Official Announcement of '4+7' Volume-Based Drug Procurement Marks a New Era in China's Pharmaceutical Market

Editor’s Note: This article is republished from Pharmaceutical Cloud Studio (WeChat Official Account: drugist), authored by Yunzhong Lu. VCBeat has been authorized to repost it.

The long-awaited announcement on the “4+7” volume-based drug procurement was finally released today, with 11 cities joining forces to conduct volume-based procurement for 31 drugs. This marks the first major exercise of the consolidated purchasing power by the National Healthcare Security Administration since its establishment, and represents the largest-scale cross-regional joint procurement in the history of domestic drug tendering. (What about the Sanming Alliance? Was it truly implemented?)

These 11 cities include the four municipalities directly under the Central Government—Beijing, Shanghai, Tianjin, and Chongqing—as well as seven sub-provincial or cities with independent planning status: Shenyang, Dalian, Guangzhou, Shenzhen, Xiamen, Chengdu, and Xi’an. Located in the central urban areas of China’s Bohai Rim, southeastern coastal region, Northeast, and Northwest, these cities essentially cover the most economically developed regions with the densest and highest-quality medical resources, making them highly representative.

According to analysts, the market capacity of these 11 cities is estimated to account for approximately 24.8% of the domestic market for relevant pharmaceuticals. Based on a rough estimate of sales volumes for 31 drug varieties, this figure represents nearly 10% of the national market share (based on data from Menet, the Ministry of Commerce’s 2017 data, and sales statistics for the 31 varieties).

The 31 varieties are as follows:

The Medicine Cloud Studio conducted a comparative analysis and found that two items had been removed from the previously circulated list of 33 products. These two products are: Cefazolin Sodium/Sodium Chloride Injection and Paclitaxel Injection (Albumin-Bound).

A joint procurement office, composed of representatives delegated from the pilot regions for volume-based procurement, was established as the operational body to conduct centralized procurement on behalf of public medical institutions in these pilot areas. The Shanghai Medical Pharmaceutical Centralized Bidding and Procurement Management Office is responsible for daily operations and specific implementation.

Scope of Procurement: Three Main Categories; Procurement Cycle: 12 Months

1. Originator Drugs and Reference Listed Drugs

2. Generic drugs that have passed the consistency evaluation

3. Generic drugs approved under the new registration classification for chemical drugs

Regarding the widely concerned issue of whether volume commitments are included, the volumes have already been listed in the table. Additionally, please note:

1. The agreed procurement volume for drugs in this centralized bulk procurement is determined based on submissions from each pilot region.

2. All pilot regions shall uniformly implement the results of centralized procurement. During the implementation period of the centralized procurement results, medical institutions must prioritize the use of selected products from the centralized procurement and ensure the completion of the agreed procurement volume.

3. Medical institutions in each pilot region shall, on the basis of giving priority to the use of selected varieties from centralized procurement,The remaining dosage may be procured in appropriate quantities from non-selected drugs of the same therapeutic class with reasonable prices, in accordance with the relevant regulations on centralized drug procurement management in the respective region.

The announcement did not specify the detailed procurement rules. According to previous disclosures by informed sources, for varieties with three or more manufacturers under the same generic name, procurement will be conducted through competitive bidding, with the lowest bidder winning; this approach is equivalent to the previous “double-envelope” procurement system, with an estimated price reduction of 40%. For varieties with two manufacturers, procurement will proceed through price negotiation, but it is reported that companies must proactively offer price cuts exceeding the average reduction rate, with an estimated price decrease of 20%. For varieties with only one manufacturer, procurement will be carried out through direct negotiation, with an estimated price reduction of 10%.

In the current industry landscape, it is not surprising that prices of some originator drugs have experienced cliff-like declines, effectively serving as sacrificial offerings for healthcare reform. Meanwhile, it seems difficult for generic drugs to gain an advantage under these new rules. Moreover, certain products, such as Salubris’s Taijia (clopidogrel), have actually achieved market shares nearly on par with the originator drug Plavix, while Chia Tai Tianqing’s Runzhong has long surpassed the originator in market share. These products have essentially suffered silent losses in the face of the volume-based procurement game.

Expired patented drugs and medications that have passed the consistency evaluation will weigh the pros and cons, either entering into a price war destined for significant declines or abandoning the market to retain their share in non-volume-based procurement channels, which may account for only 30%. Consequently, intense competition ensues between generic and originator drugs, among different generic drugs, and between generics and products that have failed the consistency evaluation. These players engage in strategic gaming based on their existing market shares, price floors, and future expectations.

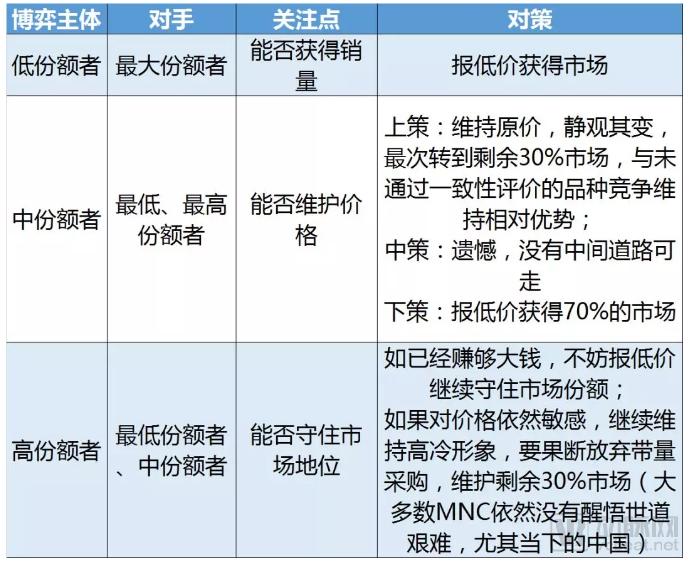

In the existing market, the larger the installed base, the more apprehensive players become about potential losses; it seems unlikely that they can simultaneously maintain prices and defend market share. In contrast, products with the smallest installed base currently enjoy a favorable position akin to “those with bare feet having nothing to lose against those wearing shoes.” Who says the pharmaceutical market only rewards first-mover advantage? Under the current volume-based procurement regime, particularly with rules committing to single-source supply, latecomers are essentially empowered: the disadvantage of being a late entrant is instantly transformed into an advantage.

If we conduct a countermeasure analysis from the single dimension of existing stock size, the cloud has also established the following game theory model:

A Brief Analysis of Game Strategies and Countermeasures

Of course, for multiple parties engaged in a game under complex rules, it is unlikely that decision-making models can be evaluated solely from the dimension of existing stock. Factors such as the corporate strategy behind the product, the current market life cycle of the product, and the intensity of competition may all alter the aforementioned single-dimensional model.

Furthermore, the rules of the recent volume-based procurement across 11 cities have once again validated the “market access + procurement + sales” integrated marketing trend proposed by Pharma Cloud Studio in 2015. The sales function is gradually diminishing, with the contribution of sales teams to sales volume declining year by year. This trend is even more pronounced for products that forfeit the volume-based procurement market. In the future, layoffs, role reassignments, and transformations within sales teams are inevitable.