What Puzzle Pieces Is Tencent Still Missing in Healthcare After Pony Ma's Open Letter?

Next, we must serve as a “connector,” providing the richest “digital interfaces” for various industries to enter the “digital world”; act as a “toolbox,” offering the most comprehensive “digital tools”; and, more importantly, fulfill our role as an “ecosystem co-builder” by providing new infrastructure such as cloud computing, big data, and artificial intelligence. This will inspire every participant to engage in digital innovation and jointly build a “digital ecosystem community” with partners across all industries.

The above passage is excerpted from “Ma Huateng’s Open Letter: Helping the Real Economy Nurture More World Champions,” published on Tencent’s official WeChat account yesterday.

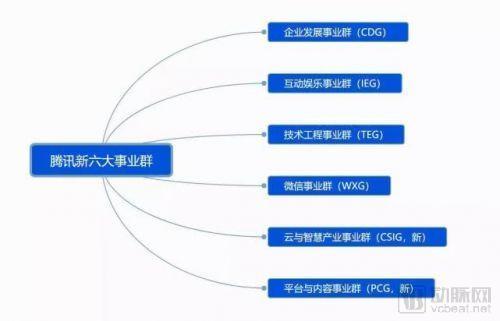

Recently, Tencent’s widely discussed reorganization into six business groups involved retaining the existing Technology and Engineering Group (TEG), WeChat Group (WXG), Interactive Entertainment Group (IEG), and Corporate Development Group (CDG), while integrating and establishing two new business groups: the Cloud and Smart Industries Group (CSIG) and the Platform and Content Group (PCG).

According to the official explanation, CSIG will integrate industry solutions across Tencent Cloud, Internet Plus, Smart Retail, Education, Healthcare, Security, and LBS, thereby driving the digital transformation of industries. Today, we will focus solely on Tencent Cloud, the core component of the newly established To-B business unit, the Cloud and Smart Industries Group (CSIG).

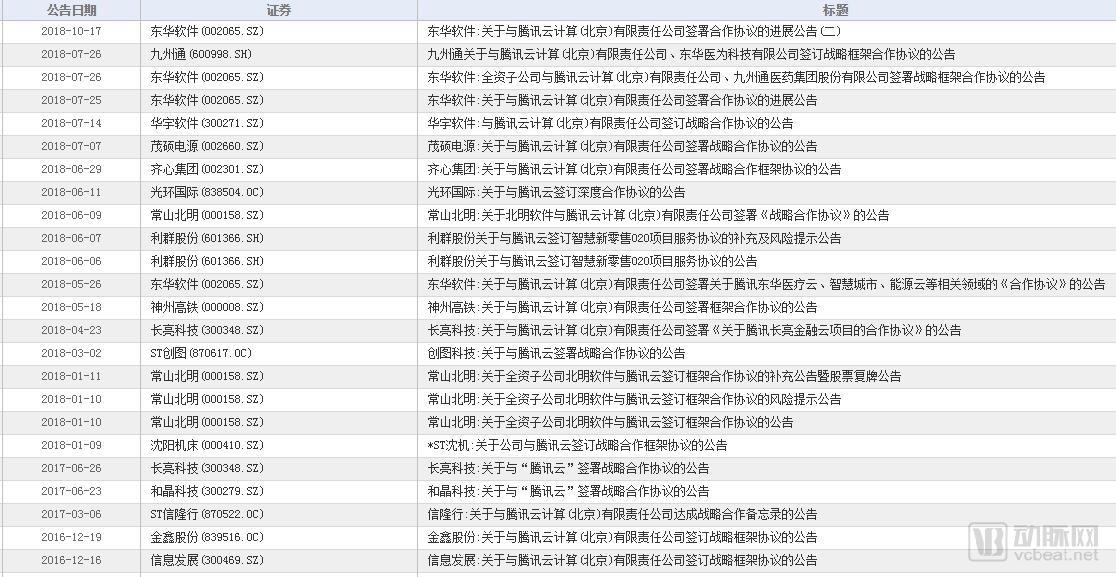

Source: Choice Financial Terminal

Source: Choice Financial Terminal

The chart above illustrates the listed companies that have partnered with Tencent Cloud over the past three years (note that as some partnerships were contracted directly with Tencent’s parent company, the data presented here reflects only a portion of the overall situation). Evidently, Tencent Cloud made significant efforts in its To-B business in 2018, signing agreements with 13 companies. By comparison, only four companies were signed in total from 2016 to 2017.

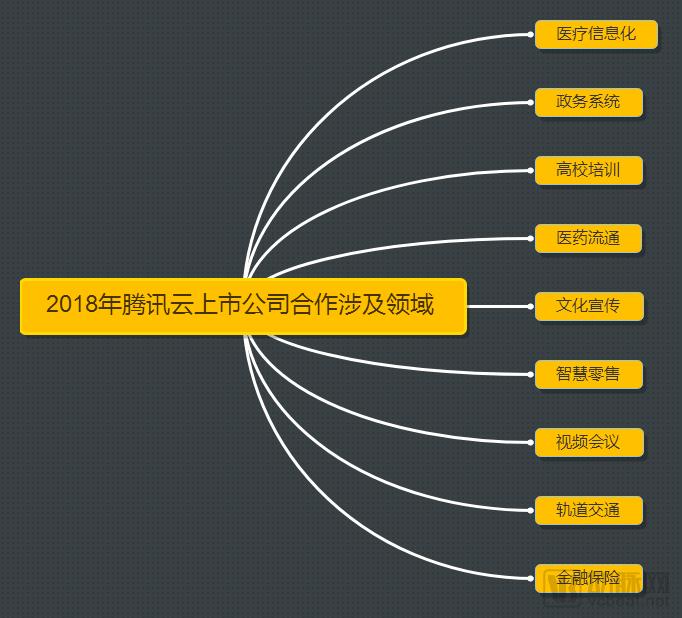

The collaboration primarily involves the following areas:

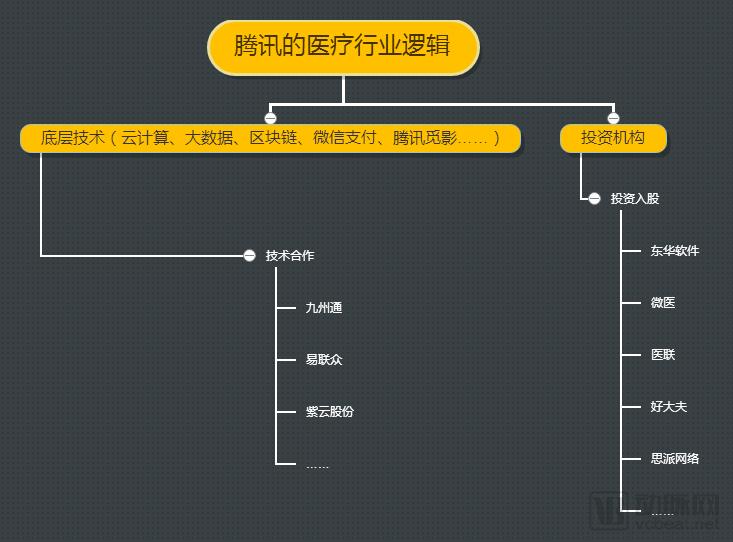

In terms of the number of enterprises, healthcare is one of the more active sectors, primarily involving pharmaceutical distribution (Jointown Pharmaceutical Group) and healthcare informatics (Donghua Software). Notably, in June 2018, Tencent announced a capital injection of RMB 1.266 billion into Donghua Chengxin, acquiring a 5% stake in Donghua Software. This move can be regarded as part of the background for their collaboration.

An analysis of DHC Software’s collaboration model reveals that traffic and resources form the foundation of the entire partnership.

Traffic Side: Donghua Yiwei, along with Shenzhen Tencent and its subsidiaries, has fully integrated Donghua Yiwei’s resources in the B-end (medical institutions) and G-end (Health Commissions, Healthcare Security Administrations) with Tencent’s substantial C-end traffic advantages, achieving complementary capabilities.

Resource Side: Donghua Yiwei’s application experience in hospitals, public health, medical insurance, and health management is integrated with Tencent’s technological capabilities in cloud computing, AI, big data, and blockchain to achieve technological interoperability.

Specifically, Donghua Yiwei, in collaboration with Tencent, has proposed the “One Chain, Three Clouds” strategy: using the Health Chain as a bridge to connect three clouds—namely, the Health Administration Cloud (serving government entities such as the National Health Commission and the National Healthcare Security Administration), the Medical Care Cloud (serving healthcare institutions of all levels and types on the B2B side), and the Personal Health Cloud (serving patients on the consumer side).

Meanwhile, both parties jointly implemented the “One Chain, Three Clouds” strategy by establishing the Health Chain Application Alliance and launching six major solutions: the Regional Healthcare Consortium Solution, the Medical Insurance Collaboration Solution, the Medical Union Cloud Solution, the Smart Hospital Solution, the Cloud HIS Solution, and the Internet + Healthcare Solution.

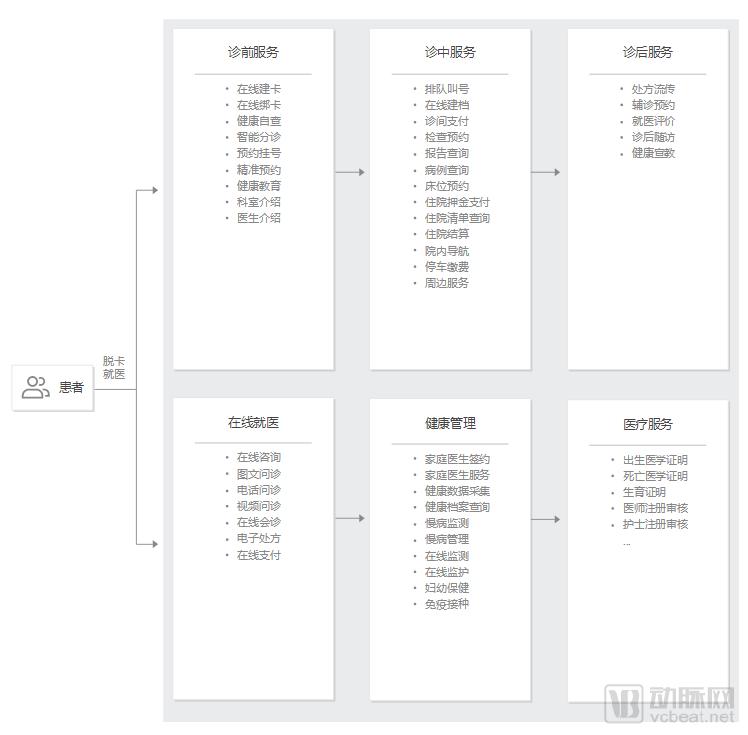

Under this collaboration model, what technical support can Tencent Cloud actually provide? After reviewing Tencent Cloud’s official materials, VCBeat found that the offerings mainly consist of Smart Healthcare Cloud and Smart Medical Services. The Smart Medical Services include the following components:

Additionally, VCBeat has learned that Tencent Cloud’s healthcare solutions actually integrate products and services from Tencent Cloud, WeChat, Miying (Tencent MIYING), Tencent Video, WeChat Pay, as well as those of its partners, forming a comprehensive, industry-wide, end-to-end healthcare solution. Therefore, offerings such as Tencent Miying and WeChat Pay can be considered complementary components of Tencent Cloud’s healthcare services.

Based on the above information, a logical framework for Tencent’s healthcare industry strategy can be broadly outlined:

The core issue with this logic is that neither Tencent’s direct equity investment nor its existing technical service collaborations can fundamentally alter the current state of “connected but not integrated” medical data. VCBeat believes that for leading enterprises to deeply penetrate and dominate an industry, they must become the central data hub for that entire sector. Taking Tencent and Alibaba as examples, Tencent is unequivocally the data center of the social networking industry, while Alibaba serves as the data center for e-commerce. In the healthcare sector, however, this position appears to remain vacant at present.

Taking the most representative hospitals as an example, with the increasing proliferation of hospital information systems, various “silo projects” have made information islands the norm. In an effort to integrate these “silos,” hospital management has resorted to creating a “spider web” of interfaces. Ultimately, hospitals often find themselves held hostage by IT vendors: during the integration platform docking process, some developers have gone bankrupt, some vendors are unwilling to open their interfaces, and those capable of developing interface engines charge exorbitant prices.

To address this situation, the National Health Commission has been mandating hospitals to achieve interoperability through government directives over the past two years, as exemplified by the “Standardized Maturity Assessment Scheme for Regional (Hospital) Health Information Interoperability (2017 Edition)” released in 2017. The core technology involved is the integration platform.

The reason is that the integration platform adopts HL7 (Health Level 7) interfaces as its standard, a mature medical electronic information exchange standard recognized by the vast majority of healthcare IT vendors and hospitals worldwide. The integration platform standardizes medical information management formats, enables data sharing among various subsystems and software applications, facilitates seamless information exchange between different medical information systems, and achieves cross-platform utilization of medical data. This provides clinical healthcare professionals with accurate and timely clinical diagnosis and treatment information from multiple perspectives and in a comprehensive manner.

Taking the First Affiliated Hospital of Fujian Medical University as an example, the entire interoperability project was launched in February 2014. The integration of major business systems into the service bus was completed in October, and the data center was fully established in December, with platform-based applications subsequently going live.

Overall Platform Development: In terms of the service bus, HL7 is adopted as the interaction standard, integrating 22 heterogeneous systems with a daily message volume ranging from 150,000 to 200,000. For the data center, real-time data synchronization combined with ETL (Extract, Transform, Load) technology is employed to achieve real-time data acquisition and standardized conversion. Regarding platform application development, applications such as personal portals, patient integrated views, comprehensive medical record browsers, closed-loop information displays, clinical decision support systems (CDSS), and mobile hospital services are established based on the data center. Meanwhile, emphasis is placed on operations and maintenance (O&M) management through the implementation of O&M management portals and real-time monitoring systems.

However, the construction of integration platforms is often costly. Taking bidding data from the China Government Procurement Network as an example, the average unit price for such platforms in China is approximately RMB 5.4 million.

![M`ME5DUTMBTXQ9{Q1V7M}]R.png](https://vcbeat.top/upload/image/03/09/18/17/1537240658830944.png)

Source: Chinese Government Procurement Network

Consequently, due to funding constraints, the effective implementation of health information interoperability is largely confined to a select few Grade A tertiary hospitals.

Returning to the topic of Tencent Cloud,Provide the richest “digital interfaces” for industries across all sectors to enter the “digital world”; and build a robust “toolbox” offering the most comprehensive “digital tools.”The significance of Mr. Ma’s statement precisely reflects an area where Tencent Cloud currently needs to strengthen its capabilities: the data middle platform.

To explain the concept of a data middle platform, Alibaba Cloud is perhaps the best example.

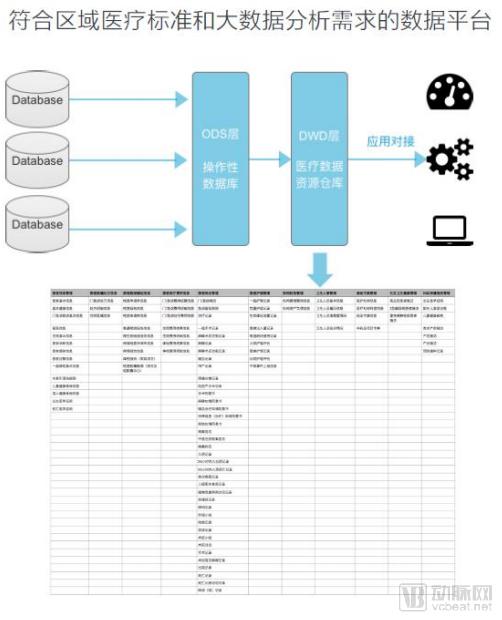

The integration platform connects all information subsystems within the hospital via an Enterprise Service Bus (ESB), acting as the neural center of the entire information network and resolving issues related to real-time data interaction. In contrast, the Alibaba Cloud Data Middle Platform functions more like a data warehouse, consolidating data from all of the hospital’s information systems into the middle platform. Through standardized services for data integration, data development, data operations and maintenance, quality management, data security, and data exchange, the Data Middle Platform ensures that the sources and usage of all data are clear and well-defined.

The platform integrates algorithmic resources, enabling the invocation of algorithmic capabilities during data management and application. For instance, it employs medical natural language processing (NLP) to assist in the post-structuring of electronic medical records, establishes predictive models by monitoring changes in data and metrics, and builds scheduling engines through data analysis. The Data Middle Platform differs from the Clinical Data Repository (CDR). While the CDR primarily stores clinical medical data, the Data Middle Platform consolidates all hospital data, including operational data such as surgery start and completion times, as well as supply chain and material data.

With the development of hospital information systems, vertical-domain data centers have emerged. How to integrate these data silos and construct them under unified standards to achieve the goals of reducing technical costs, improving application efficiency, and empowering business operations is a challenge faced by many hospitals. Alibaba’s Data Middle Platform model was proposed precisely to address these issues, and through practical implementation, it has established a unified, enterprise-wide data system.

Although Alibaba’s data middle platform is still in the validation phase within hospitals in China, the data management philosophy it introduces can be applied across various industries. If Tencent Cloud truly intends to fulfill the commitments stated in Mr. Ma’s open letter, it should accelerate the development of its own data middle platform product.

Having clarified the importance of data centers, VCBeat boldly predicts that Tencent’s future investments will center on core medical data. In particular, companies capable of accessing hospital clinical data are likely to become key targets for Tencent’s investment. The rationale is that Tencent needs to leverage their channels to acquire the most valuable medical data, andMedical Informatics, Medical Big DataIn addition to capital support from Tencent, these related enterprises also require the backing of underlying technology platforms such as Tencent Cloud.

This point can be analogized to the relationship between JD.com and Tencent. Tencent has opened up consumer-side (C-end) traffic redirection to only a select few enterprises, with JD.com being one of them. User consumption data can be regarded as a key factor in their partnership. Similarly, in business-side (B-end) collaborations, data middle platforms and integration platforms should serve as tools, while the power of capital remains indispensable; the two are complementary to each other.

If Tencent can leverage Tencent Cloud to conquer the “hard nut” of healthcare, replicating this model in the aforementioned sectors—such as finance, government affairs, culture, and education—will be far from difficult.

From “connected but not integrated” to achieving underlying data connectivity, once Tencent accomplishes this, its role as a connector is poised for further elevation. Describing itself as an “ecosystem co-builder” may merely be a modest facade; the true intent likely lies in leveraging capital and data to dominate the entire industry.