Land Grabbing and Rapid Expansion: China's Third-Party Medical Laboratory Market

Editor’s Note: This article is republished from 36Kr Jingzhun Research Institute, authored by Jiang Juntao, and reposted by VCBeat with authorization.

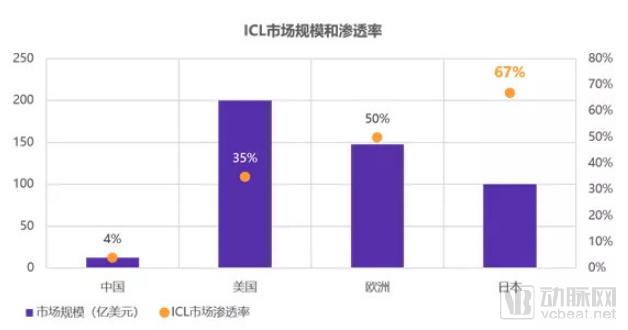

Guided by policies promoting tiered diagnosis and treatment as well as health insurance cost containment, the third-party medical testing market in China has achieved a compound annual growth rate (CAGR) of over 30% in recent years. In 2017, the total revenue of this market reached approximately RMB 12 billion, with a penetration rate of less than 5%, significantly lower than the roughly 50% penetration rate observed in developed countries. This indicates that China’s independent clinical laboratory (ICL) industry holds broad prospects for development.

To this end, we intend to discuss the following issues in this report:

1. What are the advantages of the ICL industry compared to traditional hospital clinical laboratories?

2. What is the current competitive landscape and development status of the ICL industry?

3. How do government policy guidelines impact the ICL industry?

4. Characteristics of Business Classification in Medical Laboratory Testing Services: What Are the Industry’s Key Features?

5. What are the development trends for the domestic ICL industry in China, and what types of companies are entering the ICL sector?

Independent Clinical Laboratory (ICL) refers to a medical institution that is licensed by health administrative authorities, possesses independent legal entity status, operates independently of other medical institutions, is capable of independently assuming relevant medical liabilities, and provides medical testing or pathological diagnostic services.

Compared with the clinical laboratories of medical institutions, the main advantages of ICLs are reflected in two major aspects: cost and level of specialization.

1) By centrally providing outsourced medical laboratory services to various healthcare institutions, centralized procurement of equipment and reagents can effectively reduce procurement costs, while high-volume testing can lower the fixed cost per test.

2) Centralized testing also enables ICLs to achieve specialized division of labor, allowing them to perform high-end, complex tests that hospital laboratories cannot conduct due to low sample volumes and high costs. Through specialized division of labor and economies of scale, ICLs surpass hospital laboratories in terms of test menu diversity, efficiency, and technical proficiency.

Benefiting from tiered diagnosis and treatment systems and medical insurance cost containment, the ICL industry addresses key pain points and boasts a promising future.

Tiered Diagnosis and Treatment Gradually Opens Up the Primary Care Market: China suffers from severe inequities in the distribution of medical resources, with relatively poor primary care resources and service capacity. This has led patients to blindly rely on large hospitals, resulting in a waste of medical resources.

In 2017, tertiary hospitals, accounting for 11% of the total, handled 53% of patient visits, with an average annual bed occupancy rate as high as 97.9%. The tiered diagnosis and treatment system, by implementing a care model featuring initial consultations at primary care facilities, two-way referrals, triage based on acute versus chronic conditions, and coordinated care across different levels of institutions, effectively decentralizes high-quality medical resources. Consequently, patient visit rates and testing demands at secondary hospitals and primary care institutions will be significantly unleashed.

As the tiered diagnosis and treatment system is gradually implemented, patient volume is shifting downward, leading to an increase in laboratory samples at primary healthcare institutions. Limited budgetary resources and insufficient staffing have become key constraints on the patient reception capacity of these institutions at this stage. Independent Clinical Laboratories (ICLs) can effectively address issues related to cost control and specialization of diagnosis and treatment at the grassroots level, playing a role in reducing costs and improving efficiency, thereby facilitating the advancement of the tiered diagnosis and treatment system.

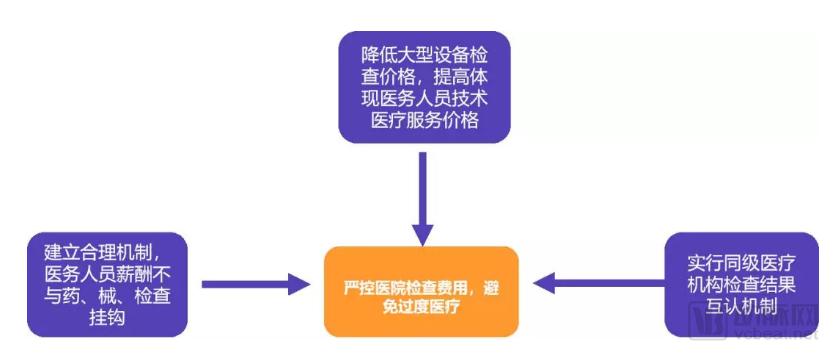

Health Insurance Cost Containment Boosts Public Hospitals’ Willingness to Outsource Diagnostic Tests: In recent years, in order to curb the unreasonable growth of medical expenses, regulatory authorities have repeatedly introduced policies to reduce fees for hospital diagnostic tests. These measures aim to prevent a shift from “funding healthcare through drug sales” to “subsidizing healthcare through diagnostic testing,” and to avoid excessive medical practices such as unnecessary extensive testing.

Source: Public information, Jingzhun Research Institute

Given the high costs of medical testing equipment and personnel, regulatory mandates to lower test prices have reduced laboratory profit margins. Consequently, hospitals are incentivized to outsource testing to independent clinical laboratories with cost advantages, thereby achieving reasonable operational savings while ensuring test quality.

1. Third-party medical testing is in its early stages of development, with in-house laboratory testing still dominating the landscape

In 2010, the market size of China's independent clinical laboratories (ICL) was only RMB 1.2 billion, reaching RMB 12.5 billion in 2017, with a compound annual growth rate exceeding 30%, indicating extremely rapid development. In 2016, the national revenue from medical laboratory services in public hospitals was approximately RMB 250 billion, with ICL accounting for less than 5%.

Source: Announcements of Listed Companies, Jingzhun Research Institute

Uneven Distribution of Medical Resources in China and Low Motivation for Test Outsourcing in Tertiary Hospitals: In developed countries and regions, healthcare systems and resources are relatively mature, with a higher proportion of community hospitals and private clinics, thereby driving the development of the Independent Clinical Laboratory (ICL) industry. Currently, the uneven distribution of medical resources in China is quite pronounced, with high-quality medical resources and testing samples primarily concentrated in tertiary hospitals. As these hospitals possess advanced equipment and professional testing processes, their motivation to outsource laboratory tests remains weak. Medical institutions in prefecture-level cities and counties will become the key customer base for ICLs to increase their market penetration.

Source: Public information, Jingzhun Research Institute

Benchmarking Against Developed Nations, China’s ICL Industry Has Significant Growth Potential: The number of test items offered by independent clinical laboratories (ICLs) in China is far lower than that in developed countries. Large-scale ICLs in developed nations such as the United States and Japan offer more than 4,000 test items, whereas large-scale ICLs in China currently offer approximately 2,000. Overall, China’s ICL market has substantial room for growth compared to developed countries in terms of revenue, penetration rate, and the number of available test items.

2. The ICL industry is experiencing rapid development, with a swift increase in the number of institutions, forming a “4+X” market structure.

In recent years, China’s independent clinical laboratory (ICL) market has experienced rapid growth, with the number of testing institutions rising from 89 in 2010 to nearly 1,300 in 2018. The increase in the past two years has been particularly notable, with the number of newly added testing institutions exceeding the total accumulated over the previous 16 years. Many companies leveraging new technologies such as molecular diagnostics have commonly established ICLs to promote their brands prior to obtaining product approvals.

Source: National Health Commission, Jingzhun Research Institute

Due to the relatively high barriers to entry and significant economies of scale in the independent clinical laboratory (ICL) industry, China’s ICL market has formed a “4+X” competitive landscape. KingMed Diagnostics, Dian Diagnostics, Adicon, and Da An Gene collectively hold a 70% market share, with KingMed Diagnostics accounting for over 30%. In 2017, KingMed Diagnostics reported RMB 3.59 billion in revenue from third-party medical diagnostic services.

Source: Announcements of listed companies, Jingzhun Research Institute

3. The ICL industry features a diverse range of participants

In recent years, the domestic independent clinical laboratory (ICL) industry in China has seen a diversification of participants. Beyond the traditional four major leaders, various companies have accelerated their industry expansion by leveraging their own resources or channel advantages. These include manufacturers of in vitro diagnostic (IVD) reagents and instruments, providers of new technology services such as gene sequencing, IVD distributors, and pharmaceutical companies.

IVD Product Companies: Leveraging their pricing advantages, manufacturers are entering the ICL market. Currently, A-share listed in vitro diagnostic (IVD) companies such as Autobio Diagnostics, Hybribio, and Medcon Bio have begun to establish a presence in the third-party clinical laboratory business. Among them, Medcon Bio has achieved notable success. According to the company’s announcements, by the first half of 2018, it had established nearly 40 regional shared testing centers. These centers generated RMB 233 million in diagnostic service revenue during the first half of 2018, representing a year-on-year increase of 163.56%.

New Technology Service Providers: Benefiting from the continuous rise in demand for clinical laboratory testing and the widespread adoption of gene sequencing technology in clinical applications, new technology service providers operate third-party clinical laboratory businesses prior to product approval. This strategy enhances brand visibility, facilitates the acquisition of clinical data, and strengthens corporate capabilities.

IVD Product Distributors: Leveraging their channel advantages accumulated over many years, product distributors have expanded into the third-party clinical laboratory business. For example, in 2017, Runda Medical jointly established Zhongke Runda, an independent third-party medical laboratory, with the Shanghai Advanced Research Institute of the Chinese Academy of Sciences and Giant Star Medical Holdings Co., Ltd. Furthermore, Zhongke Runda collaborated with Roche Diagnostics to establish three Roche Demonstration Laboratories, creating internationally leading, high-quality, and highly automated medical testing laboratories.

Pharmaceutical Company: In early 2018, WuXi AppTec Group and Mayo Clinic jointly established WuXi NextCODE Diagnostics (WuXi Aoce). While focusing on high-end specialized tests in in vitro diagnostics (IVD), the company has built an IVD service platform, introduced more than 3,000 test items from Mayo Clinic, and continuously expanded its strategic presence in the field of precision medicine.

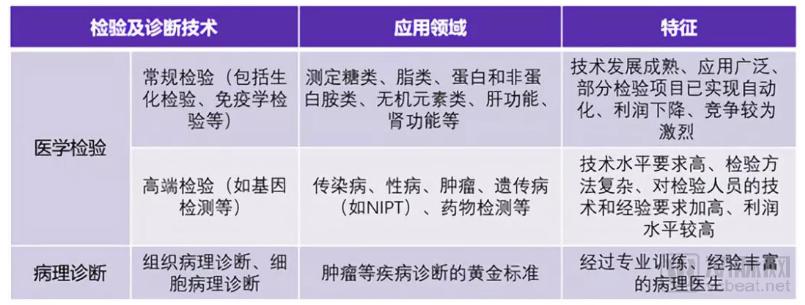

Based on the frequency and scope of clinical application, laboratory testing technologies can be categorized into two types: routine testing and advanced testing. Routine testing is widely applied across various healthcare settings, ranging from large tertiary hospitals to primary care institutions. In contrast, advanced testing places greater emphasis on personalized design, often requiring the integration of multiple testing methodologies. This imposes stringent requirements on testing equipment, reagents, as well as the expertise and operational proficiency of laboratory personnel. In the mature U.S. market for medical laboratory technology, competition in routine testing segments has become intense; consequently, the growth of advanced testing services has emerged as one of the key drivers propelling the development of the mature medical laboratory market.

Source: Public information, Jingzhun Research Institute

1. Medical testing laboratory services have a certain service radius: From the perspective of the inherent characteristics of the third-party medical testing industry, orders for routine test items are typically characterized by dispersed customers, large volumes, small individual transaction amounts, and high frequency. Due to the different testing technologies employed for various test items, some specimens have specific time limits for storage. For routine tests, such as immunoglobulin assays, test reports must be issued within one day. Sample collection for such items must be completed in a timely manner; therefore, this industry has a certain service radius. Long-distance service not only fails to meet testing requirements but also incurs unnecessary costs.

2. Continuous enrichment of testing technologies and increasing diversification of test items: Test items are trending toward personalization and molecular development, with growing diversity in test types. Industry competition is driving medical laboratory institutions to continuously improve their testing capabilities and expand the range of test offerings to meet customers’ personalized needs. Compared with developed countries, Europe and the United States offer up to 5,000 different tests, whereas leading domestic companies such as KingMed Diagnostics and Dian Diagnostics provide approximately 2,500, indicating a significant gap relative to international advanced standards. In China, biochemical and immunological test items remain underdeveloped, resulting in relatively limited profit margins.

3. High Capital Investment and Demand for Specialized Talent: The medical laboratory industry is a typical technology- and capital-intensive sector. Laboratory institutions require substantial investment in experimental equipment to facilitate advancements in testing technologies, as well as the recruitment of laboratory professionals with extensive operational expertise and practical experience. In the field of pathological diagnosis, the requirements for talent are particularly stringent, as it necessitates licensed pathologists with rich clinical experience to perform subjective assessments based on specimen sections and issue pathological diagnostic reports.

Based on the aforementioned characteristics, the primary development directions for third-party medical laboratory service providers will be a focus on chain operations and investment in research and development. By leveraging economies of scale to enhance resource utilization efficiency and pursuing specialized operations to advance testing capabilities, these institutions can secure a competitive advantage.

1. Capital Shapes the Industry’s Competitive Landscape: In terms of industry structure, the “4+X” competitive pattern will persist. Small and medium-sized third-party laboratories that have yet to achieve economies of scale are facing increasing difficulties in competition. Capital has become a key factor influencing the industry’s competitive landscape, with healthcare giants leveraging their brand and financial advantages to overtake competitors rapidly.

2. Accelerated M&A Activity: Mergers and acquisitions among independent clinical laboratories are accelerating. Drawing on the growth trajectories of U.S. industry giants, such as Quest Diagnostics’ acquisition of SBCL to strengthen bargaining power across the upstream and downstream value chain and improve gross margins, domestic industry leaders are shifting their M&A focus toward acquiring new technology platforms or partnering with leading international product and technology companies.

3. The proportion of high-end testing services will continue to rise: Conventional immunoassay, clinical chemistry, and pathology testing are experiencing limited growth rates and declining prices. In contrast, high-end testing offers higher profit margins and will become the primary source of profits for independent clinical laboratory (ICL) companies in the future. These high-end services encompass areas such as oncology, endocrinology, genomics, hematology and coagulation, neurology, infectious diseases and immunology, and toxicology.

4. Targeted Business Development: To address the uneven distribution of resources in China, the independent clinical laboratory (ICL) industry has developed tailored business strategies to meet diverse needs. For tertiary hospitals, the focus is on specialized tests characterized by relatively low sample volumes, high costs, and longer turnaround times. By collaborating with multiple tertiary hospitals across various regions to provide high-end specialized testing services, ICLs help optimize resource allocation and reduce redundant investments. For small and medium-sized hospitals and community healthcare institutions, the emphasis is on deploying routine medical testing services to enhance overall regional laboratory capabilities, improve diagnostic accuracy, and standardize quality management. In the future, the establishment of co-built regional laboratory centers will become a key focal point of market competition.