Monogenic Genetic Disease Testing Reports: The Next Billion-Dollar Market Takes Off

BGI

Scientific and Technological Service Provider and Precision Medical Service Operator

In the first three quarters of 2018, biotechnology was one of the two most active sectors in global financing. In China, the NIPT industry experienced rapid growth, giving rise to two publicly listed companies in 2018 and sparking a wave of enthusiasm in the genetic testing sector.

In the current genetic testing market, direct-to-consumer genetic testing and non-invasive prenatal testing (NIPT) account for the majority of market share. In addition to continuing to increase their share with existing products, identifying new product growth drivers will also be a top priority.

VCBeat believes that genetic testing for monogenic disorders, as a relatively mature technology in the current gene sequencing industry, is highly likely to receive policy support in the next phase and become a new hotspot in the sector. With nearly 10 million couples registering for marriage annually in China, these newlyweds will constitute the target population for monogenic disorder genetic testing, creating a market opportunity worth tens of billions of yuan.

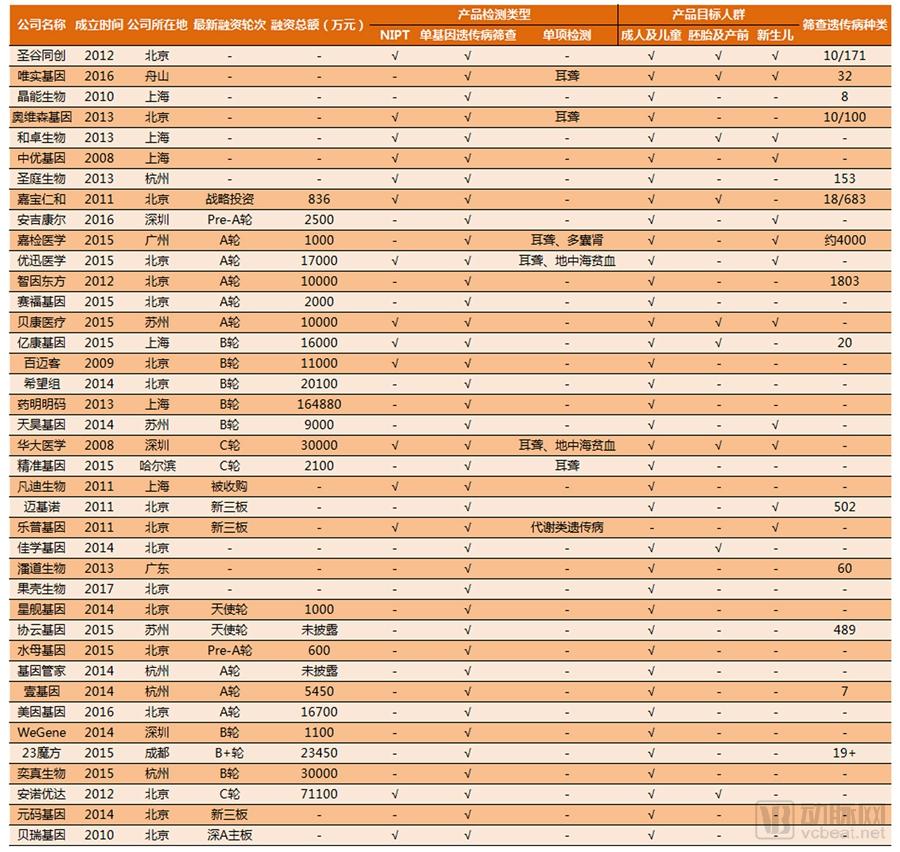

According to monitoring by the VCBeat knowledge base, 36 companies in China currently provide genetic testing services for various types of monogenic hereditary diseases, including leading firms such as BGI and Berry Genomics.

This is the first in the industry specifically targetingReport on the Genetic Testing Industry for Monogenic Disorders, welcome to join the discussion.

Report Key Highlights:

1. ReportA statistical analysis was conducted on 36 companies in China currently involved in genetic testing for monogenic disorders, covering aspects such as financing status, product types, target populations, types of screened genetic diseases, and pricing. Subsequently, data analysis was performed based on the collected statistics to objectively describe the current market landscape of the monogenic disorder genetic testing industry.

2. The market size of the genetic testing industry for monogenic hereditary diseases was estimated based on data such as product pricing, target population, and projected penetration rate.

3. Based on an understanding and analysis of the industry, we propose a key insight: the premarital check-up and newborn markets deserve focused attention.

The following is an excerpt from the report

I. Introduction to Monogenic Genetic Disorders

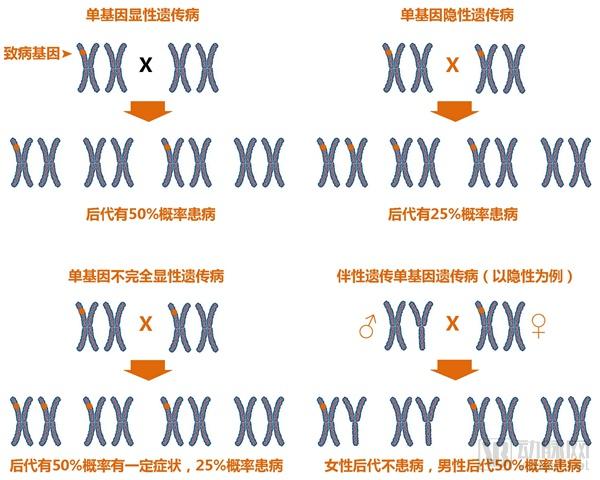

Monogenic genetic disorders, also known as Mendelian genetic disorders, refer to hereditary diseases primarily governed by a single pair of alleles. They are further classified into autosomal dominant monogenic disorders, autosomal recessive monogenic disorders, and monogenic disorders with incomplete dominance.

Figure 1. Inheritance patterns of monogenic disorders

II. The Importance of Monogenic Disorder Testing

Figure 2. Prevention and control strategies for monogenic disorders at different stages

Optimal childbearing and eugenics have always been the top priority in China’s fertility policy. As a category of genetic disorders amenable to large-scale screening, monogenic diseases have not received sufficient attention in terms of prevention. Many families adopt the attitude of “What difference does knowing make? We’ll have the baby anyway,” and thus forgo monogenic disease testing. However, with advances in single-cell sequencing technology and non-invasive prenatal testing (NIPT), most monogenic genetic disorders can now be prevented and managed at multiple stages, including preconception, during pregnancy, and postpartum.

III. Development of Detection Methods for Monogenic Disorders

Figure 3: Development of Detection Methods for Monogenic Disorders

In 1963, the detection of phenylketonuria using the BIA method marked the beginning of newborn screening for genetic disorders. Subsequently, corresponding screening methods were developed for monogenic diseases such as thalassemia, hearing impairment, and favism. The advancement of microarray technology and the emergence of next-generation sequencing (NGS) have transitioned genetic testing from research laboratories to the commercial market. Compared with first-generation sequencing, NGS has significantly improved efficiency while reducing costs. Furthermore, liquid biopsy has enabled the latest genetic testing technologies to be ultimately transformed into accessible genetic testing products.

Now, only a few milliliters of saliva are required to perform personalized analysis of an individual’s genetic profile. Individuals can clearly determine whether they are carriers of monogenic disorders and, if so, which specific conditions they carry. Based on the genetic test results of both partners, it is easy to assess the probability that their offspring will inherit a monogenic disorder, thereby enabling effective prevention and control of such conditions in children.

IV. Industry Chain Structure and Characteristics of Genetic Testing for Monogenic Disorders

Figure5: Industry Structure of Monogenic Genetic Disease Testing

Note: The ranking of enterprises is not in any particular order; the size of the icons is for graphical purposes only and carries no special significance.

Currently, the upstream segment of the monogenic disease genetic testing industry is basically dominated byIllumina holds a monopoly, with its market share exceeding 80%; Roche and Thermo Fisher Scientific’s products also have significant coverage. These three major companies collectively account for over 99% of the overall sequencing market; the remaining market is divided among other foreign companies such as Oxford Nanopore and PacBio.

Midstream companies purchase sequencing instruments, chips, and other products from upstream suppliers to provide single-gene genetic disorder testing services to downstream end-users. Some of these companies, such as BGI and Berry Genomics, have followedThe NIPT sector has seen the emergence and growth of companies that have already achieved a certain scale, while the majority are smaller firms established around 2014. These companies cater to different customer segments by offering diverse services, including personal genetic interpretation, broad-spectrum single-gene disorder testing, targeted single-gene disorder testing, and preimplantation genetic screening for IVF embryos.

The downstream user base for monogenic disorder genetic testing is extensive, encompassing not only adults and children but also embryos from in vitro fertilization (IVF), pregnant women undergoing prenatal screening, and newborns. Clients with different profiles have varying service requirements, which necessitate distinct technical approaches; consequently, most companies offer only a subset of these services.

V. Market Size of Genetic Testing for Monogenic Disorders

Current single-gene disorder testing products primarily serve adults and children. From the perspective of preventing single-gene disorders, carrier screening for newlywed couples is most critical to their prevention and control. Raising awareness among prospective parents about the risks of single-gene disorders and providing them with reliable testing services could constitute the largest market segment for single-gene disorder detection. According to the China Health Statistics Yearbook published by the National Health Commission in recent years and the Statistical Bulletin on Social Service Development issued by the Ministry of Civil Affairs, the annual number of marriage registrations in China has remained atWith approximately 10 million couples, or about 20 million individuals, recommended to undergo premarital check-ups, and given that the current market price for single-gene disorder testing products is around RMB 2,500, the potential market size for single-gene disorder testing is estimated at approximately RMB 7.5 billion, assuming a product penetration rate of 15%.

Figure 6: Market Size Forecast for the Monogenic Disease Testing Industry

In addition, the market for monogenic disorder testing also encompasses other segments such as embryo screening for in vitro fertilization (IVF), prenatal testing, and newborn screening; therefore, its potential market size isThere is still room for growth beyond 7.5 billion, with projections exceeding 10 billion.

VI. Market Landscape of Genetic Testing for Monogenic Disorders

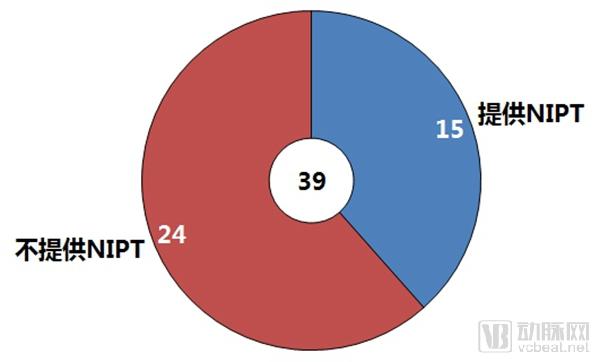

Figure 7:Statistics on 39 Companies in China Providing Genetic Testing Services for Monogenic Disorders

Currently, many companies in the Chinese market are already offering genetic testing services for monogenic hereditary diseases. VCBeat has compiled statistics on those currently providing genetic testing for monogenic hereditary diseases.39 companies, and an analysis of the overall data was conducted.

Figure8: Monogenic Genetic DisordersGeneProvided by the Testing CompanyNIPT Service Overview

Of the 39 companies, 15 offer NIPT services concurrently, accounting for 38.4% of the total. Among the 12 companies established more than five years ago, 9 provide NIPT services, representing 75% of this subgroup. Of the 27 companies founded within the past five years (in 2013 or later), only 6 offer NIPT services, constituting 22.2% of this group.

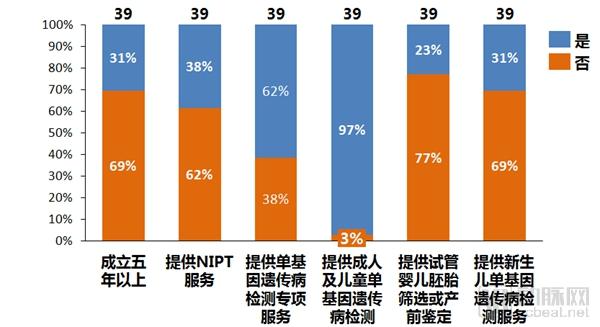

Figure9: Monogenic Genetic DisordersGeneService Overview of the Testing Company

Among the 39 companies, 24 offer specialized testing services for monogenic hereditary diseases, while the other 15 provide comprehensive consumer-grade genetic products, with monogenic hereditary disease testing being just one component.

Some companies offer specialized carrier screening for single-gene genetic disorders. These companies rarely directly targetIn the consumer market, sales are primarily conducted through collaborations with hospitals. Partnering with hospitals not only facilitates promotion but is also necessary because these tests require blood samples, which most users cannot collect on their own and thus need hospital assistance. Consequently, such companies maintain a relatively low online marketing presence and have limited public brand recognition, preferring instead to invest in R&D for new testing products to expand their business scope. Additionally, specialized single-gene genetic disorder testing products are priced relatively high, at approximately RMB 2,500, but offer comprehensive coverage, typically screening for hundreds to even thousands of single-gene disorders.

Another segment of companies generates revenue by offering personal genetic testing services, such as23mofang and WeGene. Unlike targeted testing for single-gene genetic disorders, personal genetic testing services require only a saliva sample. Consequently, companies such as 23mofang and WeGene primarily serve direct-to-consumer (DTC) customers. The choice of sample type also results in lower accuracy and limited coverage for the single-gene disorder component of personal genetic testing products, meaning these results should be used for reference purposes only. For more accurate genetic information, targeted carrier screening for single-gene genetic disorders is recommended.

VII. Competitive Factors in the Market for Genetic Testing of Monogenic Disorders

In the competitive landscape of the genetic testing market for monogenic disorders, there are both universal competitive factors, such as price and technology, and unique competitive factors, such as target population, efficiency, and accuracy. In our study, we categorize competitive factors related to a company’s core capabilities into the horizontal dimension, and those related to market strategy into the vertical dimension, to further discuss the competitive dynamics in the monogenic disorder market.

Figure10: Competitive Factors in the Monogenic Disease Testing Industry

In the longitudinal dimension, there are significant differences in the performance of various companies. In terms of solution customization, some companies choose to offer personal genetic interpretation products that include single-gene disorder testing, which we can refer to as“Bundled” sales products; while another segment of companies opts to offer standalone genetic testing products for single-gene disorders. Bundled products are relatively more affordable, with 23mofang’s pricing starting as low as RMB 399; in contrast, standalone products offering broader testing coverage command higher prices, typically around RMB 2,500. Most bundled products target only adults and children, whereas standalone products feature detailed categorization, with specialized offerings emerging for distinct populations such as IVF embryos, prenatal fetuses, and newborns. Companies occupy different market niches based on the services they provide, engaging in focused competition within each specific segment.

VIII. Future Market Development of Monogenic Genetic Disorders

Current market development for single-gene disorder genetic testing is concentrated in two areas: adults and children, and embryo screening for in vitro fertilization (IVF). There is insufficient development in the markets for prenatal diagnosis and newborns. Prenatal diagnosis of single-gene disorders has not yet reached a technical level suitable for large-scale commercialization; therefore, the newborn market is likely to become the next competitive frontier for single-gene disorder genetic testing.

For newborn screening, partnering with hospitals and postpartum care centers may represent the most effective competitive strategy. Newborn genetic disease testing currently performed in hospitals still relies on outdated blood-based biomarker assays. In comparison, genetic testing requires smaller sample volumes, offers higher throughput and accuracy, and is priced affordably for the majority of consumers, making it a viable replacement for traditional blood-based biomarker methods.

With the continuous advancement of genetic research and sequencing technologies,With advancements in PCR technology, disease-related genetic testing products are poised to become mainstream in the market. Currently, many companies are offering genetic susceptibility testing products for conditions such as cancer and cardiovascular diseases. As disease-related genetic testing matures, integrated comprehensive disease gene testing products will emerge. These highly integrated solutions hold greater potential to dominate the mainstream market.

IX. Case Studies of Genetic Testing Companies for Monogenic Disorders

Declaration: The cases selected in this report are intended to cover the enterprises and product types currently existing in the genetic testing industry for monogenic disorders, and do not necessarily represent the leading companies in the industry.

1. BGI Medicine

Company Profile

Company Name | Establishment Date | Latest Financing Round | Total Financing Amount | NIPT | Single-Gene Disorder Testing | ||

Adults and Children | Embryonic/Prenatal | Newborn | |||||

BGI Medical | 2008 | Series C | ¥300M | √ | √ | √ | √ |

Financing History

Funding Round | Financing Time | Financing Amount | Investors |

Undisclosed | 2010.01 | Undisclosed | Sequoia Capital China |

Undisclosed | 2014.01 | Not disclosed | Kaiwu Investment, Fenxiang Investment |

Series A | 2014.05 | ¥100M | SoftBank China, Greenwoods Asset Management, Shenzhen Capital Group |

Series B | 2014.05 | ¥100M | Cowin Capital |

Series C | 2014.06 | ¥100M | SV Angel, Shenzhen Capital Group |

BGI Medical was established inEstablished in 2008, it is a medical testing service company under the BGI Group. The company has completed five rounds of financing to date; the details of the first two rounds were not disclosed, while the subsequent Series A, B, and C rounds all took place between May and June 2014, with each round raising RMB 100 million.

As one of the most renowned high-tech biotechnology enterprises in China, BGI has consistently remained at the forefront of the nation’s gene sequencing industry, despite being mired in continual controversy. ThereforeIn 2008, BGI Medicine was established, and BGI began providing genetic testing services to the public.

According to BGI2018 Semi-Annual Report: In the first half of 2018, BGI Genomics reported revenue of RMB 1.141 billion, with reproductive health services generating RMB 622 million, accounting for 54.5% of total revenue. Reproductive health services remain BGI Genomics' primary revenue source, encompassing products such as NIFTY and various single-gene genetic disorder testing panels.

Product Overview

Product Name | Applicable Population | Test Sample | Product Type | Product Price |

AnYunKe Carrier Screening for Monogenic Disorders | Adults and Children | Saliva | Broad-Spectrum Testing | 2600 |

Thalassemia Gene Testing | Adults and Children, Prenatal, Neonatal | Blood | Single-Item Testing | Unknown |

EmbryoSeq-PGD: Preimplantation Genetic Testing for Monogenic Disorders | IVF Embryo | Embryonic Single Cell | Broad-Spectrum Testing | Unknown |

Genetic Testing for Monogenic Disorders | Adults and Children | Saliva | Broad-Spectrum Testing | Unknown |

Newborn Deafness Gene Testing | Newborn | Blood | Single-Item Test | Unknown |

Anxinke Newborn and Pediatric Genetic Testing | Children, Neonates | Blood | Personal Genetic Testing | 6800 |

BGI Medical offers the most comprehensive range of single-gene genetic disorder tests among all companies. Its products cover all age groups, with corresponding testing solutions for single-gene disorders from embryos to adults. Special emphasis is placed on the period from preconception to the neonatal stage, strictly controlling the occurrence of single-gene genetic disorders and supporting eugenics and healthy childbirth.

The monogenic disease genetic testing provided by BGI Clinical can detect genes involved inOver 3,000 diseases and more than 4,000 genetic mutations are covered. The sequencing coverage exceeds 95%, with an accuracy rate of 99%. Target gene fragments are captured via probe hybridization, followed by magnetic bead-based enrichment of the probe-hybridized DNA. The enriched DNA is then sequenced to determine the presence of genetic mutations.

2.23mofang

Company Profile

Company Name | Establishment Date | Latest Financing Round | Total Financing Amount | NIPT | Single-Gene Genetic Disorder Testing | ||

Adults and Children | Embryonic/Prenatal | Newborn | |||||

23mofang | 2015 | Series B+ | ¥234.5M | - | √ | - | - |

Financing History

Funding Round | Financing Date | Financing Amount | Investors |

Angel Round | 2015.03 | ¥5M | Chende Capital, SoftBank China, Yahui Precision Medicine Fund, Bencao Capital, Matrix Partners China |

Pre-A Round | 2016.01 | ¥7.5M | German Business Singularity, Yahui Precision Medicine Fund, Matrix Partners China, Hanwang Technology |

Series A | 2017.01 | ¥20M | German Meridian Singularity, Yahui Precision Medicine Fund, Fenghou Capital, Hanwang Technology |

Series B | 2017.08 | ¥40M | Hanwang Qichuang, Yahui Precision Medicine Fund |

Series B+ | 2018.03 | ¥100M | Singularity Capital, Fenghou Capital |

Series B+ | 2018.05 | ¥62M | Houfeng Capital |

23mofang, established in 2015, is a genetic testing service provider offering consumer-grade genetic products. Since its inception, 23mofang has completed six rounds of financing, with the total amount exceeding RMB 200 million.

23mofang truly gained widespread recognition through its price war with WeGene. In August 2017, 23mofang reduced the price of its genetic testing service from RMB 999 to RMB 499. Shortly thereafter, WeGene lowered its prices to match 23mofang’s level. Then, in June 2018, 23mofang further cut prices, bringing its product down to as low as RMB 299. Although there have been no public reports on 23mofang’s revenue, the price reductions proved highly attractive to a large number of undecided consumers. Currently, the price listed on 23mofang’s official website has risen back to RMB 399.

23mofang’s technological foundation is derived from Thermo Fisher Scientific, with both its sequencing instruments and custom chips sourced from Thermo Fisher. In an industry landscape dominated by Illumina’s monopoly, Thermo Fisher remains one of the few upstream sequencing suppliers capable of securing a notable market share. Consequently, 23mofang’s test results carry considerable credibility.

Product Overview

Product Name | Applicable Population | Test Sample | Product Type | Product Price |

23mofang Genetic Testing | Adults and Children | Saliva | Personal Genetic Testing | ¥399 |

Although23mofang does not offer specialized testing for single-gene genetic disorders. However, its test reports do include partial descriptions of carrier status for certain genetic conditions, such as thalassemia, favism (G6PD deficiency), and albinism. These generally cover most common single-gene genetic disorders. Nevertheless, for single-gene disorders characterized by highly variable mutation sites and potential polygenic influences, such as hereditary deafness, 23mofang’s test reports do not contain relevant information.

Overall,The comprehensive personal genetic testing product offered by 23mofang primarily aims to help individuals gain a deeper understanding of themselves through genetic interpretation, thereby providing a basis for formulating personalized health plans. Due to limitations in the capacity of microarray-based detection, such products cannot sequence and compare all known genetic loci, but only cover a subset of loci associated with monogenic hereditary diseases. Therefore, although these products can serve as a platform for monogenic hereditary disease testing, they fall short of specialized monogenic hereditary disease tests in terms of accuracy and coverage.

>>>>Table of Contents

1. Introduction to Monogenic Disorders

1.1 Monogenic Genetic Disorders

1.2 Common Monogenic Genetic Diseases in China

1.3 Incidence of Common Monogenic Genetic Disorders

2. Monogenic Genetic Disease Testing

2.1 Importance of Monogenic Genetic Disorder Testing

2.2 Development of Detection Methods for Monogenic Disorders

2.3 Policy Support for Genetic Disease Testing

2.4 Genetic Testing for Monogenic Disorders and Cancer Susceptibility Genes

3. Market for Genetic Testing of Monogenic Disorders

3.1 Composition and Characteristics of the Industry Chain

3.2 Market Size of Genetic Testing for Monogenic Disorders

3.3 Market Landscape of Genetic Testing for Monogenic Disorders

3.4 Competitive Factors in the Market for Genetic Testing of Monogenic Disorders

3.5 Future Market Development of Monogenic Genetic Diseases

4. Case Studies of Genetic Testing Companies for Monogenic Disorders

4.1 BGI Medical

4.2 23mofang

4.3 WuXi AppTec NextCODE

4.4 Guoke Gene

4.5 Shenggu Tongchuang

5. Overview of Investment and Financing for Companies Involved in Genetic Testing for Monogenic Disorders

6. Summary of Views

The above content is from "Industry Research Report on Genetic Testing for Monogenic Disorders》Excerpt: To become an official VCBeat member, click here to accessFull Report。