China Surpasses US in Healthcare Investment Deal Count in Q3 2018 with Average Funding of RMB 150 Million per Round: VC Insights from the Arterys Q3 2018 Healthcare Investment Report

Legend Capital

Early-stage venture capital and growth-stage private equity investment institutions

Preface

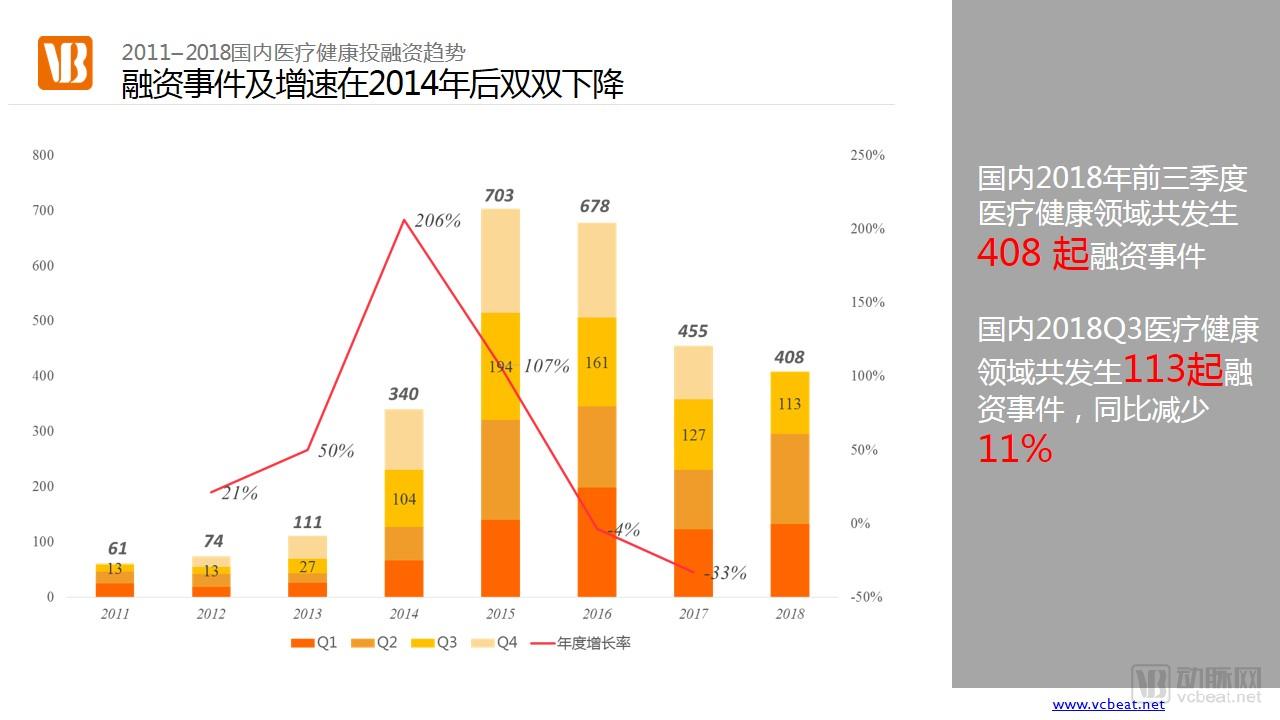

In the third quarter of 2018, China’s healthcare and medical sector saw 113 financing rounds with a total amount of RMB 17 billion, representing a 20% year-on-year increase to reach USD 2.45 billion, which accounted for approximately 29.3% of the global total.

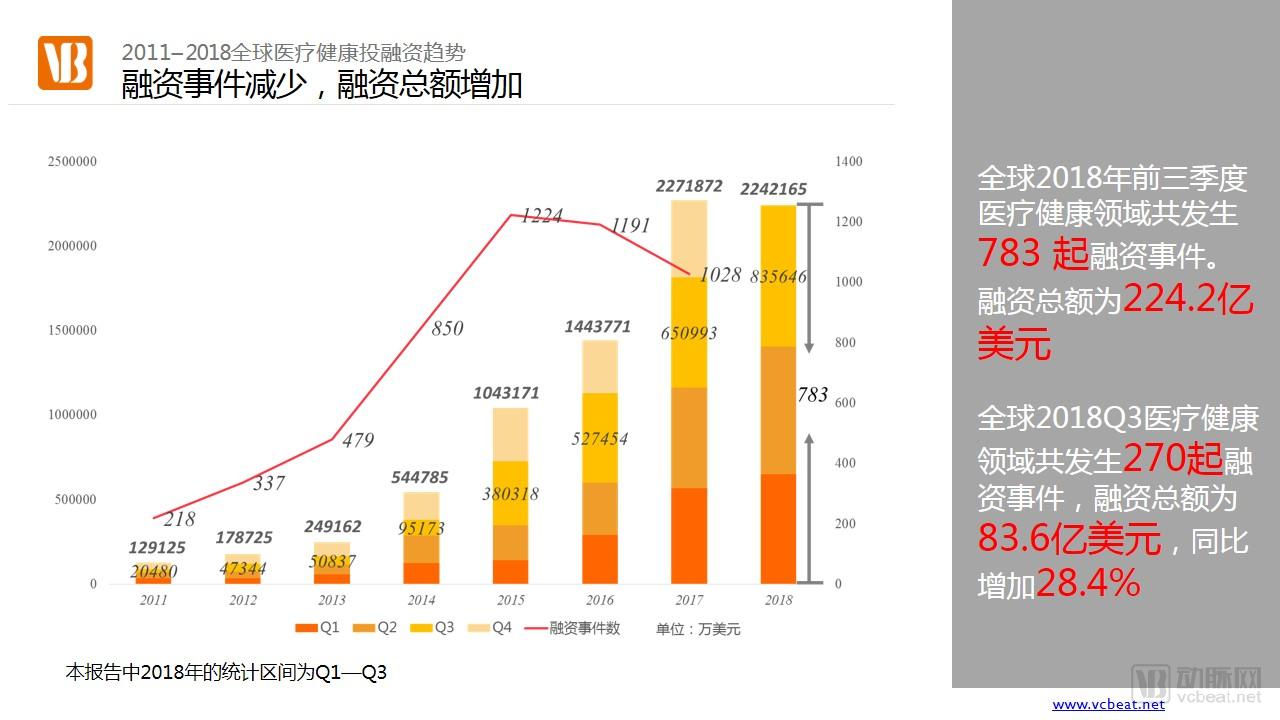

In the third quarter, global healthcare industry investment and financing reached a new high, with total funding amounting to $8.36 billion (RMB 58 billion), a year-on-year increase of 28.4%.

The above data is sourced from the “VCBeat Q3 2018 Healthcare Industry Investment and Financing Report.”

This report provides a multi-dimensional analysis of financing amounts, rounds, sectors, and geographic distribution, and offers a detailed comparison of investment and financing activities between China and the United States, aiming to comprehensively present the state of global healthcare industry financing in the third quarter.

From this, we can see many highlights, such as:

1. The amount of financing per transaction is continuously increasing, shifting from an "extensive" to an "intensive" model; in the third quarter, the average financing amount in China was RMB 150 million.

2. China’s healthcare industry has grown significantly, becoming a vital component of the global healthcare sector and attracting substantial overseas capital.

3. The United States remains the global leader in healthcare innovation, but the financing gap between China and the U.S. has further narrowed. The number of financing events in China (113) even surpassed that of the U.S. (109), although the average financing amount in China was lower than that in the U.S.

It is worth noting that, with the continuous optimization and upgrading of VCBeat’s database technology, the monitoring scope for healthcare investment and financing events now covers major countries and regions worldwide.

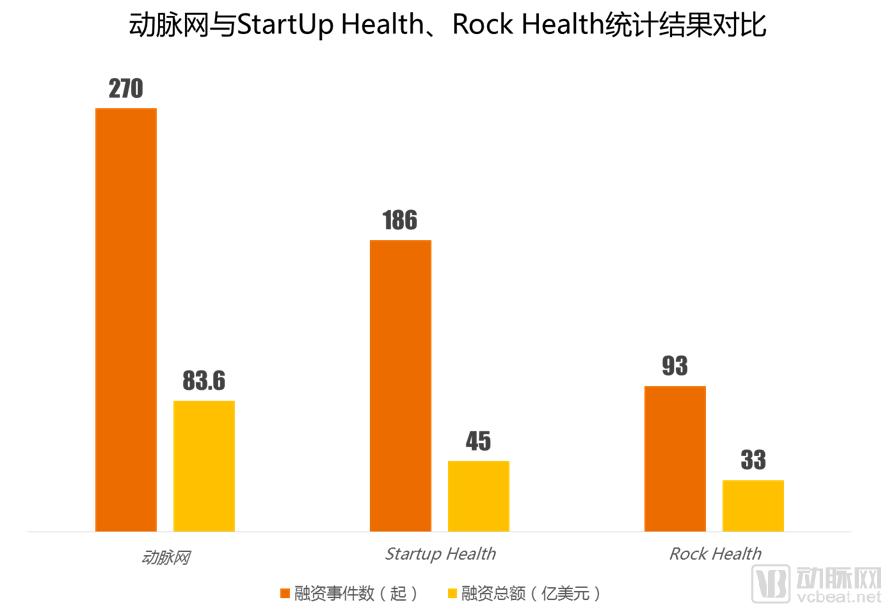

Compared with data released by globally renowned healthcare platforms StartUp Health and Rock Health, VCBeat covers a broader scope and provides more comprehensive statistics. The statistical scope of the former two is limited to digital health companies, and their coverage of Chinese companies is insufficient. In contrast, VCBeat has expanded its statistical scope to encompass the entire global healthcare industry.

Total financing reached $8.36 billion, setting the highest quarterly record in nearly eight years

The healthcare industry has become the second most popular sector for investment after TMT, with total financing continuing to maintain a growth momentum. In the third quarter of 2018, both the total financing amount and the number of financing events reached new highs, with year-on-year increases of 28.4% and 9%, respectively. Notably, the total financing amount has nearly approached the full-year total of 2017, indicating that 2018 will become the year with the highest financing for healthcare startup projects. The total financing amount in the third quarter of 2018 reached as high as $8.36 billion, setting a new quarterly record over the past eight years. On one hand, this is due to the continuous favor of capital towards the healthcare field; on the other hand, it also benefits from the expansion of the monitoring scope.

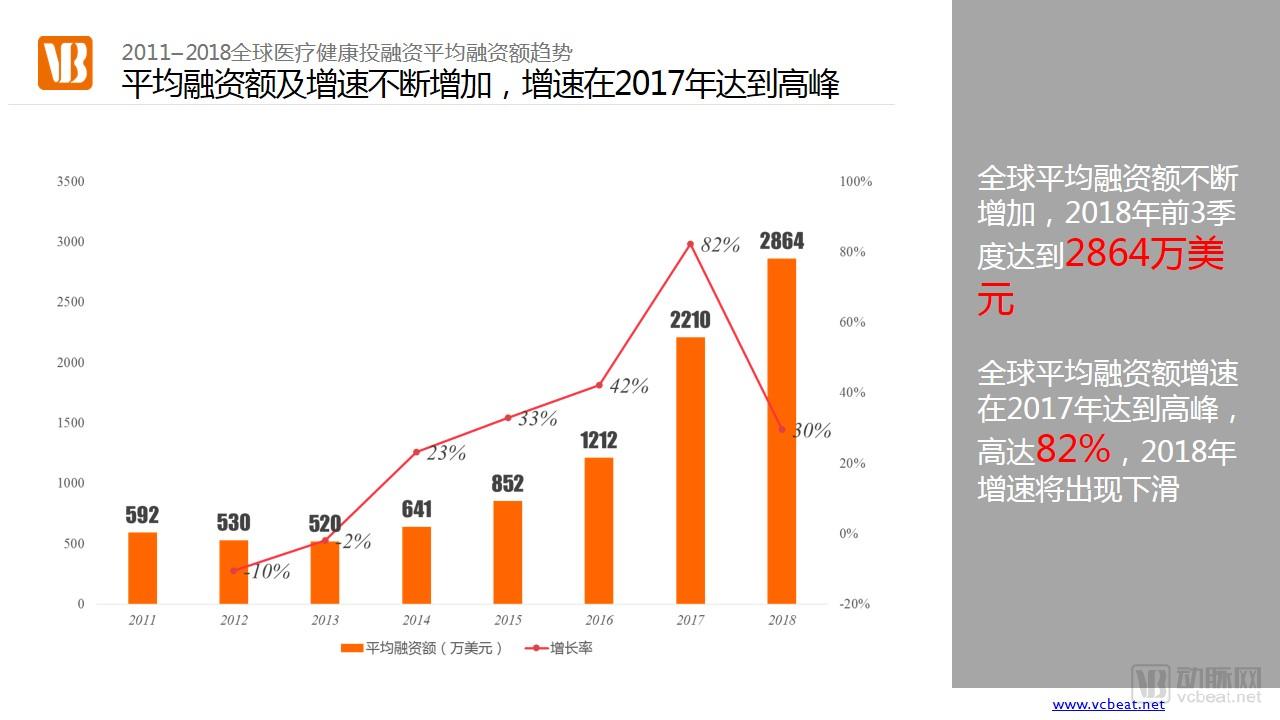

The average financing amount per project has also shown a steady growth trend, with a compound annual growth rate (CAGR) of 32.5% from 2012 to 2018, reaching an average of $28.64 million in 2018. This indicates that innovative projects in the healthcare industry are receiving increasing attention from investors. Capital allocation has shifted from an “extensive” to an “intensive” approach, enabling high-quality projects to secure larger funding rounds, thereby driving up the average financing amount.

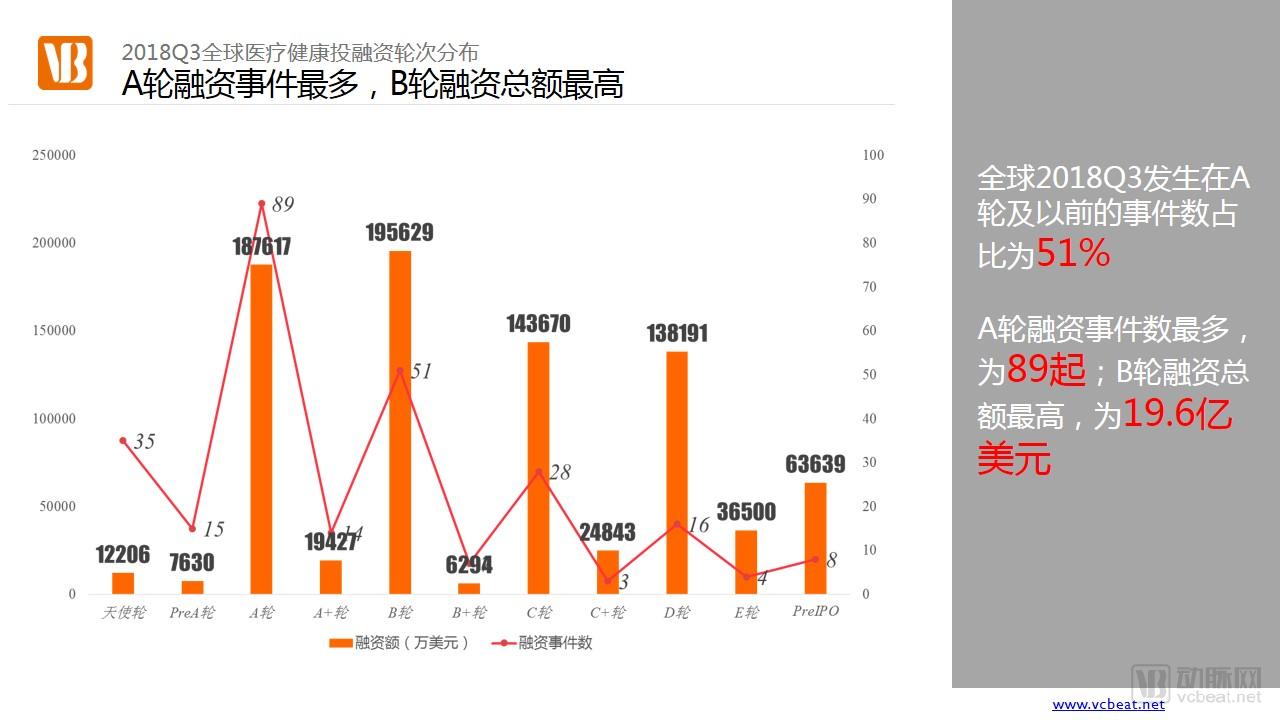

Most project financing rounds occurred at Series A or earlier, accounting for over 50%, indicating that the majority of projects are still in their early growth stage and will need to sustain continuous innovation to achieve better development.

In the Series A funding round, biotechnology company Samumed took the lead by announcing on August 7 that it had secured $438 million in financing. Its product pipeline primarily focuses on drugs for age-related diseases, with its most advanced candidates being a WNT pathway modulator for the treatment of osteoarthritis and a drug for treating hair loss. As the global population ages, market demand for the company’s products is robust, and its future development has gained strong recognition from investment institutions.

Tongrun Biopharma, also a biotechnology company, announced on July 29 that it had secured $150 million in Series A financing, jointly invested by Allient Capital, Boyu Capital, and Temasek. Tongrun Biopharma is primarily dedicated to the research and development of next-generation cancer immunotherapy drugs. The molecular candidates in its R&D pipeline are at the forefront globally, effectively addressing the limitations of existing oncology therapeutics.

In this quarter’s Series B financing round, four companies secured funding exceeding $100 million each, with two Chinese companies among them: Jianke ($130 million) and TopAlliance Biosciences ($102 million). According to Xie Fangmin, CEO of Jianke, 60% of the funds will be allocated to internet hospitals and mobile healthcare, while the remaining 40% will support pharmaceutical e-commerce, gradually realizing the company’s strategic goal of creating a closed-loop “healthcare + pharmaceuticals” full industry chain. TopAlliance Biosciences is an oncology-focused innovative drug R&D company. Currently, it has more than 10 drugs in development, including three biologics and three chemical drugs that have obtained Investigational New Drug (IND) approval for clinical trials. The proceeds from this financing round will be used to bolster drug R&D efforts, aiming to accelerate the development and market launch of novel anti-tumor therapies.

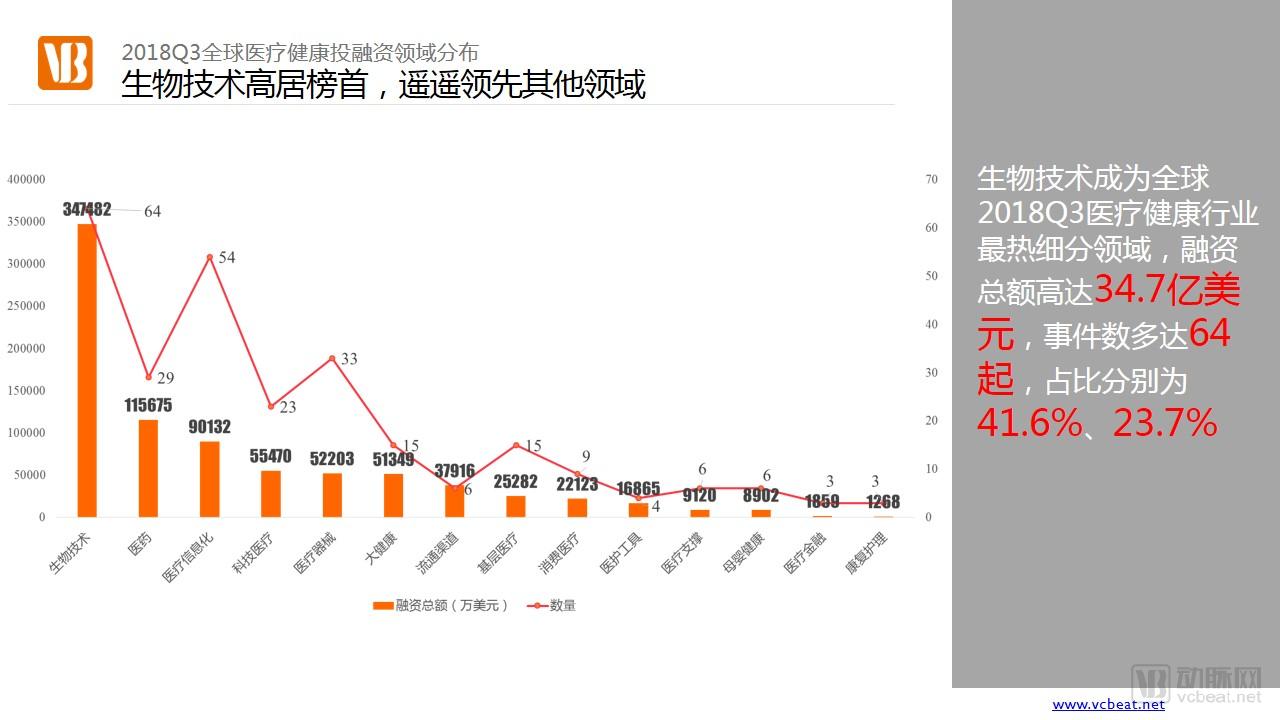

Immunotherapy and gene technology have become the typical representatives of the biotechnology sector. In the third quarter of 2018, a total of 32 immunotherapy companies and 27 gene technology companies secured financing, accounting for 92% of all biotechnology financing deals. Notable examples include BioNTech AG (Series A, $270 million), Rakuten Aspyrian (Series C, $150 million), Orchard Therapeutics (Series C, $150 million), GenCrux (Series A, $17 million), and Edigene (Series B, nearly RMB 100 million).

BioNTech AG is a German developer of biologic immunotherapeutics. Its core technologies include mRNA-based pharmaceuticals, cell and gene therapies, and protein therapeutics. The company provides services such as in vivo targeted delivery of RNA encoding proteins, T-cell genetic engineering, nanoparticle engineering, and novel small-molecule drug development. It collaborates with companies including Genentech, Eli Lilly, Sanofi, Genmab, and Bayer.

Rakuten Aspyrian leverages its unique Photoimmunotherapy technology platform to develop precision targeted cancer therapies for clinical applications.

Orchard Therapeutics has been dedicated to hematopoietic stem cell gene therapy for rare diseases, a treatment approach that involves extracting the patient’s autologous stem cells, performing genetic correction ex vivo, and then reinfusing them into the patient for therapeutic purposes.

KeRui Gene is a biotechnology company focused on the application of CRISPR (gene-editing technology). The company has established world-class gene-editing and gene-delivery platforms, specifically targeting hard-to-treat cancers and complex genetic disorders.

Hope Group focuses on integrating bioinformatics, genomics, and cutting-edge internet technology innovations. It has established a precision genomics solution centered on next-generation sequencing (NGS), third-generation sequencing, and the medical-grade GrandBox® gene analysis workstation, capable of providing precise solutions for monogenic hereditary diseases and testing services for facioscapulohumeral muscular dystrophy (FSHD).

Fewer Financing Deals in China’s Healthcare Sector, Yet Total Funding Hits Record High

As China’s healthcare industry continues to expand, it has become an integral part of the global healthcare sector. In addition to well-known domestic investment firms, it has attracted a significant influx of global capital into China.

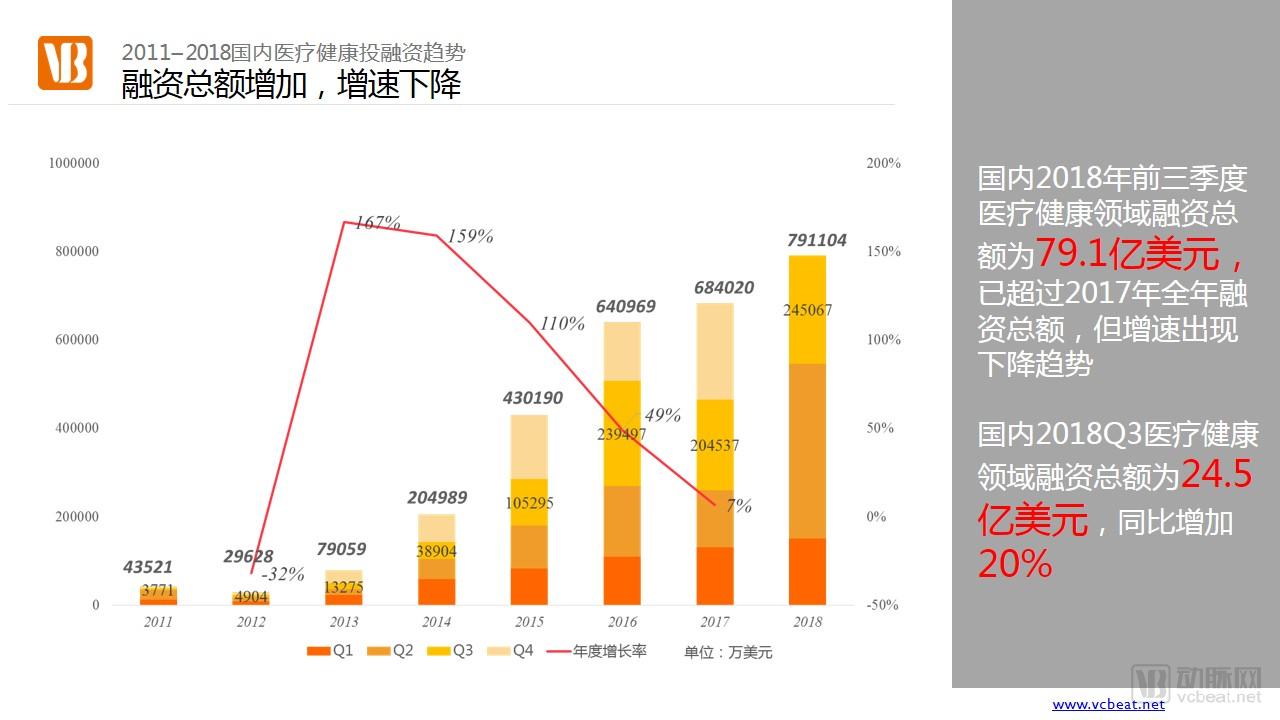

In the first three quarters of 2018, total financing in China reached as high as $7.91 billion, surpassing the full-year total of $6.84 billion in 2017. In the third quarter of 2018, although the number of financing deals remained flat compared to the same period in 2017, the total amount raised increased by 20%. This indicates that the quality of innovative projects in China’s healthcare industry is continuously improving, enabling them to attract greater capital investment.

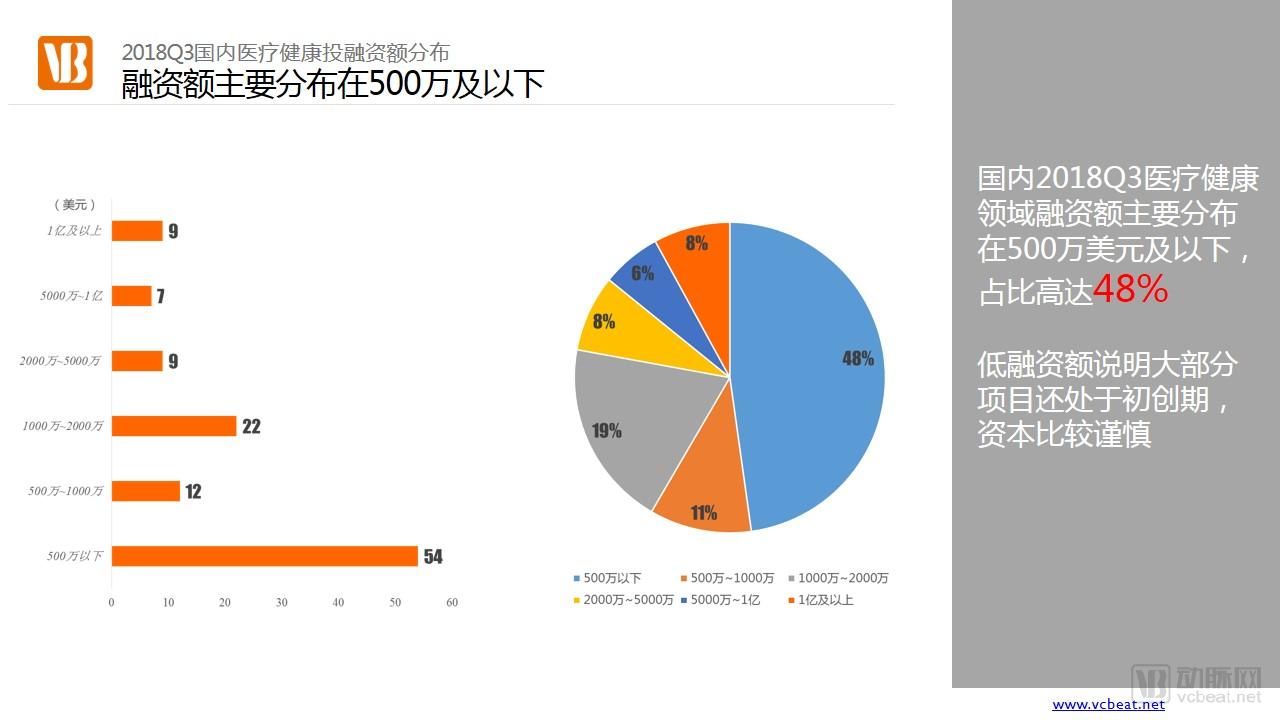

Although most financing deals this quarter were valued at $5 million or less, there was no shortage of high-quality projects reaching the hundred-million-dollar level. These include Asia Medical (strategic investment, $150 million), Tongrun Biopharma (Series B, $150 million), Medlinker (Series D, RMB 1 billion), Ascentage Pharma (Series C, RMB 1 billion), LinkDoc Technology (Series D, RMB 1 billion), Jianke (Series B, $130 million), Keep (Series D, $127 million), TopAlliance Biosciences (Series B, $102 million), and Quanyu Healthcare (Series B, RMB 700 million).

Hong Kong Asia Medical is the largest cardiovascular specialty chain group in China, with subsidiaries including Wuhan Asia Heart Hospital (one of the largest specialized heart hospitals in China), Xinjiang Yaxin Cardiovascular Disease Hospital, and Wuhan Jiangcheng Yaxin Hospital. The total number of beds across its facilities is close to 3,000.

Founded as a physician platform, Medlinker has aggregated over 500,000 real-name verified physicians and 20,000 contracted physicians. After four years of development, it has gradually formed a comprehensive ecological closed loop covering disease screening, physician education, diagnosis and treatment services, pharmaceutical distribution, financial and insurance services, and patient management services.

Ascentage Pharma is an international innovative drug R&D company based in China, which has successfully completed its product strategic layout in three major therapeutic areas: oncology, hepatitis B, and age-related diseases. The company currently has 7 products and has obtained a total of 16 clinical trial approvals. Among them, 8 clinical trial approvals were granted in China, 5 by the U.S. FDA, and 3 in Australia.

ZeroCrunch is a provider of big data solutions for oncology. Through its clinical data integration system, it helps hospitals and departments establish structured medical record databases, improving efficiency in diagnosis, follow-up, scientific research, and other processes. It has also developed structured electronic medical records covering more than 3,000 diseases, assisting physicians in clinical research and decision-making.

Among the top ten companies in Series A financing rankings, five are biotechnology firms: Keregene, BinHui Biotech, Chengyi Biopharma, Shengmei Biotech, and Rendong Medical.

Kerui Gene and Rendong Medicine primarily leverage genetic testing and gene editing technologies to provide genetic testing services and treatments for complex hereditary diseases. Binhui Biotechnology and Chengyi Biotechnology are dedicated to providing innovative products and services in the field of integrated oncology care (including diagnosis and treatment) through cellular immunotherapy technologies. Shengmei Biotechnology is a provider of tumor liquid biopsy services, equipped with Liquid Biopsy and MDA test technologies.

Similar to the global distribution of financing, healthcare IT and biotechnology have emerged as the hottest investment sectors.

Medical informatization is most prominently characterized by the development of medical big data. The government has strongly supported this initiative, successively issuing policies such as the “46312 Project,” the “Action Outline for Promoting Big Data Development,” the “Guiding Opinions on Promoting and Standardizing the Application and Development of Health and Medical Big Data,” and the “Administrative Measures for Standards, Security, and Services of National Health and Medical Big Data (Trial).” These measures provide top-level design guidance and regulation for the development of medical big data. Medical big data companies such as Clinbrain and PharmaCube secured financing in this quarter.

Biotechnology is primarily centered on cellular immunity and genetic technologies, with breakthrough progress achieved particularly in immunotherapy for tumors and in the screening and diagnosis of hereditary diseases. Biotech innovation companies represented by Quanyu Healthcare, Legend Biotech, CureGenes, and BinHui Bio have become favored by investors.

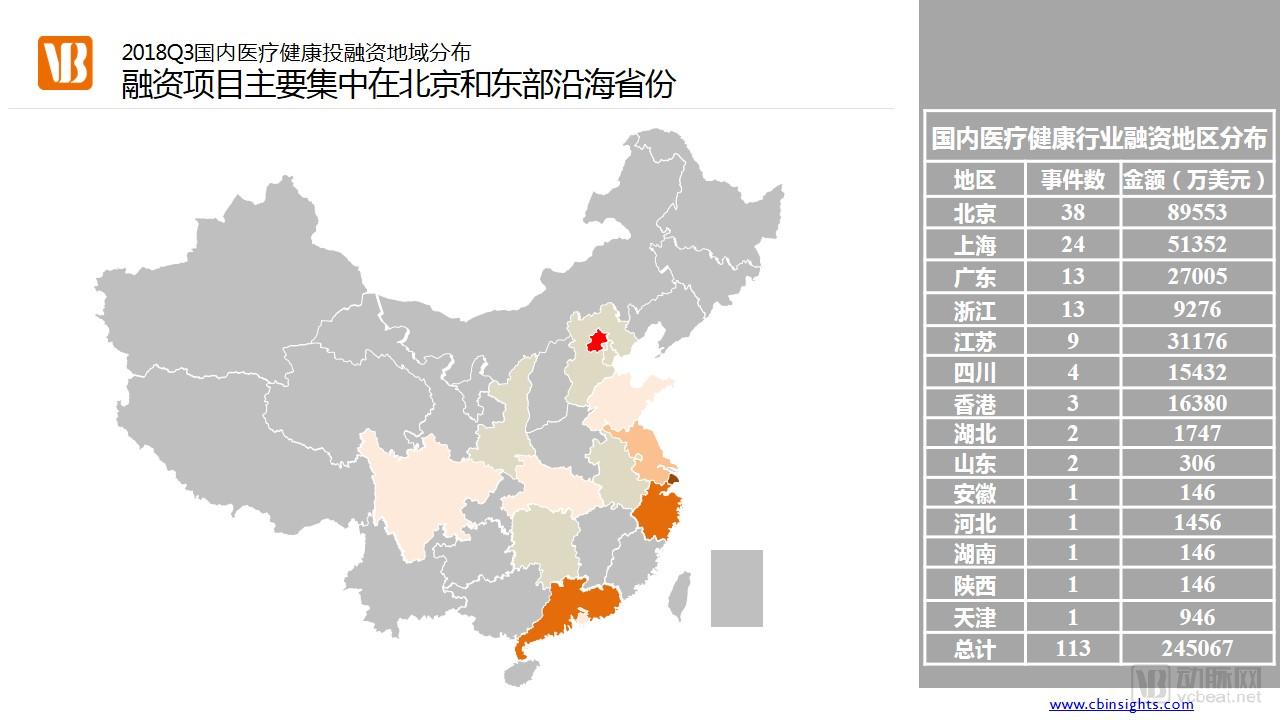

The uneven distribution of medical resources in China has led to an imbalance in the geographic distribution of healthcare startup ventures. Beijing and the eastern coastal provinces possess significant advantages in technological strength, scientific research talent, and capital volume; consequently, startups in these regions demonstrate stronger fundraising capabilities, attracting a concentration of entrepreneurs. In the third quarter, projects in the eastern region accounted for 89% of the total number of financed deals and 86% of the total financing amount.

From the perspective of project distribution, the eastern region tends to focus on technological innovation, while the central and western regions lean more toward service innovation. This is because service innovation has a lower threshold and cost, which better aligns with the resources and capabilities of companies in the central and western regions.

>>>>

Total financing in the overseas healthcare and medical industry is also on an upward trend, with the United States taking the lead.

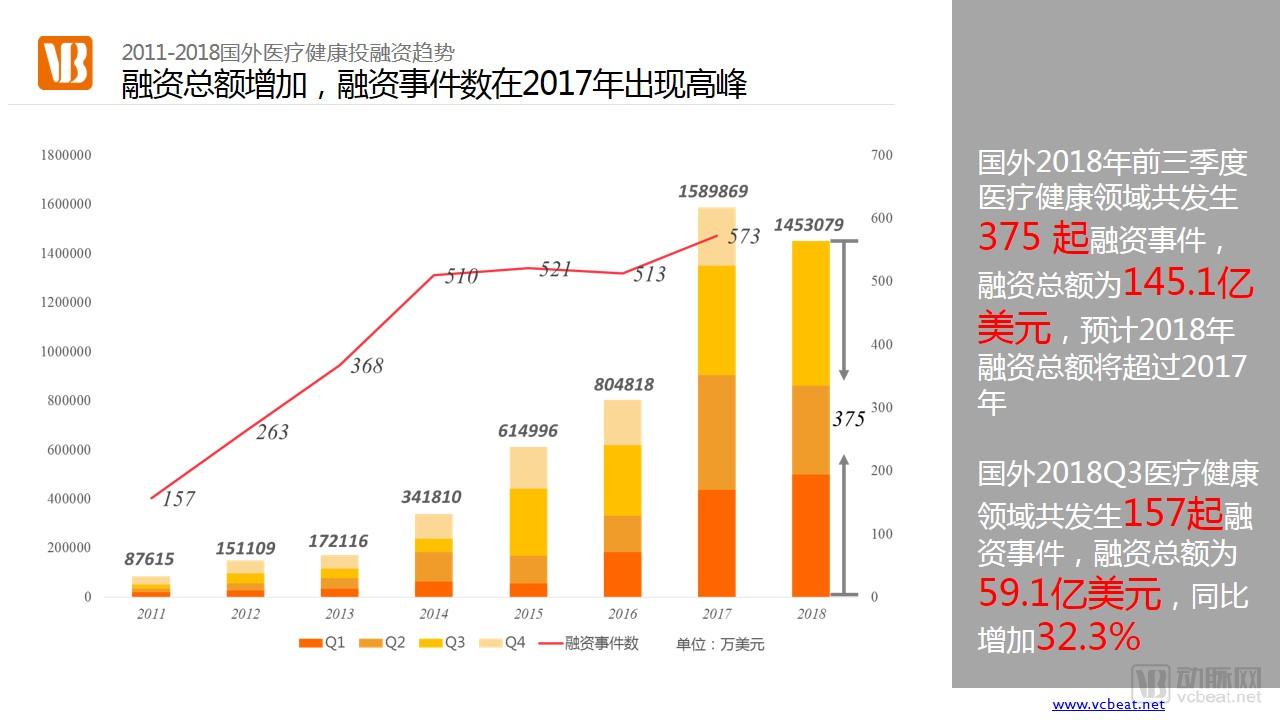

In the first three quarters of 2018, total healthcare financing abroad reached $14.51 billion. Based on global investment and financing growth trends, the total overseas financing volume in 2018 is projected to exceed that of 2017. In the third quarter of 2018, there were 157 financing deals in the overseas healthcare sector, with a total financing amount of $5.91 billion, representing a year-on-year increase of 32.3%.

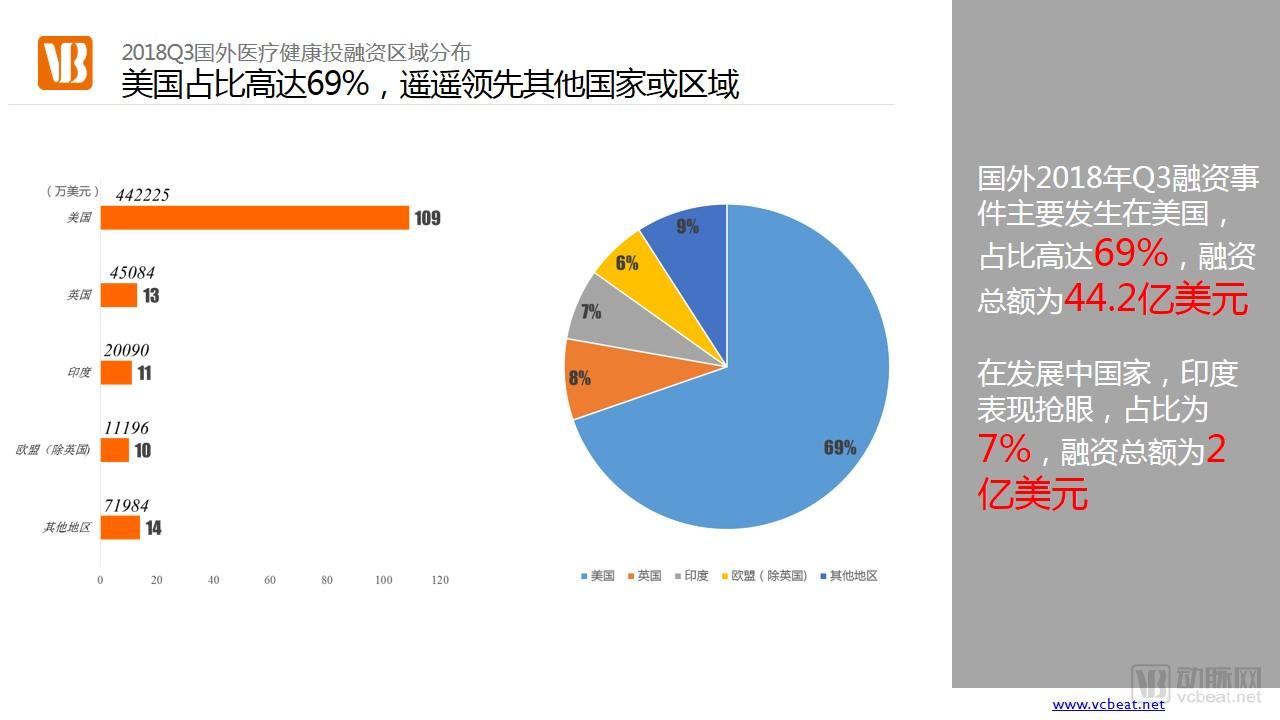

In terms of the countries and regions where financing events occurred, the United States took the lead with 109 deals, accounting for 69% of the total. The total financing amount reached $4.42 billion, representing 74.9% of the global share. This demonstrates that the U.S. remains the global leader in innovation within the healthcare industry.

Among developing countries, India has stood out, accounting for 7% of financing deals with a total funding amount of $200 million. Its healthcare investment and financing scale is second only to China’s, and its future development potential should not be underestimated.

Comparison of Healthcare Investment and Financing in China and the US: Similar Number of Financing Deals, with Total Financing Volume in the US Approximately Twice That of China

Whether in terms of the number of financing deals or the total amount raised, China and the United States are both global leaders in the healthcare industry, playing an irreplaceable role in driving its worldwide development.

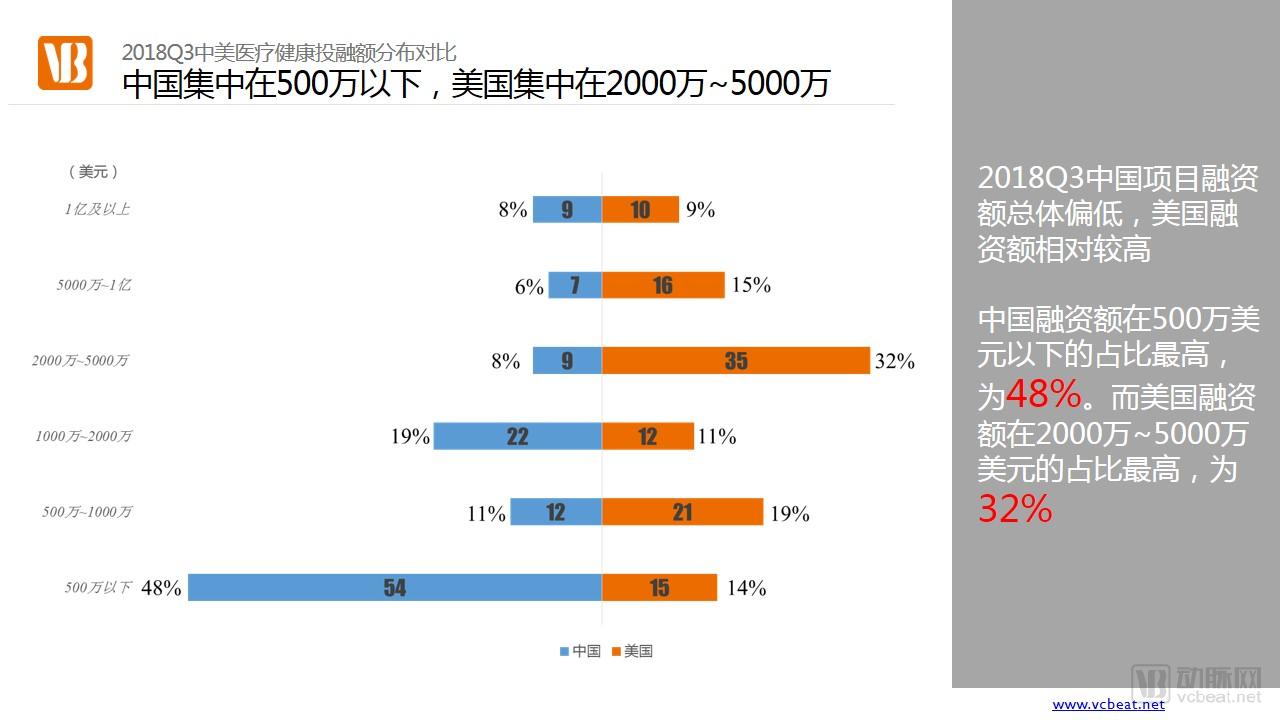

The number of financing events in China and the United States is comparable, indicating a similar level of innovation enthusiasm in the healthcare industries of both countries. However, the total financing amount in the U.S. is approximately twice that of China. In China, project financing is concentrated below $5 million, whereas in the U.S., it is concentrated in the range of $20 million to $50 million. This disparity suggests, on one hand, that U.S. healthcare startups are of higher quality; on the other hand, the advanced development of the U.S. capital market has laid the foundation for larger financing volumes.

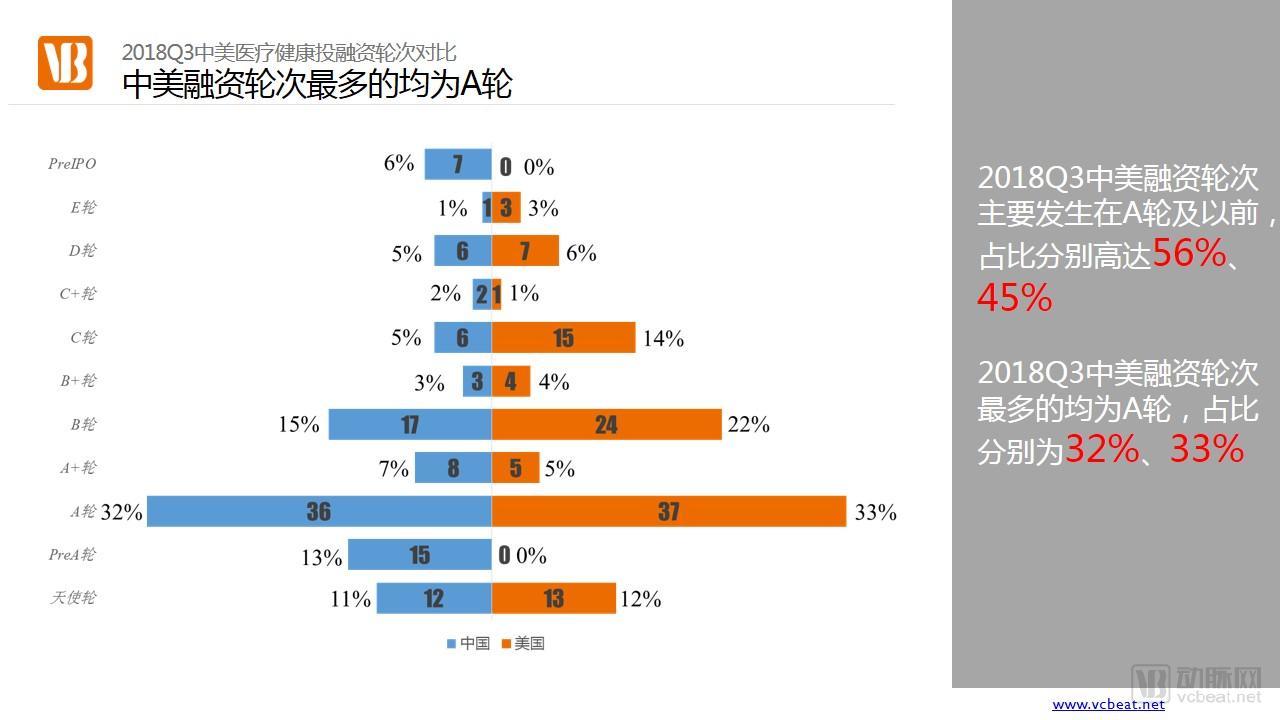

In terms of funding rounds, both China and the United States see Series A as the most common stage. Moreover, projects at Series A or earlier account for 56% and 45% of the total in China and the U.S., respectively, indicating that the majority of projects are still in their early stages.

From a financing perspective, healthcare informatics and biotechnology have emerged as hot sectors, indicating that investment institutions in both China and the United States are focusing on technological innovation within the healthcare industry, aligning with global mainstream trends.

Summary

Based on an analysis of global healthcare industry investment and financing in the third quarter of 2018, we can draw the following conclusions:

1. Total financing continues to increase, but the growth rate has declined, indicating that capital is returning to rationality and shifting from an “extensive” to an “intensive” model.

2. Most projects are still in the early growth stage and will need to sustain continuous innovation to achieve better development.

3. Technological innovation has become a key driver of transformation in healthcare, and capital will be heavily invested in this area.

4. The growing strength of China’s healthcare industry has become an important component of the global healthcare sector, attracting substantial overseas capital.

5. The United States remains the global leader in healthcare innovation, but the gap between China and the U.S. is narrowing