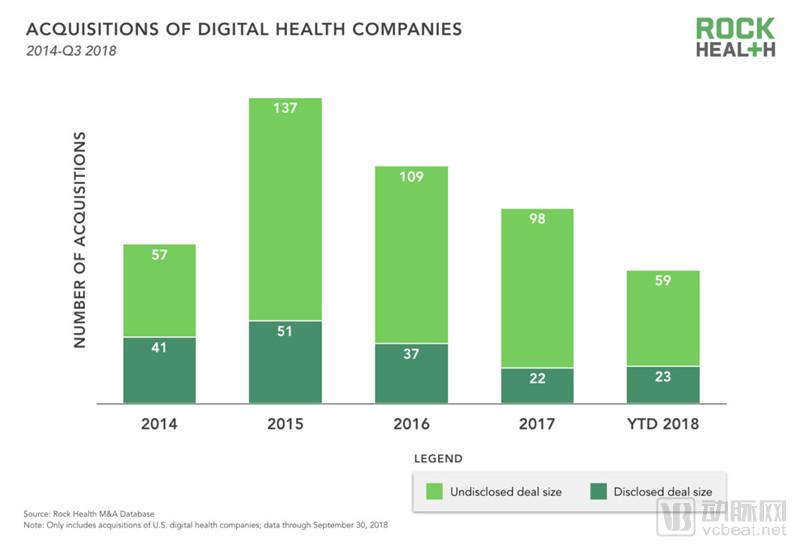

82 Digital Health Companies Acquired, Consolidation Emerges as a Visible Trend

In the first three quarters of 2018, 82 digital health companies were acquired, nearly matching the full-year total of 120 in 2017. Among these, companies focused on improving electronic health records (EHR) and clinical workflows were the most likely to be acquired.

Eleven investment firms have exited the market,IPOs remain scarce(The last digital health IPO occurred in 2016.) As discussed in our mid-2018 report, sluggish exit mechanisms are not unique to the digital health sector. Whether consolidation within the digital health industry will accelerate remains to be seen. Although a clear trend has not yet emerged, certain data indicate that this landscape is shifting, and we believe this change will accelerate over the next one to two years.

Data shows that digital healthcare companies are undoubtedly the most prolific acquirers, accounting for approximately half of all M&A transactions this year. Given ample capital and the desire to build product pipelines, attract talent, and expand their customer base, it is no surprise that the digital health sector has seen a surge in M&A activity.

In September, Welltok acquired WellPass (itself a merged entity of Sense Health and Voxiva), continuing Welltok’s acquisition spree of digital health companies such as Mindbloom and Predilytics. Given this trend, we speculate that portfolios held by private equity and growth-stage investors will at some point drive consolidation in the digital health sector, as investors seek to combine valuable, complementary offerings to deliver services at greater scale.