How Effective Is Channel Transformation Through Chronic Disease Services? A Review of 18 Listed Pharmaceutical Companies

According to data from China Industry Information Network, in 2015, the market size of chronic disease drugs in China reached RMB 732.3 billion, a year-on-year increase of 7.3%, accounting for 53.3% of the overall pharmaceutical market. In 2016, the market size for chronic disease medications expanded to RMB 794.8 billion.

For pharmaceutical companies, medications for chronic diseases are undoubtedly a “lucrative market.” In fact, beyond drug sales, pharmaceutical companies assume higher-level responsibilities in chronic disease management, including patient education, capacity-building services, and brand outreach.

With the era of pharmaceutical sales representatives becoming a thing of the past, capturing customers’ “mindshare” has become a key focus for major pharmaceutical companies. To streamline the industry chain from medications to patients—particularly for chronic diseases that require lifelong medication—pharmaceutical companies are leveraging internet technologies to build chronic disease management networks aligned with their core business lines.

Leveraging chronic disease management services to pioneer channel transformation has become a widespread consensus and common practice among pharmaceutical companies.

VCBeat (WeChat: vcbeat)An analysis of the chronic disease management strategies of 18 domestic and international pharmaceutical companies to evaluate their market performance and the effectiveness of related services.

Our key findings are:

1. Medication adherence represents a significant market opportunity for pharmaceutical companies;

2. Pharmaceutical companies have weak service capabilities; most large pharmaceutical firms that invested heavily in chronic disease management services have failed;

3. Driven by policy and market forces, pharmaceutical companies concentrated their initiatives in chronic disease management services during the two-year period from 2015 to 2016;

4. The service layout of pharmaceutical companies is usually related to their own business lines, with diabetes being a "major player";

5. More than half of pharmaceutical companies provide services through collaborations with e-commerce platforms, internet healthcare providers, and chronic disease management apps;

6. “Internet platforms, smart hardware, and offline services” rank among the top three forms of chronic disease management services provided by pharmaceutical companies.

The Core of Chronic Disease Management Lies in Patient Adherence

Overall, the market landscape is characterized by a slowdown in the growth of the pharmaceutical market and an expansion of the chronic disease management market. With the continuous advancement and deepening of healthcare system reforms, the comprehensive implementation of policies such as medical insurance payment reform, tiered diagnosis and treatment, generic drug consistency evaluation, and the separation of prescribing from dispensing has led to sustained national efforts to control drug prices. Consequently, drug prices have generally trended downward, significantly impacting all segments of the pharmaceutical industry. If the company fails to respond appropriately to drug price reduction policies and misses the market opportunities arising from lower prices and an expanded market size by effectively scaling up sales, its profitability will be adversely affected.

Therefore, pharmaceutical companies are beginning to focus on chronic disease areas that require long-term medication, leaving chronic disease management and doctor-patient education—areas outside their core competencies—to the market and new technological solutions.

The primary objectives of chronic disease management include patient education, usage guidance, physician education, user engagement, and long-term follow-up. Currently, there are three major pain points in chronic disease management:

First is the issue of physician motivation.The book The Innovator’s Prescription points out that the biggest problem with the current business model for chronic disease management is assigning doctors and hospitals to handle it. This model, shaped by long-standing practices in acute care, yields diminishing returns when applied to chronic disease management. In terms of foreign healthcare security systems, insurance covers the diagnosis and treatment of diseases but “does not pay for doctors’ earnest advice before onset.” In the process of chronic disease management, doctors do not receive corresponding compensation for providing services aimed at maintaining patient adherence. This is the primary reason for physicians’ lack of motivation in chronic disease management.

The second is the issue of compliance.China has entered a period of high burden from chronic diseases, characterized by "a large number of patients, high medical costs, long disease duration, and substantial demand for services." While chronic diseases have a prolonged course and medications can alleviate symptoms to some extent, the key lies with the patients themselves. Effective chronic disease management requires patients to establish healthy lifestyle habits, often necessitating a struggle against previous unhealthy behaviors. This process typically involves adhering to prescribed treatments and frequently monitoring and re-evaluating key health indicators. The core of chronic disease management lies in effective patient education and adherence management.

3. Payment issues.Drawing on survey data from Latitude Health in 2016, only 28% of users were willing to pay for chronic disease management, and 67% of users had a willingness to pay of less than 500 yuan per year. Due to factors such as the difficulty in evaluating the effectiveness of chronic disease management, the inability to qualify it based on acute disease treatment, the unclear direct economic link with medical insurance cost containment, and the lack of standardization in the chronic disease management market, it is difficult to include it in the reimbursement scope. Currently, the financial pressure on medical insurance is increasing, and some regions with population outflows have already experienced medical insurance deficits. With the expanding population of chronic disease patients, including chronic disease management in the scope of medical insurance payments would inevitably result in significant additional expenses. The long-term demand for medications and treatments often places a substantial economic burden on patients with chronic diseases.

Poor patient adherence, low physician management efficiency, and weak user willingness to pay have made it difficult for chronic disease management to emerge as an independent industry. Given the growth trend of chronic disease medications and pharmaceutical companies’ sales needs, pharmaceutical companies are likely the optimal “payers” for chronic disease management services.

Analysis of Pharmaceutical Companies’ Chronic Disease Service Layout: From Medications to Holistic Solutions

Below, VCBeat has compiled the chronic disease service strategies of 11 domestically listed pharmaceutical companies and seven multinational pharmaceutical companies. As the data were collected from public sources and annual reports of listed companies, only typical collaborative projects are listed.

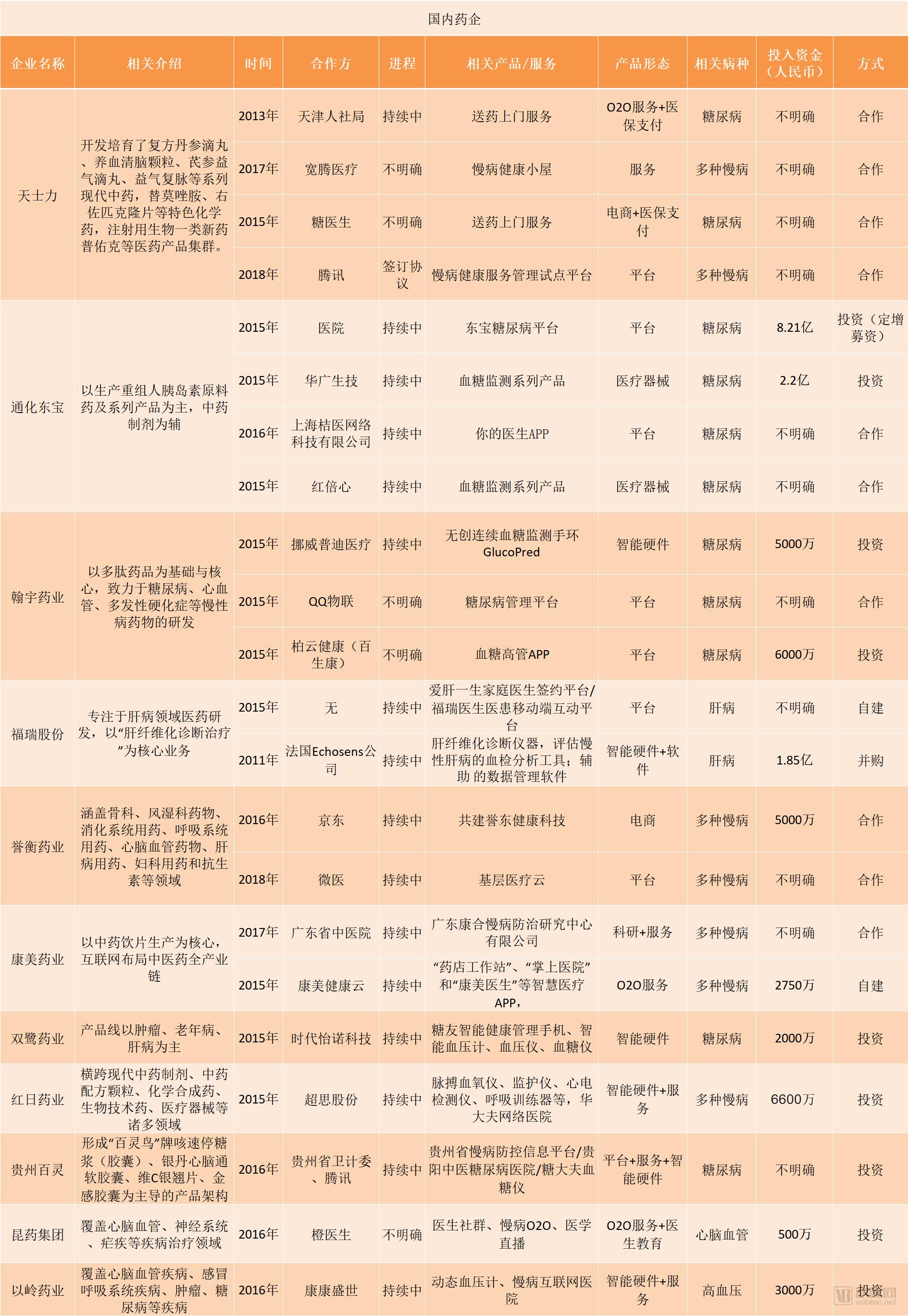

Table 1: Layout of Chronic Disease Services by Domestic Pharmaceutical Companies (Data Source: Corporate Annual Reports, Public Searches; Compiled by VCBeat)

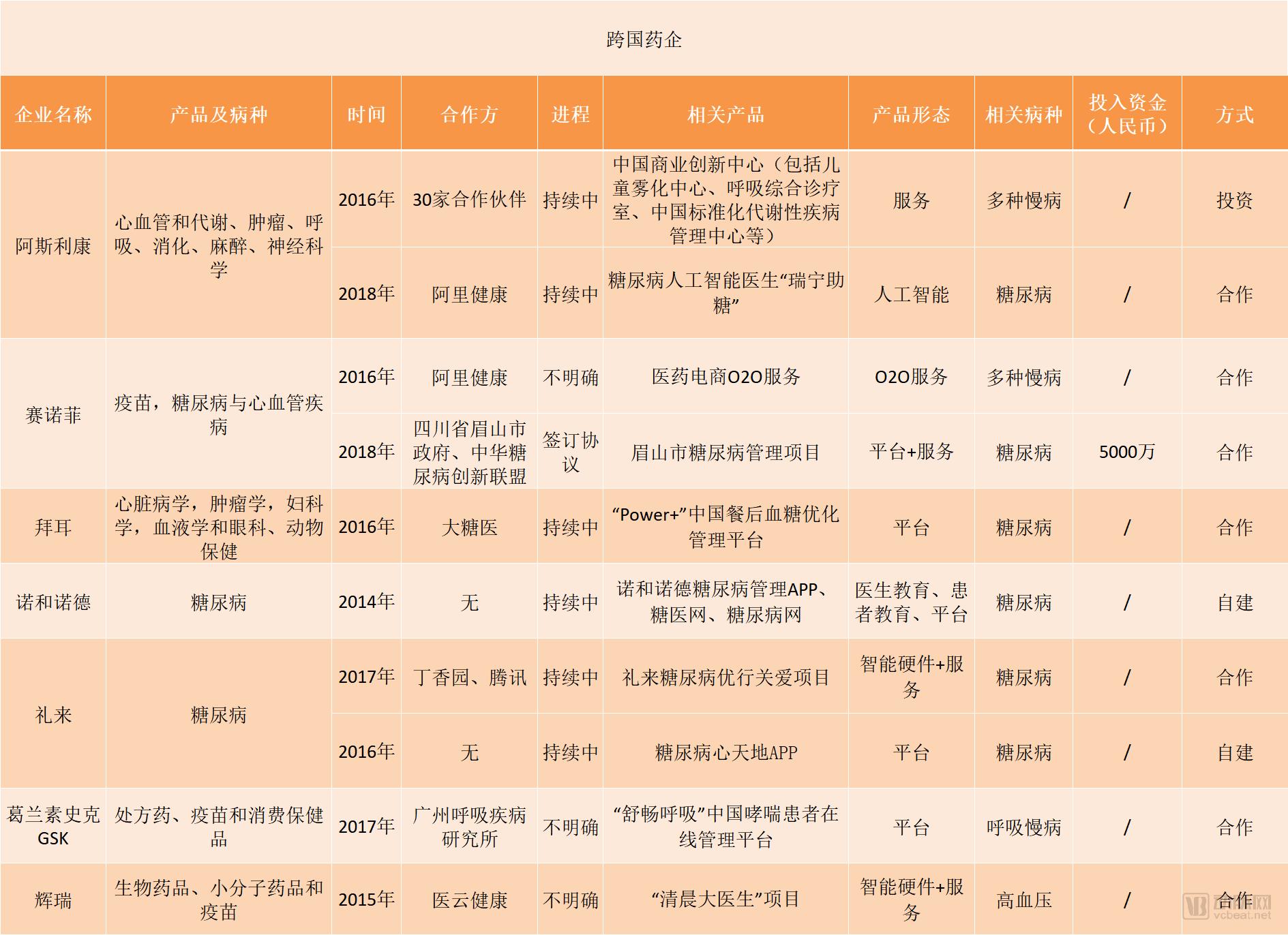

Table 2: Layout of Chronic Disease Services by Multinational Pharmaceutical Companies (Data Source: Public Search; Compiled by VCBeat)

*Note: In the table above, statistics for multinational pharmaceutical companies refer to their chronic disease management projects in China. If a project cannot be found on the official website, has low product activity, lacks updated iterations, or is only mentioned in initial cooperation announcement news, its status is considered unclear.

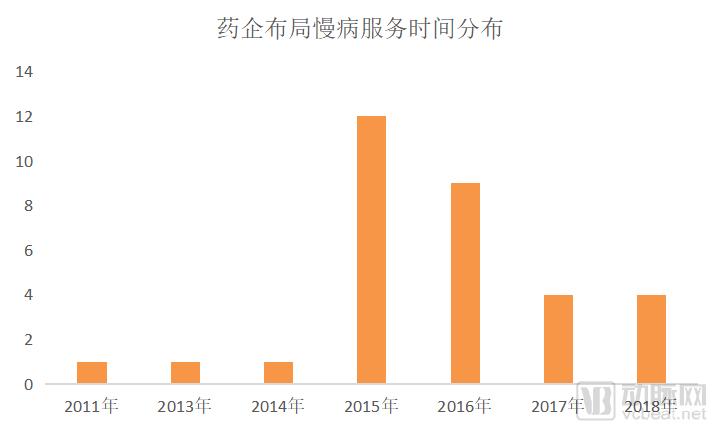

Figure 1. Distribution of Years for Chronic Disease Service Layout Projects by Pharmaceutical Companies

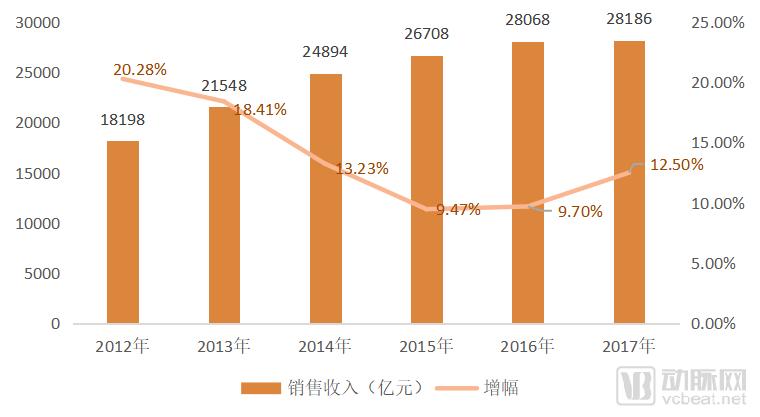

Figure 2. Sales Revenue and Growth Rate of Pharmaceutical Companies, 2012–2017 (Source: Kangmei Pharmaceutical 2017 Annual Report)

From a yearly perspective, pharmaceutical companies’ chronic disease projects have been concentrated in 2015 and thereafter. In light of the sales revenue and growth rates of pharmaceutical enterprises over the past five years, the overall trend has followed a “V-shaped” trajectory, with 2015 marking the lowest point in growth for pharmaceutical companies, representing a year-on-year decrease of approximately 4 percentage points compared to 2014.

For the pharmaceutical industry, this has been a year of turbulence. The implementation of new national tendering regulations, the introduction of drug-to-revenue ratio policies for market regulation, and the initiation of healthcare insurance payment system reforms have all converged on a single focal point: drug prices. The combined force of these policies is likely to ultimately drive a significant reduction in drug prices.

2015 was a challenging year for pharmaceutical companies, especially multinational pharmaceutical corporations. According to reports from New Kangjie, due to the pressure of bidding price caps, foreign pharmaceutical companies largely withdrew their bids in drug procurement processes in provinces such as Zhejiang, Hunan, and Fujian. Subsequently, two imported original research drugs included in the first batch of national drug pricing saw price reductions of more than 50%.

At the 2016 “Two Sessions,” “Internet + Chronic Disease Management” sparked heated discussions among deputies to the National People’s Congress and members of the Chinese People’s Political Consultative Conference. Multinational pharmaceutical giants have increasingly focused their attention on the primary battlefield of chronic disease and chronic disease management: the primary healthcare market. Investors regard chronic disease management as a gold mine within the mobile health sector. Pharmaceutical companies, medical device manufacturers, and internet firms such as BAT (Baidu, Alibaba, and Tencent) are entering this field through various models.

As shown in Table 1, pharmaceutical companies such as Hybio Pharmaceutical and Tonghua Dongbao Pharmaceutical Co., Ltd. primarily concentrated their initiatives in chronic disease management during 2015–2016, driven mainly by policy and market forces. In 2017 and 2018, internet healthcare, the primary form of medical innovation, cooled significantly compared to the previous two years. Meanwhile, chronic disease policies shifted focus toward primary care under the tiered diagnosis and treatment system. Consequently, there were fewer initiatives leveraging the internet to build chronic disease services during this period.

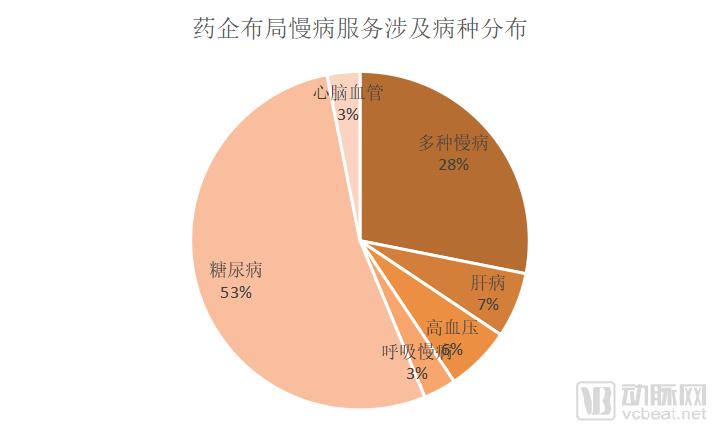

Figure 3. Distribution of Diseases Covered by Pharmaceutical Companies’ Chronic Disease Service Layouts

Insulin serves as the final line of defense in the pharmacological management of diabetes, representing an essential and irreplaceable therapy for patients in the mid-to-late stages of the disease. Prolonged poor glycemic control can lead to common complications associated with type 2 diabetes, including retinopathy, chronic renal failure, neuropathy, and cardiovascular disease. In severe cases, diabetic foot may even necessitate amputation.

Among the chronic diseases targeted by pharmaceutical companies, diabetes accounts for the largest proportion at 50%, a situation closely linked to the pain points of traditional diabetes management. Insulin is the medication most intimately associated with diabetes patients; however, conventional treatment and monitoring regimens are highly burdensome, requiring blood sampling and injections ranging from once to three or four times daily, which is profoundly counterintuitive to human nature.

According to data from sample hospitals in China, insulin accounts for 40% of diabetes medications. However, given that these sample hospitals are primarily Tier 3 Grade A hospitals located in large and medium-sized cities, where insulin usage is higher than at the primary care level, the actual proportion of insulin among diabetes medications nationwide is significantly lower than 40%. Both the “Battle of the Hundred Diabetes Drugs” around 2015 and pharmaceutical companies’ strategic investments in the diabetes sector are driven by the need for higher patient adherence among the diabetic population.

Blood glucose monitoring, medication management, and physician recommendations enhance patient visit rates and user stickiness, while also laying the foundation for the introduction of insulin products. This is likely a major reason why pharmaceutical companies are willing to pay for diabetes management services.

On the other hand, pharmaceutical companies’ strategic initiatives in diabetes are closely tied to their existing business lines. For instance, according to Tonghua Dongbao Pharmaceutical Co., Ltd.’s 2017 annual report, sales of its recombinant human insulin active pharmaceutical ingredients (APIs) accounted for over 20% of the market share, ranking second. Multinational pharmaceutical giants such as Novo Nordisk, Eli Lilly, and Sanofi have long been major players in the diabetes drug market. A 2015 Mobihealthnews report stated: “Getting patients to take their prescribed medications could help the healthcare system save nearly $290 billion, which also implies increased sales volumes for pharmaceutical companies.” Dr. Eric Topol, a cardiologist at Scripps Health Center and an advocate of digital health, believes that pharmaceutical companies have largely missed the opportunities presented by medication adherence. Pharmaceutical firms frequently forfeit a portion of the market due to poor patient adherence and subsequent discontinuation of therapy. Therefore, expanding into diabetes care services represents a strategic move for pharmaceutical companies to extend their product sales value chain.

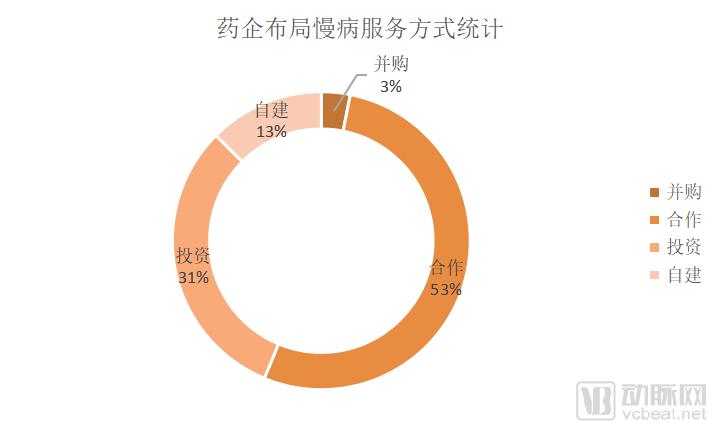

Figure 4 Distribution of Chronic Disease Service Layout Models among Pharmaceutical Companies

As shown in Figure 4, 50% of pharmaceutical companies adopt a collaborative approach to structuring their chronic disease management services. This trend is largely attributable to the frequent failures of self-operated chronic disease initiatives by pharmaceutical firms. For instance, as early as late 2015, Novo Nordisk disbanded its nationwide team of education specialists, abandoning its model of offline patient education.

Pharmaceutical companies are the closest link to patients, yet they lack strong medical service attributes. This is partly due to their “awkward identity.” If patient education is driven by sales objectives, trust between doctors and patients will inevitably be undermined; if it is completely decoupled from marketing, it becomes merely a consultation service for medicated patients, which often incurs substantial costs.

Major multinational pharmaceutical companies typically favor collaborative approaches to chronic disease management. Seven such firms, including AstraZeneca, Sanofi, and Eli Lilly, have implemented their chronic disease services in China almost exclusively through partnerships with e-commerce platforms, internet healthcare providers, and chronic disease management apps. These collaborations aim to leverage each party’s strengths to achieve a synergistic effect where “1+1>2.” For instance, Eli Lilly partnered with Tencent and DXY.cn to launch the “Eli Lilly Youxing” service. According to official data released in November 2017 from its six-month pilot operation, patients interacted with the care center team via the Youxing Care WeChat platform 200,000 times and conducted blood glucose tests 150,000 times. The proportion of patients with stable blood glucose levels increased by 15%–20%, thereby delaying the onset of complications.

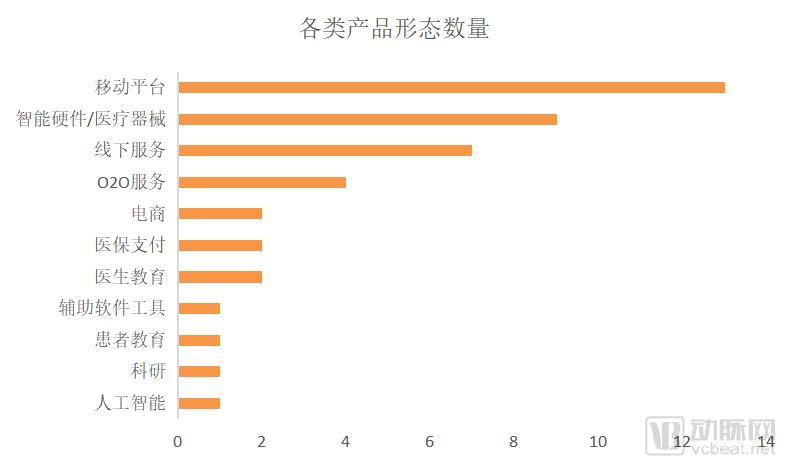

Figure 5 Distribution of Project Models in the Layout of Chronic Disease Services by Pharmaceutical Enterprises

Note: Since chronic disease services provided by pharmaceutical companies often involve overlapping models, such as “O2O services + medical insurance payment,” this statistical analysis counts each service model involved separately. For instance, if a single event involves both “O2O services” and “medical insurance payment,” it will be counted under each respective category.

Based on the above statistics, several types of partners are most favored by pharmaceutical companies:

First, the Internet platform (illustrated as a mobile platform).Among the 18 pharmaceutical companies, 12 have chronic disease management services delivered via internet-based platforms.

For pharmaceutical companies, adapting to the internet environment requires a shift in marketing strategies toward a patient-centric approach. Therefore, building mobile platforms for chronic disease management provides an additional channel for enhancing doctor-patient interaction and feedback. Meanwhile, patients’ behavioral preferences and medication habits on mobile health platforms significantly leverage the value of human-computer interaction and big data analytics, rapidly improving the efficiency and quality of services delivered to end patients.

In reality, this is also related to the dilemmas faced by mobile health. When mobile health, or internet-based healthcare, serves consumer-facing (C-end) clients, the most prominent challenges lie in data and business scenarios. From the perspective of business scenarios, providing patients with recommendations, consultations, diagnoses, and management all depend on a thorough understanding of the patients. The lack of face-to-face interaction poses significant limitations. Moreover, as the benefits of traffic dividends gradually fade, platform-based enterprises face exceedingly high costs for online customer acquisition, making it particularly difficult to precisely reach target customer segments.

Second, smart hardware.Innovations in medical devices and services driven by digital healthcare have facilitated patient self-management in chronic disease care, thereby enhancing patient adherence. For diabetes, a major disease category, the introduction of the Novo Nordisk pen marked a milestone. By enabling patients to administer their own treatment, it significantly reduced the burden on primary care and ushered in an era of patient self-management.

As the data acquisition interface for physiological indicators in patients with chronic diseases, smart hardware serves as a critical tool for treatment, monitoring, data collection, management, feedback, and reminders. It is widely applied in fields such as diabetes and cardiovascular diseases. During medical care, patients with chronic conditions often need to make repeated visits to hospitals or medical institutions to maintain stable health. Self-monitoring of key indicators via smart hardware enhances medication adherence to some extent. Furthermore, the companion apps for these devices are often the optimal platforms for patient education and interaction. Additionally, big data generated by patients represents a valuable asset for pharmaceutical companies.

Given the significant challenges in data collection during the post-discharge follow-up phase and the scarcity of CFDA-certified smart hardware capable of directly applying data to clinical diagnosis, investing in certified smart hardware represents a promising business opportunity for pharmaceutical companies.

Third, offline services。Offline services primarily consist of home medication delivery and O2O services. Chronic disease management cannot be effectively achieved through online channels alone, as digital platforms fail to address critical issues such as patient adherence and the integration of treatment with exercise.

Wen Xiaoling, General Manager of Juzhi Chronic Disease Health Management Co., Ltd. (formerly General Manager of Tasly Group’s E-commerce Company), has publicly stated that “payers will determine the future trends of the pharmaceutical industry.” Currently, two key players among payers are medical insurance and the pharmaceutical industry. In 2011, Tasly partnered with the Tianjin Municipal Human Resources and Social Security Bureau on a home-delivery medication project, which integrated the entire chain from patient order placement to drug delivery and medical insurance payment. This initiative pioneered the optimization of the full process for online prescription drug sales and introduced health screening services at pharmacies to enable precision marketing of pharmaceutical products.

In an era when the dividends of online channels have gradually faded,O2O (Online to Offline) Will Evolve into OMO (Online Merge Offline)The integration of online and offline supply and services has undergone earth-shaking changes. The only constant is the commitment to meeting patients’ needs—particularly their need for convenience—more effectively and efficiently. Future chronic disease management will likely adopt a hybrid online-offline model, with online platforms serving as tools for patient education, adherence monitoring, and communication between providers and patients, thereby complementing offline services.

Drug Sales + Chronic Disease Management: How Effective Is It?

iResearch Analysis believes that a complete closed-loop chronic disease management system mainly consists of five key players: mobile healthcare providers, physicians, medical and health institutions, pharmaceutical companies, and insurers, who collaborate to serve patients with chronic diseases. It is generally believed that internet healthcare companies and medical information technology firms are the primary drivers of healthcare transformation. However, in a market segmented by demand, pharmaceutical companies, whose core business is drug sales, are actually the type of enterprise with the broadest reach to the demand side, namely, patients.

Let us examine the effectiveness of pharmaceutical companies’ strategic layouts in chronic disease management through the following two cases:

Tasly Pharmaceutical: Bridging the Patient-Drug-Insurance Payment Loop, Gains 100,000 Diabetes Members

In September 2013, Tianjin launched a medication service program for outpatients with diabetes covered under special disease insurance. This initiative enables diabetic patients aged 60 and above to enjoy the convenience of online pharmaceutical purchasing and home delivery without leaving their homes, while also benefiting from existing medical insurance reimbursement policies. Tasly Pharmaceutical serves as the provider of information network technology and the service provider for medication ordering and distribution.

According to Tasly Pharmaceutical’s 2017 annual report, its chronic disease management platform for diabetes had cumulatively enrolled nearly 100,000 patients. In 2017, the platform achieved sales revenue of RMB 345 million, representing a 53% year-on-year increase from 2016, and a tenfold growth in sales over the preceding three years. Meanwhile, it helped reduce the proportion of pharmaceutical expenditures in hospitals and saved tens of millions of RMB in medical insurance spending for Tianjin Municipality.

In 2017, to enhance operational efficiency and service quality, Tasly Pharmaceutical carried out iterative upgrades across multiple dimensions, including pharmaceutical distribution, value-added services, and the introduction of big data systems.

In pharmaceutical distribution, direct integration with hospital prescriptions has enabled medicines to be delivered directly from distribution centers to patients. Meanwhile, the drug QR code traceability system has successfully addressed challenges in precise medication use and drug regulation.

Value-Added Services Segment: Centering on Tasly Pharmacy stores, the company has established multiple chronic disease health management centers to provide existing users with a range of offline services, including monitoring, screening, and pharmaceutical care. This initiative not only alleviates the inconvenience patients face with routine hospital testing but also saves Tianjin’s medical insurance fund substantial registration and consultation fees, thereby enhancing the utilization efficiency of medical insurance funds.Big Data Services Segment: The company is progressively building a chronic disease PBM (Pharmacy Benefit Management) model. By integrating with hospital HIS (Hospital Information System) platforms, it has achieved prescription circulation connectivity with over ten major diabetes hospitals in Tianjin, enabling the out-of-hospital transfer of prescriptions. Furthermore, through integration with medical insurance settlement departments, patients can now genuinely settle payments online using their medical insurance cards.

By leveraging the "Internet Plus" model and integrating online medical insurance payments with offline pharmaceutical distribution, Tasly Pharmaceutical has established a novel service model connecting patients, hospitals, and medical insurance providers. This innovation led to its Diabetes Chronic Disease Management Platform being designated as the sole pilot project in China by the Ministry of Human Resources and Social Security. Building on the platform’s successful implementation in Tianjin, Tasly is actively promoting the replication of this model across multiple provinces.

Tonghua Dongbao: Dual Strategy of Acquisitions and In-House Development Effectively Manages Over 200,000 Patients

Tonghua Dongbao’s primary product is recombinant human insulin injection (brand name: Gan Shulin). Prior to the launch of its recombinant human insulin products, 99.9% of the market share was monopolized by foreign companies. Since its market entry, Tonghua Dongbao’s recombinant human insulin has captured over 20% of the market share, ranking second.

Leveraging its own business chain, Tonghua Dongbao’s chronic diabetes management platform integrates three core components: pharmacological treatment (insulin, Ypsomed pens and needles; and future oral and other therapeutic agents), blood glucose monitoring (Bionime and the Hongbeixin app), and patient behavior management (the “Your Doctor” app). This integrated approach organically connects doctors, patients, the platform, and monetization channels (including pharmaceuticals, medical devices, and services).

By leveraging the “Your Doctor” app, developed in partnership with Shanghai Juyi Network Co., Ltd., we aim to enhance engagement between physicians and patients. Through the integration of pharmaceuticals, medical devices, and mobile internet technologies, we strive to achieve the strategic objective of “Insulin + Blood Glucose Monitoring Devices + Dongbao Diabetes Platform.”

According to the 2017 annual report, by the end of 2017, more than 9,000 frontline endocrinologists had effectively managed over 200,000 patients through this platform, with more than 750,000 patient visits benefiting from its services. On the other hand, Tonghua Dongbao Pharmaceutical Co., Ltd. drove sales growth for its human insulin products, ultra-thin wall insulin pen needles, and blood glucose monitoring test strips through a comprehensive marketing model based on chronic disease management and centered on providing holistic solutions for diabetes insulin therapy.

Figure 6. Sales of Tonghua Dongbao’s Diabetes Products in 2017 (Data Source: Tonghua Dongbao 2017 Annual Report)

Through a series of strategic service deployments, Tonghua Dongbao Pharmaceutical Co.,Ltd. has established itself as a provider of comprehensive diabetes solutions. Its chronic disease management platform, centered on “diabetes treatment, blood glucose monitoring, and patient behavior management,” has taken shape. Consequently, Tonghua Dongbao is gradually transforming from a pharmaceutical manufacturer into a holistic solution provider for insulin therapy in diabetes care.

If diabetic patients learn to monitor their blood glucose levels, take hypoglycemic medications, and administer insulin themselves, what role is left for hospital physicians? This statement encapsulates the core importance of medication adherence among patients with chronic diseases. In reality, beyond patient education, physician education also poses a significant challenge for pharmaceutical companies. Therefore, through a series of strategic service initiatives, pharmaceutical companies can collaborate with mobile platforms, smart hardware providers, and even healthcare institutions to achieve mutually beneficial outcomes.

The strengths of their own business lines help pharmaceutical companies leverage core competitive advantages during the transition toward chronic disease management and internet-based healthcare. As the ultimate goal for major pharmaceutical manufacturers is to enhance marketing and sales, internet companies, pharmaceutical firms, and clinical service providers are joining forces in their service layouts to explore more precise diagnosis and treatment as well as more effective management approaches.

Challengers in a given field may be displaced by innovative incumbent enterprises; as mobile applications prepare to disrupt the self-management of chronic diseases, they must inevitably bear the operating costs resulting from the disappearance of the internet dividend.

From another perspective, pharmaceutical companies that invest in chronic disease management services and innovate their service models effectively act as both the “egg-laying hen” and the “cooking chef,” thereby enhancing patient experience—a win-win scenario.