Investor Insights on 2019 Trends in China's Healthcare Industry

Editor’s Note: This article is reprinted from 36Kr Jingzhun Insights, authored by Liu Jiaying, Jiang Juntao, Xu Chen, and Hu Xing. VCBeat has republished it with authorization.

Looking back at 2018, the establishment of the National Healthcare Security Administration, the National Health Commission, and the National Medical Products Administration marked the beginning of healthcare reform in China. The listings of Ping An Good Doctor and Innovent Biologics on the Hong Kong Stock Exchange, Mindray Medical’s listing on the A-share market, and Blue Sail Medical’s RMB 1.9 billion acquisition of Biosensors International collectively pushed total investment and financing in the healthcare industry to new heights. As a typical counter-cyclical sector, the healthcare industry is expected to remain one of the most watched investment areas during the “capital winter” in 2019. Which sub-sectors will continue to be at the forefront of investment trends? What industry development trends deserve attention?

The author visited multiple investment institutions and investment banking partners, including China Renaissance Capital and Daotong Investment, to analyze the trends and investment opportunities in the healthcare industry in 2019. Selected highlights are presented below:

Q: The healthcare industry is receiving increasing attention. How should we understand the development trajectory of the healthcare sector in recent years?

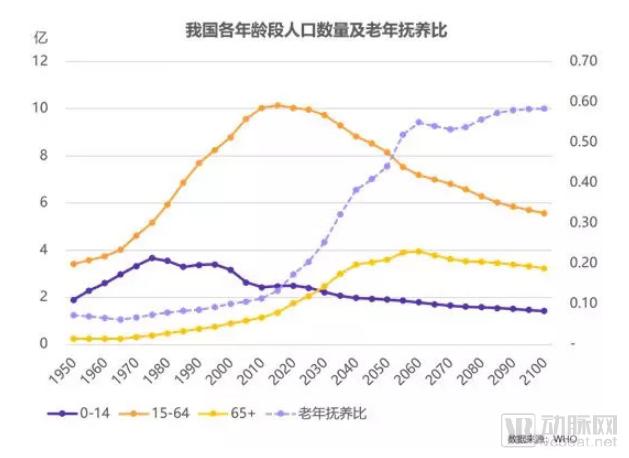

Li Gang, Partner at China Renaissance Capital:Technology is a key driver in the healthcare industry. For instance, the scientific community’s deepening understanding of cancer has enabled the development of many novel cancer therapies and treatment modalities. Another important context is that healthcare is profoundly influenced by policy, economic, and social environments. Examining the development of the healthcare industry in recent years, it can be broadly summarized along three dimensions: consumption upgrading, medical insurance, and population aging. These three dimensions help explain the overarching logic behind the industry’s growth.

The first dimension is consumption upgrading. It is evident that after years of sustained high-speed growth, China’s economy has seen a significant rise in public consumption levels, with people increasingly seeking better medical experiences and treatment outcomes. Against this backdrop, new concepts and business models have emerged, such as private chain clinics and precision medicine. The second dimension is healthcare cost containment. Amid continuously rising medical costs and expenditures, improving the efficiency of fund utilization and achieving optimal resource allocation are challenges faced by most countries worldwide. In China, this is specifically reflected in healthcare reform policies such as the consistency evaluation of generic drugs and the re-evaluation of the efficacy and safety of traditional Chinese medicine proprietary products. The third dimension is population aging, which has led to shifts in the disease spectrum and increased demand for rehabilitation and nursing care.

Q: Since the second half of 2018, there has been ongoing debate about a “capital winter.” Will the development of the healthcare industry be affected by this?

Sun Qi, Partner at Daotong Investment:Currently, market participants are slowing down and adopting a wait-and-see approach, but the market cannot remain in a deep freeze indefinitely. We have repeatedly emphasized the importance of capturing relative certainty amidst high market uncertainty. From this perspective, healthcare services represent a relatively stable segment within the broader healthcare industry, characterized by healthy cash flows and lower reliance on external financing. Should the market gradually recover in 2019, capital is likely to flow into the healthcare services sector first. While innovative technologies such as AI are viewed favorably, their development remains subject to multiple factors, including national policies.

Q: In the healthcare services sector, which niche segments are worth watching?

Wang Bin, Executive Director at China Renaissance Capital:Let us first examine how medical services are categorized. Medical services can be broadly divided into general hospitals, specialized chain institutions, and B2C or B2B services. Over the past five years, comprehensive private healthcare groups have accumulated substantial medical assets through mergers and acquisitions and by participating in the restructuring of state-owned enterprise hospitals. Meanwhile, certain specialized services, which operate as self-contained systems and are more easily spun off from public hospitals, have gradually evolved into specialized medical chain institutions in the market. B2C or B2B services, on the other hand, require close collaboration with hospitals and physicians.

Specialized medical institutions can be further categorized into those with a clinical focus and those with a consumer-oriented focus. Clinically focused institutions primarily address disease-related needs, such as in neurology, cardiology, and orthopedics; these facilities require advanced medical equipment and technical expertise, as well as coverage under public health insurance schemes. In contrast, consumer-oriented institutions mainly cater to non-disease-related needs, typically paid for through commercial insurance or out-of-pocket, with brand reputation serving as their core competitive advantage.

Moreover, in the development of consumer-oriented specialized medical chains, high-quality physician resources and single-store operational capabilities are also critical factors. For instance, Arrail Dental, our long-term partner, has grown since 1999 to operate over 100 clinics across China. Nearly each individual clinic achieves rapid standardized expansion, while physician resource challenges are addressed through its proprietary supply system. Currently, Arrail Dental has established itself as a professional brand in the premium dental care sector.

As a boutique investment bank focused on the new economy, if asked which niche sectors we are watching next, we believe that obstetrics and gynecology, pediatrics, and dentistry will remain highly attractive. With the gradual relaxation of birth policy restrictions and the significant shortcomings of public hospitals in pediatric care, the pediatric sector is expected to attract more social capital in the future. However, innovation in business models is needed in these fields to align market demand with users’ ability to pay.

Dentistry, medical aesthetics, and rehabilitation are significantly influenced by the trend of consumption upgrading. China has moved beyond the development stage of merely satisfying basic needs for food and clothing, and people’s health demands are continuously escalating. How to differentiate medical services is a key consideration for the government, enterprises, and investors. For instance, the average per capita expenditure on dental treatment in China is approximately RMB 300, compared to USD 2,400 in the United States. This disparity highlights the substantial growth potential for consumer-oriented medical specialties driven by consumption upgrading.

Q: The sectors of women’s and children’s health, dentistry, and medical aesthetics have remained hot for the past two to three years. What new opportunities will emerge in 2019?

Wang Bin, Executive Director of China Renaissance:Indeed, competition in the consumer-oriented segment of medical services has intensified into a "red ocean," with players increasingly competing on brand building, channel control, and differentiation. For instance, in first-tier cities like Beijing, one may encounter a dental clinic every twenty minutes or so. However, the density of dental clinics remains insufficient in the vast second-, third-, and fourth-tier cities, presenting significant growth opportunities. Institutions that focus on differentiated services or positioning—such as pediatric dentistry, dental implants, or orthodontics—are well-positioned to stand out.

Q: Innovative drugs are one of the most prominent investment hotspots in China’s pharmaceutical sector and the broader healthcare industry, yet homogenization remains a significant challenge. How should we view the prospects for new drug development in China?

Zhang Xiao, Vice President of China Renaissance Capital:Domestic innovative drugs are on the rise, with opportunities and risks coexisting.

On the one hand, the National Medical Products Administration has introduced a series of policies and reform measures that benefit industry development. Industry professionals with overseas study or work experience are increasingly returning to China to start businesses. Meanwhile, domestic sectors such as Contract Research Organizations (CROs) and Contract Manufacturing Organizations (CMOs) have matured over years of development, and the industrial environment has become increasingly robust, all of which favor the growth of China’s innovative drug industry. On the other hand, compared with developed countries such as the United States, Chinese enterprises still have relatively weak independent R&D capabilities, need to accumulate more experience in industrialization, and face significant gaps in payment systems. Therefore, there is still a long way to go before catching up with developed nations.

Regarding the second issue, domestic innovative drug companies are relatively diverse; however, homogeneous competition exists in areas such as biosimilars and “me-too” or “me-better” products targeting popular therapeutic targets. For instance, biosimilars and innovative drugs targeting PD-1/PD-L1 may face intense market competition due to homogeneity, resulting in significant pricing pressure. Coupled with high production costs and insufficient large-scale manufacturing capacity in China, the profitability of these companies’ products is likely to be adversely affected in the future.

Zhang Yuan, Investment Director of Biopharmaceuticals at Guozhong Venture Capital: Domestic innovative drug development primarily follows international trends. For instance, when a specific target has already entered Phase II or III clinical trials abroad, Chinese companies either initiate their own development or directly acquire the patent rights for the China region. Homogenization is indeed a prominent characteristic of current innovative drug R&D in China. When therapeutic efficacies are comparable, R&D speed, manufacturing processes, and production capacity become critical factors. Currently, the majority of the global pharmaceutical market is still concentrated in developed countries in Europe and the United States, where commercial health insurance systems are relatively mature. In contrast, China’s payment capacity is unlikely to improve significantly in the short term.

Q: What are the current hot areas in new drug development? Will there be any changes in the next year? Apart from innovative drugs, what investment opportunities exist for generic drugs?

Zhang Xiao, Vice President of China RenaissanceInnovative biologics that address unmet clinical needs remain a focal point of R&D; emerging technologies such as CAR-T, TCR-T, and gene editing are also garnering significant attention. Increasing focus is being placed on targets, technology platforms, or product categories with a global perspective, as well as therapeutic areas beyond oncology, including autoimmune diseases, central nervous system disorders, and rare diseases.

Zhang Yuan, Investment Director of Biopharmaceuticals at Guozhong Venture Capital: Beyond innovative drugs, generic drugs also present opportunities. However, the key lies in identifying the reference product, assessing the feasibility of achieving first-to-file generic status, and evaluating the complexity of replication. Although the molecular structure of a drug becomes readily accessible after its patent expires, its formulation and manufacturing processes remain proprietary. Consequently, generics that are challenging to develop—such as those for complex respiratory diseases or psychiatric disorders—offer substantial market potential.

Q: Apart from CAR-T therapy and PD-1/L1 inhibitors, what other novel therapies or targets in the field of immunotherapy are worth attention?

Sun Lei, Partner at Mifang Capital:Tumor immunotherapy is a broad concept. Simply put, it encompasses any approach that directly or indirectly leverages the immune system to treat cancer, including immune cell therapies (such as T-cell, NK cell, and macrophage therapies), antibodies (monoclonal, bispecific, and multispecific antibodies), cytokine-based recombinant proteins (interleukins and chemokines), oncolytic viruses (viruses with oncolytic effects), and therapeutic vaccines (conventional vaccines and neoantigen-based vaccines).

Specifically in the antibody field, taking immune checkpoint-related targets as an example, besides PD-1, other targets such as TIM3, LAG-3, VISTA, and CD80, as well as bispecific antibodies based on immune checkpoint targets combined with other targets, are all worthy of attention. In the field of immune cell therapy, current products represented by CAR-T for hematologic malignancies and TCR-T for solid tumors focus on breakthroughs in cost, industrialization, and therapeutic efficacy. Whether non-mainstream products such as CAR-NK and CAR-M can secure a place in the anti-tumor sector also remains noteworthy.

From a mechanistic perspective, the combination of oncolytic viruses (such as T-VEC) and PD-1 inhibitors can enhance the response rate to PD-1 therapy in cancer patients. This potential synergistic effect has prompted multinational pharmaceutical companies to actively invest in this area. Traditional therapeutic cancer vaccines have demonstrated poor efficacy, which is currently attributed primarily to issues in target selection. The focus is shifting from tumor-associated antigens to tumor-specific antigens, with neoantigens being a prime example. We are optimistic about the neoantigen approach; however, whether it will deliver remarkable clinical benefits largely depends on the design of clinical trials.

Q: In recent years, China’s medical device industry has experienced rapid growth, with a growth rate exceeding the international average. Except for a few niche segments such as biochemical diagnostics and coronary stents, where domestic products have achieved import substitution, most sectors remain reliant on imports. What are the key areas of interest and long-term development directions worthy of attention in this industry going forward?

Sun Qi, Partner at DaoTong Investment:We continue to focus on domestic substitution, as Chinese companies achieve ongoing breakthroughs in products and core technologies. Leveraging policy incentives, their market share is expected to rise steadily. We also prioritize technological innovation, making forward-looking strategic arrangements for long-term development, with the goal of becoming a global leader in innovative medical devices through independent R&D.

Q: In the medical device sector, high-tech fields such as molecular diagnostics are developing rapidly, with gene testing technology in particular driving industry transformation. What is the current overall stage of development for gene testing in China? Which niche application areas hold significant commercial value?

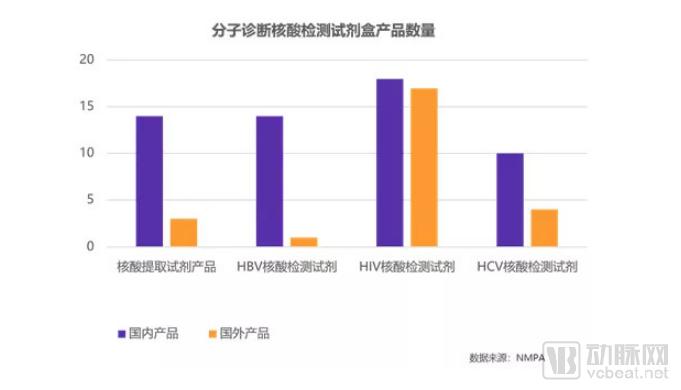

Chen Huawei, Partner at Oriental Fortune Capital:In the field of molecular diagnostics, the clinical application of genetic testing in hospitals remains at a relatively early stage of development, with a shortage of clinical testing equipment and qualified professionals. However, as a critical diagnostic modality for tumor targeted therapy, genetic testing has been incorporated into medication guidelines. Companies leveraging genetic testing as their technological platform warrant close attention. In the future, with advancements in genetic testing technologies and the continuous reduction in testing costs, its level of clinical application is expected to increase further.

Upstream in the industry chain, reagent and equipment manufacturing are currently the focal points of investment. However, at this stage, the maturity of domestic technologies still lags behind international leading standards, with few high-quality investment targets available in the equipment sector. Molecular diagnostic reagents, due to their controllable production costs, represent the primary profit center for the industry at present.

It is worth noting that as the industry matures, products directly targeting patients will constitute a larger market. Furthermore, technology is a key factor driving industry development. Currently, there is a significant number of Chinese professionals engaged in the global molecular diagnostics sector. Coupled with policy support and the increasing maturity of clinical applications, China’s molecular diagnostics industry holds substantial potential for future growth.

Q: Currently, many bioinformatics analysis companies that integrate big data and artificial intelligence technologies have emerged in the downstream sector of genetic testing. How should we define the position of these companies in the future industry landscape?

Chen Huawei, Partner at Oriental Fortune Capital:Companies engaged in bioinformatics services currently occupy a somewhat awkward position. This is primarily because gene testing companies typically possess basic data analysis capabilities and only outsource their work to specialized data analysis firms when encountering more complex and challenging problems. Consequently, these bioinformatics companies are highly constrained by upstream clients, have a relatively small total business volume, and face limited room for revenue growth. It is unlikely that bioinformatics analysis will develop into an independent sector; instead, its future development will mainly lie in industry mergers and acquisitions and integration, becoming an important component of gene testing companies’ operations and serving as a complementary service to gene testing.

Q: After experiencing the dramatic rise and fall of the “Internet + Healthcare” boom, AI applications in healthcare have become a new hotspot. Will the 2019 surge in “AI + Healthcare” continue? Amid product homogenization, which other directions deserve attention?

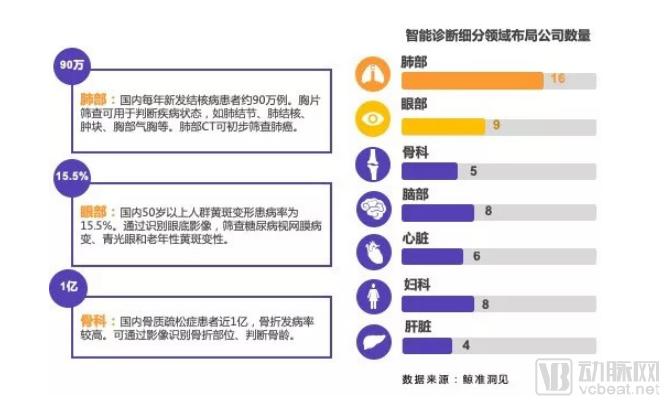

Wen Gang, Partner at Kaifeng Venture Capital:Artificial intelligence holds substantial social value, yet there is uncertainty surrounding its path to commercialization. However, compared with internet-based healthcare, the business model of “AI + Healthcare” entails less uncertainty. For instance, intelligent diagnostic products for medical imaging, which were among the earliest to be deployed, target hospitals as the primary payers, presenting a seemingly clearer business model.

However, current AI-based diagnostic imaging products show limited differentiation among competitors, with accuracy rates of leading companies differing by only a few percentage points. When product distinctiveness is low, questions arise regarding users’ willingness to pay, potentially driving down product prices. Additionally, the size of the market for AI-assisted diagnostic imaging must be considered. If AI diagnostics were to replace radiologists’ image interpretation tasks in the long term, I believe the market ceiling would equate to the total salary expenditure for radiologists. In the future, providing comprehensive treatment plans based on integrated patient data from both in-hospital and out-of-hospital settings may hold greater promise and value, but significant progress remains to be made.

Sun Qi, Partner at Daotong Investment:The application value of artificial intelligence is substantial, but the market is increasingly approaching a "red ocean" state. Therefore, it is crucial to identify market gaps. Early applications of AI in the healthcare sector were heavily concentrated in products such as pulmonary nodule screening and fundus image screening. However, as developments delve deeper, the challenges become more complex and the barriers to entry rise. For instance, the development of intelligent diagnostic products for brain imaging requires the establishment of a Chinese brain imaging database, incorporating multi-dimensional data metrics such as changes in hippocampal volume and gray-white matter thickness. From this perspective, there are early-stage opportunities in developing distinctive, vertically specialized intelligent diagnostic products.

Furthermore, platform-based companies also warrant attention. A hospital’s radiology department cannot realistically engage with dozens of different vendors to acquire various types of imaging diagnostic products; this is precisely where the value of a platform lies. If a platform can offer a comprehensive suite of imaging diagnostic products or services covering most categories, it stands to achieve a winner-takes-all outcome in the future. Given that the number of such platform companies will likely remain limited, investors should prioritize leading teams, even if valuations are high.

From a market prospect perspective, the early development of intelligent diagnostic products requires collaboration with leading hospitals and top-tier institutions to ensure access to high-quality sample data. However, large-scale monetization in the future is likely to occur within primary healthcare institutions, where there is substantial unmet market demand. Composite capabilities such as channel control and marketing will become increasingly important for companies in the AI + healthcare sector. In particular, by 2019, companies in the AI + healthcare field will need to compete on their revenue monetization capabilities.

Q: With the development of artificial intelligence technology, the scope and depth of medical big data applications have also expanded. In the field of medical big data applications, what core competencies should enterprises possess?

Wen Gang, Partner at Kaifeng Venture Capital:First, it is technically difficult to establish barriers. Second, although many companies claim to have accumulated vast amounts of data, data itself does not constitute a barrier. With state-backed entities having entered the market, the threshold for data acquisition is expected to decrease further. Therefore, relying solely on data is insufficient; service capability is the core competitiveness for companies in this sector. Healthcare is a capital- and operation-intensive industry; providing only superficial services will not generate significant commercial value nor create competitive moats. Only by truly delivering high-quality services can companies encourage users to pay, while also unlocking the value of patients’ out-of-hospital data.

Online light consultations once attracted significant attention, but the industry now has a clear perspective. Even if a company were to capture the entire national market, it would still generate limited revenue and profit by relying solely on online light consultations. Many companies have hoped to launch tools that can be mass-replicated across most hospitals and departments, creating an appearance of high production efficiency. However, given the highly personalized nature of healthcare, achieving cross-disciplinary mass replication is extremely difficult. Therefore, whether in chronic disease management, telemedicine, or unlocking the value of medical data, companies must deeply understand user needs and provide specialized, in-depth services.

Sun Qi, Partner at DaoTong Investment:In the early stages of industry development, the ability to consistently acquire high-quality data at low cost is a critical competitive advantage for startups. However, as the "national team" continues to build and refine high-speed data infrastructure, data availability will no longer be a bottleneck. Moreover, the volume of accumulated data merely represents a baseline threshold; significant challenges may still arise in subsequent data cleaning and modeling. Even more difficult is the monetization of data.

We observe that companies currently capable of truly monetizing big data are able to establish a closed loop spanning data collection, processing, and application, thereby ensuring that the quality of collected data aligns with the requirements for data utilization. However, how can medical big data be monetized? From whom can value be derived? In what product forms can this monetization take place? Medical data suffers from numerous quality issues, such as missing or incomplete data, manual contamination, and inconsistent formats. These challenges pose significant obstacles to monetization.