"AI + Medical Imaging" in 2018: The Year of Real-World Implementation – Nine Key Transformations

Winter Has Arrived, Yet Dawn Lies Ahead.

The development of artificial intelligence is evolving at a breathtaking pace, yet it remains inextricably linked to two key metrics for assessing product quality: “quality” and “demand.” From the historic man-versus-machine showdowns to the scramble for market share in hospitals, and now to the imminent commercial deployment, this sector has undergone dramatic transformations in just two short years.

Rapid development often invites skepticism, and “AI-driven innovation in medical imaging” has long been a contentious topic both within and outside the industry. Nevertheless, regardless of public opinion, AI companies have made tangible progress in implementation, with more than 1,000 tertiary Grade-A hospitals having adopted AI solutions from these enterprises.

So, in this year of coexisting opportunities and challenges, what has artificial intelligence changed? And how has artificial intelligence itself evolved?

Following the opening ceremony of RSNA 2018, Chair Vijay M. Rao, MD, stated in an interview with the Daily Bulletin: “AI and machine learning applications have effectively demonstrated their value in radiology, but we have only scratched the surface of these technologies. Current AI applications have liberated physicians from repetitive tasks, enabling them to work with greater efficiency; patients no longer face prolonged waits due to technological advancements, making the entire field of radiology more transparent.”

As Rao noted, in contrast to the hesitation displayed by physicians at last year’s RSNA, we are witnessing the most significant shift in medical AI: a change in mindset. This paradigm shift stands out as the most important development this year, driving data accumulation, innovation, and potential commercial benefits for AI. Therefore, only when physicians genuinely accept and embrace AI will AI technology move beyond the laboratory and into real-world clinical practice.

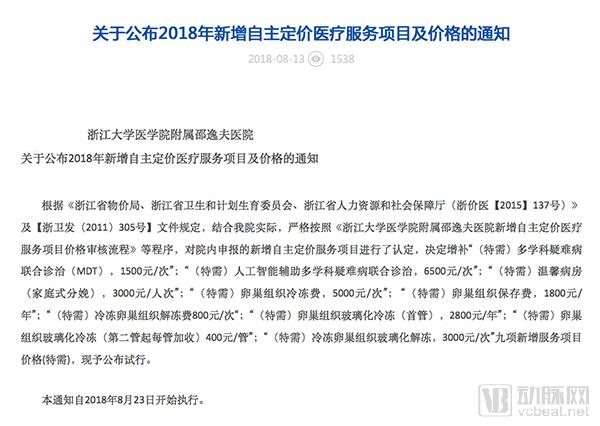

The same attitude prevails in China. In mid-August, Sir Run Run Shaw Hospital, Zhejiang University School of Medicine, took the lead in opening its fee schedule to AI-related products, specifying “(Special Needs) AI-assisted multidisciplinary joint diagnosis and treatment of complex and refractory diseases, RMB 6,500 per session.” Regions such as Qingdao and Liaoning quickly followed suit, adding certain AI services to their fee schedules. Hospitals have already made significant breakthroughs this year.

Medical imaging was not the first application scenario for AI. Many enterprises’ AI technologies originated from the transfer of computer vision techniques, which were then trained and optimized based on the characteristics of specific diseases. The advantage of transfer learning algorithms lies in enabling developers to rapidly enter the medical field, thereby accelerating the development of the medical AI industry.

This year, algorithmic changes have primarily occurred in two areas. On one hand, traditional transfer learning algorithms have been continuously optimized through data and experimentation, leading to significant improvements in metrics such as robustness and accuracy. On the other hand, some AI medical imaging companies have declined to use open-source algorithms, opting instead to develop proprietary algorithms tailored for AI medical imaging.

Both models have their own advantages, but to fully break through the bottlenecks of current AI technology, algorithms alone may not be sufficient. A holistic approach that considers other factors, such as genetics, could offer an alternative path forward.

Given the availability of public databases for pulmonary nodules and fundus images, with the pulmonary nodule databases being particularly rich and comprehensive, most AI companies currently prioritize pulmonary nodule products as their core offerings. This trend remains unchanged; what has shifted is that developers are now turning their attention to a broader range of emerging fields.

At the 2017 RSNA Annual Meeting, only a handful of companies were engaged in radiomics research; in China, Huiyi Huiying’s radiomics cloud platform was the sole representative of such efforts. This year, however, more companies have embarked on radiomics research, attempting to extract valid information from medical images through high-throughput methods.

Breast cancer has emerged as a highlight of the AI industry this year. Although it is known as the most common cancer among women, only a handful of companies launched AI products for this indication last year. In contrast, early breast cancer screening has nearly become a standard offering for every company this year, with each releasing at least one early screening product (including X-ray, ultrasound, and mammography).

Hisi’s AI for digestive endoscopy and Shukun Technology’s AI for cardiovascular care are continuously deepening their research within single clinical scenarios. Their focused approach is likely to establish robust technical barriers in an era of diverse innovation.

Furthermore, increased cross-industry integration is underway, with “AI + New Drug Development” undoubtedly being a major hotspot this year. Globally, the number of companies labeled in this niche sector has doubled. In China, XtalPi secured $46 million in Series B+ financing, Deepwise obtained $15 million in Series B financing, and AccutarBio also raised $15 million toward the end of 2017.

Additionally, NLP-based clinical decision support systems and video capture technologies are becoming increasingly mature. Tencent’s Medical AI Laboratory is at the global forefront of R&D in innovation; however, there are currently no signs of commercialization in these areas.

2018 was arguably the year when medical AI moved into practical implementation. As physicians’ mindsets shifted, they not only began adopting AI products but also gradually participated in product development and the training of AI professionals, leading to more frequent collaboration between clinicians and researchers.

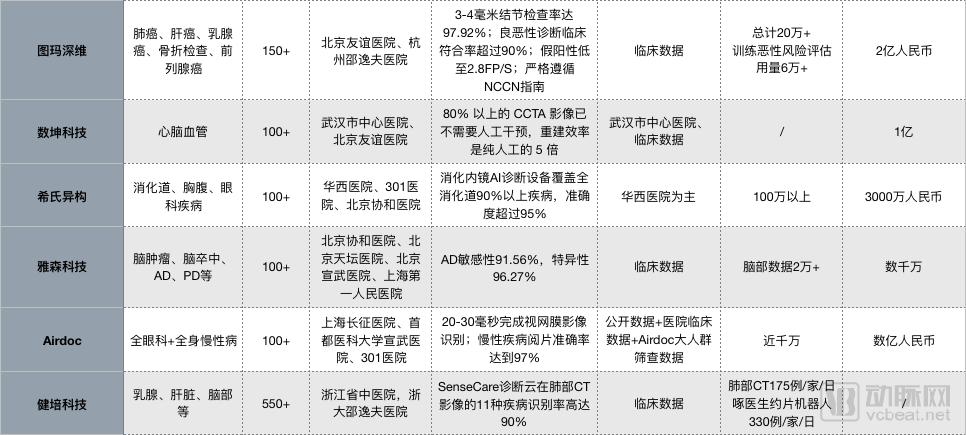

According to statistics from VCBeat, the current implementation status of major enterprises is shown in the figure below:

As shown in the figure, well-known artificial intelligence companies have demonstrated strong performance in practical implementation, with their corresponding maturity indicators continuously rising. However, what needs to be discussed next is the issue of metrics for AI products.

As the accuracy of AI algorithms continues to improve, gradually approaching perfection, this process has also introduced numerous challenges. One of the most significant issues is that, in their pursuit of higher algorithmic accuracy, some companies have seen not only an increase in precision but also a concurrent rise in false-positive rates. As one physician noted, “AI typically does not miss diagnoses for routine cases; however, when a misdiagnosis does occur, it invariably leads to serious consequences. Although some products can make basic determinations regarding whether a condition is benign or malignant, they remain far from mature.”

To address these issues and describe the state of AI development, new metrics such as hospital idle rates and report adoption rates have emerged. These metrics, in conjunction with accuracy and robustness, provide a more comprehensive reflection of the integration between AI products and physicians.

Prior to the approval of Class III medical devices, many AI products were able to obtain CFDA Class II medical device certification, a scenario that fostered the emergence of pricing models worthy of future reference.

1. Fee-for-use pricing; currently, this payment model is primarily adopted by third-party imaging centers.

2. Purchase products through outright acquisition. At this stage, hospitals are the primary adopters of this payment model.

3. Annual Fee Model. No relevant data has been collected for products currently adopting this pricing model.

Different pricing models reflect varying market demands. The pay-per-use model offers flexibility and ease of cost control, but it is not sustainable. For third-party imaging centers, an emerging sector with relatively low business volume and rapid product iteration, purchasing products through outright buyouts is excessively expensive. This approach strains corporate cash flow and fails to align with the enterprises’ image interpretation needs.

For hospitals, in the absence of cash flow pressures and with a high level of satisfaction with the product, it is clearly more profitable to purchase the product outright via full payment before its pricing matures, as the current price is inevitably significantly lower than the post-commercialization price.

Although relevant data has not yet been collected for the annual fee model, it is highly likely to become mainstream after product approval. On one hand, this operational model facilitates cost control; on the other hand, if hospitals or imaging centers are dissatisfied with a particular product, they can switch to an alternative in a timely manner.

Setting aside commercialization models, AI’s technological breakthroughs are also worth noting.

“Cell” Presents Research Findings from Chinese Team

In February, CELL featured an AI tool developed by a Chinese team. This artificial intelligence tool is capable of accurately diagnosing two major categories of diseases: ocular disorders and pneumonia. It effectively classifies images into macular degeneration and diabetic retinopathy, determining within 30 seconds whether patients require treatment, with an accuracy exceeding 95%. Furthermore, it achieves an accuracy rate of over 90% in differentiating between viral and bacterial pneumonia. The study developed an artificial intelligence system utilizing transfer learning technology.

Skin Cancer Recognition Using CNN

In a study published in *Annals of Oncology*, researchers developed a deep learning convolutional neural network (CNN) to identify skin cancer by training it on more than 100,000 images of malignant melanomas and benign nevi. The CNN missed fewer melanomas than dermatologists and had a lower rate of misdiagnosing benign lesions as malignant. This marks the first time scientists have demonstrated that a CNN, as a form of artificial intelligence or machine learning, can diagnose skin cancer more accurately than experienced dermatologists.

Stanford’s Andrew Ng Team Releases Largest Medical Imaging Dataset, Featuring 40,000 X-Ray Images of the Human Upper Extremities

Stanford University’s Andrew Ng research team has open-sourced MURA, a dataset comprising 40,000 X-ray images of the upper extremities, and utilized this dataset to train convolutional neural networks (CNNs) to detect and localize abnormalities in the X-rays. According to research, musculoskeletal disorders currently affect over 1.7 billion people worldwide, resulting in approximately 30 million emergency department visits annually. As one of the largest open-access radiology datasets, MURA facilitates the diagnosis of bone diseases in the upper extremities.

No Biopsy Needed: AI Can Predict Immunotherapy Efficacy from CT Images

A study published in *The Lancet Oncology* by Dr. Eric Deutsch’s team from France trained artificial intelligence using CT images of cancer patients, resulting in an AI platform capable of accurately predicting the efficacy of PD-1 inhibitor therapy based on patients’ CT scans. The median overall survival for patients predicted to respond favorably was 24.3 months, more than double the 11.5 months observed in those predicted to be non-responders.

Liao Hongen’s Team at Tsinghua University Publishes Series of Papers on Artificial Intelligence Imaging Genomics in IEEE Transactions on Biomedical Engineering

Professor Liao Hongen’s research group, comprising distinguished experts from the Department of Biomedical Engineering at Tsinghua University School of Medicine, utilized artificial intelligence to analyze magnetic resonance imaging (MRI) features in a large cohort of patients with brainstem gliomas. By deeply mining the associations between these imaging features and specific genes, the study not only provides clinicians with genetic diagnostic evidence but also identifies imaging and clinical parameters closely linked to genetic profiles, thereby enhancing diagnostic expertise. This series of research findings was published in IEEE Transactions on Biomedical Engineering, a prestigious journal in the field of biomedical engineering.

World’s First AI-Based Automatic Segmentation Method for Type B Aortic Dissection Developed

On April 21, Huiyi Huiying, in collaboration with the Department of Vascular Surgery of the Chinese PLA General Hospital, launched the “AORTIST 2.0: AI-Powered Cloud Platform for Aortic Research.” This marks the world’s first development of an AI-based automatic segmentation method for Type B aortic dissection, addressing three core challenges in the surgical management of this condition: precise measurement, prognosis prediction, and remote follow-up.

According to statistics from the VCBeat database, there are 244 companies worldwide applying artificial intelligence in the healthcare sector, primarily focusing on three application scenarios: medical imaging, health management, and medical record/literature analysis. Among these, 60 companies are involved in medical imaging, a figure significantly higher than that of other application scenarios. In China, 96 healthcare AI companies mainly focus on medical imaging and medical record/literature analysis, while fewer companies are engaged in hospital management, disease screening, and prediction.

From a domestic perspective, AI startups in the healthcare and medical sector have demonstrated particularly outstanding performance. In the first quarter of 2018 alone, more than 20 medical AI companies secured financing. However, as the economy cooled in the second half of the year, both the number of investments and the total investment amount declined. Nevertheless, a new wave of large-scale financing in the AI sector is anticipated before the arrival of the new year.

Top 10 AI Financing Rankings from January to September 2018

Few policies have been specifically issued for artificial intelligence (AI); instead, AI-related initiatives are generally subsumed under broader “Internet + Healthcare” policies. The Government Work Report released by the State Council in March 2018, the Action Plan for Artificial Intelligence Innovation in Higher Education Institutions issued by the Ministry of Education in April 2018, and the State Council’s Action Plan to Promote Innovation in “Internet + Healthcare” all emphasized the development of AI and the cultivation of related talent. For enterprises, however, a more critical consideration is the review of medical devices conducted by the Optoelectromechanical Laboratory of the National Institutes for Food and Drug Control (NIFDC).

Effective August 1, 2018, the new version of China’s “Medical Device Classification Catalog” officially came into force, establishing separate regulatory approval pathways for medical software as Class II and Class III medical devices.

“The Catalog” states that if diagnostic software provides diagnostic recommendations through its algorithms,This recommendation serves only as an auxiliary diagnostic aid and does not provide a direct diagnostic conclusion.Products listed in this subcatalog are regulated as Class II medical devices. However, if diagnostic software automatically identifies lesions through its algorithms and provides explicit diagnostic prompts, it carries a relatively higher risk level, and the relevant products in this subcatalog are regulated as Class III medical devices. Therefore, most of the AI products currently available should be classified as Class III medical devices.

In response to this policy, most companies in China have adopted the strategy of adding or removing diagnostic functions while simultaneously applying for Class II and Class III medical device registrations. Currently, several companies have taken the lead in obtaining Class II certificates, includingXishi Yigou, Yasen Technology, Huiyi Huiying, Deepwise Medical, TomoDeep, Infervision, Airdoc, Yitu HealthcareWell-known artificial intelligence companies are actively filing for Class III medical device approvals. Yitu Healthcare stated that its entire product portfolio is undergoing Class III certification, while Airdoc submitted China’s first server equipped with AI software pending review. However, no product has yet obtained a Class III certificate.

In accordance with the medical device registration process, a product must undergo six stages from application to final approval: product finalization, testing, clinical trials, registration submission, technical review, and administrative approval. Currently, most medical artificial intelligence products applying for Class III device certification remain at the initial stage of registration submission.

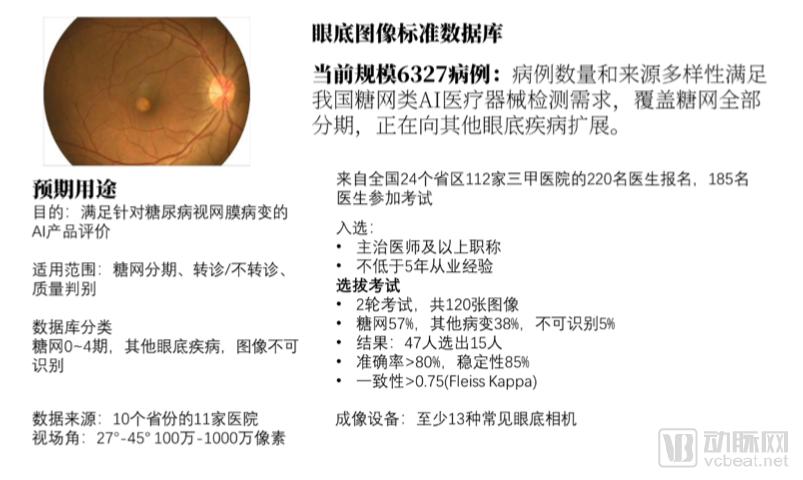

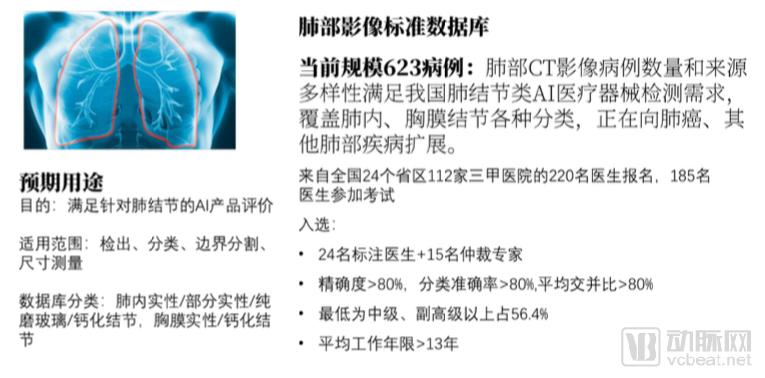

As a national technical support institution for regulatory oversight, the National Institutes for Food and Drug Control (NIFDC) has undertaken the evaluation and research of medical artificial intelligence product quality. Leveraging its extensive expertise in medical device software testing, the Optics, Mechanics, and Electronics Laboratory has established a dedicated AI team to carry out this work. As of October 2018, the standard database for fundus imaging and the pulmonary nodule database had taken preliminary shape, as detailed below:

The establishment of a standardized database for fundus imaging began relatively early, and it has now grown to include 6,327 cases.

Data sourced from VCBeat's "2018 Medical Artificial Intelligence Report"

The construction of the standard database for lung imaging was initiated in February 2018. In April, experts for pulmonary nodule image annotation were recruited nationwide. By early May, online examinations, selection, and training for these experts were completed. On June 10, the offline closed-door annotation work was finalized, with 24 annotation experts and 15 adjudication experts jointly completing the case annotations.

Data sourced from VCBeat’s “2018 Medical Artificial Intelligence Report”

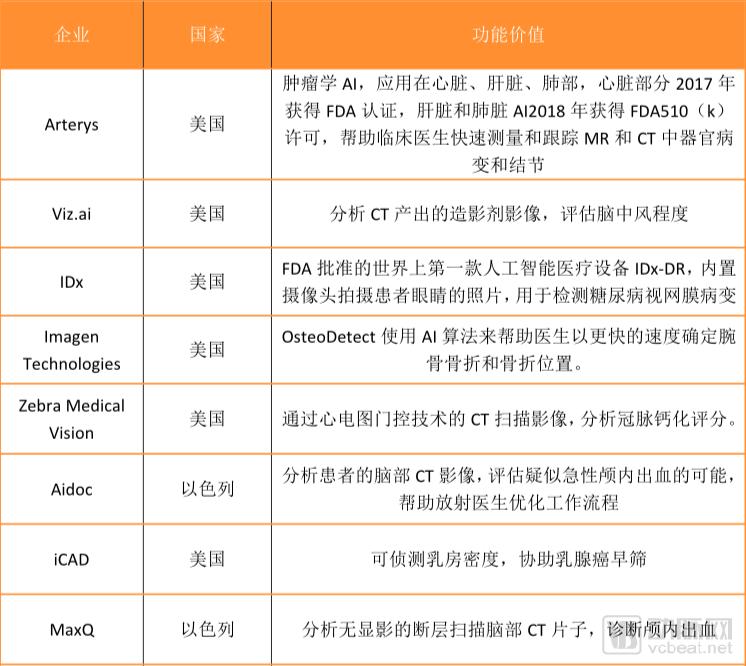

Compared with the U.S. FDA, which already has 4–6 years of experience in approving AI products, China’s National Medical Products Administration (NMPA) is relatively new. In response, many companies opt for parallel submissions to both the FDA and the NMPA. This approach allows them to draw on the FDA’s regulatory experience while also facilitating their expansion into overseas markets. Below are some companies and projects that received FDA approval in 2018, with the aim of providing additional insights for domestic companies navigating the approval process.

Some data in the charts are provided by Huiyi Huiying.

In the future, the review of digital medical products will proceed in two phases. The first phase involves establishing relevant guidelines and standards to unify inspection and testing criteria; only in the second phase will products that meet these standards be approved for market release. Some eligible products may be exempted from clinical trials.

In the field of medical artificial intelligence, Tencent regards it as a strategic initiative to strengthen its B2B pathways. In addition to the core Tencent Medical AI Lab, related entities such as Youtu Lab and AI Lab have also contributed to Tencent’s medical AI landscape. Recently, Tencent was awarded another key special project on “Research and Development of Digital Diagnostic and Therapeutic Equipment,” focusing on the development of an Artificial Intelligence-Assisted Clinical Decision Support System (AIACDSS). Through this initiative, Tencent will gain substantial training data and AI development expertise from scientific research collaborations, while Tencent Cloud will play a more profound role in the AI healthcare sector.

At the Apsara Conference in September, Alibaba’s ET Medical Brain launched its version 2.0. Jointly developed by AliHealth and Alibaba Cloud, the system inherently boasts robust computational power and diverse data advantages. Unlike Tencent, the genetic makeup of ET Medical Brain is designed to foster ecosystem development. In the future, ET Medical Brain 2.0 will concentrate its efforts on five major scenarios: clinical practice, scientific research, training and education, hospital management, and urban healthcare brain systems for smart cities.

Baidu Research Institute has released an AI algorithm named “Neural Conditional Random Fields,” which boasts powerful capabilities in detecting tumor pathology slides. Its detection accuracy even surpasses that of professional pathologists, breaking the previous highest record. This algorithm can not only make judgments on individual small images but also simulate spatial relationships between image tiles, significantly improving diagnostic accuracy and marking a breakthrough in the application of artificial intelligence in medical imaging.

Baidu holds an absolute advantage in AI technology, yet its involvement in the healthcare sector remains shallow, with its strategic presence primarily established indirectly through investments. Following its exit in 2017, healthcare-related news concerning Baidu was scarce in 2018. It was not until the Baidu World Conference in September that Robin Li announced the donation of 500 AI-powered fundus screening all-in-one machines developed by Baidu to impoverished counties, thereby forging a new positive association between Baidu and the healthcare industry.

However, Baidu’s strength is beyond doubt. Given that the vast majority of AI imaging algorithms are based on transfer learning, it would be quite easy for Baidu—which focuses on computer vision and autonomous driving technologies—to enter the medical AI sector. The key question is whether direct investment in this field is truly necessary.

In the realm of smart healthcare, following the establishment of China’s first smart hospital and the launch of “iFlytek Medical Assistant”—the first system nationwide to achieve a score of 456 on the comprehensive written examination for the National Clinical Practitioner Qualification—iFlytek has continued to strengthen its efforts in empowering physicians and facilitating the full implementation of tiered diagnosis and treatment. Significant breakthroughs have also been made in medical imaging. The iFlytek Medical Imaging Cloud Platform integrates multiple AI-assisted diagnostic technologies, such as those for CT and DR, helping physicians complete imaging diagnoses quickly and accurately while effectively reducing missed and misdiagnoses. Furthermore, by leveraging AI technology to extend high-quality medical resources to primary care settings, it enables people to access superior medical services more conveniently. Currently, iFlytek’s AI healthcare products have been deployed in 121 tertiary hospitals and nearly 2,000 primary healthcare institutions across China, cumulatively serving over 3 million patient visits.

On the global stage, numerous technology companies and medical device giants are also intensifying their efforts in the field of AI-driven healthcare. The table below highlights their advancements in AI over the past year.

AI Achievements of Tech Giants (Partial)

AI Achievements of Medical Device Giants (Partial)

2018 marked the year when artificial intelligence began to be implemented in practical applications, while 2019 will see AI gaining clearer direction on where it will be applied. Recently, iKang Guobin, a leading health management organization in China, officially launched the iKangAI+ initiative. Partner companies include Yitu Healthcare, Airdoc, iFlytek, Alibaba Health’s ET Medical Brain Laboratory, and Baiyang Smart Technology’s IBM Watson Division.

It is not only iKang and its affiliated companies; VoxelCloud, Tencent Miying, and others are also continuously moving downstream and expanding into broader application scenarios.

This marks another turning point in the downward penetration of artificial intelligence technologies. While we may see AI offering strategic insights for clinical applications in Grade 3A hospitals, achieving deep integration into the entire diagnostic workflow is likely not a target for next year under the current NMPA approval framework. Therefore, AI companies must secure business models suited to their needs at an early stage.

Another direction is collaboration with traditional medical device manufacturers, akin to the integration of smartphones and software—a win-win choice.

Ultimately, the integration of AI and medical imaging is a path guaranteed to succeed; yet in paving this way, why not embrace less hype and more grounded, pragmatic efforts?