Alibaba Health Reports Revenue and Gross Profit Doubling: RMB 1.879 Billion in Revenue and Over RMB 25 Billion GMV on Tmall Pharmacy

On the evening of November 19, Alibaba Health announced its financial results for the first half of fiscal year 2019. For the six months ended September 30, 2018, Alibaba Health reported revenue of RMB 1.879 billion, a year-on-year increase of 111.2%; gross profit of RMB 529 million, up 107.1% year on year; and an adjusted net profit of RMB 10.5 million.(Note: Alibaba Health’s fiscal year does not align with the calendar year; the reporting period for its 2019 semi-annual report was from April 1 to September 30, 2018.)

Alibaba Health promptly disclosed this information to VCBeat (WeChat ID: vcbeat). We reviewed the report and conducted an in-depth analysis, focusing primarily on the following questions: Why has Alibaba Health achieved such rapid performance growth, and what has it done right? Following this period of rapid expansion, what are its next steps, and how will it synergize with other healthcare initiatives within the Alibaba ecosystem?

“Robust growth in revenue and gross profit was primarily driven by the rapid expansion of its proprietary pharmaceutical business and pharmaceutical e-commerce platform operations,” the announcement stated. As of September 2018, Ali Health’s revenue from its proprietary pharmaceutical business reached RMB 1.6 billion, while the gross merchandise volume (GMV) of Tmall Pharmaceutical Pavilion exceeded RMB 25 billion, representing year-on-year increases of 100.2% and 50%, respectively. Revenue from consumer healthcare services grew by 125.1% year on year.

The announcement stated, “The Group’s sustained enhancement in profitability will help us continue to invest in medical big data, medical artificial intelligence, and other related fields, while increasing our investment and strategic layout in innovative businesses such as internet healthcare and smart healthcare.”

The structure of this article is as follows:

1. Proprietary business takes the lead, driving rapid performance growth;

2. Penetrate the “heartland” of healthcare by securing hospitals and pharmacies;

3. Vertical and Horizontal Integration: Alibaba May Disrupt China’s Healthcare Ecosystem.

Alibaba Health was established in January 2014, when Alibaba Group partnered with Yunfeng Capital to make a strategic investment of US$170 million (approximately RMB 1.037 billion) in the Hong Kong-listed CITIC 21st Century, acquiring a 54.3% stake in the company.

Since Alibaba’s capital injection in 2014, Alibaba Health has roughly undergone four development stages: the Capital Injection Initiation Stage, during which its business primarily focused on electronic supervision codes and e-commerce services; the Business Adjustment Stage, marked by pilot initiatives in internet hospitals, pharmaceutical O2O (Online-to-Offline), and self-operated e-commerce; the Business Stabilization Stage, in which its operational framework gradually took shape, forming four core business lines—pharmaceutical e-commerce, product traceability, smart healthcare, and health management; and the Continued Deepening Stage, where, after several years of exploration, Alibaba Health has identified its position within the industry and established stable revenue streams, subsequently focusing on deepening its industry presence and upgrading existing businesses.

A review of historical data reveals that self-operated business has been the primary driver of Alibaba Health’s performance growth. Its revenue in fiscal year 2016 was only over RMB 56 million; after launching its self-operated business, revenue rose to RMB 470 million in fiscal year 2017 and further surged to RMB 2.442 billion in fiscal year 2018, representing a nearly 50-fold increase over three years.

In addition to its self-operated business, the injection of Alibaba-affiliated pharmaceutical operations has also been a significant factor. Since Alibaba Health launched its self-operated pharmaceutical business on Tmall in September 2016, its layout in the pharmaceutical e-commerce sector has become increasingly comprehensive. In June 2017, Alibaba Health completed the acquisition of Tmall’s “Blue Hat” health food business. In early August 2018, it further acquired Tmall’s e-commerce platform operations covering categories such as medical devices and health products, adult family planning products, contact lenses, and medical and health services. Meanwhile, Alibaba Health has expanded its outsourced and value-added services for the nutritional supplements and health care category on the Tmall platform, achieving full-category coverage of the Tmall Pharmacy Hall.

In addition to its B2C pharmaceutical business, Alibaba Health is also “actively expanding into the offline pharmaceutical retail market and continuously exploring new development pathways for new retail in the pharmaceutical sector.” In May 2016, Alibaba Health took the lead in establishing the China Pharmaceutical O2O Pioneer Alliance together with 65 retail pharmacy chains. Over the past few months, Alibaba Health has collaborated with leading offline pharmacy chains within the O2O Pioneer Alliance, partnering respectively with Cainiao and Ele.me’s Hummingbird delivery service to launch 24-hour emergency medication delivery services in four cities: Beijing, Guangzhou, Shenzhen, and Hangzhou. Meanwhile, Alibaba Health has made successive strategic investments in regional leading pharmacy chains such as Shandong Shuyu Pingmin, Anhui Huaren Health, and Guizhou Yishu, promoting the integration of online and offline pharmaceutical retail channels within the operational regions of these pharmacy chains.

The performance announcement also revealed that the “Ma Shang Fang Xin” platform, serving as the infrastructure for drug traceability, continued to achieve steady growth over the past six months. The number of pharmaceutical manufacturers registered and renewing their contracts on the platform has remained stable at 80% of the total number of drug manufacturing enterprises in China, with coverage rates exceeding 95% for key products under national priority, such as vaccines. In July this year, Alibaba Health leveraged its traceability code capabilities to provide users with tools to scan codes and query batch numbers for problematic vaccines. Recently, the National Medical Products Administration (NMPA) issued the “Guiding Opinions on the Construction of an Information-based Drug Traceability System,” providing a policy foundation for further increasing the coverage rate of the “Ma Shang Fang Xin” platform.

Led by the “flagship platform” Alibaba Health, Alibaba has this year pushed its healthcare strategy deeper into the core of the medical sector. If previously Alibaba approached healthcare with an internet-business mindset, a clear shift has emerged since the beginning of this year: Alibaba is now penetrating the “heartland” of healthcare, aiming to capture the two most critical strongholds—hospitals and pharmacies.

In the hospital sector, in mid-June, Shanghai Yunxin planned to acquire a 5.05% equity stake in Winning Health through share agreement transfer, with a transaction consideration of approximately RMB 1.058 billion. Shanghai Yunxin is a wholly-owned subsidiary of Ant Financial and serves as its key platform for external investments.

Additionally, in mid-October, it was reported that Alibaba Health, Alipay, and Yuhang First People’s Hospital, after six months of system development and joint debugging, officially integrated and successfully implemented health insurance point-of-care settlement at Yuhang First People’s Hospital. During the one-and-a-half-month trial period, there were over 1,000 instances of “face-scan medical visits,” and 200 patients completed their registration at the hospital using facial recognition.

Just four days ago, Alibaba Health announced the signing of a strategic cooperation agreement with Alipay, a subsidiary of Ant Group. Under this agreement, an independent medical and healthcare services channel will be exclusively established within the Alipay app, with Alibaba Health assuming full responsibility for managing and operating the healthcare businesses and industry partnerships within this channel.

In the field of smart healthcare, Alibaba Health and Alibaba Cloud announced in September the joint development of Alibaba’s medical artificial intelligence system—ET Medical Brain 2.0. One month later, Alibaba Health and the Beijing Municipal Science & Technology Commission announced the establishment of China’s first open innovation application platform for medical AI, while also launching a third-party AI open platform dedicated to the medical AI industry.

Meanwhile, the earnings announcement revealed that Ali Health’s proprietary artificial intelligence (AI) products are being fully implemented: it has launched China’s first commercial AI product for comprehensive CT-based detection of pulmonary diseases and deployed it across partner institutions. In collaboration with the National Metabolic Disease Research Center, Ali Health has completed the development of the “Rui Ning Zhu Tang” AI-assisted decision support system for diabetes medication management and organized the “Rui Ning Zhu Tang” Artificial Intelligence Competition.

First, let us consider why Alibaba is interested in hospitals and pharmacies. The reason is quite simple: hospitals and pharmacies are core players in the healthcare sector. China’s healthcare delivery model, dominated by public hospitals, grants these institutions immense medical resources, strong patient trust, and unparalleled influence within the healthcare system. Pharmacies, with their extensive coverage across cities and rural areas, serve as the most accessible pharmaceutical service providers for the general public and represent an excellent “traffic” entry point. In the future, whether for tiered diagnosis and treatment or health management, pharmacies can play a pivotal role.

The currently surging trend of “outflow of prescriptions” offers greater potential for both hospitals and pharmacies. This phenomenon involves the decoupling of diagnosis, treatment, and medication dispensing—processes previously completed entirely within hospitals—with medication dispensing now taking place outside hospital settings. Nevertheless, the source of prescriptions remains critical; without deep integration with hospitals, securing prescription flows becomes a significant challenge. The outflow of prescriptions is primarily absorbed by pharmacies that possess strong capabilities in product portfolio management and pharmaceutical care services. These pharmacies are typically large chains or regional leaders. By partnering with these key players, Alibaba has established its capacity to capture the outflow of prescriptions.

Therefore, Alibaba Health’s strategic moves in the hospital and pharmacy sectors this year represent a brilliant maneuver that has undoubtedly penetrated the core of healthcare. This not only left competitors lingering at the hospital gates trailing behind but also put significant pressure on traditional players in the medical and pharmacy industries.

In particular, the traditional chain pharmacy business model is likely to suffer a severe blow under the impact of Alibaba Health’s new retail initiatives. Traditional pharmacies rely on customers visiting physical stores to make purchases, which then creates opportunities for secondary sales development. However, if patients complete their consultations at hospitals and have medications delivered directly to their homes through Alibaba Health’s O2O (Online-to-Offline) service, they will not visit physical stores. Without store visits, there will be no opportunities for secondary sales development, resulting in a significant loss of foot traffic and customer flow for traditional pharmacies.

Of course, traditional pharmacies can also choose to partner with Alibaba by joining the O2O Pioneer Alliance or the Ele.me Pharmaceutical Platform. This approach not only generates traffic but also positions them as pioneers in new pharmaceutical retail, staying one step ahead of their competitors. Furthermore, retail pharmacies may opt to accept equity investment from Alibaba, similar to its investments in Shuyu Pingmin, Anhui Huaren, and Guizhou Yishu. Alibaba’s equity participation is relatively “gentle,” as it does not seek absolute control nor require performance-based valuation adjustment mechanisms (VAMs). This presents an excellent opportunity for regional leaders aiming to expand their scale.

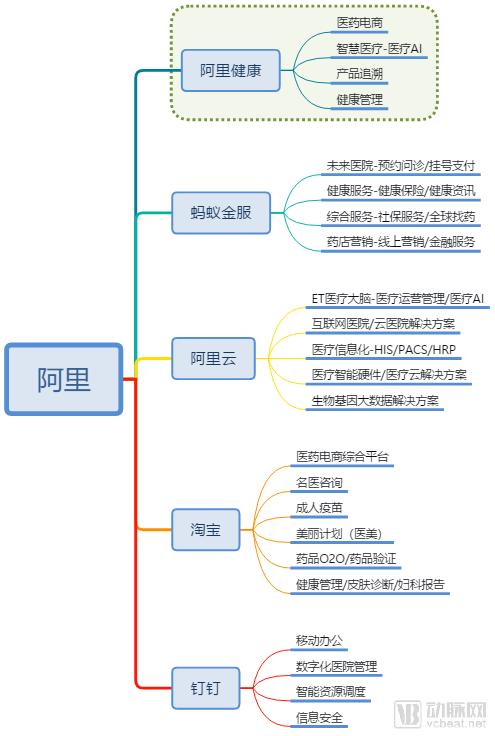

Any discussion of Alibaba Health’s development inevitably brings to light the broader layout of the Alibaba ecosystem in the healthcare sector. VCBeat’s analysis reveals that nearly all major companies within the Alibaba ecosystem have healthcare-related businesses, such as Ant Financial’s Future Hospital, health services, financial services, and insurance services; Alibaba Cloud’s healthcare informatization, cloud solutions, and bio-genetic big data solutions; Taobao’s adult vaccination programs and Beauty Plan; and DingTalk’s digital hospital initiatives.

Additionally, examples include Ele.me’s pharmaceutical O2O services, UC Browser’s health information offerings, and Youku’s health-related video business. With its extensive product portfolio and strong service penetration capabilities, the Alibaba ecosystem can comprehensively reach consumer-end users. If these resources are effectively integrated and interconnected, they will create a “super gateway” for medical and healthcare services, enabling more comprehensive and precise healthcare delivery.

One Chart to Understand Alibaba’s “Core” Medical Healthcare Layout

In addition to its proprietary businesses, Alibaba has also made extensive strategic investments in both domestic and international targets, spanning sectors such as pharmaceuticals, genomics, healthcare IT, pharmaceutical retail, consumer healthcare, insurance, physical examinations, and medical big data. Notable portfolio companies include Buonsalute (Italy), BGI Genomics, Guangzhou Baiyunshan Pharmaceutical Holdings, ZhongAn Insurance, iKang Healthcare Group, and Winning Health Technology Group.

Alibaba served as the lead investor in some of these projects and as a follow-on investor in others. Although it is difficult to determine the exact amount of Alibaba’s investments, a rough calculation based on the financing rounds of the involved companies suggests that Alibaba’s total investment in the healthcare sector may exceed RMB 3 billion.

At present, it is difficult to distill a core logic from the Alibaba ecosystem’s capital investments in the healthcare and medical sector. Most investment decisions are driven by strategic considerations, with coverage across a diverse range of subsectors. As Alibaba’s healthcare strategy takes shape, high-quality assets can be integrated into its healthcare portfolio, enabling a comprehensive, end-to-end layout spanning the entire healthcare value chain. For instance, iKang Guobin’s health examination services could be incorporated into “Alibaba Clinic,” while Winning Health’s capabilities and resources in healthcare informatics could generate synergies with initiatives such as “Future Hospital” and medical payment services.

The most pressing priority now is to bring order to Alibaba’s sprawling and complex healthcare initiatives, while also identifying a “helmsman” to steer them. This is crucial for Alibaba’s healthcare strategy. Only with a clear, comprehensive, and well-planned logical structure and framework can the critical bottlenecks be resolved, enabling resources to be utilized effectively and appropriately. While having abundant resources is certainly an advantage, an excess of resources can sometimes become an obstacle to progress.

Business operations can be categorized according to the broad framework of “healthcare services, pharmaceuticals, and insurance.” Meanwhile, product lines such as health informatics and artificial intelligence inevitably serve a complementary role. The top priority is to clearly understand the core needs of Tier-3 Grade-A hospitals. Whether it involves point-of-care payment solutions or electronic medical records (EMR), development should be driven by the actual demands of hospitals. The strategy should focus first on penetrating the market with initial products, followed by subsequent enhancements and upgrades. Next, patient needs must be addressed; these represent the “pain points” that internet companies are most keen to analyze and will inevitably serve as key references for product development and marketing promotion.

Of course, among Alibaba’s healthcare initiatives, Alibaba Health undoubtedly holds the greatest potential and is best positioned to integrate the group’s overall healthcare strategy. As evident from Alibaba Health’s performance announcements, the company has established pharmaceutical e-commerce and new retail, internet-based healthcare, smart healthcare, and consumer healthcare as its core business lines. It is forging close collaborations with partners such as medical institutions, pharmaceutical manufacturers, drug retailers, and third-party service providers to build an upstream-downstream industry ecosystem centered on “Internet + Healthcare.” By continuously strengthening cooperation both within and outside the Alibaba ecosystem, Alibaba Health has steadily solidified its position as the flagship healthcare platform within Alibaba Group.

Through strategic alliances and vertical integration, Alibaba may reshape the ecosystem of China’s healthcare industry, just as it did in the e-commerce and retail sectors.