Magnetic-Controlled Capsule Gastroscope Robot: A $1.25B Global Opportunity with $9B Potential in China

Authors: Chen Chuan, Ma Quanchang, Huayi Capital

Capsule gastroscopy robots are likely familiar to most people. This medical device is currently positioned for early screening of gastric cancer and general gastric health check-ups. Last year, AnHan emerged as a unicorn in this field, with a valuation exceeding $1 billion, making it the only company in China that has obtained regulatory approval and is commercially selling capsule gastroscopy robots. Several other companies are also currently engaged in R&D in this area.

Many investors are paying close attention to this sector, but most believe that the market is relatively new and lacks pioneering efforts by large multinational corporations, making it challenging for new entrants to establish a foothold. For novel medical devices, the extent of market education remains a key concern for investors, aiming to avoid a scenario where products with strong technical merits fail to achieve commercial success. Additionally, assessing the true size of the market is relatively difficult, sales channels are perceived as somewhat limited, and questions remain regarding the precise nature of technological barriers.

This article addresses the aforementioned questions by discussing the investment logic in this field.

Current Status of Gastric Cancer Screening in China

1. High incidence rate, high case fatality rate

Gastric cancer is the second most common cancer in China. According to Chinese cancer data analysis, there were 679,000 new cases of gastric cancer and 498,000 deaths in 2015, with an incidence rate of 30 per 100,000 population. High-prevalence conditions include gastritis, peptic ulcer disease, and gastric cancer. Among these, the prevalence of peptic ulcer disease in the population is as high as 17.2%, significantly higher than that in Western countries (4.1%).

Unlike in other countries, gastric cancer in China is characterized by high incidence and mortality rates, a low proportion of early-stage cases (approximately 10%), and a primary focus on the diagnosis and treatment of advanced-stage cases. Furthermore, in recent years, newly diagnosed gastric cancer patients have shown a trend toward younger ages, with the proportion of patients under 30 years old rising sharply from 1.7% in the 1970s to the current 3.3%.

The early diagnosis rate of gastric cancer in China is extremely low, which severely affects prognosis.

Compared with South Korea, Japan is a country with a high incidence of gastric cancer. It began gastric cancer screening in 1983, conducting annual barium meal examinations for individuals over the age of 40. In 2015, Japan’s relevant guidelines were updated, explicitly recommending endoscopy for gastric cancer screening and suggesting that individuals aged 50 and older undergo gastroscopy every two years. Nationwide endoscopic screening has enabled Japan to achieve an early diagnosis rate for gastric cancer of approximately 70%. South Korea initiated gastrointestinal tumor screening in 1999, providing endoscopic examinations every two years for individuals over the age of 40.

Currently, the early-stage gastric cancer diagnosis rate in South Korea ranges from 60% to 67%.

Currently, approximately 90% of gastric cancer cases identified in China are at an advanced stage. The prognosis of gastric cancer is closely related to the timing of diagnosis and treatment. Even with surgical intervention, the five-year survival rate for advanced gastric cancer remains below 30%, whereas the five-year survival rate for early-stage gastric cancer can exceed 90%, potentially achieving a cure. However, the diagnosis and treatment rate for early-stage gastric cancer in China is less than 10%, significantly lower than that in Japan (70%) and South Korea (60–67%). Furthermore, due to the high cost of early screening for gastric cancer in China, opportunistic outpatient screening has been the prevailing approach, resulting in an early diagnosis rate of less than 10%, which is far below the levels observed in Japan and South Korea.

Let me share a brief anecdote. Many investors in the industry are likely familiar with Ms. Han Xiaohong, founder of Ciming Health Checkup (acquired by Meinian Onehealth in 2017). In the early stages of her entrepreneurial journey, she was diagnosed with early-stage gastric cancer during a visit to South Korea in 2005. The diagnosis was made using painless gastroscopy and colonoscopy, a method commonly employed in South Korea at the time. Fortunately, the cancer was detected at an early stage. She underwent surgery and chemotherapy promptly and returned to work just four months after the operation. Her condition was adenocarcinoma, which can progress rapidly if not identified and treated in a timely manner.

In her article “How I Defeated Cancer in Eight Years (2013),” Han Xiaohong stated, “People of our generation did not have the habit of undergoing regular health checkups. Moreover, at that time, Ciming Health Checkup only offered packages priced at 2,000 yuan, whereas this South Korean provider offered services worth 20,000 yuan. Even if I had wanted to undergo such comprehensive screening at my own health checkup center, it would not have been detectable.”

This statement was made by her in 2013. Over the following five years, the early gastric cancer screening industry underwent significant changes. Meinian Onehealth Healthcare invested in Anhan Medical, promoting the sale of capsule gastroscopy robots to health checkup institutions. Sales have grown year after year, benefiting many patients with early-stage gastric cancer.

2. Preliminary completion of market education: In 2018, the capsule endoscopy robot was included in the Expert Consensus (Draft) on Screening Procedures for Early Gastric Cancer in China

Internationally, only South Korea and Japan have relatively comprehensive gastric cancer prevention and screening systems. China still lacks consensus guidelines on early gastric cancer screening protocols.

To further implement the Healthy China Strategy, on December 22, 2017, led by the National Clinical Research Center for Digestive Diseases (Shanghai), in collaboration with the Chinese Society of Gastroenterology’s Branches of Digestive Endoscopy and Health Management, the Chinese Medical Doctor Association’s Committee of Digestive Endoscopy and Committee of Health Management and Physical Examination for Digestive Endoscopy, the National Quality Control Center for Digestive Endoscopy, and the Professional Committee of Tumor Endoscopy of the China Anti-Cancer Association, multidisciplinary experts in gastroenterology, endoscopy, oncology, and health management from across China were organized. Building upon the “Consensus on Screening and Endoscopic Diagnosis and Treatment of Early Gastric Cancer in China (April 2014, Changsha)” formulated in 2014, these experts further refined and established an early gastric cancer screening process suited to China’s national conditions, jointly developing the “Expert Consensus on the Screening Process for Early Gastric Cancer in China (Draft) (2017, Shanghai),” which was published in the first quarter of 2018.

This consensus statement (draft) explicitly mentions for the first time that magnetically controlled capsule gastroscopy screening is an optional screening modality: its cancer detection rate has reached the level of electronic gastroscopy screening in Japan and South Korea, with high patient acceptance and no serious complications. Therefore, magnetically controlled capsule gastroscopy serves as an optional screening method for populations at risk of gastric cancer, facilitating the detection of precancerous lesions or conditions, and is suitable for large-scale gastric cancer screening in the general population.

The publication of this consensus opinion (draft) signals that gastric cancer screening may be elevated to a national program; from an investment perspective, it indicates that market education for the concept of early gastric cancer screening has been initially completed, bringing related medical devices into the scope of investable assets with potential for rapid development and profitability.

3. Policy and Medical Insurance Support Rapid Development

In April 2018, the launch conference for the National “Screening, Early Diagnosis, and Early Treatment of Gastrointestinal Tumors Project” was jointly initiated by seven organizations, including the National Clinical Research Center for Digestive Diseases (Shanghai), the Endoscopist Branch of the Chinese Medical Doctor Association, the Health Management Branch of the Chinese Medical Association, and the China Health Promotion Foundation. The project plans to establish more than 200 gastrointestinal tumor screening centers across China within one to two years, aiming to screen 10 to 20 million people annually. Furthermore, it seeks to leverage these screening efforts to increase the early diagnosis rate of gastrointestinal cancers to 20% and raise the five-year survival rate for gastrointestinal cancers to 50% by 2030.

Furthermore, medical insurance coverage is a key driver accelerating the marketization of capsule endoscopy. Currently, capsule endoscopy procedures have been sequentially included in the medical insurance schemes in regions such as Guangdong, Shanghai, Chongqing, and Shandong, thereby driving rapid market expansion. Notably, in Guangdong Province, capsule endoscopy costs below RMB 3,800 are fully reimbursable.

Market Size Analysis

According to statistics from the World Health Management Alliance, the global number of patients with gastric diseases has increased from 150 million in 1985 to 500 million in 2012, and this figure is projected to reach 700 million by 2025. Data from the World Health Organization indicates that more than 10 million people die annually from gastrointestinal diseases worldwide, including 4 million deaths attributable to diarrhea. As a stubborn and chronic condition, gastrointestinal disease can lead to severe consequences if not treated early, and may even progress to cancer.

If these patients underwent endoscopy every two years, as is common in Japan and South Korea, the global annual number of endoscopic procedures would exceed 250 million. Assuming a 10% substitution rate with capsule endoscopy and a price of $500 per capsule, the potential market size would reach $12.5 billion.

Internationally, capsule endoscopy primarily refers to capsule enteroscopy. Key manufacturers include Given Imaging (Israel), Olympus (Japan), IntroMedic (South Korea), and CapsoVision (United States). As the pioneer in the capsule endoscopy industry, Given Imaging has focused its sales on European and American markets, capturing a significant share of the international market. The company was acquired by Covidien in 2014, and Covidien was subsequently acquired by Medtronic in 2015. Given Imaging reported revenues of USD 180 million in 2012. Based on historical growth rates, its revenue was projected to reach approximately USD 280 million by 2017. Even assuming Given Imaging held a 50% market share, the global market size would be estimated at around USD 500 million, indicating that the global capsule endoscopy market remains relatively small. Specifically regarding capsule gastroscopy, no related products are currently available on foreign markets.

According to statistics from the Ministry of Health, China has 120 million patients with gastrointestinal disorders, with a peptic ulcer incidence rate of 10% and a chronic gastritis incidence rate of 30%, making China unequivocally a “major country for gastric diseases” worldwide. Meanwhile, China is also a high-incidence region for gastric cancer, with 400,000 new cases diagnosed annually, accounting for 42% of the global total. In recent years, the onset of gastric cancer has shown a trend toward younger age groups, and the incidence rate among middle-aged patients has been increasing year by year. If endoscopic examinations are conducted once every two years, the annual number of such procedures would exceed 60 million. Assuming a 10% substitution rate of capsule endoscopy and an ex-factory price of RMB 1,000–1,500 per capsule, the potential market size would reach RMB 6–9 billion.

In China, capsule endoscopes are primarily categorized into capsule colonoscopes and capsule gastroscopes. The annual sales volume of capsule colonoscopes in China ranges from 100,000 to 150,000 units, with a market size of RMB 150–200 million. Capsule gastroscopes, to some extent, pose competitive pressure on and partially substitute for capsule colonoscopes.

In the capsule endoscopy market, based on different application scenarios, the market is mainly divided into three parts:

1) Premium Health Checkups: High-end health screening services offered by leading providers such as Meinian Onehealth and iKang Guobin;

2) Hospital Examination: Endoscopic examination in the gastroenterology department of a hospital at Level II or above.

3) Primary screening: Early screening primarily conducted by community hospitals and first-tier hospitals;

Currently, the primary user base consists of mid-to-high-end clients at health checkup institutions. As China has not yet launched large-scale gastric cancer census and screening programs, screening mainly relies on opportunistic gastroscopy for symptomatic outpatients. Consequently, the volume of screenings at primary care facilities remains low. Furthermore, the adoption rate of capsule endoscopy as a substitute for conventional gastroscopy in tertiary hospitals is also low. This is primarily because patients visiting tertiary hospitals are generally not seeking early screening; they often require biopsies and therapeutic interventions. Additionally, from a physician’s perspective, the current image quality and operational efficiency (procedure time) of capsule endoscopy are insufficient to replace conventional gastroscopy, although it can serve as a beneficial supplement. At present, Anhan, a domestic unicorn company, derives the majority of its sales from checkup clients at Meinian Onehealth, with relatively few units sold in tertiary and primary care hospitals. This sales distribution reflects the current state of the industry.

We can estimate and project the future market size and development trends of capsule gastroscopy from three major market perspectives.

1) High-end Physical Examination Market

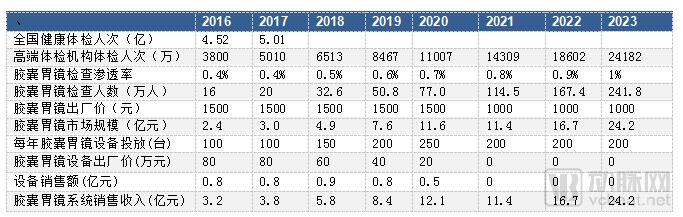

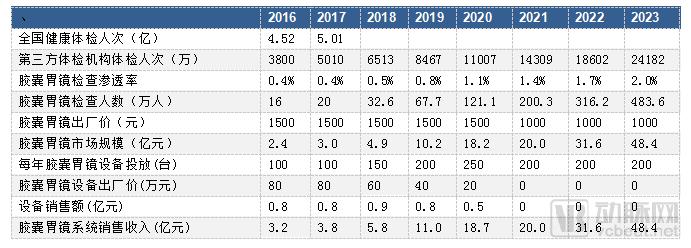

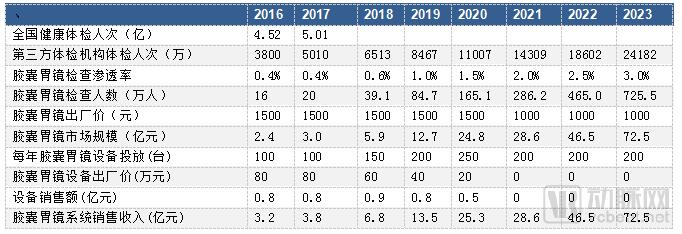

Among the three major markets in China, the high-end health checkup market has been gradually opened up by Anhan through its collaboration with Meinian Onehealth, the largest health checkup provider in the country. As public awareness of health continues to grow, the volume of high-end health checkups is expected to increase year by year. In 2016, the number of health checkup visits in China reached 452 million. However, since routine checkup packages do not include gastroscopy, extrapolating from this figure would result in significant deviation. Therefore, the market size can be estimated based on the volume of high-end checkups conducted by providers such as Meinian Health. Private checkup institutions account for approximately 10% of the national market share, corresponding to 40–50 million visits.

In 2016, Meinian Onehealth conducted 16.61 million health examinations, and Anhan sold 160,000 capsule gastroscopy units. In 2017, the number of Meinian Onehealth examination centers reached 400, with the volume of health examinations exceeding 21.6 million. Anhan’s capsule gastroscopy sales in 2017 ranged from 200,000 to 300,000 units, the vast majority of which were driven by Meinian Onehealth. This indicates an overall penetration rate of approximately 0.4%.

The high-end health checkup market is expected to maintain rapid growth. Assuming a compound annual growth rate (CAGR) of 30% over the next five years, with a conservative penetration rate of 1% and an optimistic penetration rate of 2% for capsule gastroscopy, and considering that chain health checkup centers can leverage centralized procurement to obtain discounted prices for capsule gastroscopy consumables and equipment, the market size for capsule gastroscopy in the high-end health checkup sector in 2023 is estimated at RMB 2.42 billion to RMB 7.25 billion.

The specific calculation model is as follows:

Conservative Forecast of the Market Size for High-End Health Checkup Capsule Gastroscopy

Neutral Forecast of the Market Size for High-End Health Checkup Capsule Gastroscopy

Optimistic Forecast for the Market Size of High-End Health Checkup Capsule Gastroscopy

2) Hospital Testing Market

In the hospital inspection market, given that digestive endoscopy equipment and physician resources are primarily concentrated in hospitals at Level II and above, data from hospital-based digestive endoscopy procedures can serve as a reference. Although capsule gastroscopy is not yet sufficient to replace traditional gastroscopy, its performance is gradually improving—for instance, with procedure time reduced to approximately 10 minutes—thereby progressively opening up the hospital market. Based on 2012 digestive endoscopy data, when a total of 22.23 million routine gastroscopies and therapeutic procedures were performed, and assuming an annual growth rate of 5% in procedural volume, the number of digestive endoscopy procedures is projected to reach 28.37 million by 2018 and 38.02 million by 2023.

Assuming a replacement rate of 0.2% in 2018, the conservative, neutral, and optimistic forecasts for the replacement rate in 2023 are 2.5% and 5%, respectively. Given that capsule endoscopy requires bundled equipment sales, with the current terminal price of the equipment ranging from RMB 2 million to RMB 3 million and an assumed ex-factory price of RMB 1.5 million, data from 2012 indicates there were 6,128 institutions capable of performing gastrointestinal endoscopic diagnosis and treatment. Assuming full market penetration over a 10-year period, the rollout is divided into three phases: the first three years as a market promotion phase with gradual volume increase, the next four years as a maturity phase, and the final three years as a decline phase with gradual contraction. In line with common strategies for mature medical devices, the primary approaches include sales (direct and distribution), financial leasing, and equipment placement.

Currently, Anhan is the only company with devices on the market, allowing it to maintain high prices. In 2–3 years, as equipment from other manufacturers enters the market, financial leasing and placement strategies will further drive down device prices while sales volume reaches its peak. In 6–7 years, the business model is expected to shift primarily toward device placement in exchange for increased consumables sales. Thus, the market size for capsule gastroscopy in hospitals in 2023 was RMB 1.75–3.84 billion.

The specific calculation model is as follows:

Conservative Forecast of the Market Size for Capsule Endoscopy in Hospitals

Neutral Forecast of the Market Size for Capsule Gastroscopy in Hospitals

Optimistic Forecast for the Hospital Market Size of Capsule Endoscopy

The current suboptimal market penetration of hospital-based examinations is primarily attributed to the fact that magnetically controlled capsule gastroscopy typically requires around 30 minutes to complete, whereas conventional intubation gastroscopy takes less than 10 minutes. To fully capture this market, two key strategies are essential: first, intensify market education to raise awareness of early gastric cancer screening, thereby transforming opportunistic outpatient screening into a routine early-detection practice; second, further reduce the procedure time for magnetically controlled capsule gastroscopy to 10–15 minutes, which would significantly enhance its competitiveness. However, shortening the procedure time is directly linked to the robotic manipulation system, representing a technically challenging barrier with high entry thresholds.

3) Primary Care Screening Market

Primary care screening represents the most suitable application scenario for capsule gastroscopy. With the advancement of tiered diagnosis and treatment, a system featuring early screening at the primary care level and diagnostic evaluation and treatment at secondary hospitals or above constitutes the most rational healthcare model. The capsule gastroscopy system effectively decouples image acquisition from interpretation. Image acquisition is a standardized procedure that can be fully performed by nurses, with images transmitted remotely to physicians for diagnostic review. Further examinations are then conducted to confirm any identified abnormalities.

Certainly, primary-level early screening also faces several issues:

First,China has not yet launched large-scale population-based screening programs for gastric cancer; however, experts are currently calling for the elevation of “early screening for gastric cancer” to a national strategy, which is expected to be realized in the near future.

Secondly,There is a shortage of endoscopists at the primary care level, and training physicians takes 10 years. Implementing large-scale early screening will inevitably generate a substantial demand for image interpretation and diagnosis. Currently, AI-assisted diagnosis appears to be a more suitable solution, although the technology still requires time to reach full maturity.

Furthermore,, the high price of capsule endoscopy is prohibitive; primary care early screening requires cost-effective products, and the current price range of RMB 3,000–4,000 is clearly unsuitable. The production cost of the capsule itself is not high, and with increased screening volume, the end-user price can be reduced rapidly.

Given that resolving these issues will take some time, the primary care early screening market is expected to remain 5–8 years away from maturity. Meanwhile, due to the limited financial resources of primary healthcare institutions, capsule endoscopy equipment is likely to be deployed primarily through placement models. China has 120 million patients with gastrointestinal disorders. If each patient undergoes screening once every two years, the annual screening volume will exceed 60 million procedures. With the factory price per capsule reduced to RMB 500, the market size would reach RMB 30 billion. Assuming conservative, neutral, and optimistic penetration rates for capsule endoscopy screening of 10%, 15%, and 20%, respectively, the screening volume would exceed 10 million, and the market size would range from RMB 3.09 billion to RMB 6.14 billion. This demonstrates the substantial growth potential of the primary care screening market.

Conservative Forecast of the Market Size for Capsule Endoscopy in the Primary Healthcare Market

Neutral Forecast of the Capsule Endoscopy Market Size in Primary Care Markets

Optimistic Forecast for the Market Size of Capsule Endoscopy in Primary Care Markets

Overall Forecast: Before 2020, capsule endoscopy will continue to grow in tandem with the expansion of high-end health checkups, a segment experiencing rapid growth. After 2020, as multiple products enter the market, competition will intensify and overall prices will decline, leading to a significant surge in hospital-based examination volumes. Beyond 2023, with the widespread adoption of early gastric cancer screening and the relative maturity of AI-assisted diagnosis, capsule prices will further decrease, ushering in large-scale expansion of the primary care early screening market.

Market Size Estimation Summary:

It is estimated that by 2023, the market size will be approximately RMB 5.17 billion under a conservative scenario, RMB 9.04 billion under a neutral scenario, and RMB 13.09 billion under an optimistic scenario.

Current Status of Magnetically Controlled Capsule Gastroscopy Development

To prevent investors new to this field from confusing “conventional capsule endoscopy” with “magnetically controlled capsule gastroscopy,” we must first introduce conventional capsule endoscopy, which operates without power or external control. Magnetically controlled capsule gastroscopy has evolved from conventional capsule endoscopy over several decades.

Capsule Endoscopy Without External Control: The Development History of Small Bowel Capsule Endoscopy

Capsule Endoscopy (CE), fully named “Intelligent Capsule Gastrointestinal Endoscopy System,” also known as “Medical Wireless Endoscopy.” The principle involves the examinee orally ingesting an intelligent capsule equipped with a built-in camera and signal transmission device. Propelled by gastrointestinal peristalsis or controlled by an external power system, the capsule moves through the gastrointestinal tract, capturing images. Physicians then use an external image recorder and imaging workstation to review the entire gastrointestinal tract, enabling them to diagnose the patient’s condition.

Capsule Endoscopy: From Concept to Clinical AdoptionFrom its initial conception to its integration into the medical field, capsule endoscopy underwent a lengthy development process. First introduced in 2000, it was originally designed for examining the small intestine. The capsule traverses the gastrointestinal tract via natural peristalsis, aided by gravity and swallowing. Equipped with an integrated camera, the device captures images of the small intestine—an area inaccessible to conventional flexible endoscopy. As a diagnostic tool, it enables the localization of bleeding sources in the mid-gastrointestinal tract and the identification of conditions such as inflammatory bowel disease (Crohn’s disease), polyposis syndromes, and tumors.

The notion that capsule endoscopy can effectively examine the small intestine is now firmly entrenched. Undeniably, there is a strong preference for gastrointestinal examinations that are minimally invasive and offer high patient comfort.

Development History:

The invention of the first transistor in the early 1950s enabled the miniaturization of radio transmission circuits that could be embedded into pills, making wireless telemetry devices capable of transmitting signals from within the body possible.

It was not until the 1990s that scientists integrated cameras into capsules, thereby developing the first generation of capsule endoscopy (CE) devices, which are small enough to be swallowed and capable of imaging the entire gastrointestinal tract.

In 1995, independent research conducted by teams from the Royal London Hospital and Rafael (Israel’s government defense R&D agency) provided the initial concept for wireless capsule endoscopy (WCE) and led to the first patent application. Subsequently, the first animal imaging demonstration was performed in 1997. Ultimately, through the joint efforts of the two groups, the first successful study was conducted in 1999 with ten healthy volunteers.

In 2001, this work was finally commercialized with the launch of the first wireless capsule endoscope by Given Imaging. Since its release, the capsule named M2A™ has become the gold standard for comprehensive small bowel screening. Since then, other manufacturers of capsule endoscopes have entered the market. Olympus Medical released a competing product, EndoCapsule, in 2005, which offered higher resolution and real-time viewing capabilities. The product was subsequently launched immediately in Europe (2006) and the United States (2007). Jinshan Science & Technology from China has become the leader in the Chinese small bowel capsule endoscopy market with its OMOM capsule.

Given has pushed capsule technology to its limits; however, a notable drawback remains. Traditional capsule endoscopes move passively, relying on gravity and gastrointestinal peristalsis, and capture random images of the digestive tract mucosa without achieving active control. Given has yet to make breakthroughs in active control technology.

Magnetically Controlled Capsule Gastroscopy

Thanks to the efforts of scientists and medical device manufacturers, capsule endoscopy for small bowel examination has been successfully commercialized. In contrast, magnetically controlled capsule gastroscopy for gastric examination has undergone many years of research and development.

The application of capsule endoscopy is primarily limited by the large volume and irregular anatomical structure of the stomach. Unlike conventional gastroscopy, which allows for observation under mucosal distension, gastric peristaltic waves and contractile states increase the difficulty of achieving comprehensive visualization of the gastric mucosal surface with capsule endoscopy. Compared with conventional gastroscopy, for capsule gastroscopy to gain acceptance, it must first be proven reliable and capable of providing complete visualization of the mucosa.

As previously mentioned, capsule endoscopy is passive. Therefore, to perform gastric examinations, primary attention has been focused on internal and external drive methods to address how to achieve active movement and free manipulation. Since the 1960s, patents have been granted for the use of external magnetic fields to non-invasively manipulate foreign insertions within body cavities.

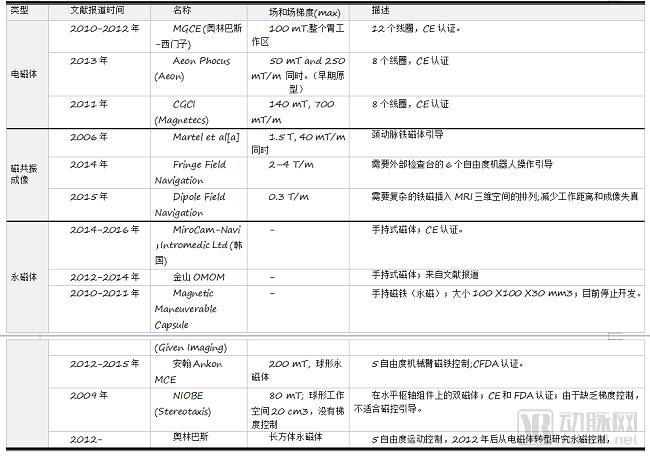

Another technical analysis article by the author on magnetically controlled capsule gastroscopy robots mentioned the following development history and control classifications:

The author has compiled a table of other R&D developments both domestically and internationally,Based on the type of magnetic control, they are classified into electromagnets, magnetic resonance, and permanent magnets.

1. Handheld Magnet Control (Representative companies in commercialization: Jinshan and Intromedic from South Korea)

As early as 2010, Swain and his colleagues first demonstrated magnetic manipulation in the human esophagus and stomach. In this single-case study, a volunteer swallowed a modified wireless capsule endoscope. The prototype was based on the PillCam COLON capsule (Given Imaging Ltd.). Modified magnetic materials were incorporated to enable external magnetic control while maintaining the capability for image capture and transmission. To achieve this, a thermal switch was used to replace the standard reed switch, activating the capsule in hot water at 60°C.

However, this modification occupies internal space within the capsule; therefore, the image capture rate is fixed at four frames per second by using a single image sensor instead of a dual-sensor configuration. A real-time camera (Given Imaging Ltd.) and an external rectangular magnet are located at the junction of the capsule. Meanwhile, gastroscopy is used to assess the capsule’s movement in real time.

This study reported favorable controllability of the capsule; however, conventional gastroscopy with air insufflation to distend the gastric lumen was still required during examination. Over time, it was subsequently demonstrated that this seemingly straightforward procedure was not reproducible due to the stomach’s propensity for collapse and peristaltic waves.

Around 2012, China’s Jinshan Technology also launched the OMOM controllable capsule system, which utilizes a handheld magnetic field generator. It demonstrated maneuverability in the upper gastrointestinal tract in human body models. The handheld magnetic field generator is highly cost-effective, and endoscopists can master its operation in a short period of time.

However, in terms of motion precision, this handheld operation is inferior to robotic control. For instance, to project a sufficiently strong magnetic field and magnetic field gradient into the gastrointestinal tract, especially for obese patients, significantly larger magnets must be used. Employing such a handheld system throughout the entire gastroscopy procedure imposes a heavy physical burden on the operator.

Intromedic Ltd. of South Korea has developed the MiroCam-Navi capsule endoscope (Figure 1). This system utilizes the standard MiroCam small bowel capsule endoscope, with modifications to its internal magnetic mechanism to enable magnetic control within the upper gastrointestinal tract. The magnetic control is achieved via an external hammer-shaped handheld permanent magnet, while images are transmitted through sensors attached to the patient using Wi-Fi and real-time visualization software. A 2015 study described the first demonstration of the MiroCam-Navi system’s efficacy in 26 volunteers.

In their study, Rahman and colleagues successfully reported visualization rates of 88%–100% for the major anatomical regions of the upper gastrointestinal tract (gastroesophageal junction, 92%; cardia, 88%; gastric fundus, 96%; gastric body, 100%; gastric angle, 96%; gastric antrum, 96%; pylorus, 100%). However, it is noteworthy that the Z-line (dentate line) was visualized in only 46% of cases, with the authors reporting difficulty in controlling the speed at which the capsule entered the stomach.

Figure 1. The Mirocam-Navi system.

The challenges reported in this study are consistent with those described in the 2010 study. In this study, the controllability of the capsule within the stomach (particularly in the proximal region) was limited by the distance from the body surface to the magnetic cross-section.Handheld control systems can be considered an obsolete technology.

2. Electromagnetic Robot Control System (Olympus and Siemens)

The appealing features of handheld magnets are their ease of use and affordability. However, a 2010 paper by Ciuiti demonstrated in a porcine model that robotic control outperforms manual operation in terms of motion precision.

In 2010, when Olympus first collaborated with Siemens, the electromagnetic system employed utilized 12 coils. Although this device resembled an MRI scanner in appearance, its magnetic control force for maneuvering the capsule endoscope was significantly weaker (the magnetic control force used in conventional MRI scans is 150–500 times greater than that of this system). The system generates a magnetic flux density of up to 0.1 T within a sufficiently large working volume.

To facilitate magnetic control, the sensor incorporates magnetic materials. By precisely regulating the magnetic force using two joysticks, physicians can maneuver the capsule with five degrees of freedom in three-dimensional space, including linear motion along the X, Y, and Z axes, as well as horizontal rotation and vertical tumbling.

This capsule endoscope includes two image sensors, and the images viewed by physicians are delayed relative to real-time display.

In the volunteer trial, the average examination time was 30 minutes.

Between 2010 and 2015, researchers from Olympus and Siemens conducted three phases of studies, with published papers reporting the diagnostic performance observed in volunteer trials. They proposed that further improvements in navigation and control methods are still required. The researchers analyzed that changes in patient positioning are necessary to facilitate examination using magnetically controlled capsule endoscopy; therefore, the procedure does not rely solely on magnetic manipulation. Furthermore, visualizing the gastric fundus and angulus in collapsed regions of the stomach remains a challenge for magnetically controlled capsules. Additionally, in several other cases, strong antegrade or retrograde contractions of the gastric wall hindered the visualization of the gastric antrum and pylorus, as the magnetic control force cannot overcome the physiological peristalsis of the gastric wall.

After 2012, it was found that although coil-based systems are complex, they fail to achieve precise point levitation. Consequently, Olympus shifted to using permanent magnets (see subsequent patent technology transitions for details), specifically designing permanent magnets with specialized configurations.

3. Permanent Magnet Robot Control System (Anhan)

Anhan Technology possesses a patented, clinically approved robotic magnetic capsule guidance system, which has recently been reported to be installed in hundreds of medical centers across China. Their robotic system consists of a mechanical arm with five degrees of freedom (two rotational and three translational). Field generation is achieved using a single spherical magnet, capable of reaching field strengths of up to 0.2 T within the working area. The embedded video capsule is controlled by manipulating the magnet, enabling real-time video input at 2 fps.

In 2015, Zou and colleagues further demonstrated the diagnostic accuracy of the ANKON system. In a study involving 68 patients, participants underwent MACE examination first, followed by electronic gastroscopy within 4–24 hours. The mean examination time for magnetically controlled capsule endoscopy was 29.1 minutes, while that for electronic gastroscopy was 8.5 minutes. Notably, electronic gastroscopy captured at least 22 images per patient. Pathological findings were identified in all 68 cases, with concordant results between the two methods in 53 cases. Electronic gastroscopy alone detected abnormalities in 7 cases, whereas magnetically controlled capsule endoscopy identified 3 cases of erosion, 2 cases of ulcer, 1 case of atrophy, and 1 case of mucosal elevation.

Magnetically controlled capsule gastroscopy alone detected 8 cases, whereas conventional electronic gastroscopy missed 6 cases of erosion, 1 case of polyp, and 1 case of mucosal elevation. Two patients experienced abdominal pain, which resolved spontaneously. The authors also comprehensively compared the concordance between magnetically controlled capsule gastroscopy and conventional electronic gastroscopy in assessing the normality of gastric mucosa. The overall concordance rate reached 91.2% (McNemar’s test p-value = 0.687, indicating no significant difference).

In this study, mucosal visibility was improved by rotating or moving the capsule to create friction against the mucosa. However, mucosal observation remained impaired in three patients due to inadequate gastric cleansing preparation. The study did not directly compare patient satisfaction between the two examination methods, but the reported adverse event rates were very similar. Two patients experienced transient, self-resolving abdominal pain one day after the examination. Another patient developed chronic diarrhea, and subsequent colonoscopy revealed the capsule endoscope lodged in the ileocecal region.

4. MRI Magnetic Control Technology (No representative companies at present; mostly academic research)

Magnetic Resonance Imaging (MRI) is the most ubiquitous magnetic system used in medical applications. It can generate body-uniform unidirectional fields of up to 7 Tesla, as well as gradient-like pulses and RF signals. It can be used to simultaneously power capsule motion and perform real-time imaging and localization of the capsule. Researchers at ETH Zurich have proposed an innovative solution that utilizes MRI technology for capsule endoscopy, demonstrating the concept and securing a patent. The research team proposes a capsule with a flexible tail housing one or more micro-coils. Alternating currents generated in these coils produce a magnetic field that attempts to align with B0, thereby causing movement of the flexible tail to generate propulsion. The capsule’s power source is either a non-magnetic battery or energy harvested via induction through additional coils. The imaging capabilities of the MRI scanner can then be used to track the capsule and establish closed-loop motion control.

Sylvain Martel’s group at the California Institute of Technology is also dedicated to the concept of MRI-powered and guided magnetic robots. They have proposed a novel strategy, Fringe Field Navigation (FFN), which leverages the extremely high field gradients (2–4 T/m) generated by the fringe fields surrounding an MRI scanner to navigate magnetic wires and catheters across a whole-body region. These field gradients, produced by the superconducting scanner coils, are significantly higher and cover a larger workspace than those achievable with resistive coils or permanent magnet assemblies. Although practically cumbersome, they suggest manipulating the patient’s body to exploit the stationary fringe fields for controlling internal magnetic robots.

An improved strategy for generating large gradient fields without moving the patient involves using soft ferromagnetic inserts to distort the scanner’s large uniaxial field, thereby simultaneously producing strong static fields and gradients. This concept, termed Dipole Field Navigation (DFN), can generate gradients of 0.3 T/m within the whole-body workspace. Although distortion of the internal magnetic field hinders conventional MRI imaging, this limitation can be circumvented in specific regions of the scanner.

5. Other internally driven magnetic capsules (not yet commercialized; primarily academic research)

For example, a fish-like swimming magnetic capsule; in 2008, researchers including Morita from Osaka Medical College in Japan reported a capsule endoscope with a permanent magnet-embedded fin at its rear, propelled by fish-like motion in a stomach model. The device, named Self-Propelled Capsule Endoscopy (SPCE), was successfully tested in the water-filled stomachs of dogs in vivo. A simple electromagnetic coil system generates an alternating magnetic field (5–12 mT) to actuate the fins. A joystick controls the direction and speed of the swimming motion.

Morita et al. used permanent magnets in the fins of a capsule.

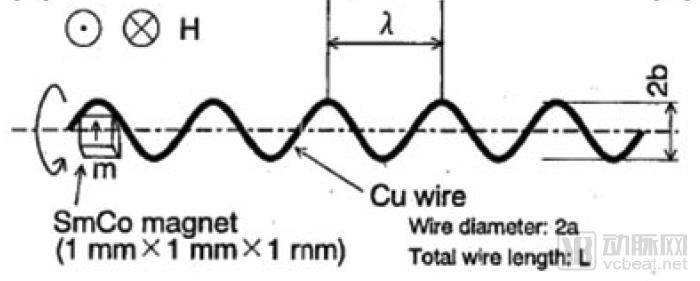

# Helical Magnetic CapsuleThe concept of helical capsule endoscopy employs rotation-induced linear propulsion of the capsule for gastrointestinal screening. In 1996, researchers at Tohoku University in Japan demonstrated their helical magnetic capsule, an untethered robot inspired by bacterial flagella. Composed of permanent magnets attached to a rigid helix, the robot can advance in a spiral manner under low Reynolds number conditions and within a rotating magnetic field.

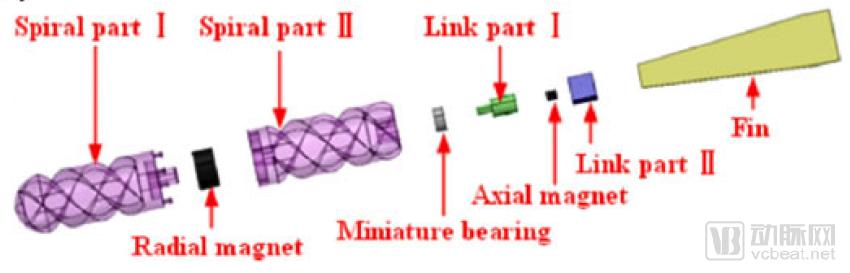

Hybrid Locomotion Capsule. A collaborative project between Tianjin University of Technology (China) and Kagawa University (Japan) describes a novel magnetically propelled millimeter-scale robot that combines fish-like undulatory motion with helical motion. Furthermore, it incorporates a gravity compensation method. By integrating these two distinct locomotion techniques, the researchers aim to define a more versatile approach to enable movement within the heterogeneous environment of the gastrointestinal tract. The robot employs a radially oriented magnet to control the rotation of the helical body and an axially oriented magnet to generate fin-like motion.

The feasibility of the internally driven model requires further ethical review, which limits its clinical application and thus hinders its widespread adoption.

Summary

Currently, most domestic companies developing capsule gastroscopy robots are working on devices controlled by external permanent magnet robotic arms (i.e., similar to those from Anhan and Olympus).

On the Level of Technical Barriers:

Passive small bowel capsules are highly mature, with Jinshan Technology holding the largest market share in China. Most companies capable of producing gastroscopic capsules can also develop small bowel capsules, which will to some extent impact the existing market share of small bowel capsules. The technical challenge of magnetically controlled gastroscopic capsules lies in capsule maneuverability; reducing the examination time from approximately 30 minutes to 10–15 minutes would significantly facilitate their adoption and sales within hospital systems.

To achieve effective control of capsule endoscopes, real-time localization is essential. Currently, all capsule endoscopes primarily rely on positional information derived from images captured by the capsule; however, this approach still does not allow physicians to definitively confirm the capsule’s exact location.

Capsule Localization in Magnetic Fields: A Brief OverviewThe topic of capsule localization within magnetic fields is extensive; here, we provide a concise description. Localization techniques can be broadly categorized into two types. The first employs an external array of sensors placed outside the body to measure the magnitude and directionality of the magnetic field generated by a magnet embedded within the capsule. The second operates in the reverse manner, utilizing magnetic field sensors inside the capsule to measure the field produced by field generators positioned externally to the body. Regarding localization sensors integrated within the capsule, although some literature exists, research remains confined to the fundamental study of the sensors themselves, and no suitable sensors are currently available for practical use.

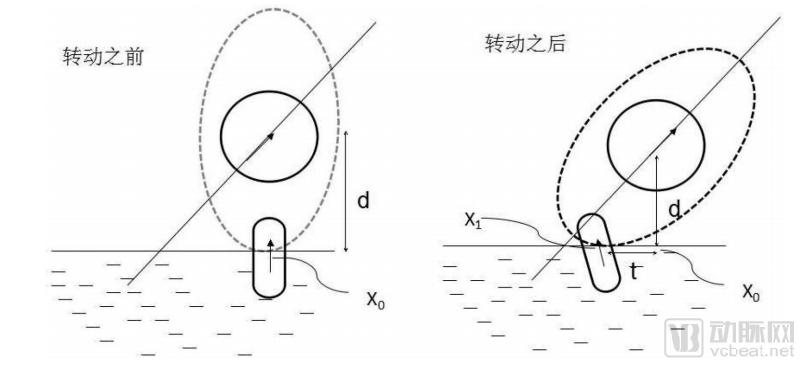

The prolonged operation time of the Anhan capsule is also constrained by this limitation. In Anhan’s patent, “Device and Method for Controlling the Movement of a Capsule Endoscope in the Human Digestive Tract (CN103222842A),” the intended objective is for the capsule to float on the water surface. However, as illustrated in the patent drawings, the equipotential magnetic lines of the spherical magnet are elliptical. Consequently, it is necessary to adjust the vertical distance between the external magnet and the capsule while rotating the external magnet; otherwise, the magnetic force exerted on the capsule will decrease, causing it to sink easily to the bottom. So-called precise movement is difficult to achieve in the absence of positioning sensors.

Patent Drawing: Device and Method for Controlling the Movement of a Capsule Endoscope in the Human Digestive Tract, CN103222842A

A Brief Overview of the Development of Domestic Enterprises

In terms of technological development among domestic enterprises, Anhan currently stands out as a leader and ranks among the top internationally. Other companies with ongoing research and development, such as Shenzhen Zifu, a spin-off enterprise from Shanghai Jiao Tong University, and Chongqing Jinshan, will not be individually reviewed here; instead, an objective patent review is cited to provide an indirect overview.

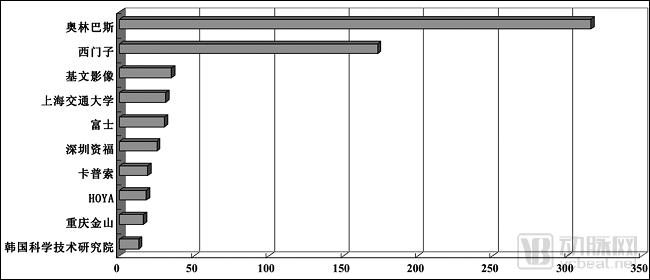

A 2017 patent review mentioned:

Top Patent Applicants and Number of Patent Applications Over the Years

“Around 2013, magnetic control technology in China garnered significant attention. Multiple domestic enterprises launched related research and achieved certain breakthroughs, enabling Chinese applicants, such as Shanghai Jiao Tong University, Shenzhen Zifu Co., Ltd., and Chongqing Jinshan Science & Technology (Group) Co., Ltd., to file a series of related patents.”

Foreign companies, led by Olympus Corporation and Siemens AG, hold an absolute technological lead in the field of magnetic control, which is inseparable from their advantages in magnetic field control for other medical products. In contrast, research on magnetic control in China started later and has progressed relatively slowly. However, Shanghai Jiao Tong University has achieved significant results in the active control of capsule endoscopes based on bionic principles. Currently, more domestic enterprises are investing in research in this area, and it is believed that Chinese companies will soon achieve notable successes in this field. (Li Kun, Patent Examination Cooperation Guangdong Center of the Patent Office, China National Intellectual Property Administration. Review of Patent Technologies for Capsule Endoscopy Guidance Systems[J]. Technology Outlook, 2017, 27(20).)

Investment Recommendation

Market Size:

Based on calculations, the market size in this field is projected to reach approximately RMB 5.17 billion under a conservative estimate, RMB 9.04 billion under a neutral estimate, and RMB 13.09 billion under an optimistic estimate by 2023, indicating a substantial market.

This sector represents a blue ocean market. Currently, only the high-end health checkup market has been tapped, while the hospital and primary care markets remain untapped, necessitating comprehensive and systematic market education. Progress in market education is encouraging: early gastric cancer screening has been included in the expert consensus (draft), with calls to elevate it to the national level. Furthermore, progress toward inclusion in the national medical insurance scheme signals the dawn of a market boom.

Competitive Landscape:

Currently, Anhan Technology is the only company that has obtained regulatory approval and has products on the market. Valued at over $1 billion, it has achieved unicorn status, while other companies with products in development have not yet received approval.

Valuation Reference:

Based on grassroots research, the valuations of companies with products under development range from RMB 200 million to RMB 1 billion. Under conservative assumptions, the market size in 2023 was RMB 5.17 billion. If a company with products under development could capture at least 10% of the market in 2023, its sales revenue would reach RMB 517 million. Assuming a price-to-sales (P/S) multiple of 2x, the corresponding valuation for 2023 would be RMB 1.034 billion. Discounted at an internal rate of return (IRR) of 25%, the present value amounts to RMB 338 million. Therefore, if the valuation for investing in such an early-stage company this year exceeds RMB 338 million, there may be certain market risks. (This valuation reference does not account for valuation premiums driven by technological innovation; it assumes investment in companies with similar product portfolios.)

For enterprises driving technological innovation that can enhance capsule control capabilities and reduce screening time to 10–15 minutes, greater attention should be given, and valuation requirements should be relaxed.