Pharmacy M&A in 2018: Multi-Source Capital Frenzy and the Need for Vertical Integration

“Mergers and acquisitions were in full swing during the first half of this year, particularly involving Gaoling-affiliated Gaoji Medical, which is rumored to have acquired more than 10,000 pharmacies, reaching a massive sales volume of RMB 26 billion. However, M&A activity has cooled since the second half of the year, primarily because these large capital consortia experienced ‘indigestion’ during the integration process after rapidly acquiring a substantial number of pharmacies in a short period,” an industry insider told VCBeat, noting that the trend of M&A and consolidation in the retail pharmacy sector is undergoing changes.

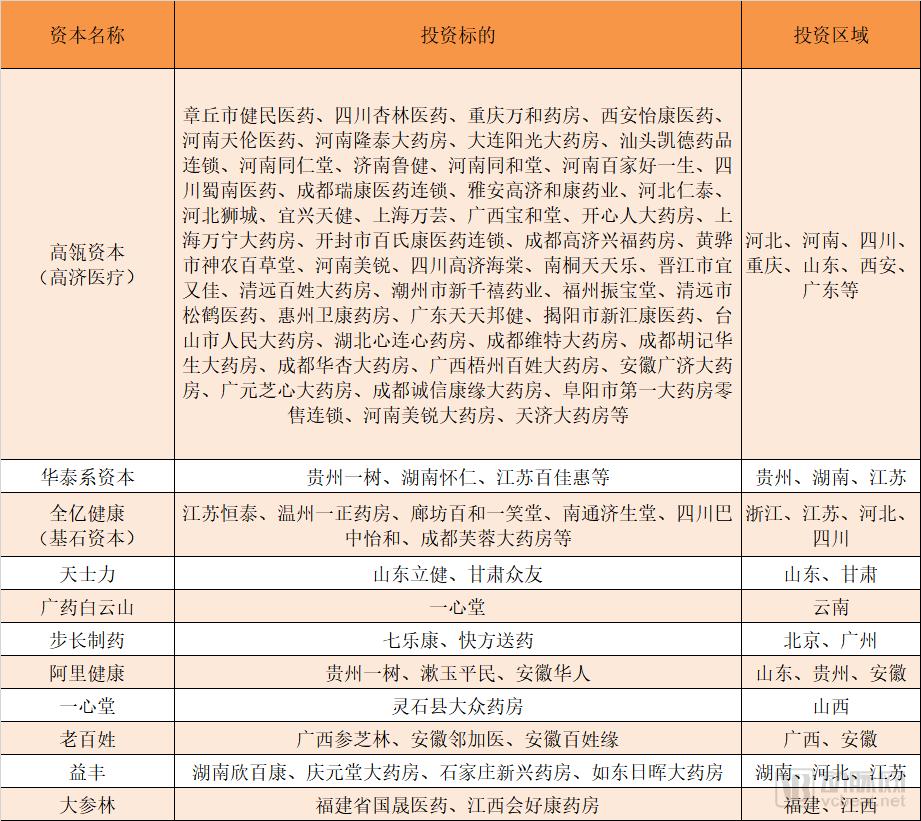

According to incomplete statistics from VCBeat, in recent years, four major capital factions have been eyeing the retail pharmacy sector. These include: non-industry investors such as Hillhouse Capital and Morgan Stanley; pharmaceutical groups including industrial conglomerates like Guangzhou Pharmaceutical Holdings (Baiyunshan), Tasly Group, and Buchang Pharma; listed pharmacy chains such as Yixintang, Laobaixing, Yifeng, and Dashenlin; and internet-plus-pharma platforms like Ping An, Alibaba, and JD.com.

Capital acts as a catalyst for industry development, accelerating the process of industry evolution. Changes in scale, competitive landscape, and business models that previously took ten or even twenty years to materialize are now being initially completed within just one or two years.

Following rapid “forced maturation,” acquirers and operators in the retail pharmacy sector must grapple with how to avoid “integration without cohesion” and swiftly leverage economies of scale to achieve—or even surpass—expected value returns. After all, the essence of business lies in strategic foresight and proactive execution.

This article primarily explores the “post-merger era” of chain pharmacies, with the following structure:

1. From “Value Investing” to “Integration Without Consolidation”;

2. Prescription outflow fell short of expectations; impact from “Internet + Healthcare”;

3. Is the U.S. Vertical Integration Model Worth Learning From?—Commercial Insurance and PBMs;

4. Tiered and Classified Management of Pharmacies—Greater Capability, Greater Responsibility.

Undoubtedly, the wave of mergers and acquisitions (M&A) and consolidation in the chain pharmacy industry has begun to cool down. This trend is manifested in three key aspects. First, valuation: as the M&A momentum has built up, transaction prices have continued to rise and are now approaching a critical threshold. Second, target availability: with large capital players, major conglomerates, and industry insiders aggressively vying for market share, high-quality, scarce acquisition targets have become a thing of the past. Third, “diseconomies of scale”: as chain pharmacies backed by capital expand in size, their existing human resource reserves, organizational structures, and management practices have proven inadequate to handle the enlarged scale, leading to increasingly higher friction costs within enterprises.

Capital’s “Hunt” for Chain Pharmacies

Source: VCBeat

Let us break this down point by point. First, regarding valuation: there are two primary pricing models for mergers and acquisitions (M&A) in the chain pharmacy sector—price-to-earnings (P/E) ratio and price-to-sales (P/S) ratio. The P/S ratio is generally used as the key metric, calculated as the acquisition price divided by the pharmacy’s annual sales revenue. Capital-driven M&A activity has pushed P/S ratios steadily upward. Two years ago, these ratios ranged from 0.7x to 0.9x; currently, many have risen above 1x, with premium assets such as hospital-adjacent pharmacies and large-format stores reaching multiples as high as 1.5x.

Do not underestimate this slight change. Assuming an average annual revenue of RMB 2 million per pharmacy, a company with 200 stores would be valued at approximately RMB 300 million under the previous valuation method. However, using a price-to-sales (P/S) ratio of 1.5x, the valuation would jump to RMB 600 million. This sharp increase in price makes transactions even more difficult to close during a capital winter.

Furthermore, capital participation in the M&A and consolidation of retail pharmacies is often benchmarked against listed companies in the industry, such as Yixintang and Laobaixing. Listed companies are valued based on their price-to-earnings (P/E) ratios. In principle, the P/E ratio assigned to acquired enterprises should not exceed that of listed companies, because going public requires a series of processes, including shareholding reform, structural restructuring, operational optimization, and pre-IPO tutoring—essentially ensuring that “the price of flour is lower than that of bread.” However, with recent setbacks in the stock market, the market capitalizations of many retail pharmacy concept stocks have corrected. At this time, investing in the secondary market has become more advantageous than investing in the primary market, resulting in a scenario where “bread is cheaper than flour” and causing a severe inversion in valuation levels.

Let us examine the landscape of investment targets in the market. Capital inflows typically avoid enterprises with excessively small scales, focusing instead on leading players at the municipal or county level—often referred to as “growth-oriented” pharmacies—which have the potential to become dominant regional pharmacy chains. Capital possesses a keen sense of opportunity; after relentless scouting by investors, many high-quality targets have already been secured. In fact, industry insiders estimate that over 80% of regional leaders have introduced capital during their development phases. It is precisely this capital infusion that has facilitated regional consolidation, providing these companies with growth momentum beyond their organic capabilities. Few high-quality targets remain; those still available are either priced too high or lack the willingness to bring in external capital, making them unsuitable for large-scale capital injection.

Finally, there is the “negative scale effect.” As industry insiders put it: “The integration of tens of thousands of pharmacies, involving hundreds of acquired companies, presents an unprecedented management challenge. After acquisition, original founders often choose to cash out and exit or step back into secondary roles, significantly diminishing the acquired firms’ inherent resource advantages and execution capabilities. Unless the acquirer strengthens management and enhances operational capabilities, a decline in the performance of the acquired entities is inevitable. Capital injection is akin to organ transplantation, carrying similar risks of rejection. To mitigate such rejection, immunosuppression is required, the consequence of which is short-term performance adjustment. To a large extent, this adjustment is unavoidable.”

In summary, the M&A trend in the chain pharmacy industry is characterized by a scarcity of high-quality targets and escalating valuations. From a financial investment perspective, more attractive investment opportunities have emerged elsewhere. Furthermore, the rapid pace of M&A activity necessitates a period of integration and digestion. These factors collectively signal the arrival of an inflection point in industry consolidation, marking the entry into the “post-M&A era.”

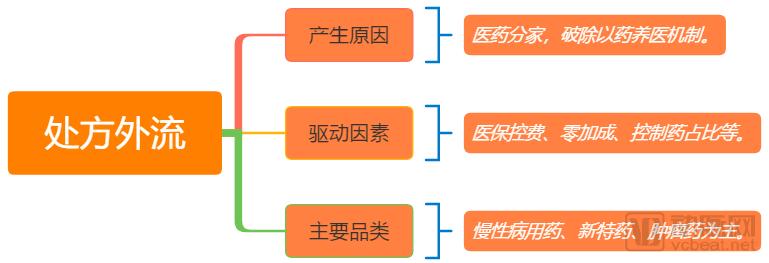

To a large extent, capital inflows into the retail pharmacy sector are a “bet” on the future. Investors favor pharmaceutical retail primarily for three reasons: first, it is a business model with relatively low entry barriers; second, the domestic pharmaceutical retail industry is highly fragmented, and capital injection can facilitate industry consolidation; third, supportive policies are boosting the development of retail pharmacies, such as the relaxation of health insurance accreditation reviews and opportunities arising from prescription outflows under the separation of prescribing and dispensing.

Capital is focusing on the third point, particularly the opportunities arising from prescription outflow under the separation of prescribing and dispensing. Global experience indicates that the separation of prescribing and dispensing is an inevitable trend. The United States has implemented a relatively thorough separation, with approximately 60–70% of medications sold through non-hospital channels (pharmacies and PBM mail-order services). Japan has practiced the separation of prescribing and dispensing for over 40 years, with currently around 70% of prescription drugs dispensed through out-of-hospital channels. The experiences of the United States and Japan provide a reference for estimating the scale of domestic prescription outflow in China, which some institutions predict will reach the trillion-yuan level. For retail pharmacies, this represents a brand-new incremental market, with significant potential for performance growth being self-evident.

However, upon careful consideration, the outflow of prescriptions does not constitute a new element of business model. Unlike the transformation e-commerce brought to retail, which could be achieved merely through shifts in consumer and supplier habits, the realization of prescription outflow is highly complex. It involves numerous stakeholders, including social security authorities, health and family planning commissions, drug administration agencies, hospitals, physicians, and pharmacies. If any single link in this chain says “no” to prescription outflow, the initiative will largely stall. Relatively speaking, pharmacies act as recipients in this process; they are the passive party, having to wait for policy approval and the transfer of prescriptions from hospitals. Consequently, pharmacies have very limited control over the entire prescription outflow process.

To capture the outflow of prescriptions, retail pharmacies must overcome “three major hurdles”: prescription sources, supply chain and pharmaceutical care capabilities, and social insurance support. Generally speaking, few retail pharmacies have strong ties with hospitals—except for integrated wholesale-retail enterprises. In contrast, distribution and logistics companies possess hospital resources and can access prescriptions. Secondly, regarding drug supply assurance and pharmaceutical care services, prescription drugs have not been the operational focus or primary profit source for pharmacies in the long term; therefore, their variety of prescription drugs and service capabilities are limited. Lastly, concerning social insurance support, it is currently difficult to integrate with the pooled social insurance funds. If reimbursement is unavailable, the appeal to patients remains limited.

Of course, this is not to say that retail pharmacies are completely unable to absorb the outflow of prescriptions from hospitals; rather, it means that due to their inherent operational characteristics and business models, retail pharmacies may fail to meet expectations when attempting to capture this prescription volume. Having identified the challenges, the next step is determining how to overcome them, which lies at the core of management focus in the “post-M&A era.”

Furthermore, we should address the impact of the “Internet + Healthcare” model, particularly from a capital perspective. Major players such as Ping An, Alibaba, and JD.com have made significant investments in pharmaceutical retail. Among them, Alibaba has established the most systematic approach. Leveraging its flagship health platform, Ali Health, Alibaba has recently intensified its investments in regional leading pharmacy chains, including Shuyu Civilian in Shandong, Huaren Health in Anhui, and Yishu Pharmacy in Guizhou. These investments aim to promote the integration of online and offline pharmaceutical retail channels within the respective regions covered by these chains. Alibaba’s equity participation is relatively “moderate,” as it does not seek absolute control nor impose performance valuation adjustment mechanisms (VAMs). This presents an excellent opportunity for regional leaders aspiring to expand their scale.

The second major impact of the “Internet + Healthcare” model is the rise of “New Retail,” or more specifically, the O2O (Online-to-Offline) model. Why does the O2O model disrupt traditional pharmaceutical retail? Traditional retail pharmacies operate within a 300–500 meter radius, relying entirely on offline presence; securing a prime location with high foot traffic ensures strong business performance. In contrast, O2O expands the service coverage of individual pharmacies to a 3–5 kilometer radius. The most immediate consequence is a reduced need for physical stores, leading to a significant decrease in the number of pharmacies within any given area. Many pharmacies failing to meet performance expectations will inevitably be eliminated.

The impact of O2O on traditional pharmacies is also reflected in the decline of foot traffic. Previously, customers had to visit physical stores to purchase medications, allowing staff to provide guided shopping experiences, make recommendations, and complete customer profiles for secondary development initiatives, such as membership management and promotional campaigns. However, under the O2O model, customers can purchase medications without visiting the store, eliminating opportunities for product recommendations and secondary development. This has placed consumers entirely outside the control of pharmacies, rendering many marketing activities that were previously executable offline uncertain in the online environment.

The correct approach for the future should involve driving traffic from offline to online, from online to offline, and fostering mutual traffic flow between the two, thereby blurring the boundaries between online and offline channels. Beyond “online ordering with in-store pickup” and “online ordering with store-based delivery,” we should explore more forms of new pharmaceutical retail based on geographic location and big data on pharmaceutical consumption. In this regard, Alibaba, JD.com, and Meituan are pioneers with valuable experience, and early participants in the industry will also benefit.

Another major event in the global pharmaceutical retail sector recently was CVS, a star enterprise among U.S. pharmacies, announcing the completion of its acquisition of health insurer Aetna. The $69 billion deal, first announced in December 2017, is not only the largest transaction in the history of the U.S. pharmaceutical retail industry but also the biggest merger and acquisition event in the global pharmaceutical industry in 2017.

The U.S. pharmaceutical retail industry is currently characterized by a duopoly. Although CVS trails Walgreens in terms of store count and retail scale, its total revenue exceeds that of Walgreens. According to CVS’s 2016 annual report, the company operated more than 9,700 pharmacies nationwide, 1,100 of which were equipped with “MinuteClinic” facilities. Its Pharmacy Benefit Management (PBM) business served nearly 90 million members. In 2016, CVS reported revenue of $177.526 billion, representing a 15.8% increase from the previous year, and net income of $5.319 billion, a 1.5% rise compared to 2015.

Aetna is one of the oldest health insurance companies in the world. In 1850, it established an Annuity department and commenced life insurance operations; in 1853, this department was spun off to form Aetna Life Insurance Company. In the United States, the company ranks among the leaders in the medical, dental, pharmaceutical, life, and group disability insurance sectors. According to Aetna’s 2016 annual report, its revenue for 2016 was $63.155 billion, a 5% increase from 2015, while net income was $2.271 billion, a 5% decrease from the previous year. The same 2016 annual report indicated that Aetna had 23.11 million health insurance members.

The intersection of pharmaceutical retail and commercial health insurance lies in Pharmacy Benefit Management (PBM) services. Following CVS’s acquisition of Aetna, a comprehensive healthcare service ecosystem encompassing “PBM + pharmaceutical retail + health insurance + medical services” will be established. Aetna’s 23 million members will serve as a source of customer traffic for CVS, while Aetna will benefit from more refined pharmacy benefit management and cost-containment measures provided by CVS. More importantly, this integration will create a powerful bargaining alliance, strengthening negotiating leverage against pharmaceutical companies and healthcare providers, thereby helping to further reduce operational costs.

In fact, it is the PBM business that has helped CVS achieve its “second growth curve.” This point was already clarified in VCBeat’s previous case analysis of CVS: From the perspective of CVS’s business model, the entire group is divided into two core segments—Pharmacy Services and Retail. The essence of Pharmacy Services lies in earning management fees and other related charges by entering into agency contracts with institutions or enterprises; whereas the essence of the Retail segment lies in generating profits through online and offline sales. In recent years, as both segments have continuously expanded their business lines, they have each demonstrated a certain degree of cross-segment operations. Together, these two segments account for nearly all of CVS’s revenue.

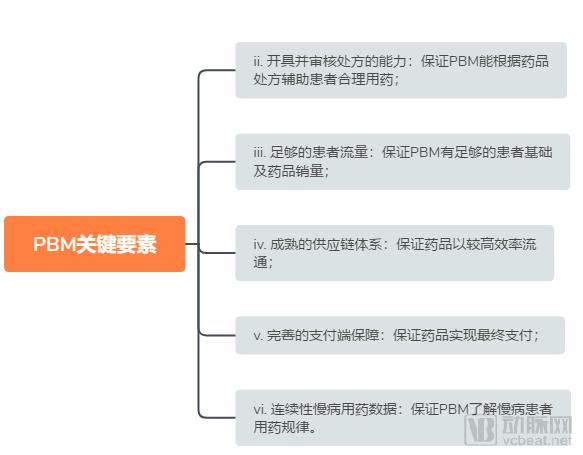

Pharmacy Benefit Management (PBM)Pharmacy Benefit Management (PBM) refers to a specialized third-party service. The PBM model primarily functions as an administrative and coordinating intermediary among insurance/benefit providers, pharmaceutical manufacturers, patients, and pharmacies. It was established to effectively manage healthcare costs, reducing medical expenditures for payers while enhancing benefits for medication consumers.

Key Elements of PBM

Source: China Renaissance Capital

The core of the U.S. PBM model lies in its penetration into every segment of the pharmaceutical distribution chain, balancing the interests of payers, suppliers, distributors, and patients through contractual agreements. By leveraging robust databases to develop formularies, PBMs provide cost-effective prescription medications tailored to the specific drug needs of different clients. This approach ensures high-quality treatment for patients while reducing healthcare expenditures for payers. The primary roles of the PBM model within the entire pharmaceutical distribution system are as follows:

1) Establish a database using extensive clinical data and medication history of insured individuals to conduct rationality reviews of prescriptions issued by physicians;

2) By regulating patient medication, the phenomena of over-treatment and drug abuse have been controlled;

3) Leverage its user base advantage to effectively control prescription drug costs by signing contracts with pharmacies and pharmaceutical manufacturers, utilizing its strong bargaining power;

4) Reduce insurance expenditures and achieve medical cost containment;

5) Connects multiple stakeholders in the pharmaceutical distribution industry (primarily patients, insurance institutions, pharmacies, and pharmaceutical companies) and achieves integration of multi-party resources;

Many retail pharmacies in China have stated on various occasions that they intend to draw lessons from CVS’s development experience and use CVS as a benchmark. However, few enterprises have successfully integrated pharmaceutical retail operations with Pharmacy Benefit Management (PBM) services. The underlying reasons are highly complex, involving differences in healthcare payers: the U.S. system is dominated by commercial insurance, whereas China relies primarily on social health insurance. Cost containment under China’s social health insurance is driven by administrative mandates, which are relatively distant from market mechanisms. Additionally, there are significant differences in the degree of retail consolidation. The U.S. implemented the separation of prescribing and dispensing earlier, leading to pronounced scale economies in the retail pharmacy sector. Companies such as CVS, Walgreens, and ESI hold absolute leading positions in retail, thereby facilitating the provision of pharmaceutical services and integrated “pharmacy + insurance” solutions both within their corporate groups and across the industry.

However, the cross-industry vertical integration along the pharmaceutical supply chain undertaken by U.S. pharmaceutical retailers offers valuable lessons for their Chinese counterparts. When horizontal integration hits a ceiling or reaches an inflection point, vertical integration can not only break the deadlock but also often achieve unexpected breakthroughs.

The differences, or rather advantages, of China’s retail pharmacy sector compared to that of the United States lie in the following aspects. First, the high saturation of pharmacies and the lower ratio of population served per pharmacy create ample time and space to deliver more innovative services. Second, pharmacy coverage is extensive; in urban areas, there is virtually always a pharmacy within 300–500 meters. As natural, neighborhood-based health service providers, pharmacies are closer to end users and hold significant potential for delivering personalized, intimate care. Additionally, factors such as a high level of urbanization and concentrated residential patterns further strengthen these advantages. The key question is how effectively the industry can leverage these resources to convert these strengths into tangible value.

In fact, we are currently witnessing innovations in the “Retail+” model within China’s pharmaceutical retail industry, such as “Retail + Insurance,” “Retail + E-commerce,” “Retail + Medical Services,” and “Retail + Health Management.” Although these models are still in their early stages, they may eventually demonstrate the value of such innovation over time.

On November 23, the Ministry of Commerce issued a notice soliciting public comments on the “Guiding Opinions on the Classified and Graded Management of Retail Pharmacies Nationwide (Draft for Comment).” The explanatory notes accompanying the draft stated that in recent years, China’s pharmaceutical retail market has demonstrated steady growth, optimized structure, and quality upgrading. Statistical data show that in 2017, the total sales volume of the national pharmaceutical retail market reached RMB 400.3 billion, a year-on-year increase of 9.0%. There were 5,409 pharmaceutical retail chain enterprises and 454,000 retail pharmacy outlets across the country.

However, the issues of small scale, fragmentation, and disorganization remain prominent in the pharmaceutical retail industry. The overall levels of standardization, informatization, and intensification are relatively low, while management standards and service capabilities among pharmacies vary significantly, thereby constraining the effective implementation of prescription drug sales and medication therapy management services. In some regions, the distribution of retail pharmacy outlets is unbalanced; individual remote areas suffer from insufficient drug supplies, leading to inconveniences and economic burdens for patients when purchasing medications. Consequently, the industry’s potential to support broader health initiatives has not been fully realized.

There is a significant gap between the overall development level of the industry and the requirements of the “Three-Medical Linkage” reform—encompassing healthcare delivery, medical insurance, and pharmaceuticals—making it difficult to support and facilitate the implementation of key reform priorities, including tiered diagnosis and treatment, modern hospital management, universal health coverage, drug supply assurance, and comprehensive regulation.

Implementing classified and tiered management for retail pharmacies helps accelerate the transformation and upgrading of the pharmaceutical retail industry, lays a foundational groundwork for deepening the coordinated reform of medical care, health insurance, and pharmaceutical supply (the “Three-Medical” linkage), enhances management capabilities for both regulatory authorities and enterprises, and enables patients to access high-quality medicines and services more affordably and conveniently, thereby fostering a superior medication-purchasing environment.

We believe that the core logic behind the classified and tiered management of pharmacies is “with greater capability comes greater responsibility.” Why do we say this? Because retail pharmacies are categorized into three classes based on their operational conditions and compliance status: Class I pharmacies are permitted to sell Class B over-the-counter (OTC) drugs; Class II pharmacies are permitted to sell OTC drugs, prescription drugs (excluding prohibited and restricted medications), and traditional Chinese medicine (TCM) decoction pieces; Class III pharmacies are permitted to sell OTC drugs, prescription drugs (excluding prohibited medications), and TCM decoction pieces.

Operating conditions and compliance status include factors such as retail pharmacies’ capacity to ensure drug quality, staffing of licensed pharmaceutical professionals, and records of administrative penalties. This implies that pharmacies with existing advantages will receive preferential allocation of administrative licensing resources, thereby expanding their growth potential. Naturally, rights and obligations are commensurate; meeting the standards for high-tier pharmacies requires higher upfront investment. As the payback period for new pharmacy establishments lengthens, this will further drive consolidation within the existing pharmacy market, benefiting mergers and acquisitions as well as business upgrades across the industry.

Opportunities and challenges coexist; it is the right time for retail pharmacies to take off. Regarding future industry trends, we make the following predictions:

1. Capital inflow into the pharmaceutical retail industry has reached an inflection point, with a greater emphasis on balancing price and future value;

2. Following large-scale M&A activities, there is a certain adjustment period, during which performance will temporarily revert;

3. Mergers and acquisitions will increase industry concentration, and the future industry landscape may consist of several national leaders plus a number of regional leaders;

4. The separation of prescribing and dispensing will continue to be implemented, with retail pharmacies becoming one of the primary recipients of outflowing prescriptions;

5. DTP pharmacies and specialty pharmacies have developed rapidly, becoming an important business format independent of general chain drugstores;

6. The “Internet + Healthcare” model continues to penetrate the market, with new retail and O2O models sweeping across China;

7. Retail pharmacies will integrate with internet healthcare, pharmaceutical e-commerce, O2O, and other models; omni-channel integration will become the industry norm, while membership management and operational capabilities will enhance market competitiveness and spur entrepreneurial opportunities;

8. Pharmaceutical retail enterprises have begun to pursue vertical integration, strengthening collaborations with commercial insurance providers and health management companies, leading to increased innovation in “Retail+” business models;

9. Rising costs for establishing new retail pharmacies and higher entry barriers are conducive to further consolidation of the existing market.