Comprehensive Analysis of the '4+7' City Pharmaceutical Volume-Based Procurement (Part I)

Editor’s Note: This article is reprinted from Zhenlipai (WeChat Official Account: zhenlipai), byAuthor: Dr.2, republished with authorization from VCBeat.

The draft minutes of the national volume-based procurement meeting released a few days ago pointed out that winning bidders will secure 60%–70% of the market in the 11 pilot cities. Although the procurement volume this time is not particularly large, these 11 pilot cities account for approximately 20%–30% of the national pharmaceutical market. If the total procurement volume is estimated based on 60%–70% of the annual total drug consumption across all public medical institutions in the future, winning bidders will directly capture 12%–21% of the national market. Among the products included in this procurement, companies that have not passed the consistency evaluation will be excluded from volume-based procurement, meaning they will directly lose most of the market in the 11 pilot cities. Therefore, to maintain their market share, most companies will inevitably engage in fierce competition for consistency evaluation under policy guidance in the future.

According to the National Drug Registration and Acceptance Database, as of November 8, the Center for Drug Evaluation (CDE) under the China Food and Drug Administration had accepted a total of 517 applications for consistency evaluation, covering 189 varieties from 196 enterprises. To date, 75 applications (covering 41 varieties) have passed the consistency evaluation.

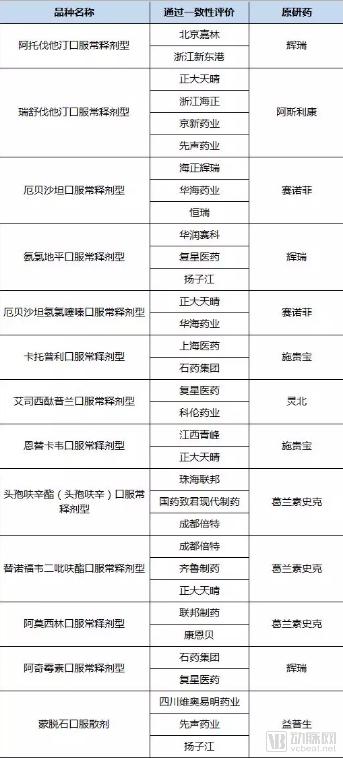

“4+7 City Drug Centralized Procurement Document” announced a procurement list involving 31 drug varieties, with 29 manufacturers of generic drugs shortlisted. Among them, 10 pharmaceutical companies had multiple varieties (two or more) shortlisted.

Huahai Pharmaceutical had the highest number of shortlisted products. Its seven shortlisted products fall within the cardiovascular and cerebrovascular system and nervous system drug categories. Meanwhile, Fosun Pharma’s four shortlisted varieties spanned four of the eight therapeutic areas covered in this volume-based procurement: cardiovascular and cerebrovascular system, nervous system drugs, systemic anti-infectives, and digestive system and metabolic drugs.

From the current perspective of the state’s top-level design, passing the consistency evaluation is merely the first step—the entry ticket—for pharmaceutical companies to access the public medical institution market. What follows is fierce market competition and brutal price wars. Manufacturers must overcome formidable obstacles and fight their way through to secure the leading position among winning bidders. Moreover, to prevent monopoly and promote competition, the validity period of the winning bid is only one year, as the state likely prefers a rotating system of winners.

Since the products have passed the consistency evaluation, their quality is theoretically guaranteed to be reliable. Therefore, there is nothing inherently wrong with implementing a procurement strategy based on the principle of “lowest bid wins.” Consequently, as more manufacturers for the same drug variety pass the consistency evaluation, the pressure to reduce prices intensifies, leading to higher-priced competitors either being eliminated or marginalized. Currently, it appears that varieties with three or more qualifying enterprises (or potentially two generic manufacturers plus the original research manufacturer) will face fierce price competition. Among the 31 drug varieties under consideration, 13 involve three or more competing products.

In other words, having more products shortlisted is not necessarily better for a company. If multiple companies compete rather than a single one holding exclusive approval through the consistency evaluation, the greater the number of shortlisted products, the larger the potential losses for the enterprise. This is because products may either win bids at low prices in exchange for volume, fail to win bids, be disqualified due to withdrawal, or even result in a complete sweep of losses.

Therefore, we note that although Chia Tai Tianqing has four products shortlisted, none are exclusive, and all face competition from more than three similar products. In particular, the immediate-release oral formulation of rosuvastatin faces competition from five manufacturers. Chia Tai Tianqing is likely to adopt targeted competitive strategies for these four products to maximize the chances of its core products winning the bids. We estimate that the sales of entecavir immediate-release oral formulations in public medical institutions reached RMB 8.425 billion in 2017, with Chia Tai Tianqing capturing half of the market share (surpassing the originator, Bristol-Myers Squibb). Given such a strong market position, the company is certain not to relinquish it easily. The market share of Chia Tai Tianqing’s irbesartan/hydrochlorothiazide tablets ranks second only to the originator product and significantly exceeds that of Huahai Pharmaceutical’s equivalent. We believe that the company is determined to win the bids for these two products. Meanwhile, sales of the immediate-release oral formulation of rosuvastatin in public medical institutions reached RMB 5 billion in 2017. The market leader for this product is the originator, AstraZeneca, while Chia Tai Tianqing and Jingxin Pharmaceutical hold comparable market shares. Having already lost the bid in the Shanghai volume-based procurement program, Jingxin Pharmaceutical, Chia Tai Tianqing, Hisun Pharmaceutical, and Simcere Pharmaceutical are poised for fierce competition in the broader national market.

Fosun Pharma also had four products shortlisted, but only its alfacalcidol oral immediate-release formulation was the exclusive product to pass the consistency evaluation. Its amlodipine oral immediate-release formulation also faces competition from four companies bidding against each other.

Therefore, products that are the sole entrants in this round face no competition from other generic drugs. If the originator drug does not significantly reduce its price, these exclusive varieties can avoid a fierce price war and are highly likely to win the bid, capturing 60%–70% of the market across the 11 pilot cities. This is because price reductions by foreign pharmaceutical companies often require approval from their global headquarters, a process characterized by low efficiency, lengthy procedures, and numerous steps, which easily leads to leakage of bottom-line prices and enables targeted pricing by exclusive generic manufacturers.

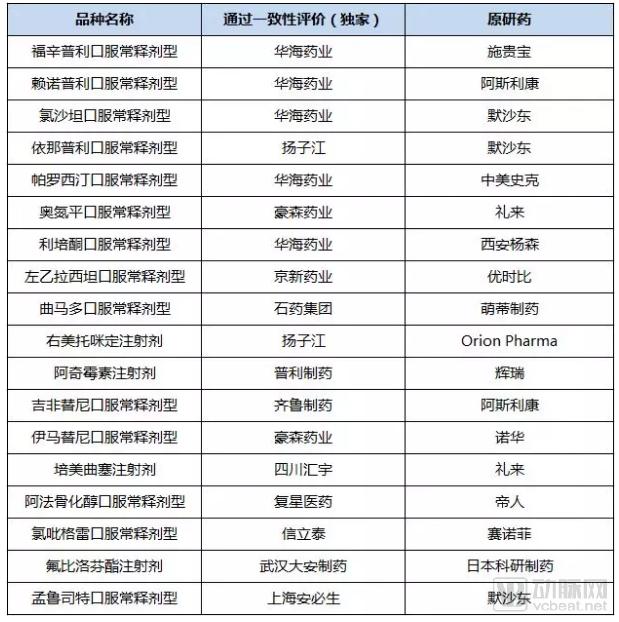

Huahai Pharmaceutical is a standout in this procurement catalog, with seven products shortlisted. Among them, five—paroxetine hydrochloride tablets, risperidone tablets, fosinopril sodium tablets, lisinopril tablets, and losartan potassium tablets—are currently the only generic versions to have passed the consistency evaluation. Historical bid-winning data indicate that, except for fosinopril sodium tablets, the prices of the other four products offered by Huahai were significantly lower than those of the originator manufacturers in the 2018 national average bid-winning prices; fosinopril sodium tablets were priced slightly below the originator product. Therefore, Huahai’s five product lines hold a competitive advantage and are highly likely to lead the pharmaceutical market in the pilot cities.

Although Huahai’s lisinopril tablets and paroxetine hydrochloride tablets already held a dominant market position prior to this tender, gradually achieving self-driven generic substitution of originator products, losartan potassium tablets (RMB 1.959 billion) and risperidone tablets (RMB 1.168 billion)—which recorded high sales in public hospitals in 2017—have long been dominated by originator drugs. Following the implementation of centralized volume-based procurement, Huahai’s two products will benefit significantly. In particular, its risperidone will deliver a disruptive competitive blow to Enhua Pharmaceutical’s flagship product. Huahai’s potential market exclusivity this year is likely to become the decisive “battle of Tianwangshan” between the two pharmaceutical companies in this therapeutic area.

Huahai’s other two non-exclusive products, irbesartan tablets and irbesartan/hydrochlorothiazide tablets, already had low market shares; however, they likely carried no historical baggage, making it entirely possible for the company to submit a shockingly low bid.

Yangtze River Pharmaceutical Group has four products shortlisted this time, among which Enalapril Maleate Tablets and Dexmedetomidine Hydrochloride Injection are exclusive. Notably, the sales revenue of Dexmedetomidine Hydrochloride Injection in the public medical institution market reaches as high as RMB 2.4 billion. The procurement specification for Dexmedetomidine Hydrochloride Injection is 0.2mg/2ml, a format offered exclusively by Yangtze River Pharmaceutical Group; the originator drug from Orion Pharma does not come in this specification. Therefore, Yangtze River can capture the market share associated with this primary specification. This constitutes significant negative news for four other companies producing this variety—Hengrui Medicine, Enhua Pharmaceutical, Cisen Pharmaceutical, and Guorui Pharmaceutical—and is particularly detrimental to Kelun Pharmaceutical, which has just obtained approval. It is a severe blow before they have even gained a foothold. However, this product is the third ANDA approved by the FDA for Hengrui Medicine. According to our regulatory authorities’ “green channel” concept, co-line production can be considered equivalent to passing the consistency evaluation, so Hengrui will also benefit. Nevertheless, due to the first-mover advantage in the anesthesiology pipeline, once a product is established, it is very difficult to replace. Seizing early market opportunity is crucial!

Although Hengrui had no products included in this volume-based procurement, the company has received FDA approval for ANDAs covering nine products to date.

Hengrui's Approved ANDA Products

In addition, Hengrui expects to receive FDA approval for ANDAs of desflurane, capecitabine, fondaparinux sodium, and other products in 2018, positioning it as a major winner in future consistency evaluations and volume-based procurement.

Although Hansoh Pharmaceutical is not the highlight of this procurement, it will still benefit significantly. The two products shortlisted by Hansoh Pharmaceutical are both exclusive: olanzapine tablets and imatinib mesylate tablets. Moreover, the sales volumes of these two products in the public medical institution market reached RMB 3.688 billion and RMB 1.932 billion, respectively. In particular, for imatinib mesylate tablets, although Novartis’s original drug currently dominates the market, Hansoh’s average winning bid price in 2018 was only one-tenth that of Novartis. Therefore, Hansoh Pharmaceutical has a very clear price advantage in this pilot city tender procurement, and its successful bid is all but certain!

Qilu Pharmaceutical has two shortlisted products in this round, with its Gefitinib tablets being the only ones to have passed the consistency evaluation. AstraZeneca, the originator of Gefitinib, once dominated the market with a share of over 90%, effectively holding a near-monopoly. However, Qilu Pharmaceutical’s winning bid price is two-thirds that of AstraZeneca’s. If Qilu can maintain its price advantage in this tender procurement, it will successfully achieve generic substitution for the originator drug in the Gefitinib segment—a major product category with future market potential reaching RMB 3 billion!

Furthermore, we have noted that four pharmaceutical companies, although having only one product shortlisted in this round, hold exclusive rights to these products. These are Pulite Pharmaceutical’s Azithromycin for Injection, Sichuan Huanyu’s Pemetrexed Injection, Salubris’s Clopidogrel Bisulfate Tablets, Wuhan Da’an Pharmaceutical’s Flurbiprofen Axetil Injection, and Shanghai Ambrosio’s Montelukast Sodium Tablets. Among these, three products each generate annual market sales of approximately RMB 2 billion, while the market sales of oral immediate-release Clopidogrel reach as high as RMB 11.479 billion, making it the highest-selling product among the 31 varieties included in this procurement. This implies that if the originator drugs do not significantly reduce their prices, these four generic drugs will face no competition in the current volume-based procurement. They can easily and completely replace the originator products, thereby capturing a substantial market share with minimal effort.

From a market performance perspective, any drug variety with high sales revenue inevitably becomes a fiercely contested battleground for major pharmaceutical companies. According to 2017 statistics on sales at public medical institutions in China, among the 31 varieties included in the current volume-based procurement list, eight had annual sales exceeding RMB 3 billion. Of these, five varieties faced intense competition between originator drugs and generics, as well as among different generic products.

Atorvastatin oral immediate-release formulations have a public market size of RMB 9 billion. Pfizer, the originator, holds a 67% share; however, its winning bid price is significantly higher than those of two other pharmaceutical companies. If Pfizer fails to substantially reduce the price for this product, Beijing Jialin and Zhejiang Xindonggang will jointly compete for the substantial market share. Currently, Beijing Jialin’s market share is far greater than that of Xindonggang; therefore, it must make an all-out effort to maintain its leading position in the pilot cities. AstraZeneca’s rosuvastatin calcium tablets also command half of the market share, with its 2017 winning bid price being approximately three times that of four other enterprises. In the irbesartan oral immediate-release segment, Sanofi occupies nearly half of the market, and its average winning bid price in 2018 was 3–4 times higher than that of three other products. Among generic alternatives, Hengrui Medicine holds the largest market share and enjoys a competitive advantage in the current tender. Similarly, among clopidogrel oral immediate-release formulations, which generated sales of RMB 11.479 billion, Sanofi’s market share exceeds 50%.

Based on the above, we find that the vast majority of sales in the public market are driven by original brand-name drugs from foreign pharmaceutical companies. These originator drugs hold an extremely high market share in China, with prices remaining persistently high. Driven by both the high prices and substantial procurement volumes of these originator drugs, their market sales have surged dramatically. Reducing medical insurance payments and squeezing out originator drugs to bring foreign companies down from their pedestal and support domestic industry is the true objective of the centralized volume-based procurement policy—a move akin to “Xiang Zhuang performing the sword dance with the intent of targeting Pei Gong.”

As the number of products passing the consistency evaluation increases and volume-based procurement is gradually implemented, originator drugs that have lost patent protection are becoming increasingly marginalized, and their currently substantial sales revenues are poised to decline. Although exclusive products appear to gain market share with ease, they cannot rest on their laurels; after the one-year validity period expires, new competitors will inevitably pass the consistency evaluation, forcing incumbent manufacturers to once again compete against these newly qualified entrants.

In the United States, once originator drugs lose patent protection, their prices plummet to rock-bottom levels; indeed, many are likely to exit the market altogether given U.S. insurance reimbursement rates. In China, however, although numerous generic manufacturers compete with originator companies for market share, originators of major drug products not only achieve overwhelming dominance but also capture more than 50%—and in some cases over 90%—of the market. Their winning bid prices are several times, and even up to ten times, higher than those of generics (for example, oral immediate-release imatinib).

Among the 31 drug varieties listed in the “4+7 City Centralized Drug Procurement Document,” the multinational pharmaceutical companies primarily affected include Pfizer, AstraZeneca, Sanofi, GlaxoSmithKline, and Bristol-Myers Squibb. For originator drugs, manufacturers face a dilemma: either reduce prices in line with generic competitors or forfeit their bids, thereby losing the majority of market share in the 11 pilot cities while continuing to focus on the remaining markets. However, as the scope of the volume-based procurement pilot expands in the future, the transitional period for price reductions of originator drugs will come to an end. It is highly likely that originator drug manufacturers will implement significant price cuts to safeguard their national market share. In 2017, the market shares of AstraZeneca’s gefitinib, GlaxoSmithKline’s tenofovir disoproxil fumarate, and UCB’s levetiracetam at public medical institution terminals in China all exceeded 90%. Therefore, it cannot be ruled out that these originator manufacturers may resort to substantial price reductions to maintain their market positions. Amidst the dual pressures of policy reforms and generic competition, how originator drugs will respond remains to be seen.