The Making of a Healthcare Oligarch: A 50-Year Evolution of CVS Health

On February 9, 2017, the General Office of the State Council issued the "Several Opinions on Further Reforming and Improving Policies for Drug Production, Circulation, and Use," which stated that outpatients may independently choose to purchase medications at either medical institutions or retail pharmacies, and medical institutions shall not restrict outpatients from filling prescriptions at retail pharmacies. In May 2017, the State Council’s Office of Healthcare Reform proposed in the "Key Tasks for Deepening Healthcare System Reform in 2017" to explore the interconnectivity and real-time sharing of prescription information from medical institutions, health insurance settlement data, and drug retail consumption information.

Meanwhile, giant chain pharmacies have reaped substantial rewards. In addition to achieving high profitability and rapid growth, large-scale mergers and acquisitions within the industry have intensified. In the first half of 2018, Yifeng Pharmacy added 440 new stores, including 209 through acquisitions; Dashenlin added 449 new stores, with 117 acquired; and Yixintang’s store count surpassed 5,376, with 349 newly built stores and a net increase of 198 stores. Meanwhile, Hillhouse Capital, another Chinese capital giant, is mobilizing hundreds of billions of yuan to make significant investments in chain pharmacies.

As a critical component of the terminal market in pharmaceutical distribution, pharmaceutical retail chain enterprises bear the significant responsibility of breaking the deadlock in China’s separation of prescribing and dispensing. At this pivotal juncture, how should China’s large-scale pharmaceutical retail chains leverage capital for strategic positioning? What layout models should they adopt? How can they achieve the transformation of traditional retail operations? And how can they establish distinctive pharmacy ecosystems tailored to their unique corporate attributes? We believe that the nearly two-century development history of the U.S. pharmacy retail market provides sufficient “answers.”

Our subject of study is CVS Health, the retail pharmacy oligopoly in the U.S. market. This remarkable company has achieved 20 years of consistent growth and successfully established its second growth curve through Pharmacy Benefit Management (PBM). It currently stands as a classic case of the only publicly listed integrated innovative pharmacy-healthcare chain enterprise.

Over the course of more than a month, VCBeat Research Institute reviewed CVS Health’s financial reports spanning two decades, with an analytical horizon extending back 50 years. The institute conducted a comprehensive analysis of CVS Health from four primary dimensions, encompassing more than ten secondary indicators and multiple tertiary metrics, culminating in the report titled “In-Depth Analysis of Pharmaceutical Retail Chain Transformation: Lessons from CVS Health.” This 87-page report, exceeding 35,000 words and featuring more than 20 core visual charts, thoroughly deconstructs how CVS Health rose to industry dominance, launched its second growth curve, and strategically positioned itself within today’s pharmaceutical retail ecosystem.

We will select two sections, condense certain content, and publish this report in two articles.

Article 1: The Formation of an Oligopoly—A 50-Year History of CVS Health;

Article 2: CVS Health’s Transformation from a “Single-Core” to a “Dual-Core” Business Model;

At the conclusion of this in-depth report, we will present 10 core “answers” regarding the development of pharmacy chain enterprises, aiming to provide reference for Chinese pharmacy chains in identifying the right growth path at the critical juncture of “separation of prescribing and dispensing.”

I. The Formation of an Oligopoly—A 50-Year History of CVS Health;

I. Breaking the Game: Industry Concentration Rises from 4.56% to 45.1%

2017 marked the first year in which the separation of prescribing from dispensing and the outflow of prescriptions were truly implemented. The state issued a series of policies to promote prescription outflow, further emphasizing and implementing specific measures for the separation of prescribing from dispensing and the outward flow of prescriptions. Meanwhile, prescription outflow will bring about structural adjustments in pharmaceutical distribution channels, representing both an adjustment of existing market share and a new growth point for the market. According to an analysis by VCBeat, after the realization of the “separation” between prescribing and dispensing, the theoretical incremental sales volume that can be brought to the pharmaceutical retail market is3772100 million yuan, while the total pharmaceutical retail market size will reach7451billion, the market size will nearly double.

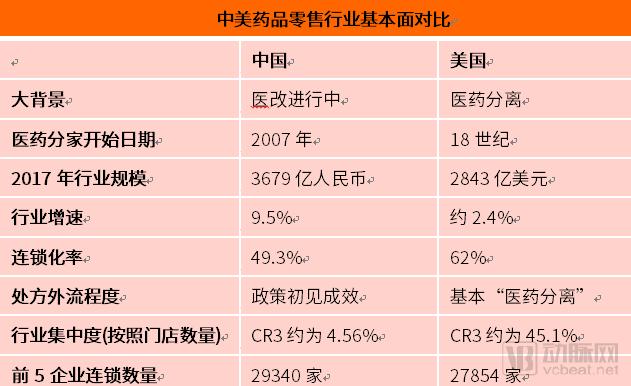

According to data from the U.S. and Chinese pharmacy chain industries, VCBeat Research Institute found that the concentration ratio of the U.S. pharmacy chain industry is 45.1%, while that of China’s pharmacy chain industry is only about one-tenth of the U.S. figure, at approximately 4.56%.Therefore, we believe that there is enormous potential in China’s pharmacy market. Driven by this sensitive data, publicly listed pharmaceutical retail companies are racing to secure their market share.

In the sweeping tide of healthcare reform,The Pharmaceutical Retail Industry Is Gradually Moving from the Sidelines to the Forefront. The Service Role at the Final End of Pharmaceutical Retail——Retail pharmacies are no longer merely passive recipients of market forces; instead, they must proactively undertake reforms. In response to the current challenges in the pharmaceutical retail industry—such as market fragmentation, pricing disorder, and low consumer trust—retail pharmacies need to foster transformation and emerge as innovators and pioneers in the marketplace.

II. The United States: The World’s Largest Single Pharmaceutical Retail Market

A. Key Metric: High Chain Affiliation

a) The chain pharmacy rate rose rapidly from 0% in 1900 to over 60% by the end of the 20th century;

B. Key Data Point 2: A Highly Concentrated Oligopolistic Industry Structure.

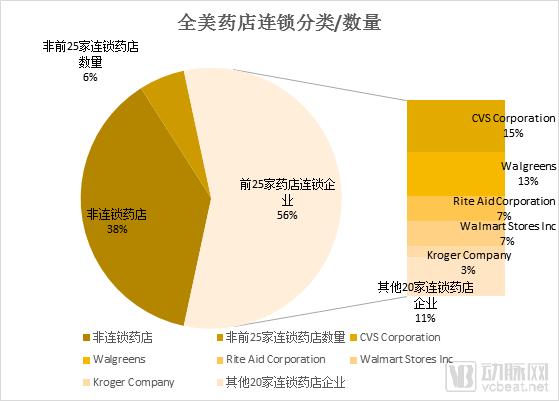

a) The top five pharmacy chains collectively operate 27,854 brick-and-mortar stores, accounting for 45.1% of all pharmacies nationwide;

b) The combined prescription drug market share of the top five pharmaceutical retail enterprises reached 60.3%;

The core backdrop to the development of the U.S. retail pharmacy industry is the separation of prescribing and dispensing. Over the three centuries since this separation was implemented, hospitals have generally maintained inpatient pharmacies but not outpatient pharmacies. Under the U.S. healthcare system, after receiving an outpatient diagnosis from a physician (without requiring hospitalization), patients obtain prescriptions from their doctors and purchase medications at independent pharmacies. At the point of purchase, the well-established U.S. health insurance system provides patients with adequate financial coverage. Throughout the long-term development of the U.S. retail pharmacy sector, chain pharmacies with strong management capabilities and significant scale advantages have become the dominant players in the pharmaceutical retail market. Against this backdrop, the U.S. pharmaceutical retail market has evolved through two main stages, gradually forming a retail landscape dominated by chain pharmacies.

According to the latest data from the “NATIONAL PHARMACY MARKET SUMMARY,” the total number of pharmacies in the United States in 2017 was 61,722, with 38,324 being chain pharmacies, resulting in a chain pharmacy rate of 62%.

The data in this report also indicates that among all chain pharmacies, the top 25 chain pharmacy enterprises collectively operate a total of 34,845 offline pharmacies, accounting for 56.45% of the total number of pharmacies nationwide and representing a share of all chain pharmacies.90.1%.The top five pharmacy chains collectively operate 27,854 stores, while the remaining 20 chains among the top 25 operate a total of 6,991 stores. This means that the number of offline outlets owned by the top five pharmaceutical retail chains accounts for 79.9% of the total number of pharmacies among the top 25 chain enterprises, and 45.1% of the total number of pharmacies nationwide.

Figure 1.1 Classification/Number of Pharmacy Chains Nationwide

Data Source:“National Pharmacy Market Summary,” public information, compiled by VCBeat

Chart by VCBeat · VBInsight

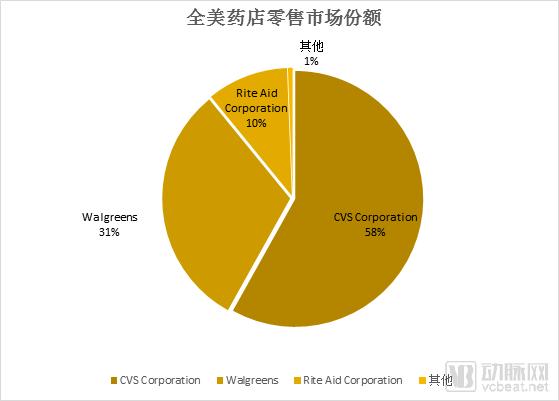

An analysis of sales across the entire U.S. retail pharmacy market reveals a more pronounced market structure, characterized by an oligopoly of “one emperor (CVS Corporation) and two kings (Walgreens and Rite Aid Corporation).”

Figure 1.2 U.S. Retail Pharmacy Market Share

Data Source:IBISWorld, public information, compiled by VCBeat

Chart by VCBeat · VBInsight

In another report, “Top U.S. pharmacies ranked by prescription drugs market share in 2017,” it was noted that the U.S. prescription drug market is similarly dominated by an oligopoly. The top five players by prescription drug market share were CVS Corporation (23.8%), Walgreens (15.6%), Express Scripts, Inc. (10.9%), UnitedHealth Group (5%), and Walmart Store, Inc. (5%), collectively accounting for 60.3% of the prescription drug market.

From these three sets of data, it is evident that after more than two decades of development, the U.S. chain pharmacy industry has evolved into a highly concentrated market structure characterized by an oligopoly.

III. China: Pharmaceutical Retail Chains on the Path of Healthcare Reform

1. Breaking the Deadlock: The “Shift” in Outflow of Prescription Drugs

A. One of the Core Policies: "Measures for the Administration of Prescriptions"

a) Date: Released on February 14, 2007; Effective May 1, 2007

b) Article 42:Excluding narcotic drugs, psychotropic substances, toxic drugs for medical use, and pediatric prescriptions,Medical institutions shall not restrict outpatients from purchasing medications at retail pharmacies using their prescriptions.

B. Core Policy No. 2: “Key Tasks for Deepening the Reform of the Medical and Healthcare System in 2016”

a) Date: April 21, 2016

b) Improve the Drug Supply and Guarantee Mechanism: Adopt Various Forms to Promote the Separation of Prescribing and Dispensing,Hospitals are prohibited from restricting the outflow of prescriptions; patients may freely choose to purchase medications either at the hospital’s outpatient pharmacy or at retail pharmacies with a prescription.(The National Development and Reform Commission, the National Health and Family Planning Commission, and the Ministry of Human Resources and Social Security shall be responsible respectively.)

C. Core Policy 3: “Plan for the Division of Key Tasks Among Departments under the Guiding Opinions on Promoting the Healthy Development of the Pharmaceutical Industry”

a) Date: July 12, 2016

b) Strengthening the Healthcare Service System: Medical institutions shall prescribe medications using their generic names.and proactively provide prescriptions to patients, safeguarding their right to choose where to purchase medications

The root cause of the core issue in the current pharmaceutical sector, known as “funding healthcare through drug sales,” lies in the contradictions among the monopoly position of large medical institutions, the medical service system, and the market economy. The key to resolving this issue is to start from the logic of the market economy and reform the current service system of medical institutions, thereby breaking the market monopoly held by large medical institutions and fostering a landscape of fair market competition. The critical breakthrough for such systemic change is to improve the compensation mechanism. Against the backdrop of broader medical reform, the focus of improving the compensation mechanism is the “separation of prescribing and dispensing,” with its core pathway being the “three-medical linkage,” namely, the coordinated reform of the medical insurance system, the healthcare delivery system, and the pharmaceutical distribution system. In summary, although reforms that touch upon vested interests are arduous and long-term, under the state’s firm commitment to advancing medical reform, the “separation of prescribing and dispensing” is an inevitable trend.

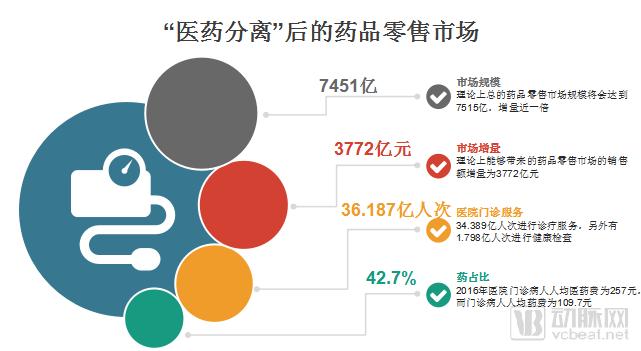

The separation of “medicine” and “pharmacy” means that pharmacies will be “decoupled” from hospitals, making pharmaceutical retail chains one of the biggest beneficiaries of prescription outflow. In the future, we can anticipate that patients will take prescriptions issued by doctors to pharmacies for medication purchases. The China Pharmaceutical Circulation Industry Development Report (2017) pointed out that in 2016, the total sales of seven major categories of pharmaceutical products nationwide reached RMB 1.8393 trillion, among which the retail pharmaceutical market accounted for only RMB 367.9 billion. Data from the 2018 China Health and Family Planning Statistical Yearbook showed that in 2017, the average per-capita medical expense for hospital outpatient visits was RMB 257, while the average per-capita drug expense was RMB 109.7, resulting in a drug-to-medical-expense ratio of 42.7%. The yearbook also noted that hospital outpatient services across all regions totaled 3.6187 billion visits in 2017, including 3.4389 billion diagnostic and treatment visits and 179.8 million health check-up visits. We can estimate that after the implementation of “separation of medicine and pharmacy,” based on an average per-capita drug expense of RMB 109.7, the theoretical incremental sales in the pharmaceutical retail market would reach RMB 377.2 billion, bringing the total theoretical size of the pharmaceutical retail market to over RMB 745.1 billion—nearly doubling the incremental growth.

Figure 1.3 Pharmaceutical Retail Market After “Drug Classification”

Data Source:“Development Report on China’s Pharmaceutical Distribution Industry (2017),” “2017 China Health and Family Planning Statistical Yearbook,” compiled by VCBeat.

Chart by VCBeat · VBInsight

2. The Market: The “1,000+ Stores” Era of Chain Pharmacies

A. GuanKey Data Point: The pharmaceutical retail chain rate reached 49.3%

a) There were 5,609 national pharmaceutical retail chain enterprises in China, a year-on-year increase of 12.6%; these chains operated 220,700 stores, a year-on-year increase of 7.7%;

b) There were 226,300 single-store pharmacies, a year-on-year decrease of 6.9%;

B. Key Data Point #2: Entering the “1,000+ Stores” Era

a) 17 companies already operate more than 1,000 stores each;

C. Key Data Point 3: Low Industry Concentration

a) The top three pharmacy chains by store count account for only 4.56% of the total number of stores nationwide;

Our research reveals that as the industry matures, the level of chain consolidation increases. With the continuous expansion of pharmacies’ business scope and the sustained growth in operational costs, chain-operated pharmacies offer greater investment value and development potential. The rapid growth of chain pharmacies is primarily attributed to:

I. Cost Advantages: The economies of scale resulting from chain expansion can significantly reduce procurement costs and substantially enhance pharmacies’ bargaining power with pharmaceutical manufacturers. Meanwhile, systematic operations enable the sharing of certain resources, thereby greatly improving the profitability of individual stores.

II. Operational Advantages: A core element of the standardized operational model is a standardized operational pathway. Standardized management can also significantly enhance clinic operational efficiency and boost industry competitiveness;

III. Capital Involvement: The significant influx of capital into pharmaceutical retail chain enterprises has substantially accelerated the pace of their chain expansion.

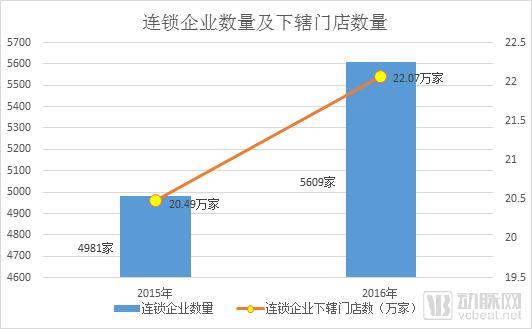

2016In 2025, the total number of retail pharmacies in China reached 447,000, a year-on-year decrease of 0.2%. Among them, the chain rate of the drug retail market has reached 49.3%. Data shows that there were 5,609 pharmaceutical retail chain enterprises, a year-on-year increase of 12.6%; with 220,700 stores under their management, a year-on-year increase of 7.7%. We believe that while the total number of retail pharmacies nationwide has not changed significantly, the substantial increase in the number of stores operated by pharmaceutical chain enterprises indicates:Independent pharmacies are rapidly declining, while the trend toward chain operations is accelerating further.

Figure 1.4 Number of Chain Enterprises and Their Subordinate Stores

Data Source:“Report on the Development of China’s Pharmaceutical Distribution Industry (2017)”

Chart by VCBeat · VBInsight

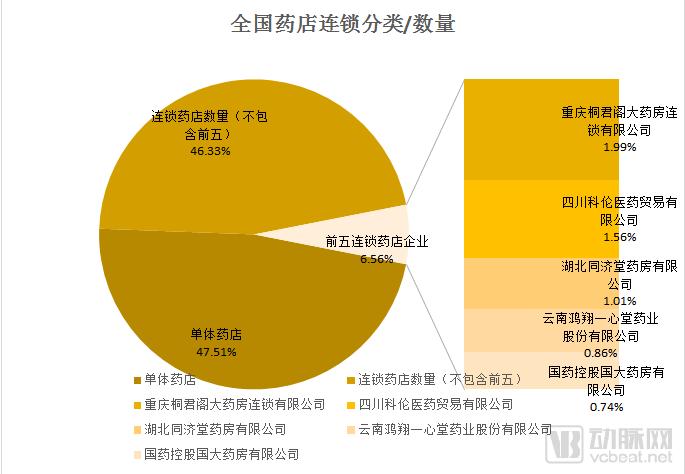

2016In China, the number of pharmaceutical retail chain enterprises with more than 100 affiliated stores has reached 87, among which 17 enterprises operate more than 1,000 stores. In terms of store count rankings, Chongqing Tongjungge Grand Pharmacy Chain Co., Ltd. has the largest number of stores, totaling 9,500; followed by Sichuan Kelun Pharmaceutical Trading Co., Ltd. with 7,423 stores; Hubei Tongjitang Pharmacy Co., Ltd. ranks third with 4,830 stores; and Guoda Pharmacy Co., Ltd. ranks fourth with 3,502 stores. Data analysis reveals that the top three pharmacy chain enterprises collectively operate approximately 21,743 stores, accounting for only 4.56% of the total number of pharmacies nationwide. Even Chongqing Tongjungge Grand Pharmacy Chain Co., Ltd., which has the largest number of stores, holds only about 2.12% of the total market share. Therefore, we believe that:Despite the continuous increase in the chain affiliation rate of pharmaceutical retail, industry concentration remains at a low level.

Figure 1.5 Classification of National Pharmacy Chains in China/Quantity

Data Source:《Report on the Development of China’s Pharmaceutical Distribution Industry (2017)》

Chart by VCBeat · VBInsight

IV. Similar Markets, Different Landscapes

A. Similar Markets in China and the United States:

a) The broader context of separating pharmaceuticals from medical services;

b) The Mainstream Trend of Industry Chain Integration;

c) The industry is shifting from fragmentation to consolidation;

B. Divergent Market Landscapes in China and the United States:

a) A market size difference of more than fivefold;

b) There is a significant gap in industry concentration;

c) Oligopolistic Market and Free Competitive Market;

C. China is at a stage that the U.S. retail pharmacy industry once experienced in its development.

The data in the table show:

1. China and the United States share a similar macro-level background;

2. Chain expansion is an inevitable development trend;

3. Large-scale pharmacy chain enterprises have already emerged;

4. Meanwhile, the industry will gradually consolidate, with large pharmacy retail enterprises acquiring small and medium-sized pharmacy retail enterprises;

However, at the same time, we must clearly see the facts:China is in the initial stage of "separation of prescribing and dispensing," while the United States has already established a robust healthcare system with this separation.Therefore, we believe that the development of China’s retail pharmacy sector is currently at an intermediate stage compared to the trajectory of the U.S. retail pharmacy industry. It is precisely this difference in developmental stages that accounts for the substantial disparity in market turnover and the markedly different market landscapes between the two countries. Despite being at different stages, a number of Chinese pharmacy chains have already achieved a certain scale of operations. However, at comparable scales, there remains a hundred-fold gap in profitability between their Chinese and U.S. counterparts. Once pharmacy chains reach a certain size, how to further tap into market potential has become a pressing challenge facing many players in the industry.

Although China and the United States are at different stages of development, China is following the path previously taken by the U.S. pharmacy retail industry. The U.S. experience may provide the answers we seek, which is also the objective of this report.

I. Introduction to CVS Health

CVS Health CorporationCentered on outstanding service, meeting customer needs, and delivering high-value customer experiences, and driven by innovation to address users’ healthcare needs, CVS Health Corporation leverages its unique integrated business model to provide innovative, channel-based solutions for patients, suppliers, and employees. This approach enables higher-quality healthcare services and enhanced customer experiences at lower costs. Currently, CVS Health Corporation operates more than 9,800 retail pharmacies and over 1,100 walk-in clinics, with its store network spanning 49 U.S. states as well as countries and territories including those in Europe, Brazil, Colombia, and Puerto Rico. CVS Health Corporation’s operations are primarily divided into two major segments:Retail Division and Pharmacy Services Division.

II. Three Stages of CVS Health’s Development

From the opening of its first convenience store in Massachusetts in 1963 to becoming a pharmaceutical retail chain giant with nearly 10,000 stores as reported in its 2017 annual report, CVS Health has emerged as one of the largest pharmacy retail giants in the United States. The half-century development of CVS Health is a legend in the evolution of pharmacy retail.

We have processed all historical data and events, dividing the development of CVS Health into three stages:

(1)Phase I (1963–1989) – Establishing a Foothold in the U.S. Market;

Analysis:

1. Expansion through a combination of mergers and acquisitions (M&A) and organic growth, with the latter being the primary strategy, resulting in over 500 self-built stores and 100–200 acquired stores;

2. Establish a regionalized chain layout;

3. Primarily engaged in pharmaceutical retail business;

(II)Phase II (1990–2012) – Market Capture + Diversified Development;

Analysis:

1. Aggressively acquired other pharmacy chain enterprises, with a total of more than 5,000 stores acquired, including the largest single transaction involving over 2,500 stores;

2. After the IPO, leverage capital to accelerate the capture of the U.S. market;

3. Establish a pharmacy ecosystem and pursue diversified development;

4. Establish a business model of “two core businesses + four services”;

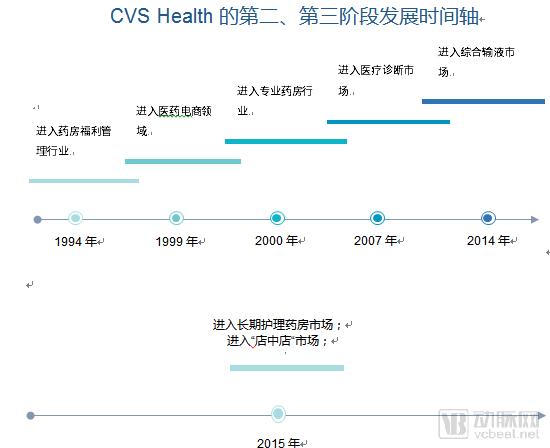

(III)Phase Three (2013–Present): Expanding Beyond the United States to Establish a Global Presence;

1. Expanding into overseas markets through mergers and acquisitions;

2. Expand the pharmacy ecosystem;

We have compiled CVS Health’s development from Phase II to Phase III, analyzed its growth data, and established a timeline of CVS Health’s development:

Given the current market conditions in China, the development of Chinese chain pharmacies is in the early stage of Phase II of CVS Health’s evolution. Therefore, this paper focuses on the transition from Phase II to Phase III of CVS Health’s development, aiming to draw insights from this progression.

This section constitutes the focal point and core of this article, detailing CVS Health’s transition from its second stage of development in the 1990s into its third stage. Over these two decades, CVS Health underwent rapid store expansion, extended its business scope, and ultimately built a comprehensive pharmacy ecosystem, evolving from a traditional pharmaceutical retail chain into a world-leading integrated innovative pharmacy and healthcare chain.

Starting from CVS Health’s annual report data, we will examine the underlying truths concealed within its historical records, dissect its core business operations, and provide a comprehensive description of the composition and evolution of CVS Health’s pharmacy ecosystem. Through an in-depth study of CVS Health, we will compile reference recommendations for the development of Chinese pharmaceutical retail chain enterprises.

I. Operations and Data: The Formation of Industry Oligopolies

1. Outstanding Financial Performance: Steady Growth in Revenue and Net Profit

We have visualized the above data in charts:

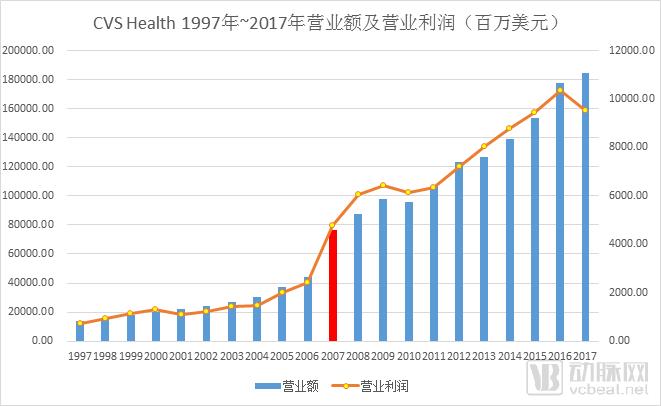

Figure 3.1 CVS Health Revenue Data from 1997 to 2017

Data Source: CVS Health Annual Report

Chart by VCBeat · VBInsight

As shown in the chart:

a. Operating Revenue: from US$13.7496 billion in 1997 to US$184.765 billion in 2017, an increase of nearly13.4x, maintaining rapid growth over the long term, with a CAGR of 14.65%.

b. Operating Profit:19972016–2017, operating profit increased from $717.5 million to $9.516 billion, a nearly13.2x, maintaining high-speed growth over the long term, with a CAGR of 14.5%.

c. The company is operating soundly, with both revenue and operating profit maintaining relatively stable, high-speed growth;

d. 2007In that year, operating revenue and profits saw significant growth, primarily due to the merger of CVS Corporation and Caremark Rx to form CVS Caremark, which became the leading integrated pharmacy services provider in the United States. The consolidation of financial statements from both companies also contributed to the substantial increase in performance.

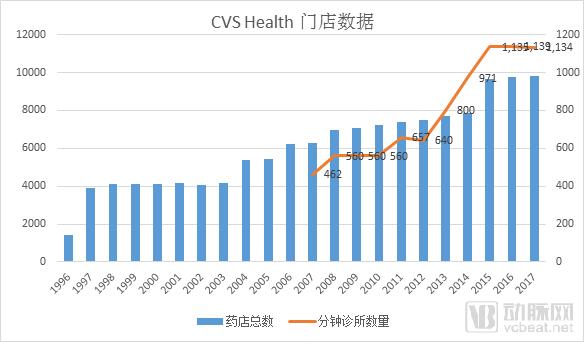

2. Store Data Continues to Grow, Offline Network Becomes Increasingly Comprehensive

We have visualized the above data in charts:

Figure 3.2 CVS Health Store Data

Source: CVS Health Annual Report

Chart by VCBeat · VBInsight

a. Number of Stores:Since 1996, the number of CVS Health’s chain pharmacy stores has grown from 1,400 to over 9,800, representing an increase of nearly 8,400 locations, with an average annual addition of approximately 400 stores.

b. Number of MinuteClinics:2007In 2018, CVS Health officially acquired MinuteClinic. The number of MinuteClinic locations grew from 462 in 2007 to 1,134 in 2017, an increase of nearly 700 clinics, with an average annual addition of approximately 70 new locations.

II. The “Three Pillars” of CVS Health’s Transformation

From 1997 to 2017, CVS Health evolved over two decades of steady growth into the world’s leading integrated, innovative pharmacy healthcare chain. Based on the preceding analysis, we believe that the core development logic underpinning CVS Health’s 20-year trajectory is"Six Steps":

Step 1:Rapid expansion of outlets through acquisitions;

Step 2:Meanwhile, leveraging its group advantages to explore the PBM business;

Step 3:PBMAfter the business reaches a certain scale, it begins to pursue mergers and acquisitions in the PBM sector;

Step 4:Expand business attributes both horizontally and vertically;

Step 5:Ultimately, a pharmacy ecosystem centered on the “pharmacy + PBM” business model will be established;

Step 6:Expand beyond the United States to pursue global business expansion;

Figure 3.3 CVS Health 2017 Core Business Statistics

Data Source: CVS Health Annual Report

Chart by VCBeat · VBInsight

In fact, CVS Health’s implementation of the six steps relies primarily on the “three pillars” of its corporate development strategy:

Approach 1: Achieve business expansion through store expansion;

Approach 2: Build a “dual-wheel” drive model of pharmacy + PBM;

Approach 3: Building CVS Health’s Pharmacy Ecosystem Through Two Core Departments;

For more details, see:

10 Breakthrough “Answers” on How Chinese Retail Pharmacy Enterprises Can Develop: Insights from CVS Health’s 20-Year Transformation (Part II)

Below is the complete table of contents. The full report consists of 4 chapters and 87 pages. To read the remaining chapters, please scan the QR code to become a VCBeat member and download the full report, or purchase the report individually in the VCBeat Reports section.

Contents

Chapter 1Insights Retail Pharmacy Systems in China and the United States............................................................... 6

I.Breaking the Deadlock: Industry Concentration Rises from 4.56% to 45.1%................................................................................................. 6

II.United States The World's Largest Single-Drug Retail Market................................................................................................... 6

1.A Century Two Phases...................................................................................................................... 7

III.Pharmaceutical Retail Chains on China's Path of Healthcare Reform..................................................................................... 11

1.Breaking the Deadlock The “Change” in Prescription Outflow............................................................................................................ 11

2.Market "Chain Pharmacies' 'Thousand Stores+“Era”.............................................................................................. 13

IV. Similar Markets, Different Landscapes.................................................................................................................... 16

Chapter 2Oligarch CVS Health’s Business Empire.................................................... 18

I.CVS HealthIntroduction............................................................................................................................... 19

II.CVS HealthThree Stages of Development.................................................................................................................... 19

Chapter 3InsightsFromCVS HealthThe Formation of Oligopolies from the Perspective of Models.................................. 25

I.Operations and Data The Formation of Industry Oligopolies............................................................................................................ 25

1.Outstanding Financial Data Steady Growth in Operating Revenue and Net Profit............................................................................. 25

2.Store Data Continues to Grow Offline Networks Are Becoming Increasingly Robust........................................................................................ 27

II.CVS HealthThe "Three Carriages" of Transformation..................................................................................................... 28

III.Store Layout Drives Performance Growth CVS HealthStore Self-Portrait......................................................................... 29

1.Total Number of Offline Stores11083Home................................................................................................. 30

2.Strategic Offline Layout in High-Potential Markets............................................................................................................ 33

3.Large-Scale M&A as the Primary Mode of Expansion............................................................................................................ 37

IV.Transition from “Single-Core” to “Dual-Core” Business Model.................................................................................................. 38

V.Collaboration Between Two Core Departments Co-buildingCVS Health's Business System.................................................................... 41

1.Two Major Divisions: Pharmacy Services Division and Retail Division.......................................................................................... 42

2.Two Core Businesses+Four Major Extended Services+Multi-Brand Drive.................................................................................. 44

a.One of the Core Businesses: Retail Pharmacy Services.............................................................................................. 46

b.Second Core Entity: Pharmacy Benefit Management (PBM).............................................................................. 53

c.Extended Service 1: Walk-in Clinic Services.............................................................................................. 62

d.Extended Service II: Comprehensive Infusion Services................................................................................................. 66

e.Extended Service 3: Professional Pharmacy Services.................................................................................................. 70

f.Extended Service 4: Long-Term Care Pharmacy Services........................................................................................... 73

VI.CVS HealthEcosystem Map of Pharmacies......................................................................................................... 75

Chapter 4Development of Pharmacy Chain Enterprises10Core “Answer”................................... 80