Ping An Leasing to Invest RMB 30 Billion, Build 1,000 Health Screening Centers and Reshape China's Independent Medical Imaging Sector

Since the State Council issued the first policy on the establishment of independent imaging centers in March 2015, independent imaging centers in China have evolved from nonexistence to emergence, subsequently receiving continuous policy support from the National Health Commission.

After more than three years, independent medical imaging centers, supported by policy, have not experienced the explosive growth once anticipated, but they continue to move forward.

In recent news, the Wuhan Center of Ping An Health (Diagnostic) Center has officially opened. On the day of the opening, Fang Weihao, Chairman and CEO of Ping An International Financial Leasing Co., Ltd. and Chairman of Ping An Haoyi Investment Management Co., Ltd., announced that Ping An Leasing plans to invest RMB 30 billion over the next five years to establish 1,000 Ping An Health (Diagnostic) Centers across China.

As one of the financial giants, no one doubts Ping An’s strength. Will the establishment of 1,000 third-party testing centers within five years open a new chapter for independent imaging centers?

Medical imaging is ubiquitous across all stages of healthcare, from physical examinations to tumor screening, with CT and MRI playing indispensable roles. Consequently, radiology departments in Grade A tertiary hospitals have long been operating under excessive workloads. However, on a national level, the aggregate inventory of imaging equipment in hospitals across China is sufficient to meet current demand; the underlying issue stems from the irrational allocation of resources.

From the perspective of China’s national healthcare structure, high-quality medical resources are concentrated in tertiary Grade A hospitals located in major cities. Consequently, residents with the financial means flock to the country’s most renowned hospitals. However, the value-added output of radiology departments is limited, yet these departments in tertiary Grade A hospitals bear an excessive workload.

According to data from VCBeat Research Institute, in Grade A tertiary hospitals, 60% of radiologists work more than eight hours a day, 25% work an average of over ten hours daily, and 75% earn a monthly salary below RMB 6,000. Nearly every hospital’s radiology department operates on a 24-hour shift system, leaving staff with no opportunity for rest from morning till night during peak periods. In addition, radiologists are exposed to radiation and other potential hazards due to prolonged work in enclosed spaces.

In contrast, primary healthcare institutions, in an effort to meet the high demand from patients, enhance their institutional image, or secure benefits associated with equipment acquisition, are often eager to procure large-scale medical devices. However, due to a limited patient base, many of these devices remain underutilized.

Therefore, both renowned hospitals and secondary hospitals possess a large number of imaging devices; however, the patient volume at renowned hospitals far exceeds their service capacity, while primary care hospitals remain largely unvisited, ultimately resulting in significant underutilization of equipment.

In this context, the advancement of independent imaging centers can not only alleviate congestion at tertiary hospitals and reduce patients’ medical costs, but also fully utilize idle imaging equipment at secondary hospitals through managed service arrangements. As a series of policies are rolled out in succession and overloaded imaging systems at renowned hospitals force patients to seek diagnostic services at lower-tier facilities, independent imaging centers have emerged as a viable alternative.

Despite support from policies and market demand, the development of independent imaging centers in China has been fraught with difficulties. To understand this phenomenon, we can seek answers by examining the following issues.

1. Where Does the Data Come From? As non-public medical institutions, it is difficult to obtain patients' historical medical record data. Apart from partner hospitals, independent imaging centers struggle to share patients' medical records.

II. How to Achieve Standardization? Independent imaging centers employ varying data entry methods, making it difficult to align with hospital standards. Consequently, hospitals often do not accept interpretations from independent imaging centers. If patients return to the hospital for treatment after undergoing examinations elsewhere, physicians will require them to undergo repeat imaging.

III. How to Purchase Equipment? Taking Magnetic Resonance Imaging (MRI) as an Example, Should One Choose 1.5T or 3T in the Absence of Reference Cases?

IV. For-Profit or Non-Profit? At the current stage, independent imaging centers face significant challenges in achieving profitability. Should they seek collaboration with public hospitals to co-establish imaging centers?

V. How to Promote? Patients are unfamiliar with and distrustful of this novel imaging service system, making it difficult for them to proactively visit independent imaging centers; physicians also do not actively refer patients to these centers.

VI. How Can Health Insurance Issues Be Resolved? Without the safety net of health insurance coverage, it is difficult for individuals with conventional income levels to choose independent imaging centers. Given that commercial health insurance has not yet become widespread in China, non-public healthcare providers lack a reliable payer. Some independent imaging centers offering high-end services must incur substantial costs to train and recruit talent in order to maintain service quality, which consequently drives up the prices of their services.

VI. How to Address the Source of Talent? In the context of a domestic shortage of high-quality radiologists, should companies make significant investments in recruiting from tertiary hospitals, or seek assistance from general radiologists?

VII. Is There Speculation? Zhu Ming, Head of the Pediatric Group of the Chinese Society of Radiology, told VCBeat that there was once an entrepreneur who raised hundreds of millions in financing in a single year under the guise of establishing an independent imaging center, yet made no actual progress in construction. How should we guard against such speculative practices?

These challenges are not insurmountable. On one hand, the government should continue to leverage policies to promote the development of imaging centers, address health insurance reimbursement issues, and drive patient referrals to these facilities. On the other hand, enterprises can study the development history of independent imaging centers in the United States and Japan, drawing lessons from their experiences in service delivery and data standardization.

Despite numerous challenges, the first batch of independent imaging centers has begun to take shape, with relevant enterprises including Ping An Health (Diagnostic) Center, Yimai Yangguang, Wanli Cloud, Kaipu Imaging, Pan-View Medical, Xinying International, and Yizhan Technology.

The data references部分内容 of the “White Paper on the Third-Party Medical Diagnostics Industry” by Health Point.

Ping An Health (Testing) Center integrates an imaging diagnosis center, a medical laboratory center, and a precision examination center. It has established imaging centers in 23 cities, including Nanchang, Wuhan, Guangzhou, and Chongqing. Its business model combines hospital partnerships with premium services. Leveraging advanced imaging equipment, nationally recognized experts, and partner medical institutions, it has built an integrated online-to-offline third-party medical sharing platform centered on medical imaging and laboratory testing technologies. The platform provides precise imaging diagnostics, blood tests, case diagnoses, and precision examinations to both medical institutions and individual consumers.

Yimai Yangguang Imaging Hospital Group primarily targets second- and third-tier cities, with its existing imaging centers distributed across more than 20 provinces and municipalities, including Beijing, Inner Mongolia, Shandong, Liaoning, Guizhou, Jiangxi, Hubei, Hunan, and Guangzhou. In terms of development strategy, its deployment models mainly consist of independent non-affiliated imaging centers, independent affiliated imaging centers, and regional shared imaging centers, all of which maximize service capacity through resource sharing. Regarding services, Yimai Yangguang uses medical imaging centers as its core framework, building upon this structure to develop an imaging cloud service platform and a Medical Imaging Academy. This approach leverages the advantages of the internet to explore new pathways for imaging service development, while also fostering internal talent cultivation to address the shortage of professionals in the medical imaging industry.

Wanli Cloud leverages the platform advantages of Ali Health, Wandong Medical, Yuwell Group, and Meinian Onehealth to build a big data cloud platform for medical imaging. It provides remote medical imaging services and cloud-based imaging technology solutions, establishes and operates offline third-party medical imaging centers, and offers technology development, promotion, and consulting services related to these operations. Currently, nine offline centers have been established in provinces such as Liaoning, Jilin, Hubei, and Heilongjiang.

Panorama Medical Imaging Diagnostic Center is an innovative institution truly dedicated to precision medicine, primarily focusing on high-end imaging examinations and diagnostics. It is committed to the early diagnosis and staging of tumors, as well as specialized screening for malignant cancers such as lung cancer and breast cancer. Its Hangzhou Imaging Center houses Zhejiang Province’s first PET/MR system in formal operation, along with other advanced equipment including PET/CT, 3.0T MRI, and 256-slice CT scanners. Currently, Panorama Medical operates in five cities: Shanghai, Guangzhou, Hangzhou, Chongqing, and Chengdu.

Heart Imaging Intelligent Technology is backed by Japan’s CVIC Heart Imaging International, with its technical strengths lying in cardiac magnetic resonance imaging (MRI). Cardiac MRI is the world’s only non-invasive, radiation-free, and repeatable imaging diagnostic method for the heart that causes no harm to the body, enabling one-stop scanning. Its cloud platform connects relevant institutions both domestically and internationally; all offline examination data are uploaded to the cloud platform, allowing for subsequent 3D analysis and processing, as well as diagnostic reports from overseas experts. Currently, CVIC has partnered with Panview Medical and established operations at the Hangzhou Panview Medical Imaging Diagnostic Center, with its image interpretation technology supported by Infervision.

In Wuhan, Fang Weihao announced that Ping An Leasing plans to invest RMB 30 billion over the next five years to establish 1,000 Ping An Health (Diagnostic) Centers nationwide, adopting a “heavy-asset, light-operation” model. This target is more clearly defined compared to the “5–8 year” goal set when the Nanchang Ping An Health (Diagnostic) Center opened in February this year.

As part of Ping An Health (Diagnostic) Center’s “triune” model, the independent imaging center will offer services with two distinct positionings. On one hand, Ping An Health (Diagnostic) Center will actively establish collaborations with hospitals at all levels in the future, alleviating the excessive medical demand on tertiary Grade A hospitals and enhancing the service quality of primary-care institutions. On the other hand, Ping An Diagnostics will procure state-of-the-art MR and CT equipment and recruit renowned specialists from tertiary Grade A hospitals to deliver high-value-added services.

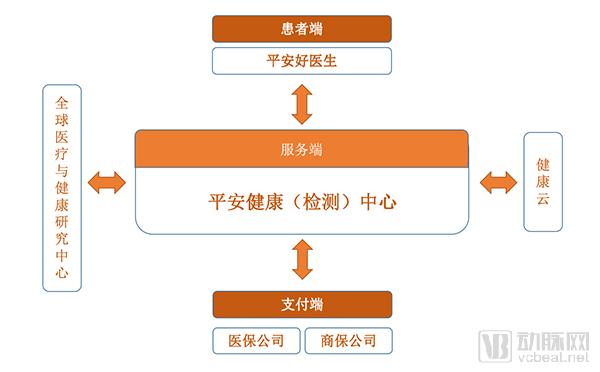

Structurally, Ping An connects the entire spectrum from the patient end to the payment end. At the patient end, Ping An Good Doctor serves as the portal, providing consultation and triage services, and referring patients requiring examinations to the Ping An Health (Testing) Center. The testing center is linked with medical insurance companies and Ping An’s commercial insurance, thereby establishing a rational payment infrastructure, reducing associated insurance costs, and enhancing the transparency of information flow. On the technical front, Ping An leverages its independent health cloud and the Global Medical and Health Research Center for support, enabling services such as imaging diagnosis, medical laboratory testing, precision examinations, specialist outpatient clinics, extended treatment, remote image interpretation, and multidisciplinary team (MDT) consultations.

According to VCBeat, Ping An Health (Testing) Center may use standard 1.5T MRI scanners for its routine services, while its high-net-worth services will feature cutting-edge imaging equipment such as the Discovery MR 3.0T and Revolution CT. Meanwhile, Ping An Testing will full-time hire highly experienced physicians from Grade A tertiary hospitals.

During the construction phase, Ping An Health (Diagnostic) Centers will establish connections with more hospitals. Patients will learn about the existence of Ping An Health (Diagnostic) Centers from their physicians and be referred to these imaging centers. Furthermore, Ping An’s commercial insurance business will create additional opportunities for non-public healthcare providers. Under Ping An’s guidance, independent imaging centers may gain support from the national medical insurance system within a relatively short period.

Overall, Ping An’s greatest advantage lies in its comprehensive industry chain, with Ping An Leasing covering the procurement of medical devices for diverse needs upstream, and Ping An Good Doctor and Ping An Insurance providing support on the patient side downstream. As a result, independent imaging centers will transcend the awkward position of being merely an intermediate link in the industry chain.

On the other hand, the construction of 1,000 imaging centers will bring economies of scale to this sector. Under current circumstances, the cost of building a single standalone imaging center is approximately RMB 80 million, making it difficult for conventional enterprises’ assets to support the construction of a large number of centers and thus hindering the formation of a chain model. Currently, there are fewer than 30 self-built standalone imaging centers. Now, leveraging the backing of Ping An Group, Ping An Health (Testing) Center can significantly scale up this figure.

During the development of Ping An Health (Diagnostic) Centers, the aforementioned issues related to data, promotion, and talent can be resolved. For some existing independent imaging centers, this trend may bring more benefits than drawbacks, particularly for those offering personalized services. After entering the Chinese market, Japan’s CVIC International began providing patients with high-end diagnostic services and medical tourism services. For CVIC, this sector is more conducive to the expansion of its service offerings.

As a provider of Yimai Yangguang’s imaging cloud services, Xi’an Yinggu’s CEO, Huang Yedong, stated: “Ping An has the capacity to empower an industry, and its entry is beneficial for the sector as a whole. Companies like Yimai Yangguang, which cater to patients in second- and third-tier cities, do not face direct competition due to differences in their business models. With Yimai Yangguang’s model now widely implemented, it is poised to become a significant force in the future.”

Every emerging sector encounters various forms of resistance in its early stages, and independent imaging centers are no exception. In the absence of precedents, companies have had to gradually accumulate operational experience for independent imaging centers, seeking a path forward through continuous trial and error.

Zhao Bin, Director of the Shandong Medical Imaging Research Institute, told VCBeat that, in his view, independent imaging centers represent an excellent practice; outsourcing this service can streamline hospital structures and facilitate hospital operations.

He also noted that the key to the success of independent imaging centers lies in whether they can provide patients with high-value, high-quality services. Positioned in the midstream of the industry chain, independent imaging centers must have renowned physicians on board to gain bargaining power; otherwise, it is difficult to achieve differentiation. Of course, policy support is also indispensable.

Now that the policies are in place, Ping An Testing’s entry has injected vitality into the entire sector. Once the Ping An ecosystem is fully established, the landscape of independent medical imaging in China may be transformed entirely.

If Ping An achieves its goals within five years, a well-deserved giant will emerge in this market. China’s independent medical imaging market will forge a path distinctly different from those of the United States and Japan, writing its own remarkable chapter in a unique way.