Only 30 Million of China's 900 Million Internet Users Leverage Online Healthcare – Transformation and Opportunities Ahead in Southwest China

Since its inception, internet healthcare has attracted significant attention. After years of development, how does capital view it? What is the status of its scenario-based applications? And where lies its future direction?

Recently, the 2018 Tianfu Software Park Annual Summit and the 12th Sichuan Internet Conference were held in Chengdu under the theme “A New Healthcare Ecosystem in the Digital Age.” The forum featured discussions on policy, investment, hospitals, enterprises, and other key issues, aiming to seek answers.

In May 2017, the National Health Commission issued new regulations to strengthen oversight of internet-based medical services, causing a brief stagnation in the development of internet hospitals. It was not until April this year that the General Office of the State Council released the “Guiding Opinions on Promoting the Development of ‘Internet + Healthcare’,” which clarified market entry rules and regulatory standards, ushering China’s internet hospitals into a new phase of standardized development.

Prior to the introduction of the new policy, the majority of internet hospitals were initiated by enterprises, with only a small number established by physical hospitals. Following the implementation of the new policy, the government expects hospitals to take the lead in advancing internet healthcare. Consequently, two distinct business models may emerge in the future:

One model is the “Hospital + Internet” approach. Led by hospitals, this model introduces new internet-based operational management practices on top of existing hospital operations, including hospitals building their own internet platforms or collaborating with third parties to establish such platforms. In this scenario, physical hospitals must apply for an Internet Hospital license as a secondary clinical entity, and physicians are not required to file separate applications to practice at multiple sites on these platforms, as exemplified by West China Hospital’s Internet Clinical services. This constitutes the first category of Internet Hospitals. Although this model can improve the utilization of medical resources and enhance physicians’ practice efficiency, relying solely on isolated breakthroughs makes it difficult to reshape the overall landscape of internet healthcare.

The second model is “Internet + Hospital.” In this model, a third party applies to establish an internet hospital but must form a close partnership with a physical medical institution. This model poses challenges for effective regulatory oversight, making it difficult to handle and adjudicate medical disputes. Therefore, the physical hospital and the third-party platform need to sign an agreement; once the agreement is terminated, the internet hospital ceases to exist and cannot continue operations.

Wu Ping, National Leader of Deloitte China’s Life Sciences and Healthcare Industry, believes that under this model, the influence of healthcare institutions has been enhanced to a certain extent. However, it is expected that after rapid consolidation in this market, only a few third-party internet hospital platforms will survive and emerge as market “oligopolies.”

This could lead to two scenarios and trends: first, hospitals at all levels will independently establish internet hospitals; second, internet healthcare companies and medical platforms will compete for high-quality resources from Grade 3A hospitals.

From an investment perspective, Wang Xiaocen, a partner at the CEC Health Fund, provided the following set of data:

In 2014, when internet healthcare first emerged, the industry saw only about 110 investment projects, with a total investment amounting to approximately RMB 11.3 billion. Seventy percent of these investments were directed toward companies at the angel and Series A stages. It was not until 2015 that internet healthcare truly expanded across all business sectors.

In 2015, the internet healthcare industry experienced explosive growth, with investments in 548 projects—a total amount approximately five times higher than that of 2014. The majority of funding in 2015 was directed toward startups, with 248 companies receiving angel-round investments alone.

In 2016, investors began to favor top-tier projects. By the relative trough in 2017, most investments had already started concentrating on these leading ventures. This posed a significant challenge for entrepreneurs. Identifying innovative opportunities within new entrepreneurial models was not easy, so everyone engaged in zero-sum competition over existing market share.

Moreover, as a mature, fragmented industry with relatively high barriers to entry, the healthcare sector cannot entirely escape the influence of Moore’s Law in incremental markets. Consequently, the barriers for new projects and entrepreneurs will continue to rise. In this context, all the major shifts observed in 2018 were largely driven by favorable policy developments.

However, the penetration rate of internet healthcare in the medical sector remains low. While the number of internet users in China appears to have surpassed 800–900 million, the user base for internet healthcare applications is actually only around 30 million, with an even lower proportion of active users. This indicates substantial room for growth in the healthcare sector, which is characterized by low-frequency but essential demand.

Furthermore, the collapse of trust in search platforms has triggered a restructuring of traffic across the entire industry, fueling the rise of more vertical-specific apps—a phenomenon that essentially fragments the original traffic ecosystem. Internet hospitals offer free applications to physical hospitals for non-clinical services, aiming to capture hospital-generated traffic.

In terms of long-tail medical value, new explorations are gradually emerging. Medical informatics infrastructure continues to be upgraded, progressively covering the entire spectrum of healthcare needs—from in-hospital diagnosis and treatment to post-discharge rehabilitation and health management. Many of the systems and facilities involved in this process are built by enterprises in collaboration with hospitals.

Wang Xiaocen believes that electronic prescriptions represent a watershed moment for future internet-based medical services and are central to accessing future internet hospitals. On this basis, China Electronics Health has significantly improved its investment model.

At present, it appears that all future projects will face new challenges. The most critical factor is whether enterprises can gain recognition and support from capital markets, especially during this period of severe valuation inversion between the secondary and primary markets. Companies must accurately identify their core value propositions.

The future business models, particularly those of private enterprises, will have their operational compliance tested depending on how government regulatory measures are implemented. In terms of policy, startups can seize emerging opportunities, while growth-stage companies must pay closer attention to regulations, standards, and enforcement thresholds to avoid wasting resources.

In fact, the currently trending internet hospitals are still dominated by major players. While the capital cost of establishing an internet hospital is not high, the communication costs are substantial. A company’s scale and prior experience determine whether it can achieve a balanced negotiating position with hospitals. Although enterprises can explore various approaches to break through, the resulting opportunity costs and time commitments are unpredictable. If the exploration phase entails significant trial-and-error expenses and time-related opportunity costs, Wang Xiaocen does not particularly recommend that startups pursue this path.

Internet hospitals are not merely a digital replica of offline hospitals; they must identify their application scenarios through mobile engagement over time and across space. In the future, out-of-hospital settings extended by traditional hospitals will become a key focus area. With the opening up of internet hospital platforms, significant opportunities will emerge in chronic disease management, rehabilitation, and various health management domains.

Is Internet Healthcare a Genuine Trend or a False Fad? Wu Ping Believes It Can Be Judged from the Following Three Key Areas:

First, the overall infrastructure and facility standards of internet hospitals remain relatively low. Internet hospitals impose stringent requirements on infrastructure, including information security, data access control, real-name authentication for medical personnel, and the establishment of electronic medical record (EMR) systems. Currently, the vast majority of hospitals in China do not have EMR systems in place.

Second, on one hand, a provincial-level regulatory platform for the quality of internet-based medical services should be established; on the other hand, policy management, the healthcare system, and social security payment systems in the region must be integrated. From this perspective, it is crucial to consider both whether hospitals themselves are qualified and whether they have government support.

Third, regulatory prohibitions on initial consultations via internet hospitals have made it more difficult for patients to access care. This restriction disproportionately affects the “Internet + Hospital” model. Deloitte suggests that practitioners should forge close partnerships with commercial insurers to acquire and retain patient loyalty. From an investment perspective, the early introduction of insurance capital will also play a crucial role in future development.

Currently, healthcare IT companies are becoming increasingly proactive in the field of internet healthcare, with many industry leaders already launching initiatives in this area. This trend is driven partly by the clear requirements for infrastructure outlined in new policies, which have given healthcare IT firms a significant first-mover advantage. Additionally, these companies hold a competitive edge over other internet enterprises in securing high-quality hospital resources.

In summary, the next three years will be a critical period for the development of internet hospitals. Whether relatively successful business models can be established and whether some platforms can emerge as industry leaders are key to determining whether China’s internet healthcare sector can achieve transformation and upgrading in the coming three years.

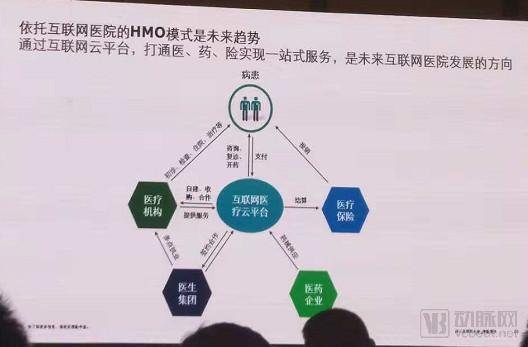

The core of an internet hospital is to enable remote diagnosis and treatment, including triage, nursing, and other consultations. In addition, its business model involves the integration of medical care, pharmaceuticals, and insurance.

The terms “standalone” and “platform” do not have absolute definitions; rather, they are primarily viewed from an operational perspective. Many hospitals, although not strictly standalone institutions, are still positioned for standalone operations. From the perspectives of capital, policy, and the overall healthcare system, a platform approach is essential to integrate resources and drive the development of internet hospitals forward. Relying solely on well-known hospital brands to build their own online presence may result in slower progress.

To address the uneven distribution of medical resources in China, online healthcare and internet hospitals represent an inevitable trend. It is essential to ensure network accessibility for patients in remote areas. Only by integrating both ends—enhancing digital infrastructure and enabling easy access for patients in these regions—can significant benefits be realized. In many remote areas, the development of network infrastructure itself remains a challenge.

Wu Ping stated that they are particularly interested in and optimistic about enterprises that have established a solid foundation within this ecosystem. Such enterprises are not standalone entities, nor do they simply transition their traditional business models into internet-based diagnosis and treatment. Instead, they are capable of effectively integrating Health Maintenance Organization (HMO) elements, including enhancing patient stickiness, introducing insurance capital, and fostering strong strategic partnerships and foundations with physician groups and medical groups. Furthermore, these enterprises demonstrate models that facilitate the integration of “medical care, pharmaceuticals, and insurance.” Even if such models are not yet fully mature, they have already taken shape or possess a robust developmental foundation.

So, what is the current state of internet hospital applications? The healthcare industry has always been patient-centered, with health administrative departments, medical service institutions, healthcare security agencies, and pharmaceutical suppliers all operating around patients, regarding them as strategic partners. However, the School of Continuing Education at Peking Union Medical College believes that the medical environment we face is changing, as are health awareness and needs. People’s demands now go beyond merely avoiding illness; they seek true health.

The accelerating pace of urbanization, shifts in lifestyle, technological transformations driven by the internet, and the continuous rise in healthcare costs constitute the fundamental backdrop for changes in the healthcare industry.

In global healthcare system reforms, informatization takes center stage. The healthcare reform proposal put forward by Obama was based on leveraging informatization to change the rules of the game in the healthcare industry. Therefore, informatization is certainly not merely a tool, but rather a system and platform. Next, it is essential to consider the payer’s perspective and adopt approaches that are acceptable to payers. Finally, the goal is to improve the quality and efficiency of care while simultaneously reducing healthcare costs.

In the healthcare industry, hygiene is a means, healthcare reform is merely a process, and health is the ultimate outcome. Wang Haitao stated that we are currently at the focal point of several contradictions, such as the efficiency and outcomes of the healthcare system, systemic performance output, per capita health expenditure, government investment in the overall health cause, and the degree of openness in the health industry.

“Internet + Smart Healthcare” is at the core of this transformation. The internet can facilitate convenient medical consultations and streamlined payment processes. Initially, we were highly cautious and restrictive toward telemedicine, even limiting its development. However, with continuous improvements in the definition and practical implementation of telemedicine, its potential for growth is immeasurable.

In addition, there are internet hospitals. What began as a mere concept has now evolved into practical, implementable solutions designed to foster industry development. This includes reforms in public hospitals: whereas pharmaceuticals previously generated revenue for hospitals through the “drug-reliance” model, they now impose costs related to pharmacy inventory and storage. Leveraging digital technologies to drive transformation presents a significant opportunity for public hospitals.

Only by integrating with insurance and establishing online medical insurance payment methods based on credit and medical record quality can efficiency be improved. Furthermore, the role of artificial intelligence in clinical decision support systems is immeasurable.

In summary, the internet is reshaping healthcare delivery models. A wide range of entities—from individual hospitals to medical alliances and medical consortia—can all be integrated with internet-based solutions. At the core of the patient, hospital, and institutional sides lies health big data. By establishing an interconnected health data platform that links data from communities, hospitals, physical examination centers, and clinics, such integration will rapidly enhance the quality of care.

Given the promising outlook and the potential for all parties to benefit, why does internet healthcare still face barriers when entering hospitals? Wang Haitai frankly stated that hospitals are currently under significant pressure. Internet medical services are consumed at market prices, incurring high costs, yet they are reimbursed or charged according to regulated medical pricing schedules. This discrepancy creates a financial burden for hospitals. Furthermore, there is a lack of adequate payment channels for health management services. Insurance companies do not yet recognize or provide coverage mechanisms for such services, while social insurance primarily covers pharmaceutical and treatment expenses, with very limited reimbursement available for health management.

In the face of industry changes, hospitals need to address core management issues with precision. On one hand, they must reduce costs; on the other, improve efficiency. Additionally, they should expand predictable revenue streams, enhance performance, and scale up expanded reproduction.

Traditional hospital information management is referred to as HIS (Hospital Information System), whereas the current standard is known as HRP (Hospital Resource Planning) system, analogous to ERP (Enterprise Resource Planning) in the corporate sector. By integrating both front-end and back-end hospital systems, augmented with big data analytics, an intelligent infrastructure essential for modern hospital management can be established.

Therefore, enterprises seeking to collaborate with hospitals must accurately identify the hospitals’ needs. If an enterprise can integrate business workflows, control flows, approval processes, and decision-making streams, the utilization rate of hospital information will increase, an intelligent management and control system can be established, and operational efficiency will naturally improve.

He believes that the core of the smart cloud platform lies in smart medical care, smart medical education, smart decision-making, and smart collaboration; however, its foundation remains the construction of a platform-based data center. Although informatization has brought convenience to patients, certain issues persist, such as disconnected service processes between online and offline channels. Community-based tiered diagnosis and treatment is also a critical component, with communities focusing primarily on chronic disease management and health management. This area will present significant opportunities for enterprises in the future.

The teaching system should also realize intelligent medical education. Since medicine is a profession of lifelong learning, with new technological advancements and new evidence-based findings emerging every day, physicians need to engage in lifelong learning.

Many practitioners have noted that we have entered an era where the human brain cannot keep pace with computers, and computers cannot keep pace with artificial intelligence. However, no matter how advanced medical technology becomes, it remains merely an auxiliary tool to assist physicians in clinical intelligent diagnosis. Artificial intelligence cannot replace the humanistic care provided by doctors. Therefore, caution must be exercised in the face of technology, integrating technological advancements with humanistic compassion.

Furthermore, it is essential to establish a patient-centered service loop. Currently, enterprises and hospitals operate at disparate points; however, if an enterprise can integrate the entire workflow into a seamless continuum, the impact would be immeasurable.

Smart healthcare should operate on a mature service system and model, starting from medical consultations, integrating medical education, and ultimately leveraging the entire Internet to drive platform operations. Healthcare is inherently complex, and the addition of information systems makes it even more so. The goal is to simplify complexity through Internet-based approaches: streamline simple tasks, standardize processes, quantify standardized procedures, digitize quantitative data, informatize digital assets, network information flows, and ultimately achieve intelligence as the final objective.

Taking Winning Health as an example, it is the first listed company in China’s healthcare IT sector. It currently ranks first in China in terms of market share for healthcare IT software and the number of healthcare service institutions served. Its core systems have been deployed in, and it provides services to, more than 6,000 hospitals.

However, Winning Health is no longer positioning itself merely as a software service provider. Through the implementation of its “Four Clouds” strategy—Cloud Medicine, Cloud Pharmacy, Cloud Wellness, and Cloud Insurance—the company aims to collaborate with partners to deliver empowered, incremental value to its clients. Winning Health integrates healthcare-related resources, including those from insurance companies, over 70,000 partnered pharmacies, and personal health examination services, into a closed-loop ecosystem that is packaged comprehensively for end users. By leveraging internet-based technologies, the company seeks to empower users, going beyond the provision of simple online consultations or isolated software functionalities.

Feng Yang, Deputy General Manager of Winning Health Internet Technology Co., Ltd., stated that numerous data points are generated through physician workstations during medical care. These data are aggregated into hospital-level data and then centralized in the hospital’s data center. Through big data processing, the data become specialized by medical discipline, enabling research analysis. Researchers leverage these data to develop AI applications, which are ultimately fed back into clinical practice. All these medical services rely on high-quality operations and maintenance (O&M). To ensure the healthy and sustainable development of the internet ecosystem, operational services are also required, with the aim of enhancing brand visibility and delivering superior services.

The most prominent feature of providing internet-based medical services is to highlight the hospital’s brand and establish its position within the entire ecosystem. When considering operations, Winning Health focuses on four core dimensions—patient needs, physician needs, hospital needs, and platform requirements—to identify the most appropriate solutions.

Taking Sir Run Run Shaw Hospital as an example, on October 12 this year, the National Health Commission held a press conference on “Internet + Healthcare” at Sir Run Run Shaw Hospital, Zhejiang University. A typical phenomenon at Sir Run Run Shaw Hospital is that before adopting our platform, the average consultation time was 4–5 hours, which has now been reduced to 1.7 hours; the average length of hospital stay has decreased by 6.17 days; and online diagnosis and treatment services along with prescription circulation services are provided.

In terms of prescription circulation, in addition to the successful implementation at Sir Run Run Shaw Hospital, Huanghai Hospital currently handles a relatively large volume of circulated prescriptions. As a Tier-2 hospital in Tianjin, Huanghai Hospital sees an outflow of more than 30 prescriptions per day.

Precision Big Data Analytics and Application: Shanghai Children's HospitalAt this hospital, patient wait times during peak hours reached 6–7 hours. By analyzing registration volumes, wait times, and departmental data, Winning Health identified Orthopedics and the Emergency Department as the two specialties with the longest wait times. By reengineering traditional processes—including registration, queuing, waiting for consultations, obtaining test and examination orders from physicians, payment, subsequent queuing, and undergoing tests—the average wait time has been reduced from 4–5 hours to 2.5 hours, demonstrating significant improvement.

In terms of AI, Winning Health has only begun extensive exploration since 2017 and has achieved notable success in bone age assessment.

Zhao Lijun, Deputy Head of the Preparatory Team for China Mobile Chengdu Industrial Research Institute, stated that the current healthcare system faces numerous challenges. There is an overall shortage of medical resources, which are also extremely unevenly distributed; the level of medical care in cities far exceeds that in rural and remote areas, as well as in second-, third-, and fourth-tier cities. Furthermore, while our medical technology is advancing rapidly, physicians’ diagnostic and treatment capabilities still require continuous training and extensive learning to keep pace with the growing complexity of diseases and the increasing variety of disease types.

The advent of 5G will bring about significant changes to the healthcare industry, as this technology possesses the following characteristics:

First, wireless telemedicine. Current wireless telemedicine relies on 4G networks, which impose limitations, restricting access to network-based medical services to fixed areas. Due to bandwidth constraints, remote physicians struggle to accurately and rapidly diagnose patients in distant locations, such as in mobile emergency care scenarios. It would be more beneficial for both patients and physicians if ambulances could transmit patients’ physiological data to doctors more quickly and effectively while en route. Additionally, high-definition video services enable physicians to visually assess patients remotely. By providing high-speed data transmission, these services facilitate the rapid transfer of large volumes of medical imaging data within information systems. This is how the high bandwidth capabilities of 5G can support the digitalization of healthcare.

Second, network slicing. Network slicing refers to dedicated networks tailored to specific service requirements, such as slices for remote surgery, remote consultation, and telemedicine education. Each slice has distinct characteristics and associated costs; therefore, selecting slices based on actual needs and service design requirements is essential to achieve optimal resource utilization.

For example, edge computing provides computational capabilities closer to the end-user, encompassing storage, computing, and analytics. Take image rendering as an example: performing it locally is undoubtedly costly, while offloading it to remote cloud servers fails to meet latency requirements. Edge computing delivers image rendering capabilities at the nearest possible location and allows sharing across multiple applications. This approach resolves the issue where each system in different hospitals must perform its own rendering. By providing unified rendering capabilities, edge computing not only reduces investment costs but also ensures quality.

Second, massive connectivity capabilities. Massive connectivity can be used for device tracking, asset management, patient management, medical waste tracking, and more. It not only supports a large volume of connections but also provides relatively accurate location data.

In the future, 5G can also be applied to more areas of Internet healthcare:

First, 5G technological upgrades can provide wireless health management solutions. Traditional medical devices are based on Wi-Fi, wired or wireless connections, or 4G networks. In the future, medical devices leveraging the higher bandwidth of 5G may emerge. For example, a company previously developed a portable ultrasound device integrated with a wireless module, enabling real-time data transmission to the cloud during ultrasound examinations. This approach offers greater convenience.

Second, build a data enablement platform tailored for the healthcare industry. This platform will facilitate more effective utilization of our 5G networks. However, as 5G is not yet a fully mature technology and has not been extensively applied abroad, this is precisely why the Chinese government places particular emphasis on 5G development, striving to synchronize its communication capabilities with global standards.

Third, cloud-based medical imaging combined with AI-assisted diagnosis represents a particularly promising application for 5G technology. He also envisions an application model that not only migrates traditional hospital services to the internet but also establishes new forms of internet hospitals.

Fourth, information is not effectively shared with patients and society. In this regard, 5G networks can play a significant role. Future edge computing capabilities and network slicing will greatly facilitate the development of hospital outreach systems.

Feng Yang believes that the Southwest region represents a second chance for the medical industry. Thanks to over a decade or two of informatization development, coastal areas have generally achieved a higher level of digital advancement than inland regions. The rise of the internet in 2018 provided a new opportunity, enabling the Southwest region to potentially catch up.

In addition, Wu Ping introduced, “Actually, Chengdu Tianfu Software Park is itself a great business incubator, with many unicorn companies and new IPO enterprises emerging. We are certainly very optimistic about it.”

Guided by the Administrative Committee of Chengdu High-Tech Industrial Development Zone, the park has gathered a large number of high-caliber professionals from across the industry. By integrating its advantageous resources, it aims to build a new platform for integrated industrial development and establish a sustainable industrial ecosystem through comprehensive, internationalized, and specialized services.

Guided by the Chengdu Hi-Tech Industrial Development Zone’s initiatives to build an “International Makers’ Paradise” and an “International Talent Hub,” and leveraging the park’s advantageous resources, Tianfu Software Park provides innovative business incubation services for entrepreneurs. Established in 2007, Tianfu Software Park’s Startup Field is a new-type incubator focused on mobile internet under the Tianfu Software Park umbrella. It stands as one of the most dynamic and significant platforms for mass entrepreneurship and innovation in China’s mobile internet sector, and serves as a leader in business incubation in Chengdu.

Chuangye Chang currently offers 35,000 square meters of incubation space, has cumulatively incubated over 1,200 projects, and is currently supporting more than 260 startup teams. It has established a multi-tiered incubation model comprising “Startup Nursery–Incubator–Accelerator–Industrial Park,” providing diverse co-working spaces such as incubation desks, shared entrepreneurial spaces, and independent offices. This ecosystem supports a comprehensive, multi-level “5C” cultivation program covering funding, talent, networks, market access, and entrepreneurial mentorship. To date, Chuangye Chang has successfully incubated a number of companies, including Medlinker, XGIMI, and Codoon.

At this conference, the Tianfu Software Park 2018 Smart Healthcare Enterprise Award and the Tianfu Software Park 2018 Most Promising Startup Award were announced. Among them, Chengdu Yiyun Technology Co., Ltd., Chengdu Shenquan Technology Co., Ltd., Chengdu Maijie Kang Technology Co., Ltd., and Borns Medical Robot Co., Ltd. received the Tianfu Software Park 2018 Smart Healthcare Enterprise Award; Fuhua Rongke (Chengdu) Technology Co., Ltd., Lianbo (Chengdu) Technology Co., Ltd., Chengdu Leke Technology Co., Ltd., Chengdu Qianke Network Technology Co., Ltd., and Chengdu Guangxiang Technology Co., Ltd. received the Tianfu Software Park 2018 Most Promising Startup Award.

However, regarding the development of internet healthcare, Feng Yang believes that enterprises must still conduct their business in accordance with policies. Currently, the state only permits the establishment of internet hospitals or the provision of online diagnosis and treatment services when relying on physical medical institutions. Consequently, many large domestic platforms face significant challenges. The regulatory stance toward internet hospitals and internet healthcare is relatively prudent, limiting permissible medical activities to specific areas: follow-up consultations for certain common and chronic diseases, which allow for prescription circulation based on such follow-ups; and family doctor contracting. At present, the scope for providing these services online is quite limited, reflecting a cautious and prudent regulatory approach.

Currently, we have merely transferred the traditional face-to-face hospital consultation model to the internet. This is still in the early stages of exploration, with the most significant development being the shift in prescription practices. This transformation represents the most critical aspect of medical practice. The opaque supply chains that previously dominated the pharmaceutical industry may be dismantled through this approach, thereby delivering substantial tangible benefits to patients.

He believes that, for industry practitioners, large companies should build extensive ecosystems and lead ecosystem development, while startups should specialize in a specific niche. If their professional, technical, or service capabilities earn the favor of major companies such as Alibaba and Tencent—demonstrating their value—they will find it easier to secure capital investment or business partnerships.