Health Insurance in 2018: Policy Support Amid Tighter Regulation, Greater Openness, and Innovation Challenges – Annual Review

The function of insurance is to spread risk. Policyholders pay premiums in advance to obtain compensation for losses when risks materialize in the future, thereby eliminating economic uncertainty. Insurance companies aggregate the needs of the insured, transform dispersed risks into approximate certainty, and realize commercial value.

Driven by the introduction of several favorable policies, heightened insurance awareness among residents, and improved consumption capacity, commercial health insurance has become the fastest-growing segment within the insurance industry in recent years. However, it is important to note that the health insurance sector currently faces challenges such as low penetration rates, a small market scale, and an imbalanced product structure. Service capabilities are also relatively insufficient, as evidenced by weak control over medical costs and inadequate provision of health management services.

Opportunities and Challenges Coexist. What favorable policies emerged for the health insurance industry in 2018? How did major companies strategize their layouts? How did third-party administrators (TPAs) and healthcare institutions collaborate with health insurers? What were the investment opportunities in the sector, and where lay the pain points in technology-enabled solutions? Let us review the changes in the health insurance industry in 2018.

(Sorted by time)

Ruihua Health Approved to Commence Operations, Becoming the Seventh Specialized Health Insurance Company in China

On May 30, Ruihua Health Insurance Co., Ltd. received approval to commence operations, becoming the seventh specialized health insurance company in China. Ruihua Insurance is a nationwide company positioned to engage in specialized health insurance and provide health management services. The company is domiciled in Xi’an, Shaanxi Province, with its business premises located in Shanghai.

Xinmei Life Mutual Insurance Society and Alipay Join Forces to Launch “Mutual Aid”

Xianghubao was launched on the Alipay client on October 16, attracting over 17 million participants within a month. Xianghubao is a mutual aid mechanism that brings together Ant Group members with similar risk protection needs to provide health coverage through shared risk pooling. It covers malignant tumors and 99 other critical illnesses. Members join while healthy; if one member falls ill, all members share the cost equally, and the affected member receives a lump-sum benefit. (The coverage amount is RMB 300,000 for initial diagnosis between ages 30 and 39, and RMB 100,000 for ages 40 to 59.) On November 27, Xianghubao was suspended and transitioned into the mutual aid platform “Xianghubao.”

Xianghubao is essentially a group critical illness insurance product. It rapidly gained popularity due to its low premiums and simple purchasing process, attracting many users who had never previously purchased commercial health insurance. From the perspective of market education, Xianghubao has undoubtedly been highly successful in popularizing knowledge about health insurance among the general public.

PICC's A-Share Listing Raises Approximately RMB 6 Billion

On November 6, PICC set its IPO price at RMB 3.34 per share, with an initial public offering of no more than 1.8 billion shares, raising an estimated RMB 6.012 billion. This marks the first listing of an insurance company on the A-share market in seven years, and PICC will become the fifth insurer to be listed on both the A-share and H-share markets.

In March 2005, PICC established China’s first specialized health insurance company—PICC Health. According to the prospectus, PICC Health held a 30.52% market share among specialized health insurers in China from January to June 2017. PICC Health is also one of the earliest companies in the industry to explore the “insurance coverage + health management” model.

(Chronological Order)

The Establishment of the CBIRC: The Emergence of a Super Regulator

On April 8, the China Banking and Insurance Regulatory Commission (hereinafter referred to as the “CBIRC”) was officially unveiled. The establishment of the CBIRC marked the formal commencement of operations for the financial regulatory framework known as the “One Committee, One Bank, and Two Commissions.”

Industry observers believe that integrated operations in the financial sector have become a trend, with deep cooperation and convergence already underway between the insurance industry, the banking sector, and other financial institutions. This regulatory reform aligns well with the current state of China’s financial and insurance markets: the consolidation of regulations can effectively address issues such as unclear regulatory responsibilities, overlapping oversight, and regulatory gaps that existed under the previous system. In particular, the enhanced scrutiny of both assets and liabilities demonstrates that the entire industry is urging insurance companies to move in the right direction, further guiding the insurance sector back to its core fundamentals.

Tianjin Insurance Regulatory Bureau Intensifies Supervision of Short-Term Medical Insurance Products Such as “Million-Yuan Medical Insurance,” with CBIRC Following Suit

On April 18, the Tianjin Insurance Regulatory Bureau issued regulatory requirements to insurance companies selling short-term medical insurance products such as “Million Medical” plans: first, clarify product attributes during the sales process; second, specify detailed underwriting and claims assessment criteria during the claims evaluation stage; and third, enhance professional competence in the claims settlement process.

On April 28, the China Banking and Insurance Regulatory Commission (CBIRC) released the “Negative List for the Development and Design of Life Insurance Products,” pointing out that some expense-reimbursement medical insurance products, in pursuit of marketing gimmicks and despite a severe lack of actuarial data and pricing basis, blindly set high benefit limits. Furthermore, these products introduce long-term insurance concepts such as “lifetime benefit limits” and “continuous renewal” into short-term health insurance, thereby exaggerating product features and disrupting market order.

From the Tianjin Insurance Regulatory Bureau to the China Banking and Insurance Regulatory Commission (CBIRC), regulators have simultaneously intensified oversight of “Million-Yuan Medical Insurance,” a move directly linked to unclear renewal rules and the mismatch between high coverage limits and low premiums. Following the issuance of regulatory guidance, numerous insurers offering Million-Yuan Medical Insurance products made adjustments.

Further Expand Opening-up to Foreign Investment and Liberalize the Business Scope of Foreign-funded Insurance Companies

On April 27, the China Banking and Insurance Regulatory Commission (CBIRC) released an article titled “Accelerating the Implementation of Measures to Open Up the Banking and Insurance Sectors.” The article pointed out that the CBIRC will facilitate foreign investment, relax conditions for the establishment of institutions by foreign investors, expand the business scope of foreign-funded institutions, and optimize regulatory rules for foreign-funded institutions.

Subsequently, the China Banking and Insurance Regulatory Commission (CBIRC) successively issued the “Notice on Lifting Restrictions on the Business Scope of Foreign-Funded Insurance Brokerage Firms,” the “Notice on Permitting Overseas Investors to Operate Insurance Agency Business in China,” and the “Notice on Permitting Overseas Investors to Operate Insurance Loss Adjusting Business in China.” With these measures, the three major sectors of insurance intermediation—brokerage, agency, and loss adjusting—have been progressively opened to foreign investment.

"Measures for the Supervision and Administration of Internet Insurance Business (Draft)" Open for Public Comment, Proposing to Lift Regional Restrictions on Health Insurance Sales

On October 23, the China Banking and Insurance Regulatory Commission (CBIRC) issued a draft for regulatory comments to solicit industry feedback on supervisory measures for internet insurance. The Draft expands the scope of insurance products eligible for cross-regional sales, allowing insurance companies to extend the operational regions for their internet insurance business—covering personal accident insurance, term life insurance, ordinary whole life insurance, health insurance (excluding long-term care insurance and reimbursement-type medical insurance), pension annuity insurance, and tax-deferred commercial pension insurance—to provinces, autonomous regions, and municipalities directly under the Central Government where they have not established branch offices.

For the health insurance industry, industry insiders believe that this policy will facilitate small health insurance companies in conducting business nationwide via the Internet.

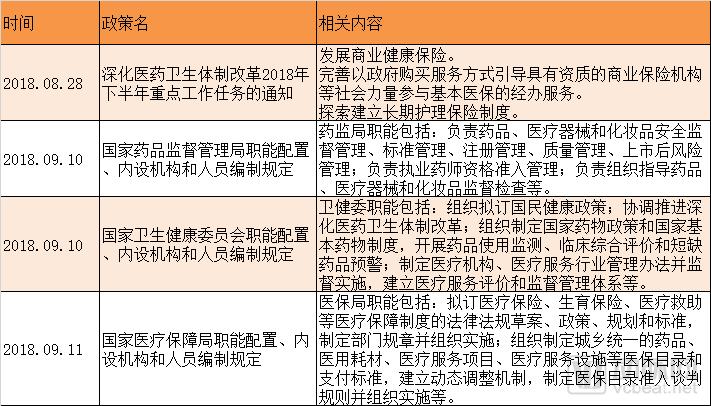

Other Policies Related to the Development of the Health Insurance Industry

Source: The Chinese Government Website, VCBeat

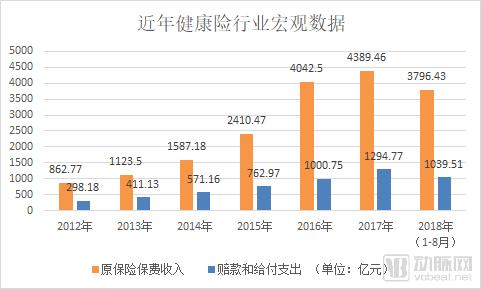

According to data from the China Banking and Insurance Regulatory Commission (CBIRC), the compound annual growth rate (CAGR) of gross written premiums in the health insurance market reached 40.6% from 2013 to 2017, significantly higher than the overall insurance market’s average growth rate of 20.7%. In terms of health insurance density and penetration, the density stood at RMB 316 per capita, and the penetration rate was 0.53% in 2017. Driven by rising household income levels, heightened insurance awareness, and innovations in insurance products and distribution channels, the sector holds substantial growth potential. Based on this, it is projected that gross written premiums for health insurance will reach RMB 1.3 trillion by 2020.

Data source: CBIRC, VCBeat

From the perspective of health insurance sub-categories, critical illness insurance and medical insurance took the lead. In 2017, the original premium income for critical illness insurance reached RMB 249.4 billion, accounting for 56.8%, while that for medical insurance was RMB 141.5 billion, representing 32.3%. The original premium income for long-term care insurance stood at RMB 47.5 billion, whereas disability income insurance generated only RMB 50 million. Growth rates varied significantly across different types of insurance: critical illness insurance saw the fastest growth at 46.9%, followed by a 25.0% year-on-year increase in medical insurance. In contrast, long-term care insurance experienced a decline of approximately 60%.

Guo Chao, Assistant to the President and Business Development Manager at Fosun Health Insurance and Health Management Group, stated that the health insurance market has been shedding “excess” over the past two years, with long-term care insurance products being the most significantly affected. In previous years, some companies repackaged wealth-management-oriented insurance products as health insurance, particularly as long-term care insurance. Following the issuance of regulations emphasizing that “insurance should primarily serve its protective function,” such products were substantially reduced. “Nevertheless, the overall growth rate of health insurance remains robust, and there is considerable room for future expansion.”

Shi Mengmeng, General Manager of Medtronic China, also stated that with the implementation of the "Healthy China" strategy, the overall development of the big health industry is favorable. Coupled with the awakening of national demand for insurance allocation, health insurance is gradually becoming a rigid demand, showing huge potential at both macro and individual levels.

Currently, there are approximately 150 insurance companies offering health insurance products, including seven specialized health insurers. In terms of operating entities, life insurance companies dominate the health insurance market. Property and casualty insurers, constrained by regulatory restrictions, are limited to underwriting short-term health insurance policies; however, these policies generally have low unit prices, resulting in modest overall premium volumes.

From the perspective of market concentration, 80% of the market is occupied by 8% of companies, indicating a very high level of concentration. Ping An Life Insurance and China Life Insurance Company each generate annual health insurance premiums exceeding RMB 60 billion; ten companies, including Hexie Health Insurance, New China Life Insurance, CPIC Life Insurance, and PICC Health Insurance, report annual health insurance premium revenues in the range of RMB 10 billion. Meanwhile, more than 110 insurance enterprises have annual health insurance premium revenues of less than RMB 100 million.

“Currently, whether in health insurance or other types of insurance, product differentiation is minimal; we are still in an era where distribution channels reign supreme. Insurance companies rely primarily on sales rather than on their products,” said Guo Chao. The traditional agent channel for health insurance remains crucial, accounting for nearly 60% of sales. However, as public awareness of insurance grows and emerging online channels gain popularity, the health insurance market is shifting from a “sales-driven” to a “customer-driven” model.

“Insurance agent channels used to be the primary distribution channel. Consumers tend to shop around and compare offerings when making a purchase; if a channel fails to provide differentiated value, comparing options via online channels becomes the most suitable approach. Online channels offer high transparency, are not constrained by geography, and have strong reach. Health insurance products with simple terms and low premiums are well-suited for online distribution, whereas products with complex terms and long coverage periods remain to be seen,” said Guo Chao.

Over the past two years, there have been continuous calls for health insurance to synergize with medical services, health management, and insurtech, thereby driving full-lifecycle innovation in the health insurance sector.

Shi Mengmeng believes that collaboration across the industry chain should first clarify the relationships between upstream and downstream segments. For health insurance companies, the upstream provides supportive service networks, hardware technologies, and informational data support, such as medical services, health check-ups, genetic screening, smart wearable devices, and Pharmacy Benefit Management (PBM) organizations. The midstream consists of professional health, life, property, and reinsurance companies, as well as insurance brokerage firms responsible for product design. Further downstream are the channels that drive sales execution, including insurers’ self-operated official websites, professional intermediary channels, and third-party traffic platforms primarily based on social networking or payment services.

“Each party fulfills its respective responsibilities and complements the others. Upstream institutions in the health insurance sector effectively enhance insurers’ intelligent risk control capabilities through their professional service networks, mature systems, and refined data analytics. Meanwhile, the analytical results from these upstream entities further enable insurers to refine customer demand profiles, providing a data-driven foundation for delivering more targeted and differentiated insurance coverage and health management services.”

“At the business development level, by leveraging the specialized services and data from upstream institutions and combining them with the brand and traffic advantages of downstream channels, we assist insurance companies in designing human-centric, scenario-based insurance products or embedded marketing solutions, thereby more effectively enhancing their customer acquisition and repurchase capabilities. In short, the collaborative synergy among upstream and downstream players in the industry chain, with each fulfilling its respective responsibilities and complementing one another, helps optimize risk prevention and control as well as the end-to-end health management experience in health insurance.” Her company, Meideyi, is exploring localized PBM (Pharmacy Benefit Management) end-to-end solutions and has successfully validated a model centered on empowering insurance companies with risk control plus comprehensive health management services in fields such as dentistry.

Another trend is the entry of cross-industry players. According to public information, more than 50 health insurance companies are currently awaiting approval. Investors include internet giants such as Alibaba and Tencent, listed healthcare companies like Aier Eye Hospital, Kangmei Pharmaceutical, and Neusoft Group, as well as some listed real estate and manufacturing companies that are also planning to join the fray.

“New entrants from outside the industry should assess what is currently lacking in the health insurance sector. Internet giants can facilitate more robust information flow and a more convenient purchasing experience, while players from the pharmaceutical industry can bring sector-specific resources and deeper industry insights. There are already precedents for integrating medical services with insurance, such as the Kaiser Permanente model and Brazil’s experience with integrated healthcare.” Cross-industry players should leverage their respective strengths and advantages, which is more important than capital alone, said Guo Chao.

Insurance companies are also strengthening the ties between payers and upstream and downstream partners through equity investments, achieving deeper business integration to realize a win-win outcome. Taking China Life Insurance as an example, it established the China Life Grand Health Fund in 2016 to extensively lay out its presence in the medical and health sectors through capital linkages. It has since invested in multiple enterprises in areas such as medical services and medical technology, actively fostering business collaboration between these portfolio companies and China Life.

A senior executive from China Life Equity Investment told VCBeat that China Life has engaged in deep collaboration with its portfolio companies, including medical technology firms such as Winning Health Technology and Shanda Digiwin, in areas like medical insurance cost containment, direct billing for commercial health insurance, and big data platform development. Following its investment in Gushengtang, China Life integrated the company into its premium customer service ecosystem. Additionally, China Guangfa Bank, a subsidiary of China Life, co-branded a credit card with Gushengtang. These initiatives have not only effectively driven business growth for the enterprise but also enhanced the service experience for China Life’s customers.

It has become an industry consensus that both industrial and capital coordination are essential. An industry report released by the Insurance Association of China (IAC) points out that the greatest challenge facing the development of commercial health insurance in China is the lack of cooperative mechanisms with healthcare service providers for risk sharing, balanced interests, and information sharing. To improve this situation, efforts should focus on refining the operational design of critical illness insurance, promoting the participation of commercial health insurance in the supply-side reform of medical services, and establishing a legal framework for health data.

Health insurance should not be limited to mere coverage; instead, it should provide comprehensive protection grounded in health. Establishing an ecosystem that integrates “insurance + healthcare + wellness” not only delivers a superior insurance experience for policyholders but also maximizes the value of health insurance.