The Strategic Triumph: How PBM Business Fueled CVS Health's Second Growth Curve

Over the course of more than a month, VCBeat reviewed CVS Health’s financial reports from the past 20 years, with an analytical horizon spanning 50 years. The analysis of CVS Health Corporation was conducted across four dimensions, encompassing more than ten secondary indicators and multiple tertiary indicators, culminating in the report “In-Depth Analysis of the Transformation of Pharmaceutical Retail Chains: A Case Study of CVS Health》. Spanning 87 pages and over 35,000 words, and featuring more than 20 core charts, this report provides an in-depth deconstruction of how CVS Health rose to become an industry giant, launched its second growth curve, and is currently strategizing its layout within the pharmaceutical retail ecosystem.

This is the second article based on the report. The first article, “The Formation of an Oligopoly: A 50-Year History of CVS Health,” was published on November 14 on VCBeat and WeChat Top Headlines.

CVS Health began resetting its strategic development plan in 1994, launching a transformation strategy centered on a “dual-core” growth model built upon an offline retail network and driven by pharmacy benefit management (PBM).

For CVS Health, the layout of its brick-and-mortar stores forms the foundation of the group’s business, while its PBM (Pharmacy Benefit Manager) operations serve as the primary engine driving rapid growth. These two pillars mutually support and reinforce each other, creating a synergistic “DNA double helix” business structure.

By making substantial investments in its PBM business, CVS Health has transformed its growth model from one traditionally driven by pharmaceutical retail to a dual-engine strategy powered by “Pharmacy Benefit Management + Pharmaceutical Retail,” thereby driving overall corporate growth.

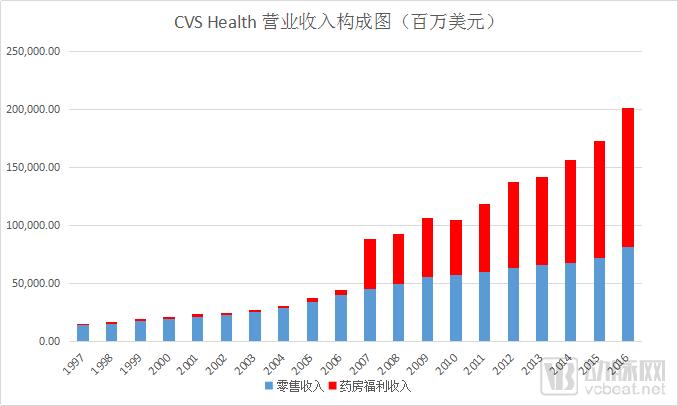

Since launching its pharmacy benefit management (PBM) business in 1994, CVS Health initially attempted to build this segment through its own retail pharmacy network. After a decade of exploration, CVS Health’s PBM business achieved year-over-year growth, reaching $3.683 billion in 2006. In 2007, CVS Corporation (its former name) merged with Caremark Rx to form CVS Caremark (now renamed CVS Health). By leveraging Caremark Rx’s established PBM operations and integrating the advantages of its offline retail network, CVS Health successfully transformed its revenue model from a single-engine reliance on pharmaceutical retail to a dual-engine drive combining pharmaceutical retail and PBM services.

We have visualized the above data in charts:

Figure3.5 CVS Health Revenue Composition Chart

Data Source:CVS Health Annual Report

VCBeat·Chart by VCBeat

Based on an analysis of its revenue structure, we believe that the characteristics of CVS Health’s revenue are as follows:

An analysis of CVS Health’s investment history reveals that the company entered the pharmacy benefit management (PBM) industry as early as 1994. However, data indicate that cross-industry expansion proved challenging for a traditional pharmaceutical retail enterprise. Between 1997 and 2007, although CVS Health operated its own PBM business, it accounted for a very small proportion of the company’s overall operations; by 2006, PBM services represented only approximately 8.4% of total revenue.We can consider that, in the more than ten years prior to 2007, CVS Health had been striving to vigorously expand its PBM business; however, in reality, its revenue remained predominantly driven by pharmaceutical retail sales.

ApprovedAfter more than a decade of accumulation, although PBM revenue accounts for a relatively small proportion of CVS Health’s total income, the company has in fact established a comprehensive pharmacy benefit management business line. In 2007, CVS Corporation (its former name) merged with Caremark Rx to form CVS Caremark.Through Mergers and AcquisitionsPBM Business Truly Becomes a Core Business of the Group. In 2007, the PBM business experienced explosive growth, with its share of operating revenue reaching 56.7%, representing a nearly seven-fold year-on-year increase, and officially becoming one of CVS Health’s two core businesses.。Through mergers and acquisitions, CVS Health has achieved a dual-core business model with parallel growth.

After 2007, CVS Health’s PBM business experienced rapid growth, supported by its extensive pharmacy network. Between 2007 and 2017, PBM revenues grew from $43.3 billion to $130.596 billion, representing an approximately threefold increase. In terms of revenue composition, PBM sales completely surpassed traditional pharmaceutical retail income, accounting for 70.6% of the total. The development of the PBM business has truly enabled CVS Health to transform from a traditional pharmaceutical retailer into an integrated, innovative pharmacy health care chain enterprise driven by both pharmaceutical retail and core pharmacy benefit management capabilities.

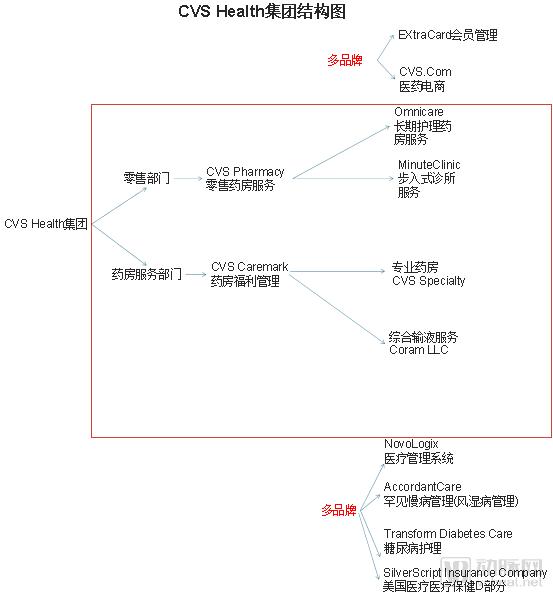

From the perspective of CVS Health’s business model, the entire group is divided into two core segments: the Pharmacy Services segment and the Retail segment. The essence of the Pharmacy Services segment lies in earning management fees and other related charges by entering into agency contracts with institutions or enterprises; whereas the Retail segment generates profits through online and offline sales. In recent years, as their respective business lines have continued to expand, both segments have exhibited a certain degree of cross-segment operations. Together, these two segments account for nearly all of CVS Health’s revenue. We have compiled and analyzed the businesses and affiliated entities of both the Pharmacy Services and Retail segments.

FromSince the early stage of the second phase of CVS Health’s development, alongside market expansion, the Group has diversified from a single pharmaceutical retail business into building a comprehensive pharmacy ecosystem. We have conducted an in-depth study of CVS Health’s annual reports from its listing in 1997 through 2017 to analyze its entire pharmacy ecosystem, excluding certain non-core departments and businesses.We believe:CVS Health has gradually built a business ecosystem centered on its two core divisions, with payers, patients, suppliers, and physicians as its foundation, aiming for high quality, high accessibility, and low cost. This ecosystem is structured as follows: two core business units + four extended services + multi-brand drive.

These two major service entities are:Retail Pharmacy Services (Retail Division Subordinates) and pharmacy benefit management (under the Pharmacy Services Department),Primarily byProvided by the two major brands, CVS Pharmacy and CVS Caremark.

The four major value-added services are:Walk-in diagnostic services, comprehensive infusion services, long-term care pharmacy services, and specialty pharmacy services are primarily offered under the brands MinuteClinic, Coram LLC, Omnicare, and CVS Specialty, respectively.

Multi-brand primarily refers to:Formed through mergers and acquisitions driven by vertical or single-domain business needs,For example:NovoLogix healthcare management system, AccordantCare rare and chronic disease management (rheumatology management), Transform Diabetes Care, SilverScript Insurance Company (U.S. Medicare Part D), and other brands.

Figure3.6 CVS Health Organizational Chart

Source: VCBeat·VCBeat

VCBeat· Chart by VCBeat

1. One of the Core Businesses: Retail Pharmacy Services

CVS Health’s retail pharmacy services fall under its Retail segment and represent the Group’s most core asset. The overall retail pharmacy operations comprise multiple brands, with a total of 9,803 retail pharmacies.The core brand is a self-built brand.CVS Pharmacy。With thisWith 9,803 brick-and-mortar pharmacies serving as the operational backdrop and physical stores acting as the central hub, these locations not only facilitate CVS Health’s core retail operations but also support the majority of the group’s other business lines, primarily those related to Pharmacy Benefit Management (PBM). Overall, these 9,803 offline pharmacies constitute CVS Health’s most critical assets, with the bulk of the group’s businesses relying on this retail pharmacy network for execution. We believe that the success of CVS’s retail pharmacy services is primarily attributable to the distinctive characteristics of its business model and its effective market positioning.

We believe that the five major values of retail pharmacy services are:

1) PBM Offline Connector;

2) Market positioning for product diversification;

3) The most successful ExtraCard membership service;

4) External Collaboration Portal;

5) Foundation for Building the Pharmacy Ecosystem;

(For each of the above values, VCBeat Research conducts a valuable attribute analysis and an analysis of application scenarios in China, taking into account multiple factors. For details, please refer to the full report.)

2. Second Core Business: Pharmacy Benefit Management (PBM):

Pharmacy Benefit Management (PBM) is a specialized third-party service. The PBM model primarily serves as a management and coordination intermediary among insurance/benefit providers, pharmaceutical manufacturers, patients, and pharmacies. It was established to effectively manage healthcare costs, reducing medical expenditures for payers while enhancing benefits for drug consumers. At the core of the U.S. PBM model is its penetration into every segment of the pharmaceutical distribution chain, balancing the interests of payers, suppliers, distributors, and consumers through contractual agreements. PBM organizations leverage robust databases to develop formularies and provide cost-effective prescription medications tailored to the specific drug needs of different clients. This approach ensures patients receive high-quality treatment while simultaneously lowering healthcare costs for payers. The primary roles of the PBM model within the entire pharmaceutical distribution system are as follows:

1) Establish a database using extensive clinical data and medication history data of insured individuals to conduct rationality reviews of prescriptions issued by physicians;

2) Strengthened oversight of patient medication, curbing over-treatment and drug abuse;

3) Leverage its user base advantage to effectively control prescription drug costs by signing contracts with pharmacies and pharmaceutical manufacturers, utilizing its strong bargaining power;

4) Reduce insurance expenditures and achieve medical cost containment;

5) Connects multiple stakeholders in the pharmaceutical distribution industry (primarily patients, insurance institutions, pharmacies, and pharmaceutical companies), and achieves the integration of multi-party resources;

CVS Health's Pharmacy Benefit ManagementServices (PBM business) belongs to the pharmacy services department, with the main providers beingCVS Caremark:In 2007, CVS Health established the CVS Caremark brand through a merger and acquisition. The brand grew to become the largest pharmacy benefit manager (PBM) in the United States, with its primary clients including large corporations, insurance companies, government health programs, and individuals.

The 2017 annual report shows that CVS Health’s Pharmacy Services segment was the group’s primary source of operating revenue, generating $130.59 billion, which accounted for 70.68% of total operating revenue, with PBM business constituting the major component of Pharmacy Services.

CVS Health’s PBM business leverages the company’s robust group advantages to integrate its information systems, healthcare professionals, and pharmacy resources. By utilizing its strong bargaining power to coordinate with upstream and downstream players in the pharmaceutical distribution industry, it reduces medical expenditure while ensuring that stakeholders of contracted parties receive comprehensive healthcare coverage. CVS Health’s PBM services primarily include: a) designing pharmacy benefit plans; b) processing prescription drug claims; c) reviewing the appropriateness of prescription medications; d) developing incentives to encourage the use of cost-effective prescription drugs; and e) providing mail-order pharmacy services.And allAmong the functions of PBM, the most core key is prescription review.

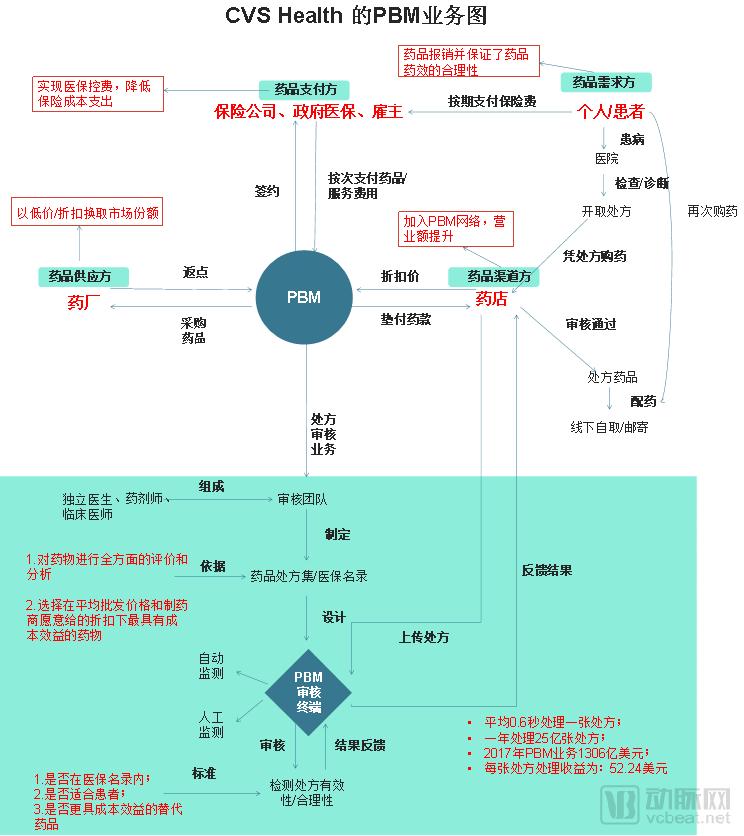

By organizing and analyzing CVS Health’s PBM business, with a particular focus on prescription audit operations, we have visualized the operational aspects of its PBM business. Its primary business model is as follows:

Figure3.7 CVS Health PBM Business Operations ChartData Source: VCBeat · VBInsightChart produced by VCBeat · VBInsight

Analyze from the perspective of demand,The core stakeholders of a Pharmacy Benefit Manager (PBM) are four parties: the drug payer, the drug supplier, the drug consumer, and the drug distribution channel. Each of these parties has its own core interests. By positioning itself as a multi-party coordinator, the PBM addresses the core needs of all four sides, balancing their demands while facilitating a mutually profitable outcome for all.

PBM Business Core Processes:

CVS Health’s PBM business is built precisely upon the needs of these four parties. After patients purchase health insurance, insurers are required to reimburse them for prescription medications. Driven by the imperative to control healthcare expenditures and reduce costs, while simultaneously safeguarding patient interests, insurers enter into agency agreements with CVS Health’s PBM subsidiary. By paying a fixed fee, insurers engage the PBM to review prescription drugs, thereby achieving their goal of lowering healthcare costs. Upon executing the agency agreement, the PBM establishes an independent review team composed primarily of independent physicians, pharmacists, and clinicians. Through professional medication reviews and assessments conducted by this team, combined with drug procurement costs negotiated with pharmaceutical manufacturers, the PBM develops a most cost-effective drug formulary/insurance coverage list. This most cost-effective drug formulary/insurance coverage list is primarily based on:

a) Comprehensive evaluation and analysis of the drug

b) Select the most cost-effective medication based on average wholesale prices and discounts offered by manufacturers

For patients, when they present a prescription at a CVS Health contracted pharmacy to fill it, the entire PBM workflow is equally straightforward:

1) Pharmacies upload prescriptions to CVS Health’s PBM review terminal system;

2) Automatic review in the PBM terminal system;

3) PBM Automated Prescription Review: a. Whether it is included in the medical insurance formulary; b. Whether it is suitable for the patient; c. Whether there are more cost-effective alternative medications;

4) Provide feedback on the test results to the contracted pharmacies;

5) Upon approval, the pharmacist dispenses the medication to the patient according to the prescription;

6) Perform automatic settlement (compensation is processed according to the system's predefined workflow);

7) The insurer settles payments with the PBM company under CVS Health;

8) PBM handles settlement with contracted pharmacies;

We believe that the five major values of PBM services are:

1) Control healthcare insurance costs at the source.CVS Health enters into contracts with pharmaceutical companies, healthcare providers, insurance companies, or hospitals to review prescriptions through audit terminals. This approach influences the prescribing behaviors of physicians and pharmacists from a market economy perspective, without compromising the quality of medical services, thereby achieving the goal of controlling the growth of drug costs.

In light of China’s actual circumstances, cost containment in medical insurance represents one of the most severe challenges currently facing the health insurance industry. From the perspective of the health insurance sector, China’s current reimbursement system—whether for government-sponsored basic medical insurance or commercial health insurance—primarily follows a “treat first, reimburse later” model. Under this framework, physicians prescribe medications or propose treatment plans, and patients subsequently obtain the prescribed drugs or undergo the proposed treatments.The fundamental objective of medical insurance cost containment is to address the phenomena of “over-treatment” and “drug abuse.” However, resolving these issues within China’s current healthcare system proves difficult. The primary reason is that even when prescribed medications are included in the medical insurance formulary, there is no mechanism to verify whether the physician’s prescription represents the most cost-effective option or is truly appropriate for the patient. Furthermore, once patients have obtained their medications or received treatment, insurance institutions are obligated to provide reimbursement as long as the services fall within the scope of the insurance policy terms, regardless of whether the treatment plan was genuinely reasonable.We believe that one of the truly effective approaches to addressing medical insurance cost containment is to tackle the issue at its source: the prescription process. By implementing prescription audits, we can establish a new workflow of “audit first, reimburse second, and treat last.”

However, we must acknowledge that most insurance companies are unable to conduct prescription reviews independently, primarily due to limitations in medical expertise, the availability of medical professionals, and structural issues within the healthcare system. Therefore, it can be argued that even though the development model for Pharmacy Benefit Management (PBM) business in China remains unclear, PBM services can address the market’s critical need for controlling health insurance costs against the backdrop of broader efforts to curb healthcare spending and separate prescribing from dispensing.

2) The most successful prescription traffic platform.In addition to generating substantial direct revenue, CVS Health’s PBM business creates significant traffic dividends by processing prescriptions from multiple sources. As pharmaceuticals are tangible goods that must be physically dispensed regardless of the purchasing method, the annual processing volume of 2.5 billion prescriptions translates into 2.5 billion instances of medication pickup services. The online PBM channel captures a large volume of prescriptions and directs this traffic to offline retail pharmacies (acting as connectors). These physical stores then facilitate the conversion of consumer profiles, effectively integrating online traffic with brick-and-mortar pharmacy operations. The PBM business and physical pharmacies are inextricably linked and mutually reinforcing, delivering synergistic effects far greater than a simple “1+1” sum.

In the context of China’s actual situation: For pharmaceutical retail chain enterprises, as the terminal end of the pharmaceutical distribution industry, the most efficient customer acquisition method is platform-driven traffic generation. By laying out PBM (Pharmacy Benefit Management) operations and obtaining substantial prescription traffic through prescription audits, these enterprises can then direct this traffic to offline retail pharmacies. Based on our previous analysis, we believe that the market pain point addressed by this traffic-generation model is the need for medical insurance cost containment. By targeting this pain point, PBM services have a certain market presence in China. Similarly, we acknowledge the differences between domestic and international contexts, which will result in significant disparities in the market size of PBM services and their corresponding direct economic benefits. Nevertheless, we still maintain that, within a certain cost framework, implementing PBM can bring extremely considerable prescription traffic conversion to pharmaceutical retail chain enterprises.

3) Diversified Revenue StreamsCVS Health’s revenue streams are primarily derived from: 1. service fees/agency fees under contracts; 2. rebates from pharmaceutical manufacturers; and 3. the margin between the “discounted price” offered by pharmacies and their procurement costs. Although government regulations strictly control drug prices, resulting in relatively low gross profit margins, CVS Health’s massive scale—processing 2.5 billion prescriptions annually—generates substantial operating revenue. According to CVS Health’s annual report, the average processing time per prescription is approximately 0.6 seconds, with each prescription contributing $52.24 in related revenue to the Pharmacy Services segment. The diversification of CVS Health’s PBM (Pharmacy Benefit Manager) business revenue is mainly attributed to: 1. business demand driven by multi-party market needs; 2. bargaining power stemming from its enormous transaction volume; and 3. channel advantages provided by CVS Health’s extensive network of brick-and-mortar retail pharmacies.

In light of China’s actual conditions: according to current statistics on the number of retail chain pharmacies in the country, 17 enterprises operate more than 1,000 stores each. These 17 pharmacy chains have already achieved a certain scale in the market and possess a degree of channel advantage. However, this channel advantage has not yet been leveraged for secondary business development. Therefore, expanding into Pharmacy Benefit Management (PBM) services would allow these companies to fully capitalize on their existing pharmacy network advantages. Their development path resembles that of CVS Health, which transitioned from traditional pharmaceutical retail to establishing a PBM business.

Amid the broader context of separating prescription from dispensing and controlling healthcare insurance expenditures, we believe that multifaceted market demand has gradually taken shape and may eventually reach a tipping point. However, whether the strong bargaining power derived from substantial patient volume can be effectively realized in China remains uncertain and requires further exploration. The primary reasons are: 1) large pharmaceutical manufacturers already possess significant bargaining power; and 2) the National Reimbursement Drug List (NRDL) and drug pricing are subject to state regulation. Consequently, in the Chinese market, the price advantages that PBM businesses could leverage through their bargaining power are significantly constrained when dealing with pharmaceutical companies. Nevertheless, by formulating reimbursement lists and pricing for certain new and specialized drugs (those not covered by basic medical insurance), PBM businesses still retain a degree of market bargaining power in the realm of commercial health insurance drug reimbursements.

4) A win-win situation for all parties.Beyond its own generated revenue, CVS Health’s PBM creates a multi-party win-win scenario, positioning the PBM business for strong growth prospects:

a) Drug payers: Pay insurance premiums on schedule, reduce medical payment costs for payers through prescription review;

b) Drug suppliers: By leveraging the large customer base of insurance providers, drug suppliers gain access to formularies and national reimbursement lists, thereby securing sales channels, obtaining substantial drug orders, and significantly boosting sales revenue;

c) Drug demand side: drug quality is guaranteed, excessive medical treatment and drug abuse are controlled, and the consumption experience is improved;

d) Pharmaceutical distribution channels: Gain access to a large base of insured customers through the PBM network. In addition to revenue generated from PBM-prescribed medications, the increased foot traffic of customers purchasing prescriptions at pharmacies also drives a significant rise in retail product sales.

In the context of China's actual situation: PBM business can also achieve a landscape of diversified profitability.

1. Both public health insurance and commercial insurance can achieve cost containment through PBM services, thereby reducing costs;

2. Although the majority of the reimbursement drug list and pricing are established at the national level, PBM services have driven sales growth for certain new specialty drugs not covered by basic medical insurance;

3. The core business of PBM, prescription review, not only reduces costs but also ensures the rationality of prescriptions, safeguarding medication safety for patients;

4. After pharmacies integrate into the PBM business network, they can leverage PBMs for patient referral and traffic generation, thereby driving sales growth.

5) Foundation for Building the Pharmacy Ecosystem.Construction of the Pharmacy Ecosystem: PBM Services as an Indispensable Component. PBM services constitute one of the two core pillars of CVS Health’s pharmacy ecosystem, primarily including:

a) To provide services to other businesses within the ecosystem through its own PBM business (primarily focused on claims adjudication);

b) Leverage the traffic dividends from the PBM business to accelerate the development of other businesses within the ecosystem;

The construction of the entire CVS Pharmacy ecosystem will be detailed in subsequent sections.

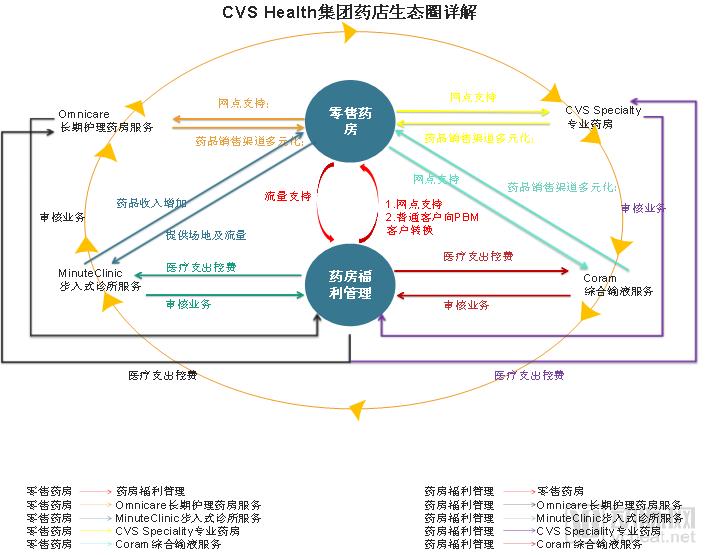

By analyzing all of CVS Health Group’s core businesses in the preceding sections, we have constructed an ecosystem map of CVS Health.

Figure 3.13 CVS Health Integrated Infusion Services Operations Chart Data Source: VCBeat·VBInsight Chart produced by VCBeat·VBInsight

We refer to CVS Health’s ecosystem as:Aggregated Ecosystem.CVS Health establishes nodes across its ecosystem through mergers and acquisitions or organic development, thereby maintaining full control over the entire ecosystem. By leveraging the services provided by these various nodes, CVS Health channels multi-party resources toward its core business.Retail Pharmacy and Pharmacy Benefit Managementmove closer. Therefore,Aggregated ecosystem refers to strengthening a company’s core value by building an ecosystem.

In the full report “In-Depth Analysis of the Transformation of Pharmaceutical Retail Chains: A Case Study of CVS Health》will provide a more detailed analysis of CVS Health’s aggregated three-tier ecosystem map, interpreting the logic behind its construction of a pharmaceutical retail ecosystem.

Meanwhile, the full report provides a more detailed analysis of CVS Health’s four value-added services: walk-in diagnostic services, comprehensive infusion services, long-term care pharmacy services, and specialty pharmacy services. For each business line, the report offers a thorough description of its characteristics and presents an exclusive business map. Based on the nature of each business and its corresponding business map, we interpret the multiple values that each business line contributes to the CVS Health ecosystem.

Finally, by integrating our in-depth analysis of CVS Health presented in this article, we will provide 10 core “answers” for the transformation journey of Chinese pharmacy chain enterprises!

For more details, see:

“An In-Depth Analysis of CVS Health: The Transformation of Pharmaceutical Retail Chains”

Below is the complete table of contents. The full report consists of 4 chapters and 87 pages. To read the remaining chapters, please scan the QR code to become a VCBeat member and download the full report, or purchase the report individually in the VCBeat Reports section.Click here to purchase

Table of Contents

Chapter 1VBInsight The Retail Pharmacy Systems in China and the United States............................................................... 6

I. Breaking the Deadlock: Industry Concentration Rises from 4.56% to 45.1%................................................................................................. 6

II. The United States: The World’s Largest Single Market for Retail Pharmaceuticals................................................................................................... 6

1. One Century, Two Stages...................................................................................................................... 7

III. Pharmaceutical Retail Chain Enterprises on the Path of China’s Healthcare Reform..................................................................................... 11

1. Breaking the Deadlock: The “Changes” in Outflow of Prescriptions............................................................................................................ 11

2. Market: The Era of “1,000+ Stores” for Chain Pharmacies.............................................................................................. 13

IV. Similar Markets, Different Landscapes.................................................................................................................... 16

Chapter 2Oligarch CVS Health's Commercial Empire.................................................... 18

I. Introduction to CVS Health............................................................................................................................... 19

II. Three Stages of CVS Health’s Development.................................................................................................................... 19

Chapter 3InsightsFromCVS HealthThe Formation of Oligopolies from the Perspective of Patterns.................................. 25

I. Operations and Data: The Formation of Industry Oligopolies............................................................................................................ 25

1. Outstanding Financial Performance: Steady Growth in Revenue and Net Profit............................................................................. 25

2. Store Data Continues to Grow, and the Offline Network Becomes Increasingly Comprehensive........................................................................................ 27

II. The “Three Pillars” of CVS Health’s Transformation..................................................................................................... 28

III. Store Layout Drives Performance Growth: CVS Health’s Store Self-Portrait......................................................................... 29

1. A total of 11,083 offline stores of various types................................................................................................. 30

2. Offline Strategic Layout in High-Potential Markets............................................................................................................ 33

3. Large-scale M&A as the Primary Mode of Expansion............................................................................................................ 37

IV. Business Transformation from “Single Core” to “Dual Core”.................................................................................................. 38

V. Collaboration Between Two Core Departments to Build the CVS Health Business System.................................................................... 41

1. Two Major Departments: Pharmacy Services Department and Retail Department.......................................................................................... 42

2. Two Core Businesses + Four Extended Services + Multi-Brand Promotion.................................................................................. 44

a. One of the Core Businesses: Retail Pharmacy Services.............................................................................................. 46

b. Second Core Entity: Pharmacy Benefit Management (PBM).............................................................................. 53

c. Extended Service 1: Walk-in Clinic Services.............................................................................................. 62

d. Extended Service 2: Comprehensive Infusion Services................................................................................................. 66

e. Extended Service 3: Professional Pharmacy Services.................................................................................................. 70

f. Extended Service 4: Long-Term Care Pharmacy Services........................................................................................... 73

VI. CVS Health’s Pharmacy Ecosystem Map......................................................................................................... 75

Chapter 4Development of Pharmacy Chain Enterprises10Core "Answer"................................... 80