New-Generation Clinics in 2018: Capital Continues to Enter, with Room for Growth in Chain Expansion, Traffic Acquisition, and Service Boundaries

The Clinic Fever Cools Down: Compared to the peak expansion period of previous years, the trend has cooled this year. On one hand, this is related to the investment environment, with capital becoming more cautious about investments; on the other hand, the head effect is becoming increasingly pronounced, exhibiting a "big fish eat small fish" characteristic.

From the overall trends in the healthcare market, China’s aging population is intensifying and medical demand is continuously rising, while medical services are far from meeting the public’s needs. As a supplement to hospitals, the highly fragmented and numerous clinics have played a significant role in alleviating this pressure. Encouraging private investment in healthcare has become a visible trend in the development of the medical industry.

"New-type clinics" primarily refer to those that excel in brand operations, product design, service capabilities, and operational standards. These clinics tend to exhibit consumer-oriented healthcare attributes, with most positioned in the mid-to-high-end market segment.

The commercial essence of healthcare services lies in balancing medical outcomes and service experience with price. Patients opt for the provider that offers the optimal combination of medical efficacy and service experience, provided that transaction costs remain manageable. In today’s landscape, characterized by a more diverse patient base and an increasingly critical role of consumer experience, clinics are placing greater emphasis on the integration of hardware, software, and services. They are leveraging digitalization to transform workflows and adopting innovations to enhance efficiency and patient volume. Particular attention is being paid to cultivating personalized brand identities within niche emerging markets.

New Clinics: What Happened in 2018? What Thorny Issues Need to Be Addressed, and What Are the Potential Trends? What Keywords Can Summarize These Developments? VCBeat (WeChat ID: vcbeat) Has Compiled and Analyzed These Insights.

Billion-Yuan New Financing and Major M&A

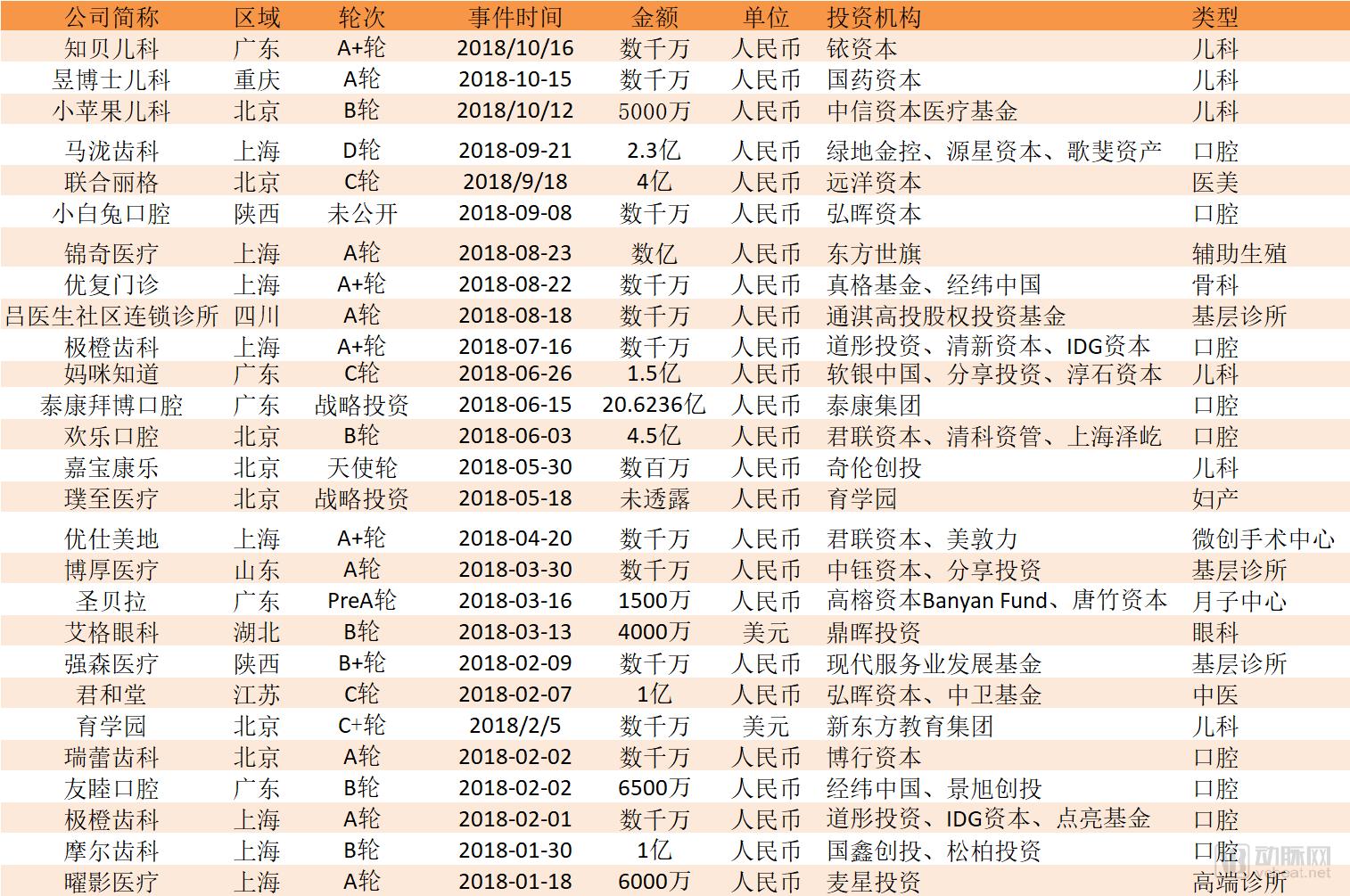

As of November 1, 2018, financing events for clinic-type enterprises. Data source: VCBeat Database

More Dental

In January, Moore Dental announced the completion of its Series B financing round, amounting to hundreds of millions of yuan, with investors including Shuangbai Investment and Guoxin Venture Capital. Leveraging this capital infusion, Moore Dental is committed to building a standardized, regulated, and modern chain brand for dental healthcare services.

Junhetang

In February, Junhetang, a chain of traditional Chinese medicine (TCM) clinics, announced the completion of its Series C financing round, raising hundreds of millions of yuan. The round was led by Zhongwei Fund, with participation from existing investor Honghui Capital. Following this financing, Junhetang will continue to strive to build China’s highest-quality TCM service brand. Junhetang has implemented a series of model innovations, including establishing specialized disease-focused project teams based on extensive clinical experience. These teams research and develop Junhetang’s distinctive solutions for specific single diseases, creating dedicated medical service offerings and signature products.

Aier Eye Hospital

In March, Aier Eye Hospital Group, a chain brand of ophthalmic hospitals, announced that it had received $40 million in Series B funding from CDH Investments. Following this round of financing, Aier Eye Hospital will accelerate the group's network layout and further enhance the service capabilities of its existing hospitals. At the same time, it will make new attempts in innovative business models that balance the decentralization of medical resources with medical quality, striving to become a leading high-quality ophthalmic hospital chain brand in China.

Taikang Bybo Dental

On May 18, with the approval of the China Banking and Insurance Regulatory Commission (CBIRC), Taikang Insurance Group officially announced its strategic investment in Bybo Dental Medical Group. Taikang Life Insurance invested RMB 2.06236 billion to acquire a 51.56% equity stake in Bybo Medical. On June 15, this strategic investment was successfully completed. Led by Taikang Health Industry Investment Holdings Co., Ltd. and funded by Taikang Life Insurance Co., Ltd., the deal marks the formal entry of Taikang’s high-end healthcare model into the specialized field of dentistry. The partnership will effectively integrate service providers with payers, facilitating the alignment of medical services with insurance payment mechanisms.

Happy Dentistry

On June 3, Happy Dentistry Medical Group announced that it had formally signed an investment cooperation agreement with Legend Capital Management Co., Ltd. and other parties, securing RMB 450 million in Series B financing. Over the past 11 years, Happy Dentistry has leveraged the technical expertise of its founding team of dentists from Peking University School of Stomatology, adhered to the philosophy of prioritizing prevention, and developed the “Three Diseases, Two Techniques” framework, thereby establishing a comprehensive system of preventive and therapeutic dental technologies characterized by rapid diagnosis, minimal discomfort, and superior clinical outcomes.

Mami Knows

On June 26, Mami Zhidao announced that it had secured RMB 150 million in Series C strategic financing, led by Fenxiang Investment and participated by SoftBank China, Chunshi Capital, Fengxin Capital, and Yiqichuang Capital. After four years of accumulation, iteration, and optimization, Mami Zhidao has meticulously crafted a new medical service model featuring “four online” components—User Online, Doctor Online, Service Online, and Management Online—to comprehensively enhance user experience and improve operational efficiency.

Jinqi Medical

In August, Jinqi Medical completed its Series A financing round, led by Oriental Shiqi, with an investment amounting to hundreds of millions of yuan. The funds will primarily be used to acquire overseas medical institutions and reproductive laboratories holding IVF licenses, as well as to further advance the construction and development of a nationwide internet-based reproductive healthcare platform and promote gene and stem cell diagnostic and therapeutic technologies. Since its establishment in 2007, Jinqi Medical has been dedicated to reproductive health and medical services. After eleven years of significant growth, it has become a diversified group company integrating domestic and international reproductive healthcare services, an online internet-based reproductive healthcare platform combined with offline clinics, pharmaceutical information services, and the sales of medical devices and imported health supplements.

Penguin Almond

On August 9, Penguin Doctor and Xingren Doctor signed a strategic merger agreement. By combining their respective advantages in platforms, resources, and technology, the two parties will form a synergistic force. Following the merger, the new group company will be collectively known as “Penguin Xingren,” while the existing platforms of “Penguin Doctor” and “Xingren Doctor” will continue to operate under their original names.

The merged management team has also completed its integration. Wang Shirui, founder of Penguin Doctor, will serve as Chief Executive Officer; Martin, founder of Almond Doctor, will serve as President; and Xu Lin will serve as Chief Operating Officer of the new company. Penguin Almond will establish an integrated online-and-offline comprehensive health service system, committed to leveraging technology to make high-quality health and medical services accessible to all.

Union Lige

On September 18, BCCG Group announced the completion of a C-round financing of RMB 400 million, exclusively invested by Sino-Ocean Capital. Over the past five years, BCCG has pursued a dual-brand strategy combining “physician brands” with the “group brand,” leveraging physician entrepreneurship and empowerment as key drivers, while implementing modular management systems encompassing operational coordination, marketing, and supply chain management. The group has jointly invested in, operated, and prepared for the launch of more than 40 medical aesthetic institutions across 15 cities in China.

Malong Dental

On September 21, Malo Clinic China announced the completion of its RMB 230 million Series D financing round. The round was led by Vertex Ventures China, with participation from Greenland Financial Holdings and Noah Asset Management. Shanghai Fuyi Daohe served as the exclusive financial advisor. Over the past five years, Malo Clinic China has continuously refined and optimized its four core systems: clinical specialty development, teaching and medical practice, precise financial operations management, and high-quality patient services. The company has completed its strategic layout across the entire industry chain in Greater China, encompassing 21 dental clinics in 16 cities, two denture processing centers, one education and training center, and one procurement center.

Current Status and Models

In collaboration with hospitals, consumer-grade medical clinics generally share three common characteristics: they operate as peripheral departments within public hospitals, serving as a supplement to hospital services; their revenue model focuses on selling products rather than pharmaceuticals, while exploring new service formats; and the average transaction value exceeds RMB 1,000. Key high-revenue specialties include medical aesthetics, dermatology, dentistry, ophthalmology, nutrition, rehabilitation, veterinary care, and health management. This trend is reflected and corroborated by the market, where chain clinics in these categories are predominant, experiencing rapid growth, attracting significant capital investment, and facing the most intense competition.

From the perspective of average transaction value, a key determinant of corporate profitability, data from VCBeat’s Eggshell Research Institute indicates that small and medium-sized clinics providing basic community healthcare services typically have an average transaction value of around RMB 100. With low consultation and treatment fees, the majority of their revenue is supported by pharmaceutical sales, resulting in a drug-to-revenue ratio exceeding 70%. In contrast, mid- to high-end clinics with higher consultation fees often achieve an average transaction value of over RMB 1,000. As physicians in these settings are not driven by profit-maximization motives, they exercise greater caution in prescribing medications, keeping the overall drug-to-revenue ratio at approximately 10%.

In contrast, the average transaction value per customer at dental clinics is significantly higher, driven by the high cost of dental treatments—particularly orthodontics and dental implants—with most clinics easily exceeding RMB 1,000 per customer. This year’s financing data for clinic-based enterprises also shows that dental companies dominate, accounting for nine financing rounds. To summarize the current status and development models of clinics in 2018, the following sets of keywords can be used.

Barriers to Entry and Replicability

Broadly speaking, high-quality clinics in the healthcare services industry must exhibit characteristics such as asset-light operations, rapid expansion, and scalability. When evaluated through the lens of replicability and barriers to entry, institutions such as health examination centers, chain pharmacies, ambulatory surgery centers, and reproductive medicine centers demonstrate the highest replicability. These sectors are characterized by a “winner-takes-all” dynamic, offering the greatest potential for the emergence of industry giants. Consequently, the early identification of these dominant players is central to investment strategy and represents the core focus of investment banking mergers and acquisitions.

In comparison, sectors such as dentistry, medical aesthetics, pediatrics, ophthalmology, and rehabilitation rank next, characterized by a “big fish eating small shrimp” dynamic. These markets are prone to tiered stratification, making the ability to identify and acquire smaller competitors a critical factor in evaluating investment targets. Conversely, specialized hospitals such as oncology, neurology, and cardiovascular centers exhibit the lowest replicability. They tend to develop through self-strengthening amidst diverse competition, with expert teams serving as the core of investment value.

From the perspective of entry barriers, oncology hospitals, neurology hospitals, cardiovascular hospitals, and reproductive centers present the greatest challenges. These sectors are prone to oligopolistic structures, require long development cycles, and exhibit a "the strong get stronger" dynamic, making it difficult for late entrants to disrupt the established landscape. Consequently, acquisitions are common, with occasional mergers taking place.

Dermatology hospitals, obstetrics and gynecology hospitals, rehabilitation hospitals, orthopedic hospitals, hemodialysis centers, and surgical centers present moderate entry barriers. This sector is characterized by a fragmented landscape with many regional players; individual entities are relatively small in scale, chain operations are limited, synergies are weak, and growth relies on both organic expansion and M&A. In contrast, dental clinics, medical aesthetics institutions, traditional Chinese medicine (TCM) clinics, chain pharmacies, health check-up centers, and primary care diagnostic facilities have the lowest entry barriers. This segment exhibits a long-tail structure, where chain operations and consolidation persist over the long term. Monopoly is a false premise, and capital continues to flow into leading platforms.

From the perspective of total investment, emerging institutions with a high degree of marketization, such as those in dentistry, medical aesthetics, and pediatrics, have relatively low entry barriers and strong replicability. Therefore, they require continuous capital infusion to address the following key issues:

Physicians and managerial talent.For clinics, physicians are a critical asset and represent one of the largest cost components. In sectors such as dentistry, medical aesthetics, pediatrics, and rehabilitation, labor costs are particularly significant—accounting for 50%–60% in rehabilitation and 20%–40% in dentistry. Given the scarcity of qualified professionals and the relatively high staff turnover, retaining talent is crucial and plays a vital role in brand expansion. The partnership model is central to this strategy, with notable examples including United Lige, Meiwei Dental Group, and Happy Dental. Furthermore, competition in the emerging clinic sector remains intense, necessitating strong managerial talent and substantial brand premium.

This October, Mommy Knows joined hands with Shanghai Jiao Tong University to launch a formal strategic partnership for talent development, establishing a training system for pediatric healthcare management professionals. The aim is to help physicians build healthcare management capabilities, creating a talent pipeline for future managerial roles and serving as the link for executing healthcare management between headquarters and clinics.

Standardization and Trust.From the perspective of customer needs, building an efficient and high-quality standardized service process has gradually become a consensus. The elements involved in standardization are complex; the general direction is to implement detailed and standardized operations within the customer service process under a centrally controlled operation and monitoring system. This not only requires leveraging information systems to accumulate and analyze customer data but also emphasizes a crucial aspect: physician-patient communication must be approachable to build trust.

Light medical aesthetic procedures are relatively safe, involve fewer disputes, allow for standardized workflows, and enable systematic analysis of quantitative metrics. Xinghe Medical Aesthetics leverages its "1-kilometer beauty ecosystem" to acquire highly sticky users, integrating multi-party systems to support precise data analysis across various dimensions. For instance, the company is currently in negotiations with Meituan regarding external hardware installations, such as in-store cameras. These cameras can precisely track a user’s location within the store on a second-by-second basis during specific time periods. This technology enables a single supervisor to manage up to 20 stores within a designated area, significantly reducing labor costs for middle management. Furthermore, an IT-based alert mechanism allows for real-time assessment of service quality, replacing traditional monitoring methods and driving the transition toward intelligent operations.

As household incomes rise and awareness of healthcare consumption strengthens, it is foreseeable that the total number of large and medium-sized public hospitals will grow slowly while their market share declines. Non-branded individual clinics will be gradually consolidated by branded chain operators, although small, single-site outpatient clinics currently remain the dominant form.

Services and Boundaries

Consolidation in the terminal healthcare sector has become a trend in China. Although private entities account for a very high proportion, the chain affiliation rate among private providers remains very low, thus driving substantial capital to fuel consolidation. Consumer-oriented new-model clinics boast higher gross margins, are easier to standardize for chain expansion, and are less prone to major medical malpractice incidents. Due to challenges in the restructuring of public hospitals and the scalability limitations of individual private clinics, new-model private chains have currently become the mainstream investment focus.

How can clinics ensure their capacity for continuous new product development and iteration? How can they deliver integrated online and offline services, creating a closed-loop service ecosystem that spans hardware, software, IT systems, and organizational structures, while exploring replicable new business models? These are the pressing challenges currently facing clinics.

Information System.This primarily refers to tracking the implementation and execution of standardized systems through digital software platforms, enabling managers to monitor store appointments, patient treatment plans, and post-procedure satisfaction in real time. From pre-consultation data collection to post-treatment outcome tracking and professional follow-up, digital system management consolidates customer inquiries, treatment records, and patient needs. Leveraging this data allows for the development of more precise and effective health management plans, thereby achieving refined operations and enhanced service quality. In exclusive interviews with VCBeat, chain clinics unanimously highlighted that informatization upgrades are a key priority for the year.

A typical example of an empowerment-oriented enterprise in this field is Linkcare Information. Currently, its products, e-Kanya (for dental practices) and YueRong Medical Aesthetics Cloud, have been integrated with the Meituan-Dianping app platform. This integration facilitates smoother communication between consumer healthcare institutions and their clients, fosters deeper connections between institutional brands and customers, and completes a closed loop encompassing brand marketing, services, transactions, and sharing. This year, the company also completed a Series B+ financing round worth tens of millions of RMB and now collaborates with over 14,000 clinics.

Patient Education.The importance and utility of patient education are self-evident. By providing medical-grade knowledge services, healthcare providers can meet users’ needs for record-keeping, knowledge acquisition, social interaction, and shopping consumption. Specific groups, such as mothers and individuals seeking aesthetic treatments, exhibit a stronger motivation to learn popular science knowledge than other demographics, driven by their desire for effective parenting and personal beautification. If health education courses and even training systems can be developed to form a comprehensive health management and medical service package, paid knowledge content represents a new profit model worth exploring. From a revenue perspective, beyond the pure medical sector, some clinics are actively exploring additional income streams through mobile product platforms, health membership programs, and education and training services.

Early this year, YuXueYuan completed its C+ round of financing, exclusively invested by New Oriental, with plans to jointly develop medical-education products. Once its online mobile products, paid content, e-commerce, education sector, and private-label products were fully established, its primary task in 2018 was to complete the healthcare segment of YuXueYuan by launching the YuXueYuan Obstetrics, Gynecology, and Pediatrics Healthcare Platform, thereby upgrading from children’s health management to a more comprehensive family health management program. On October 31, YuXueYuan announced that “Gugu Jiang,” a menstrual cycle management app targeted at young women born after 1995, would be launched and operational by the end of 2018.

Boundary.Here, it is necessary to address the issues of both the existing and incremental markets. For instance, in the rehabilitation market, beyond the existing market, the incremental market includes niche segments such as pediatric rehabilitation, geriatric rehabilitation, psychiatric rehabilitation, cardiac rehabilitation, and sports rehabilitation.

Traditional pediatric clinics typically offer services in departments such as Child Healthcare, General Pediatrics, and Dermatology. As patient volumes have grown, demand for specialized pediatric care has increasingly emerged. ZhiBei Pediatrics, a chained pediatric brand, has added multiple new departments to provide families with more comprehensive, high-quality medical services, including Pediatric Respiratory Medicine, Child Psychology, Otolaryngology (ENT), Speech and Language Delay Intervention, and Autism Rehabilitation.

Another example is the significant transformation in the model of hearing care services, which has evolved beyond mere product sales. The markets for hearing screening, examination, diagnosis, and rehabilitation hold substantial potential. By introducing advanced audiometric equipment and establishing intelligent service standards, iEar Clinic has rapidly expanded into grassroots communities through collaborations with pharmacies and health check-up centers. This approach enables the clinic to effectively serve elderly and pediatric patients, thereby fostering strong patient loyalty throughout the long-term management of chronic hearing conditions.

How to rationally expand service boundaries, reposition institutions, address the challenge of differentiated experiences, and build market barriers directly determines whether a clinic can achieve rapid growth. For instance, hair transplant clinics and reproductive centers are currently largely tapping into existing market stock. How to transition from treating infertility to promoting eugenics and healthy childbirth, from hair transplantation to hair care and maintenance, and how pediatric clinics can find new pathways in children’s health management are all questions worthy of institutional reflection.

Pain Points and the Future

New-type clinics indeed face numerous challenges in their development. For instance, compared with public hospitals, they suffer from insufficient patient traffic. While regional replication is relatively easy, establishing a nationwide chain is difficult due to weak front-end brand effects and high supply chain requirements. Bottlenecks often arise in building teams of physicians and management talent. Moreover, the overall profit margin of clinics tends to hit a ceiling, as diagnostic and treatment services are limited, with primary revenue streams derived from consultations, registration fees, and basic pharmaceuticals. The following analysis focuses on this year’s most prominent concerns: “chain expansion” and “patient traffic.”

Chain Model

Behind chain operations lie quality standard controls and a unified brand image. The current lenient policies for clinic establishment, the trend toward privatization of clinics, and the liberalization of physicians’ multi-site and independent practice have all laid the foundation for the chain operation of clinics.

Chain expansion can reduce procurement costs. However, standardized chain operations can only be implemented after the standardization of medical services and personnel training has been thoroughly established. This is a long-term process of refinement; otherwise, it may result in “chained but not locked” operations, or even losses. This trend is particularly evident in the fields of dentistry, medical aesthetics, and pediatrics, where data disclosed by some clinics this year show that few have achieved overall profitability. Nevertheless, Malo Clinic China achieved overall operational profitability in 2018. Over the five years since its establishment, it did not focus on blind pursuit of scale-driven expansion, but instead explored a sustainable business path suited to its private specialized chain medical service model.

Nationwide Chain Expansion of Clinics: Typically, expansion into new regions is achieved through three approaches: self-operation, acquisitions, and franchising. The prevailing model generally follows a “1 (flagship clinic) + N (smaller clinics)” structure. The ability to successfully expand into new markets depends on numerous factors, such as identifying geographic markets suitable for the types of services offered, understanding local consumer preferences, addressing competition in local markets, negotiating acceptable lease terms (including ideal rental rates), recruiting, training, and retaining medical staff, successfully integrating new facilities into existing control structures and operational systems (including information technology systems), and securing financing or maintaining sufficient capital required for investment in new facilities or acquisitions.

Among clinic enterprises that secured financing this year, a major priority for most has been expansion or the establishment of a chain-based medical management system. However, clinic services are inherently constrained by geographical management radii. Managing cross-regional chains entails an excessively large management radius, requiring clinics to possess exceptional capabilities in management, coordination, and centralized resource allocation from headquarters. By replicating chain management models, clinics can reduce costs and enhance operational efficiency.

Among the types of clinics we have observed, few are monopolistic chain clinics; most enterprises require time to build brand awareness and establish a comprehensive operational system.

According to previous statistics and observations by VCBeat, there are currently few nationwide chain clinic enterprises that have developed well. Most of them are dental and pediatric clinics, while some comprehensive general practice clinics are regionally concentrated with relatively simple management.

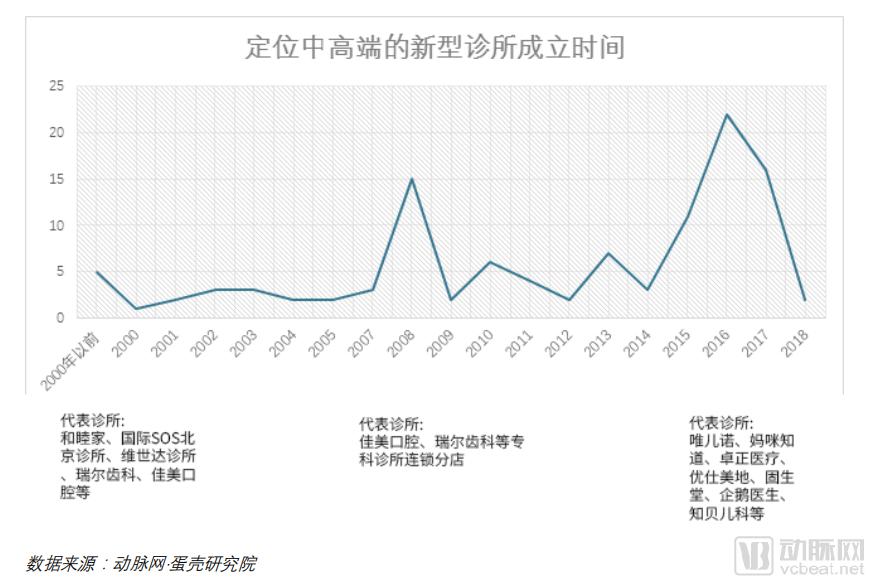

A visible trend is that dental and pediatric clinics are transitioning from a period of rapid expansion (2013–2014 for dental, and 2016–2017 for pediatrics) to an era of intensive, refined development. This shift emphasizes strengthening internal capabilities, such as management systems, physician training programs, information technology systems, operational frameworks, and brand building. The year 2018 may well serve as a watershed moment.

From the perspective of capital investors, an analysis of clinic investment trends reveals that core competitiveness primarily lies in the ability to deliver standardized services. Technological upgrades and evolving consumer mindsets are driving changes in service offerings—shifting from mere treatment and product demands to comprehensive medical service needs. Medical institutions will become more chain-operated, premium, and digitalized. While the current competitive landscape is fragmented, industry consolidation is expected in the future, with mergers and acquisitions serving as the primary exit channel for capital.

Continuous Flow

Every clinic aims to continuously attract more patients at a low cost. Patient acquisition operates on two dimensions: acquiring new patients and extending the service lifecycle of existing ones. This demand for precise patient traffic is particularly acute in highly competitive, consumption-driven sectors such as medical aesthetics, dentistry, skin care management, and health management. Clinics that expand too aggressively often face closure or merger and acquisition due to shortages of physicians and patients, a scenario that has been quite common this year.

From the perspective of economic principles, in any emerging field, if traffic acquisition is required, purchasing it early—even at a high current cost—will result in lower overall costs compared to late entrants, as traffic prices will only continue to rise.

So, what constitutes precise traffic? Generally, it must meet several key elements. In addition to basic user volume and stickiness, one must also consider transactional attributes and the intensity of demand. To achieve higher conversion rates, we believe that clinics should leverage mass-market, high-frequency, and low-cost products or services to attract traffic. Clinics should develop service packages of this nature based on their product and service offerings, thereby driving traffic. Examples include fluoride treatments and dental cleanings at dental clinics, skincare services at medical aesthetic clinics, and growth and development testing and monitoring at pediatric clinics.

In the post-traffic era, products and services themselves become traffic drivers. The focus is shifting from mere traffic acquisition back to brand building, and from online channels back to offline presence. This trend toward offline engagement is particularly evident in consumer-oriented healthcare sectors. For instance, when selecting locations, mid-to-high-end clinics and chain clinics often prioritize high-footfall commercial districts to attract customers. These clinics primarily draw patients through enhanced service experiences, implementing changes in interior design and even the professional image of medical staff to alleviate patients’ fear of seeking medical care. However, the premium service quality offered by mid-to-high-end clinics comes at the cost of higher consultation fees.

Although online traffic acquisition is regarded as a significant source of users, the actual patient volume it can generate for clinics often hits a bottleneck. This is particularly evident in specialties such as gynecology, pediatrics, and obstetrics. The majority of patient flow for postpartum care centers, postpartum rehabilitation institutions, and pediatric clinics still originates from hospitals.

Online patient acquisition plays a positive role primarily in brand building, patient education, and communication. This is not to say that online acquisition is ineffective; rather, it necessitates the creation of a new offline business model that both delivers experiential value and addresses challenges related to service density and timeliness. Clinics are urgently seeking new online-to-offline (O2O) consumption scenarios and engaging in cross-industry collaborations, making them truly “busy” this year.

For online platforms, there is a shift from mere traffic matching to a mindset of professional and refined services, while continuously expanding the boundaries of new services and exploring new entry points for online-to-offline integration. This represents the new strategy adopted by vertical platforms such as So-Young, Gengmei, Yuemei, and Meibei, as well as internet giants like Meituan-Dianping and AliHealth, to empower merchants and the industry chain—transitioning from traffic-driven platforms to deep engagement in professional service domains. So-Young plans to recruit 100 medical professionals this year to position itself as a professional service provider. Gengmei aims to enhance user decision-making efficiency in the next golden decade of medical aesthetics by rapidly providing structured information. Meituan-Dianping’s Beauty Division has introduced the “Beauty Store, Meituan Core” solution this year, committing to becoming the engine for stores and a driver for merchants’ revenue growth.

We believe that looking ahead, the integration of online and offline models—leveraging foundational capabilities such as digital information systems, standardized service delivery, intelligent hardware and software, and data support—to transform clinics was only just beginning in 2018. In the coming years, driven by economies of scale and capital investment, the chain affiliation rate of new-type clinics is expected to rise rapidly, particularly in sectors with higher levels of consumerization. As clinics develop professional service capabilities and build strong brand reputations, these assets will truly become competitive barriers for enterprises.