PBM in China: Opportunities Through Local Innovation

PBM (Pharmacy Benefit Management), which translates directly to pharmaceutical benefit management, made its way from the United States to China around 2010 and has roughly undergone three stages of development: “emergence,” “dormancy,” and “revival.”

When PBMs first entered the market, the industry’s expectation was that “stones from other hills may serve to polish the jade of this one.” During their period of stagnation, the prevailing view was that “oranges grown south of the Huai River remain oranges, but those grown north of it become trifoliate oranges.” With their recent resurgence, greater emphasis is being placed on “localization” and “China-style innovation.”

PBMs mediate among numerous stakeholders—pharmaceutical companies, insurers, healthcare providers, pharmacies, and patients—to optimize diagnostic, treatment, and medication pathways, striving to minimize healthcare expenditures while ensuring therapeutic efficacy. In China’s rapidly reforming healthcare market, where stakeholder interests are even more intricate, only innovation can break the deadlock; thus, PBMs are once again held in high expectation.

This article explores the exploratory practices of the PBM business model in China and is divided into three parts:

1. A Detailed Explanation of PBM: More Than Just Cost Control

2. PBM Practice: Localized Innovation

3. The Future of PBMs: Role Reallocation

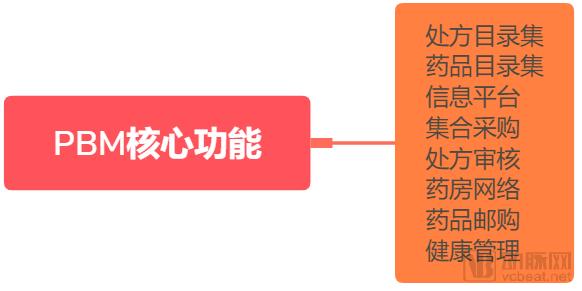

Pharmaceutical Benefit Management (PBM) models are not complex in principle. According to the definition by the American Pharmacists Association, PBM is a specialized third-party healthcare service that comprehensively manages medical services, particularly medication use, through measures such as prescription management, optimization of drug access channels, differentiated cost-sharing ratios, and health management. This approach helps optimize medication structures and achieve rational cost control.

VCBeat Graphic

PBM emerged in the United States in the late 1960s, coinciding with the invention of plastic insurance cards. In the 1970s, the rudiments of prescription drug utilization review appeared. During the 1980s, this model further evolved, establishing PBM as a cornerstone in the management of outpatient prescription medications.

Since the 1980s, the PBM industry has experienced rapid growth driven by two major factors: first, the rising demand for cost containment amid surging healthcare service and prescription drug expenses; second, the advent of the “golden age” of drug discovery, which brought a large number of new drugs to market each year, necessitating institutions to help payers track the launch and utilization of these new therapies and balance the selection between older and newer medications based on metrics such as efficacy and cost.

As of today, players in the U.S. PBM market can be broadly categorized into three types: first, PBMs embedded within insurance companies, such as Optum, the PBM subsidiary of UnitedHealth Group; second, PBMs operated by retail pharmacy chains, such as Caremark, owned by CVS Health; and third, independent PBMs, such as Medimpact.

Another noteworthy point is the increasing concentration of PBM companies in the U.S. market. The industry was highly fragmented in the 1990s, but entered a peak period of consolidation around the year 2000. CVS’s acquisition of Caremark in 2007 is regarded as the starting point for cross-industry integration. Subsequently, CVS further acquired Aetna, a commercial health insurer, for nearly $70 billion. Currently, Cigna is seeking to acquire ESI, leaving very few independent PBM companies remaining.

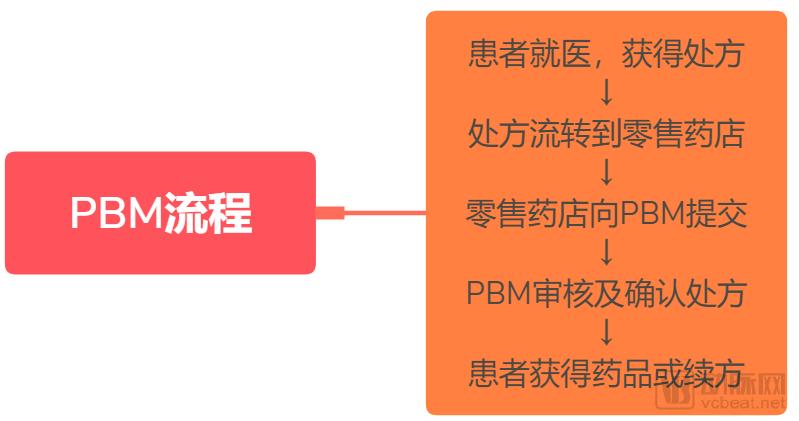

A typical PBM business process is as follows: A patient seeks medical care at a hospital, where a prescription is issued; the prescription is transmitted to a pharmacy, which then submits it to the PBM. The PBM reviews the prescription based on insurance product requirements and clinical rules, returns the adjudication results to the pharmacy, and the pharmacy dispenses the medication to the patient.

VCBeat Graphic

Of course, the above is only a relatively simplified process. In actual business operations, Pharmacy Benefit Managers (PBMs) have become an integral part of the pharmaceutical supply chain. They participate in centralized drug procurement to secure discounts through volume-based pricing; establish central warehouses; and provide mail-order pharmacy services for patients with chronic diseases requiring long-term prescriptions via their own or partnered pharmacy networks. Patients can directly renew their prescriptions simply by placing orders via phone or online.

Although the concept of Pharmacy Benefit Management (PBM) has been introduced to China for many years, the industry’s understanding of the PBM business model remains relatively narrow, with the concept largely confined to cost containment. Shi Mengmeng, General Manager of Medimpact China, and Liu Zeyuan, Senior Investment Manager in the Healthcare Group at Easy Capital, both emphasized to VCBeat that the functions of PBM extend far beyond mere cost control.

“PBM’s initial function was to enable the interconnectivity of prescription information. It subsequently evolved to include prescription review, achieving cost control on the pharmaceutical side while ensuring safety, efficacy, and economic efficiency. This was followed by the development of mature third-party pharmaceutical services, such as assisting insurers in building pharmacy networks, securing drug discounts, providing mail-order services, and distributing new and specialty drugs, as well as designing new insurance products and conducting market analysis based on data analytics,” said Shi Mengmeng. She added that PBMs provide diversified services tailored to the varying needs of insurers and patients.

Liu Zeyuan stated, “There are misconceptions within the industry regarding Pharmacy Benefit Management (PBM), with many viewing it merely as an information technology system for medical cost containment, whether in a SaaS model or other forms. This perception differs significantly from mature PBM business models, as cost containment is only one of PBM’s functions. The core function of PBM should be to provide centralized medication supply based on long-term, continuous, personalized, and regular medication data from patients with chronic diseases, which is the most economically efficient approach.” In other words, PBM should be an efficient pharmaceutical supply solution driven by the needs of both patients and insurance companies.

Amid a landscape dominated by the basic medical insurance fund, with commercial insurance accounting for a modest share and interests deeply intertwined, exploring a viable commercial pathway is an imperative challenge for all companies. In a system where the basic medical insurance fund plays the predominant role, monetization through “surplus sharing” is difficult to achieve; this has not been, nor will it be, the primary revenue source for Pharmacy Benefit Managers (PBMs) in China.

It is already a widespread industry consensus that Pharmacy Benefit Management (PBM) must be localized and adapted to China’s specific conditions. Below, we introduce two cases of localized PBM innovation—Medici and KeyShiQuan. Interestingly, these two companies have taken distinct paths, exploring greater possibilities for the development of PBM services.

Medtronic: Crossing Oceans to Deepen Its Roots in the Chinese Market for 7 Years

Shi Mengmeng, General Manager of Medimpact China, told VCBeat that Medimpact was founded in 1989 by pharmacists and other healthcare professionals. It is the largest non-publicly traded pharmacy benefit management (PBM) company in the United States that does not sell any medications. Eight of the top ten insurance companies in the U.S. have chosen Medimpact as their PBM partner. Medimpact serves over 50 million insured members, manages $18 billion in prescription drug expenditures, and processes more than 400 million claims reviews annually.

In 2011, Medidata began preparing to enter the Chinese market. “When we started exploring the domestic market, there was a widespread lack of awareness about Pharmacy Benefit Management (PBM) in the industry. Our entry point was to address the needs of public hospitals, which required internal monitoring of prescription appropriateness and the generation of reports for submission to regulatory authorities,” said Shi Mengmeng.

Subsequently, Meideyi spent over three years building a database encompassing diagnoses, prescriptions, and data on more than 170,000 pharmaceutical products, and collaborated with insurance companies, medical institutions, and dental practices to pilot its PBM (Pharmacy Benefit Management) services.

Currently, Meideyi’s business operations in China primarily consist of four segments: hospital-based rational and compliant healthcare solutions, dental benefit solutions, localized PBM services, and one-stop pharmacy benefit services for Chinese nationals overseas. Among these, the localized PBM services mainly include modules for cost control, quality and safety supervision, and reporting and analytics.

Services Provided by Medtronic China

Source: Medtronic

Starting with dental benefits management represents a relatively “compromise” solution. Dentistry is a highly commercialized sub-sector of medical services in China, characterized by high standardization and robust commercial insurance coverage. From the perspective of dental institutions, the introduction of Pharmacy Benefit Management (PBM) concepts is also welcomed, as it enables the provision of professional, effective, and cost-efficient dental treatment solutions for patients. Meideyi collaborates with insurance companies to design dental products in advance based on clinical incidence data. During the course of treatment, they provide “second opinion” consultations tailored to individual patient cases based on their specific dental symptoms, thereby accumulating experience in localized Dental Benefits Management (DBM).

“Identifying pain points” is the core logic driving Meide Yi’s business expansion. For instance, hospitals seek greater convenience in claims processing; by joining a PBM (Pharmacy Benefit Manager) network, they can achieve real-time claims settlement. Insurance companies, meanwhile, aim to enhance their health management service capabilities and collaboratively explore new channels, all while pursuing long-term cost containment as a primary objective.

Shi Mengmeng told VCBeat that after seven years of exploration, Meideyi has become a pioneer in localized PBM (Pharmacy Benefit Management) services. The company has built a localized PBM engine, reviewed more than 35 million prescriptions for multiple hospitals, and reached cooperative consensus with several insurance companies to explore the implementation of localized PBM solutions.

“From a lack of conceptual understanding to gradual comprehension, the development of PBM in China has indeed been quite tortuous. As a global company, Medici also launched its operations in the Middle East during the same period and has since become the leading PBM provider in that region. Although it entered the South African market later than the Chinese market, it has still managed to rank among the top three locally. ‘Fortunately, we are currently in discussions with several state-owned commercial insurance companies regarding the phased implementation of localized PBM solutions. This is one of the positive signals for the industry,’ said Shi Mengmeng.”

“Not only between China and the United States, but in fact, the global healthcare industry faces common driving factors—such as population aging and rapidly rising healthcare expenditures—which are all favorable conditions for developing PBM businesses. Of course, given the vastly different national contexts of China and the United States, it is often not feasible to directly replicate the mature PBM business models from the U.S. market; adjustments must be made based on actual needs,” said Shi Mengmeng.

Shi Mengmeng also emphasized that Medidata has always maintained an open mindset in its strategic layout for the Chinese market. By providing PBM engines, solutions, and other services to numerous insurance companies and similar entities, Medidata aims to explore a localized PBM system tailored to China’s specific conditions, continuously enrich its PBM products and services, and further improve the healthcare benefits management ecosystem.

Keyshi Circle: From “Infrastructure” to Dual Drivers of “Prescription + Insurance”

Yao Shi Quan Cloud Health was established in July 2015 as a joint venture funded by Winning Health and Sinopharm Health. Its name is a homophone for “Pharmacy Affairs Circle” in Chinese. The company aims to integrate the pharmaceutical supply chain and the retail network of physical pharmacies, providing users with professional services in five key areas: online direct payment and claims settlement for medications, cloud-based prescription circulation services, direct drug supply, pharmacist services, and out-of-hospital medication distribution.

In August 2017, Keyshiquan secured nearly RMB 200 million in investment from numerous industry investors, including Winning Health, Sinopharm Health, Qianji Capital, and Zhizhong Investment (Supor Industrial Investment). Within just over two years, it has completed the integration and acquisition of nearly ten companies.

KeyWorld is the implementation platform for Winning Health’s “Cloud Pharmacy” strategy. As a leading domestic healthcare IT vendor, Winning Health has been actively laying out and transforming into the health services industry in recent years, building on its efforts to strengthen and expand its Healthcare Information Technology (HIT) business. The company aims to transition from software services to health services, with Cloud Medicine, Cloud Pharmacy, Cloud Wellness, Cloud Insurance, and an innovative service platform serving as the focal points of its transformation.

Zhou Shun, General Manager of KeyShiQuan, believes that the true implementation of PBM in China requires a solid foundation and supportive policies, such as a system for the circulation of electronic prescriptions, online claims processing information from insurers to pharmacies, and a conducive policy environment. Therefore, KeyShiQuan’s strategy is to adapt to local conditions, leveraging China’s existing software and hardware infrastructure to gradually implement a comprehensive pharmacy benefit management solution.

Zhou Shun told VCBeat that Yaoshi Circle’s “Cloud Pharmacy” strategy is primarily implemented in two steps. The first step involves building infrastructure centered on commercial health insurance. By leveraging the “Pharmacy Alliance” network of nearly 70,000 social pharmacies across China and integrating cost-control solutions required by insurers, it establishes an online direct-payment claims system for medications. This process accumulates data, enabling price discount negotiations with pharmacies and pharmaceutical companies based on the scale of managed insurance funds and pharmacy claim amounts. The second step targets opportunities arising from the “separation of prescribing and dispensing” and “outflow of prescriptions,” by establishing a third-party prescription sharing platform that connects hospital prescriptions with pharmacies. This achieves online direct-payment claims for prescription drugs, rational cost control, and cost optimization.

From the perspective of the payment environment, the total volume of commercial health insurance has grown rapidly in recent years. However, to date, reimbursement for many commercial insurance policies still relies solely on invoice-based claims, which is neither cost-effective nor efficient. KeyShiQuan’s solution is to establish a “Direct Billing Claims Platform” that connects pharmacies with insurance companies, creating a payment ecosystem centered around the “Key Card” to enable real-time claims settlement for insured members when purchasing medications. Currently, KeyShiQuan manages approximately RMB 3 billion in insured coverage.

Zhou Shun emphasized that without electronic prescriptions, the implementation of Pharmacy Benefit Management (PBM) in China would remain merely formalistic. Therefore, the establishment of a prescription platform is particularly crucial in China. Public medical institutions are the core sites where prescriptions are generated. With the implementation of policies such as “separation of prescribing and dispensing” and “outflow of prescriptions,” outpatient medication demand is gradually shifting from hospitals to community pharmacies. This transition from hospitals to pharmacies necessitates an independent information connectivity platform, a function that the Yaoshiquan Prescription Sharing Platform can fulfill. Yaoshiquan has also introduced blockchain technology to analyze medication patterns using authentic, large-scale prescription data, thereby exploring services such as pharmacy benefit management and centralized procurement.

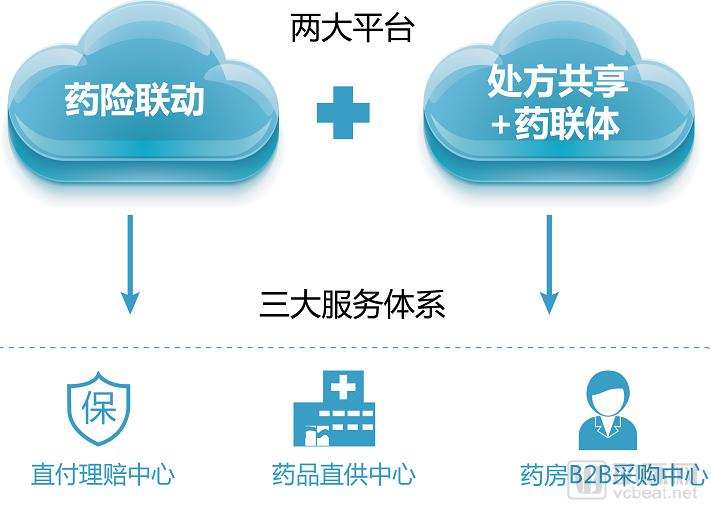

Zhou Shun told VCBeat that, at present, KeyWorld Circle mainly drives business development through two major systems—the online direct-payment claims platform and the prescription circulation platform—combined with three operational centers: the Direct-Payment Claims Center, the Direct Drug Supply Center, and the Pharmacy B2B Procurement Center.

Key World Business Model

Source: KeyShiQuan

“The essence of Pharmacy Benefit Management (PBM) lies in service. Through systematic operations, it helps patients conveniently access services and medications, comprehensively meeting their needs to facilitate gradual disease management and improve medication adherence. Furthermore, by providing multi-faceted services to insurance companies, pharmaceutical manufacturers, and pharmacies, PBMs effectively enhance the operational efficiency of the drug supply chain, thereby further optimizing the overall cost of delivering medications from manufacturers to patients.” Currently, we observe that certain local healthcare security administrations are implementing volume-based procurement, which actually signifies the gradual evolution of the PBM model in China. Zhou Shun believes that PBMs will continue to leverage resource synergy effects, fostering integration among medical care, pharmaceuticals, and health insurance to better manage and utilize medical resources and insurance funds.

China Renaissance is a leading new-economy investment bank and investment firm in China. Its core businesses include private equity financing, mergers and acquisitions, and asset management. A distinguishing feature of China Renaissance is its investment approach guided by rigorous industry research. In recent years, the firm has released multiple industry research reports covering sectors such as consumer entertainment, the new economy, and healthcare, among which the PBM industry research report is one.

Liu Zeyuan, Senior Investment Manager of the Healthcare Team at China Renaissance Capital, told VCBeat that their interest in the PBM (Pharmacy Benefit Management) industry is driven primarily by two factors. First, PBMs align with policy directions in China, including reforms to medical insurance payment methods, the implementation of tiered diagnosis and treatment, and the outflow of prescriptions from hospitals. Second, the U.S. PBM industry is witnessing large-scale mergers and acquisitions, with transaction values reaching hundreds of billions of yuan, leading to a restructuring of the competitive landscape. By examining domestic conditions alongside the evolutionary patterns of the U.S. market, investment opportunities may emerge.

China Capital observed that the development of the PBM (Pharmacy Benefit Management) business in China is still in a very early stage. Although commercial insurance institutions, healthcare IT vendors, and pharmaceutical distribution and retail enterprises are participating, their business models all face challenges.

For instance, commercial insurance providers often exclude middle-aged and elderly patients with chronic diseases from coverage; they possess limited bargaining power for drug pricing and weak capacity to handle prescriptions. Furthermore, their cost-containment objectives conflict with the interests of pharmaceutical companies, thereby failing to secure industry support. Healthcare IT vendors lack both drug pricing negotiation authority and prescription review rights, do not directly engage with consumers, and are not integrated with commercial insurance systems. Meanwhile, pharmaceutical distribution and retail enterprises remain distant from patients and face significant challenges in obtaining prescriptions.

Based on the analysis of the aforementioned players, iCapital points out that six key elements are required for the successful implementation of localized PBM businesses in China:

i. Strong drug price negotiation power: Ensures that PBMs can procure drugs from upstream pharmaceutical manufacturers at lower prices;

ii. Capability to prescribe and review prescriptions: Ensuring that PBMs can assist patients in rational medication use based on drug prescriptions;

iii. Sufficient patient volume: Ensure that the PBM has an adequate patient base and pharmaceutical sales volume;

iv. Mature supply chain system: ensuring efficient circulation of pharmaceuticals;

v. Comprehensive payment-side safeguards: Ensuring final payment for pharmaceuticals;

vi. Continuous medication data for chronic diseases: Ensuring PBMs understand the medication adherence patterns of patients with chronic conditions.

Based on the above inferences, China Renaissance Capital concludes that urban community-level health service centers are the most suitable settings for PBM implementation, as they simultaneously meet all the aforementioned criteria.

First, community health service institutions command substantial patient volumes, with nearly 800 million visits recorded at community health service centers in 2017. As healthcare reform policies—such as initial diagnosis at the primary care level, tiered diagnosis and treatment, and family doctor contract services—are continuously advanced, patient flow is increasingly shifting toward primary care facilities, driving higher traffic growth for community health service institutions.

Secondly, community health service institutions bear the primary responsibility for the prevention and control of chronic diseases. By unifying the procurement and reimbursement catalogs for commonly used medications during the stable phase of four major chronic conditions—hypertension, diabetes, coronary heart disease, and cerebrovascular disease—between large hospitals and primary healthcare institutions, eligible patients can benefit from two-month long-term prescriptions at primary healthcare facilities. This measure is expected to attract more patients with chronic diseases to obtain their medications within their communities.

Another point is that community health service institutions are the preferred destination for prescription outflow. Unlike pharmacies and other non-medical institutions, community health service institutions possess the capability to prescribe and review prescriptions. Furthermore, these institutions have relatively abundant physician resources, enabling them to better accommodate the needs of patients referred through triage.

Most importantly, community health service institutions have a comprehensive payment guarantee system. All such institutions are connected to the medical insurance network, allowing patients to use both their personal medical insurance accounts and pooled funds. For patients with chronic diseases, long-term medication needs result in ongoing pharmaceutical expenses, making reimbursement eligibility a critical factor in choosing where to obtain prescriptions. A robust payment guarantee system will thus drive higher patient traffic to community health service institutions.

The report concludes that the PBM model, which originated in the United States, has disrupted the traditional pharmaceutical supply system. Its core philosophy has shifted from a “supply-driven” model, where physicians prescribe medications, to a “demand-driven” model centered on patients’ medication adherence. By leveraging lean supply chain management and highly automated warehousing and logistics systems, the model streamlines pharmaceutical distribution channels and enhances inventory turnover efficiency. Meanwhile, it employs data-driven models to accurately predict patients’ medication needs, thereby meeting the long-term treatment requirements of chronic disease patients while reducing waste from unused medications. This approach truly delivers benefits to the public and aligns with the current direction of China’s healthcare reform policies.

Liu Zeyuan stated, “Centralized drug distribution is the core of the PBM business. Nearly all major U.S. PBM companies engage in centralized procurement and price negotiation, providing mail-order services to patients through central pharmacies. Only by participating in drug supply can monetization be achieved, thereby validating the business model.” Of course, this is not to say that the service-fee model is invalid, but rather that it is difficult to scale significantly.

Regarding investment opportunities in this sector, Liu Zeyuan stated that there are currently nearly 40,000 urban community health service institutions in China, which generally fall into two categories: clinics and centers. Most “clinics” are privately operated, whereas “centers” are public. For investors bullish on the prospects of community health service institutions, it is advisable to strategically invest in chained community health service providers. Such chain operations can enhance management standards and allow for early positioning in emerging business areas such as “outflow of prescriptions” and Pharmacy Benefit Management (PBM).

The rise of Pharmacy Benefit Managers (PBMs) in the United States is closely tied to the fact that healthcare expenditures are primarily borne by employers and commercial insurers, who have a direct incentive to control costs. Coupled with the high level of healthcare informatization in the U.S., PBM companies benefit from abundant data sources that support evidence-based medicine, thereby earning recognition from all stakeholders, including patients.

In fact, after PBM matured in the commercial insurance sector, it was also introduced into Part D of the U.S. “Medicare” program (the Medicare prescription drug benefit) to help manage healthcare costs. This demonstrates that whether a system is primarily driven by public or private insurance does not fundamentally affect the basis for PBM development.

Part of the reason why Pharmacy Benefit Managers (PBMs) face challenges in China is that the vested interests tied to prescriptions are difficult to disrupt. Although policies now mandate the separation of pharmaceutical sales from medical services, hospitals continue to derive substantial benefits from the prescription circulation process. At its core, a PBM’s function involves the review and modification of prescriptions; thus, it is difficult to persuade hospitals to relinquish this authority in the short term.

Beyond pharmacy benefit management, PBMs can collaborate with insurers to provide professional services such as health plan design, claims process optimization, and medical data support. This represents the future direction of PBM development.

“Healthcare Reform” Context: China’s Healthcare Industry Is Rapidly Evolving, with Foreign Best Practices Finding Fertile Ground for Pilot Implementation—Such as Adopting the U.S. PBM Model, Learning from Japan’s Tiered Management of Retail Pharmacies, and Promoting Scale and Intensification in Drug Production, Distribution, and Use.

Seeking opportunities amid change, rather than being constrained by the rigid frameworks of business models, is the foundation of innovation.