Rehabilitation Healthcare Market Insight: U.S. Physical Therapy Exceeds $30 Billion with Community Clinics as the Dominant Model, While China’s Market Is Just Emerging

When it comes to the term “rehabilitation medicine,” it remains a relatively ambiguous concept in China, particularly unfamiliar to the general public. For instance, whether they are athletes prone to injuries from long-term training, urban white-collar workers who sit for prolonged periods, or elderly individuals suffering from chronic diseases, most people in China tend to seek treatment at major hospitals immediately after an accidental injury. Following medical consultation, they generally adhere to doctors’ advice to rest quietly at home and avoid physical activity. The traditional Chinese belief that “it takes 100 days to heal injuries to tendons and bones” is deeply ingrained; consequently, many find it difficult to imagine using “exercise” as a therapeutic approach for muscle damage and other sports-related injuries. At the current stage, when rehabilitation medicine has not yet been widely adopted in China, such an approach may even appear somewhat “absurd” to them. Therefore, the key to developing China’s rehabilitation healthcare industry lies in addressing public education and awareness, gradually enabling more people to recognize and accept the existence and necessity of rehabilitation medicine.

Although rehabilitative medicine is still a nascent field in its early stages of development in China, rehabilitation institutions are ubiquitous across the United States, on the other side of the Pacific. As of 2016, the U.S. rehabilitative medicine market was valued at approximately $20 billion; when long-term care is included, the overall market reaches as high as $200 billion, with per capita rehabilitation expenditures amounting to $800. What, then, are the underlying success factors behind such a vast market? What exactly are rehabilitative medicine and physical therapy? How have they developed in the United States? How many benchmark enterprises exist? What implications do these hold for the development of related industries in China? VCBeat will now reveal the answers.

What is Rehabilitation Medicine?

Source: Athletico Official Website, VCBeat

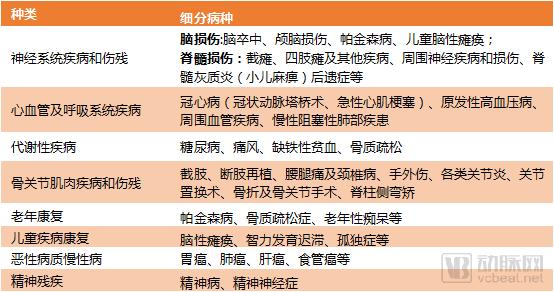

Rehabilitation medicine, together with preventive medicine, healthcare medicine, and clinical medicine, is collectively referred to as the “Four Major Branches of Medicine.” Rehabilitation medicine is an applied medical discipline focused on the rehabilitation of individuals with disabilities and patients. Its objective is to alleviate, compensate for, and reconstruct functional impairments through various interventions—including physical therapy, exercise therapy, activities of daily living training, skills training, speech therapy, and psychological counseling—thereby compensating for and rebuilding functional losses, and striving to improve and enhance overall human functioning. This encompasses the prevention, diagnosis, assessment, treatment, training, and recovery related to functional disabilities. Rehabilitation treatments can be categorized into six major types based on disease conditions: rehabilitation for neurological disorders (e.g., stroke), rehabilitation for musculoskeletal and joint diseases and disabilities (e.g., amputation, fractures), rehabilitation for cardiovascular and respiratory diseases, geriatric rehabilitation, pediatric rehabilitation, and rehabilitation for psychiatric disabilities.

Table: Classification of Rehabilitation Medical Services by Disease Type. Source: Public Information; Chart by VCBeat.

The Value of Rehabilitation Medicine

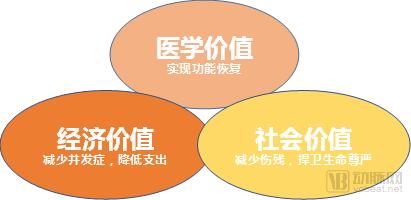

Rehabilitation medicine is not merely an adjunctive therapy in the public eye, but has been proven through practice to possess substantial medical, economic, and social value.

Figure: The Three Major Values of Rehabilitation Medicine, Graphic by VCBeat

First, rehabilitation medicine holds significant medical value. Rehabilitation helps patients heal from psychological and physical trauma, restore normal function, enhance work capacity, and improve quality of life. Furthermore, rehabilitation therapy is a crucial component of chronic disease management, effectively reducing the risk of recurrence and improving treatment outcomes. For instance, the disability rate following stroke in the United States is approximately 30%, whereas in China it exceeds 75%, primarily due to the lack of rehabilitation care for patients.

Secondly, rehabilitation medicine possesses significant economic value. It accelerates the recovery of physical functions, reduces recurrence rates and complications, and lowers overall treatment costs. Total expenses decline significantly following rehabilitation therapy, showing a month-on-month downward trend. Furthermore, in the United States, where rehabilitation services are covered by nearly all major insurance plans, this aligns well with the broader trend of controlling healthcare expenditures under medical insurance systems.

Furthermore, rehabilitation medicine holds certain social value from a humanistic perspective. It reduces disability, restores functional impairments in patients, and upholds the dignity of life.

The Development History of Rehabilitation Medicine in the United States

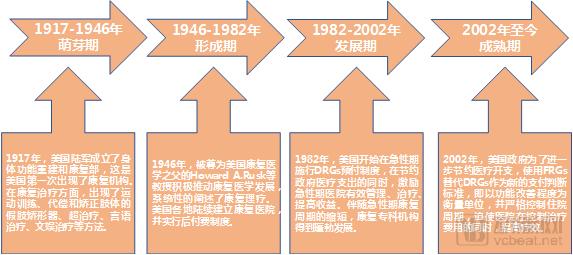

The first rehabilitation institution emerged in the United States in 1917, marking over a century of development that has progressed through four major phases: inception, formation, expansion, and maturity.

Figure: Development History of the Rehabilitation Medical Industry in the United States, Source: Shenwan Hongyuan Research, VCBeat

These four major development periods were also accompanied by continuous changes in the U.S. healthcare payment system. The reforms in the healthcare payment system have greatly promoted the development of the rehabilitation medical industry, with specific impacts evolving through three stages. The first stage was the “Fee-for-Service” period implemented from the 1960s to the 1980s. The second stage, spanning from the 1980s to the early 21st century, was characterized by the coexistence of “Prospective Payment System/Per-Item Payment.” It was precisely this dual payment system that facilitated the growth of the U.S. rehabilitation sector. The third stage is the comprehensive “Prepayment System” period implemented since 2002.

1. Phase I: Fee-for-Service (1965–1982)

In the United States, the earliest payment model was fee-for-service, under which costs for inpatient rehabilitation and acute care hospitalization were not separated. This is a retrospective payment system, where settlement is made according to reimbursement standards and ratios after healthcare providers have delivered services. A drawback of this model is that patients are viewed as sources of hospital profit, leading to overutilization of medical services and making it difficult to control healthcare costs in the long run.

2. Phase II: Acute Care Hospitals Adopt DRGs (Diagnosis-Related Groups) (1982–2002)

Since 1982, the U.S. Medicare program has implemented a prospective payment system based on Diagnosis-Related Groups (DRGs) for acute care. DRGs are a typical representation of prospective payment systems, under which health insurance agencies determine a relatively fixed payment standard to reimburse healthcare providers before services are rendered. At that time, DRGs were still in their infancy and were primarily indicated for acute conditions with clear diagnoses, relatively consistent treatment methods, stable treatment protocols, and shorter hospital stays. Due to the specific characteristics of four categories of care—including inpatient rehabilitation and mental health disorders—such as prolonged hospital stays, complex treatments, and high costs, the DRG-based payment method was not adopted; instead, the fee-for-service model continued to be used.

DRG policies have served as a catalyst for enhancing efficient hospital referrals and advancing the development of rehabilitation medicine, ushering in an explosive golden era for the U.S. rehabilitation industry. Within ten years of DRG implementation, the number of rehabilitation beds doubled, while specialized rehabilitation institutions and long-term care facilities proliferated rapidly.

Phase III: The Prepayment Era of FRGs (Post-2002)

After 2002, a prospective payment system based on Functional Related Groups (FRGs) was implemented for patients in the post-acute phase, using functional improvement as the primary basis for insurance reimbursement. FRGs classify patients according to the disability and impairment criteria of the International Classification of Impairments, Disabilities, and Handicaps (ICIDH). Patients are then stratified into several groups based on their functional status and age, utilizing data and information from the Uniform Data System for Medical Rehabilitation (UDSMR). The medical cost standards for each classification level within each group are calculated, and a fixed payment rate is determined in conjunction with the length of stay, which is then prospectively paid to rehabilitation medical institutions.

The implementation of Functional Related Groups (FRGs) has a twofold impact on rehabilitation medicine. First, it determines prospective reimbursement amounts based on medical conditions, thereby reducing the incidence of excessive rehabilitation. Second, reimbursement is contingent upon tangible functional improvements in patients. This incentivizes hospitals to prioritize functional recovery, guiding rehabilitation institutions to develop and refine their services to meet patients’ diverse needs across different levels and stages of treatment, thus facilitating timely, proactive, and seamless patient referrals. In summary, driven by the prospective payment system, improving patient function and ensuring smooth referral transitions have become the primary objectives for hospitals.

In summary, the development and improvement of the U.S. rehabilitation medical service system are inseparable from the guiding role of the health insurance payment system.

Current Status of Rehabilitation Medicine Development in the United States

A well-established three-tier rehabilitation medical network is a common model for rehabilitation healthcare systems in developed countries and regions. The three-tier rehabilitation healthcare system in the United States is broadly categorized into acute-care rehabilitation facilities (including inpatient rehabilitation facilities), post-acute care facilities (including skilled nursing facilities, etc.), and long-term care facilities (such as outpatient rehabilitation clinics and community-based clinics).

In the United States, various rehabilitation institutions have clearly defined roles and scopes of practice. Differential reimbursement policies have established a clear division of labor among these facilities, effectively alleviating patient pressure on emergency hospitals. This article focuses on physical therapy, a primary modality within rehabilitative medicine that is service-oriented. Consequently, most physical therapy providers in the U.S. operate as community-based clinics within the three-tier healthcare network.

It is worth noting that,The United States Advocates the Concept of Early Rehabilitation Integration. In the United States, early rehabilitation intervention is manifested as bedside rehabilitation during the acute phase, which is implemented by non-rehabilitation departments in acute care hospitals. This approach provides patients with moderate-intensity rehabilitation therapy at an early stage, ensuring timely initiation of rehabilitative care.

Figure: The Three-Tier Rehabilitation Medical System in the United States, VCBeat

Under the construction of a three-tier rehabilitation medical network, there exists a smooth and efficient referral mechanism.In the United States, once patients have passed the acute phase, physicians assess their condition using the Functional Independence Measure (FIM) and promptly transfer them to inpatient rehabilitation units or specialized skilled nursing facilities for rehabilitation. Those who do not require inpatient rehabilitation are transitioned to community-based services as soon as possible. This function-based evaluation system ensures seamless coordination across care settings, integrating them into a cohesive whole.

Furthermore, the development of the United States’ robust and advanced rehabilitation healthcare system is inseparable from its emphasis on talent cultivation.The vast majority of rehabilitation therapies are conducted in accordance with evidence-based medicine standards, grounded in a medical understanding of human movement. According to Shenwan Hongyuan Research, there are 761 institutions of higher education in the United States offering programs in rehabilitation medicine. Among these, the physical therapy specialty, which encompasses exercise rehabilitation, features high entry barriers and attracts high-caliber students. These programs are typically housed within comprehensive universities, with some even established within medical schools, and are offered at the graduate level. Students undergo a curriculum similar to that of medical students, comprising four years of foundational coursework followed by three years of specialized professional study, and must obtain licensure before practicing. In the United States, rehabilitation therapy is generally delivered on a one-on-one basis, particularly in the management of chronic diseases, where exercise and nutritional interventions are employed as first-line treatments, with pharmacological therapy reserved for cases where these initial measures prove ineffective. Physical therapists are primarily categorized into Exercise Physiologists (EPs) and Physical Therapists (PTs). As of 2016, there were more than 60 physical therapists per 100,000 people nationwide in the U.S., a ratio that fully meets the talent demands of the rehabilitation healthcare industry.

In addition to the government's emphasis on talent development,U.S. residents hold rehabilitation therapists in high regard; these professionals enjoy a relatively high social status and are widely respected in American society.Unlike in the Chinese market, where rehabilitative medicine has not yet gained widespread public consensus and remains a relatively unfamiliar and ambiguous concept, the situation in the United States is markedly different. There, rehabilitative care is as common and familiar as clinical medical treatment, with community-based rehabilitation clinics visible throughout neighborhoods. Additionally, rehabilitation therapists enjoy considerable income; for instance, physical therapists earn annual salaries ranging from $50,000 to $100,000, depending on their level of expertise.

Physical Therapy, a Key Branch of Rehabilitation Medicine, Boasts a Market Size Exceeding $30 Billion

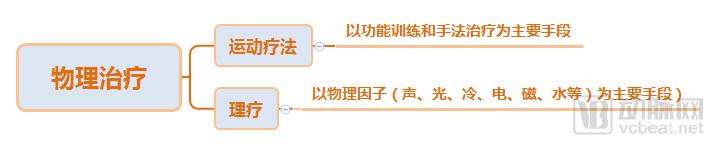

Physical Therapy Is an Important Branch of Rehabilitation Medicine, primarily utilizing physical agents such as sound, light, cold, heat, electricity, and force (movement and pressure) for therapeutic purposes. It employs non-invasive, non-pharmacological interventions to address local or systemic functional impairments or pathologies, aiming to restore the body’s original physiological functions. Physical therapy is a crucial component of both modern and traditional medicine. It can be categorized into two major types: one that primarily relies on functional training and manual therapy, also known as therapeutic exercise or kinesiotherapy; and another that primarily utilizes various physical agents (such as sound, light, cold, heat, electricity, magnetism, and water), also referred to as physiotherapy.

Figure: Major Categories of Physical Therapy, Chart by VCBeat

As a key modality of rehabilitative care, physical therapy attracts a broad patient population, including individuals with sports injuries, older adults suffering from pain, and those in a suboptimal health state. The mature U.S. physical therapy market still holds significant potential for value growth.

According to research by Jakari Care, the U.S. physical therapy market is highly mature, with an estimated total market size of $30–33 billion and an annual growth rate of approximately 3%–5%. The market comprises 60,316 rehabilitation enterprises, including approximately 16,000–18,000 physical therapy clinics. Outpatient clinics are estimated to account for $8–12 billion of the total physical therapy market.

The top five institutions by market share are:

Source: Jakari Care study; graphic by VCBeat

Overall, the physical therapy industry remains relatively fragmented, with no single dominant player. As shown in the table above, the top five companies in the U.S. physical therapy market collectively hold only around 20% of the market share. However, in recent years, mergers and acquisitions have become increasingly frequent in the U.S. physical therapy market, intensifying the trend toward industry consolidation.

According to a physical therapy research report by Capstone Partners LLC, there were 46 major mergers and acquisitions in the U.S. physical therapy market from 2015 to March 2017. The largest transaction was the acquisition of Concentra by Select Medical and WCAS in 2015, with a deal value of $1.055 billion.

Major Business Models in the U.S. Physical Therapy Market

First, let us examine the traditional rehabilitation industry chain. Overall, the traditional rehabilitation industry chain can be divided into three segments:

Upstream: Rehabilitation equipment manufacturers, rehabilitation drug manufacturers

Midstream: Sports medicine or rehabilitation departments in general hospitals (with a severe shortage of sports rehabilitation service capacity), and specialized rehabilitation institutions

End Users: Consumer Segment—Competitive athletes and public sports rehabilitation; Business Segment—Sports event medical support, professional sports teams, etc.

Physical therapy is service-oriented, representing the midstream segment of the industry chain. Companies in this field, whether operating online or offline, are primarily service-focused.In the United States, the business model of operating outpatient clinics is relatively common, with a small number of comprehensive inpatient rehabilitation hospitals as well.Taking the top five companies in the U.S. physical therapy market share listed in the previous table as an example, four of them operate solely through community clinics, while only one company, Select Medical, adopts a dual model combining rehabilitation hospitals with community clinics. This corroborates the earlier point that within the U.S. three-tier rehabilitation healthcare network, physical therapy services, due to their inherent nature, are predominantly delivered through community clinics at the downstream end of the system. This structure is supported by a well-established referral mechanism in the United States, where rehabilitation hospitals and outpatient clinics are interconnected, ensuring smooth patient referrals. For instance, most patients at our physical therapy clinics are referred from upstream orthopedic rehabilitation hospitals. The advantages of community clinics lie in providing patients with a better care experience through a more personalized approach, while also offering greater operational flexibility, which facilitates customer acquisition and enhances client retention.

Source: Corporate official websites, annual reports of listed companies, VCBeat

Case Analysis of the US Market

As previously mentioned, the U.S. physical therapy industry remains highly fragmented, with no single dominant player. ATI and Athletico, two of the top five market leaders, adopt a similar business model that combines large-scale corporate resources with a closed-loop network of community clinics. This section analyzes these two companies to examine the current state of development of the community clinic model in the U.S. physical therapy sector.

1. ATI

Image source: Facebook

ATI Physical Therapy, founded in 1996 and headquartered in Illinois, USA, is a private chain of outpatient rehabilitation clinics dedicated to providing high-quality comprehensive rehabilitation services. ATI offers holistic, goal-oriented treatment plans tailored to individual patient needs. It stands out in the rehabilitation industry through its one-on-one care model. ATI Physical Therapy has been recognized by Advance Magazine as one of the “Best Physical Therapy Practices” in the United States, demonstrating excellence in patient care and growth, employee training, community service, clinical facilities, and corporate expansion. Since its inception, ATI has evolved from focusing primarily on rehabilitation services for injured workers to becoming a specialized private rehabilitation clinic offering multidisciplinary services, including physical therapy, sports medicine, hand therapy, women’s health, and pediatric health. Currently, ATI operates nearly 700 clinics across 24 U.S. states, making it one of the largest private chains in the physical therapy sector nationwide. According to Crunchbase data, ATI achieved $15.1 million in revenue in 2017, accounting for approximately 3.5% of the national physical therapy market share.

Since opening its first clinic in Willowbrook, Illinois, in 1996, ATI has remained true to its original mission, dedicating itself to providing “one-on-one” care that makes patients feel the warmth of home. As previously mentioned, the U.S. rehabilitation system is primarily structured into a three-tier framework. ATI has targeted the downstream segment of this tiered system, focusing on community-based clinic rehabilitation. The advantage of community clinics lies in their ability to offer a better patient experience through a more “personalized” approach. Furthermore, community clinics possess greater operational flexibility, facilitating customer acquisition and enhancing client retention. Practice has proven that this asset-light business model is conducive to continuous replication and expansion. From the single clinic opened in 1996, ATI expanded to cover nearly 700 clinics across 24 U.S. states by 2018. Over 22 years, it achieved a remarkable transformation from one to 700 locations, with an average annual expansion rate of nearly 32 clinics. This astonishing growth speed benefits from the brand advantages and corporate resources backing ATI—specifically, a model combining large-corporate resources with small-clinic operations. In doing so, ATI has pioneered a new path for rehabilitation groups, achieving nationwide coverage through a network of small clinics.

Figure: Schematic diagram of ATI patient consultation, source: ATI official website

In addition to the continuous replication and expansion of its own branded clinics, ATI has also demonstrated strong proficiency in leveraging capital instruments for business innovation and growth, expanding through acquisitions of other clinics. According to incomplete statistics, ATI completed a total of 11 acquisitions between 2006 and 2016, indicating frequent activity in the capital markets.

Figure: ATI’s Acquisition History (Incomplete Statistics), Source: ATI Official Website

To enhance the professionalism of its therapies, ATI has established an internal research department. Under the leadership of Dr. Chris Stout, ATI aims to improve patient outcomes through basic science, research, and evidence-based medicine, thereby making its therapeutic practices more scientific and professional—a hallmark of its unique approach.

Moreover, ATI has introduced the ATI Patient Outcomes Registry to provide a platform for collaborative research and to advance the sharing of clinical knowledge. As an industry first, the ATI Patient Registry represents a unique milestone in the field of rehabilitative care, offering groundbreaking guidance for future evidence-based scientific treatments. It employs a unique approach to collect and observe epidemiological clinical data, provides innovative methods for physical therapy, facilitates rapid access to knowledge for users, and enables the comprehensive collection of feedback on patient diagnostic outcomes. This initiative delivers a clearer understanding than ever before of the rehabilitation process and its impact on patients’ quality of life.

Perhaps due to the inherent characteristics of the industry, although the rehabilitation medical system in the United States is quite mature, the market is dominated by strong institutions such as rehabilitation hospitals, while community clinics and similar entities often receive less favor from capital. ATI is no exception; over its 22 years of operation, it has completed only four rounds of financing, with a cumulative total of $256 million (this amount excludes the latest round, as the funding size was not disclosed), and it has not yet gone public on the capital markets.

Figure: ATI’s Financing History, Source: Crunchbase

2. Athletico

Image source: Facebook

Founded in 1991 and headquartered in the Greater Chicago area of the U.S. Midwest, Athletico Physical Therapy has rapidly evolved over the past twenty-five years from a single orthopedic rehabilitation clinic into a major national healthcare provider, operating more than 450 clinics across eleven states. With a team of over 1,500 clinical and administrative professionals, Athletico offers more than 40 specialized services in rehabilitation, outreach, and fitness. Its expert team includes physical therapists, occupational therapists, certified athletic trainers, personal fitness trainers, strength and conditioning specialists, and massage therapists. Athletico also provides functional assessments and improvement services for workers. Additionally, Athletico delivers athletic training, physical and occupational therapy, and fitness services to more than 150 affiliated organizations, including high schools, universities, and numerous professional sports teams in Chicago.

In the words of founder Mark, Athletico’s business model is “community healthcare in a retail setting.” This entails leveraging the strength of the Athletico brand to facilitate marketing through community-based locations and expanding gradually via clinic outlets that embody “retail” characteristics. Furthermore, Athletico operates 24 hours a day, providing continuous care to community patients regardless of the time of day or night. Meanwhile, it actively participates in community public-welfare initiatives to enhance familiarity and recognition among local residents.

Figure: Athletico conducts community activities. Source: Twitter

In addition to reaching individual consumers, Athletico is also actively expanding its base of institutional (B2B) clients. Athletico has partnered with professional sports teams at various levels, universities and high schools, a wide range of sporting events, and performing arts groups, serving as their official provider of athletic training and physical therapy services. Athletico supports these organizations through multiple channels, including on-site consultations and injury assessments, physical therapy, athletic training, manual therapy, and educational programs.

Figure: Athletic Sports Partner, Source: Official Website of Athletic

Athletico also prioritizes internal research to enhance the professionalism and accuracy of patient care. It has established an in-house research team and actively collaborates with universities and research institutions to conduct advanced studies in rehabilitation. Additionally, Athletico partners with Focus on Therapeutic Outcomes Inc. (FOTO), a leading provider of rehabilitation outcomes databases, to measure and compare patient outcome statistics from thousands of clinics and millions of patients across the United States. By analyzing these data, Athletico is committed to optimizing patient treatment protocols, thereby embodying the forefront of its core values.

In terms of clinic expansion, Athletico primarily adopts a replication model for its branded clinics, supplemented by limited mergers and acquisitions in the capital market to integrate industry resources. The most notable event was the 2014 announcement of the acquisition of Accelerated Rehab, the largest rehabilitation chain in the Chicago area. Following the merger, the two companies were integrated under Athletico’s physical therapy brand, creating a powerful alliance that significantly expanded Athletico’s brand influence in the Chicago region.

By deeply cultivating the community clinic model within retail environments, Athletico has absorbed a broad consumer base of local residents while continuously expanding its official sports partnerships to secure institutional clients such as professional sports teams, thereby penetrating the B2B sector. This dual-track approach, serving both community and institutional clients, has enabled Athletico to steadily accumulate its customer base and professional network. Over the past 25 years, the company has maintained strong growth momentum and has become the largest healthcare giant in the Chicago area. It holds approximately 2.5% of the national physical therapy market share in the United States, ranking fourth nationwide, behind Select Medical (9.4%), ATI (3.5%), and US Physical Therapy (3.2%). Additionally, Athletico has demonstrated solid profitability. According to Crunchbase statistics, Athletico achieved revenue of $10 million in 2017.Financing details have not been disclosed.。

Overview of the Development of Rehabilitation Medicine in China

Rehabilitation medicine in China started relatively late.Modern rehabilitation medicine was first introduced to China in the early 1980s. The development of China’s rehabilitation industry has broadly undergone three stages.

In 1988, the completion of the China Rehabilitation Research Center marked a milestone in the history of rehabilitation industry development in China, signaling the official commencement of rehabilitation undertakings in the country. During the Eighth Five-Year Plan period, numerous rehabilitation institution construction projects were approved and initiated across China.

Phase II: Pilot Promotion Phase (1995–2005). During the Ninth and Tenth Five-Year Plan periods, China’s rehabilitation industry and institutional infrastructure achieved substantial development. More than twenty provinces, autonomous regions, and municipalities successively established rehabilitation service institutions, and expanded the coverage of rehabilitation services by implementing a model that integrated rehabilitation services with key projects.

Phase III: Comprehensive Development (2005–Present). During this period, the state has not only continued to prioritize the expansion of rehabilitation coverage and the growth in the number of rehabilitation institutions, but also placed equal emphasis on improving the quality of rehabilitation services. Building on comprehensive promotion, greater attention has been devoted to enhancing the coordination and sustainability of the rehabilitation sector. The 2008 Wenchuan earthquake spurred rapid development in China’s rehabilitation medical services. In 2012, China issued its first specific policy document on rehabilitation work—the “Guiding Opinions on Rehabilitation Medical Services during the 12th Five-Year Plan Period”—elevating rehabilitation to a national strategic priority.

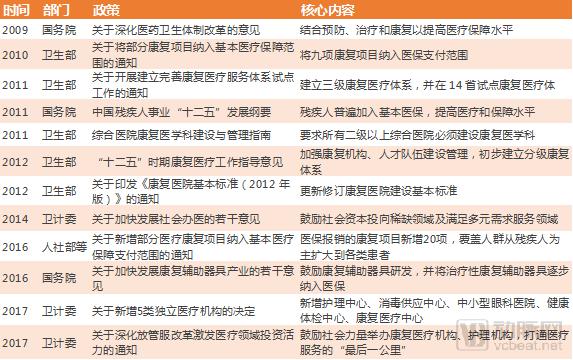

The following is a list of policies issued by relevant authorities in recent years regarding the development of rehabilitation:

Figure: Government Policies on Rehabilitation Medicine Over the Years. Source: Government Documents, VCBeat

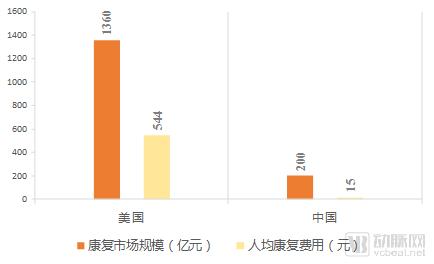

Compared with the relatively mature rehabilitation medical systems in developed countries abroad, China's rehabilitation medical industry remains somewhat nascent, as evidenced bySmall Scale of the Rehabilitation Industry, Weak Public Awareness of Rehabilitation, and Severe Imbalance Between Supply and DemandAs of 2016, the market size of China’s rehabilitation medical industry was RMB 32 billion, with a per capita expenditure of RMB 15. In the same period, the U.S. rehabilitation medical market reached as high as USD 20 billion, with a per capita expenditure of USD 80. When long-term care is included, the U.S. rehabilitation market expands to USD 200 billion. There is a substantial gap between China and the United States in terms of current market size, indicating significant room for growth in China. Furthermore, orthopedic combined with neurological rehabilitation accounts for 60%–70% of China’s rehabilitation medical market. This segment offers relatively standardized, replicable processes and low risk, representing the future direction of development for China’s rehabilitation medical industry.

Figure: Comparison of the Rehabilitation Market Size Between China and the United States, Source: Shenwan Hongyuan Research, VCBeat

Benchmarking against the physical therapy market within the U.S. rehabilitation system, China’s counterpart primarily refers to the sports rehabilitation market (with exercise therapy being the primary modality of physical therapy).Sports rehabilitation is an important branch of rehabilitative medicine, essentially integrating “sports” with “medical care.” As a multidisciplinary specialty, it employs various approaches—including equipment-based rehabilitation, manual therapy, and active patient exercises—to repair sports injuries and restore motor function. Its target populations include individuals with musculoskeletal injuries and post-orthopedic surgery patients; those with chronic diseases; as well as the elderly, adolescents, and individuals in a suboptimal health state.

As previously analyzed, the dominant business model in the U.S. physical therapy market is the asset-light community clinic model operated under large corporate entities. In contrast, China’s sports rehabilitation market (noted earlier as the primary focus of China’s physical therapy sector) is predominantly composed of small startups. Most of these enterprises adopt a hybrid online-to-offline (O2O) service model, while purely offline physical rehabilitation providers are relatively scarce. This trend aligns with China’s current landscape of a highly developed internet economy, where leveraging digital platforms facilitates customer acquisition and efficiently drives traffic to offline facilities.

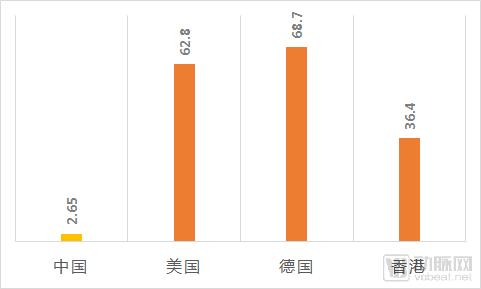

Additionally,The shortage of talent is also a major factor limiting the development of sports rehabilitation in China.In China, there are only 128 undergraduate programs related to Rehabilitation Therapy and Sports Rehabilitation. In comparison, the United States has 219 such programs, Germany has 280, and Japan has 249. At the master’s and doctoral levels, educational resources in China are even more scarce. According to publicly available data, there are currently approximately 36,000 certified rehabilitation therapists in China. Based on international standards, this translates to 2.65 physical therapists per 100,000 population. In contrast, the average in North America and Europe is 60 per 100,000 population, with the United States at 62.8, Germany at 68.7, and Hong Kong at 36.4 per 100,000 population.

Figure: Comparison of the Number of Physical Therapists per 100,000 Population in China and Developed Countries (Regions), VCBeat

With the rise of China’s sports industry and nationwide fitness initiatives, cases of sports-related injuries, conditions, and even sudden cardiac death during exercise are on the increase, driving growing demand for sports rehabilitation. Public data indicate that approximately 500 million people in China currently engage in regular physical exercise. Conservative estimates from industry experts suggest that around 20% of these individuals experience varying degrees of injury or pain each year, meaning that roughly 100 million people require treatment and services for sports-related injuries and conditions.Currently, the sports rehabilitation market in China has a theoretical potential to reach a scale of approximately RMB 50 billion.

Insights from the Development of Rehabilitation Medicine in the United States for China's Market Growth

In the U.S. market, rehabilitation medicine has reached a relatively mature and well-developed stage. In contrast, China’s sports rehabilitation sector remains in its early stages, with significant untapped market potential. This “gold mine” of rehabilitation calls for more pioneers to explore its opportunities. However, several challenges must be addressed: limited public awareness, a shortage of qualified professionals, incomplete medical insurance policies, and high rehabilitation costs.

Based on the above analysis of the U.S. market, VCBeat draws the following insights, hoping to provide valuable references for the development of this industry in China.

First, strengthen public awareness education and popularize the concept of rehabilitation to enable more members of the general public to recognize and accept the existence and necessity of rehabilitative medical care.

Second, improve the medical insurance system, expand coverage for rehabilitation medical services, and reduce patient costs.

Furthermore, emphasis should be placed on the cultivation of rehabilitation professionals, and the qualification access system for rehabilitation therapists should be improved.

Finally, improve the construction of a three-tier rehabilitation medical network and establish an efficient and interconnected referral mechanism, with particular emphasis on building and expanding community clinics at the downstream end of the three-tier network. Community clinics offer the advantages of asset-light operations, easy replicability, and effective patient acquisition.