Song Liangjing of TH Capital: 'The Winter Is Colder Than Imagined—Entrepreneurship Enters the Silver Age'

Editor’s Note: This article is reprinted from Taihe Capital, with authorization granted to VCBeat.

On November 27, 2018, Song Liangjing, Managing Partner and CEO of Taihe Capital, shared his observations and reflections on the current state of the primary market. The key points are as follows:

From the three dimensions of investor returns from newly listed companies, strategies of active investors in the primary market, and actual project financing data, we find that the 2018 capital winter was colder than most people imagined.

A deeper analysis reveals that this capital winter differs from previous ones, as it represents the convergence of four major cycles: the economic cycle, industrial cycle, capital cycle, and policy cycle.

The era of abundant “golden” opportunities has passed. In the next decade, we will enter the “silver age” of entrepreneurship and investment, with industrial internet as the central theme of opportunity.

The following is a transcript of the speech.

The topic I am sharing today is titled “Primary Market: The Cycle Returns,” which pertains to the cyclical nature of market fluctuations.

It is 2018. We often speak of ten-year cycles, such as the global financial crisis ten years ago and the Asian financial crisis twenty years ago. Could 2018 mark the end of the golden decade for entrepreneurship and serve as a turning point from peak prosperity to decline? Opinions on this may vary. However, in 2018, we have at least witnessed a rare coexistence of “ice” and “fire” in the capital markets. Why “fire”? We have seen an almost unprecedented IPO boom in the secondary market, with a large number of TMT companies successfully listing in the United States and Hong Kong. Over the past year, the market has witnessed cases where certain investment firms took more than ten portfolio companies public, generating $1 billion in returns for their limited partners (LPs). Yet 2018 has also been characterized by “ice,” with the chill in the primary market exceeding all expectations.

Over the past decade, I have experienced three market cycles: in 2008, 2012, and 2015. However, none of these previous cycles witnessed such a stark divergence where the secondary market was extremely hot while the primary market remained exceptionally cold. Perhaps in a few years, when we look back on 2018, it will be remembered as a noteworthy year for both entrepreneurs and the venture capital community.

Having just discussed our overall perception of the capital markets in 2018, I will now walk you through three sets of data. The first set concerns the actual return on investment (ROI) delivered to investors by companies that went public. Let us examine the secondary market performance in 2018 to determine whether IPOs genuinely generated profits for investors. Earlier, several investment bankers subtly suggested that companies in the new economy should avoid setting excessively high IPO prices, thereby allowing participants in the secondary market to achieve positive returns.

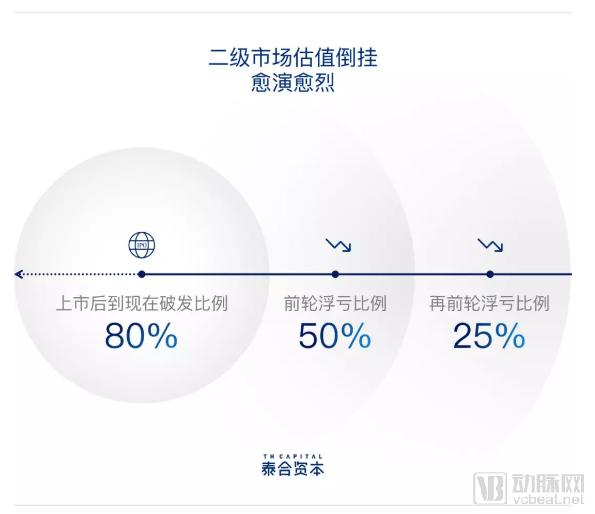

Our team recently conducted such a quantitative analysis, selecting dozens of TMT companies newly listed on the Hong Kong and U.S. stock markets over the past year to examine investor profits and losses across their last three financing rounds. The findings reveal that, based on the latest prices, 80% of cornerstone investors in these IPOs have incurred losses since listing. Looking further back at the Pre-IPO round, 50% of investors are at a loss. Moreover, for 25% of the companies, their current market capitalization is lower than the valuation in the preceding round, meaning those investors have yet to realize any gains. Thus, while an IPO is undoubtedly a prestigious milestone, generating tangible financial returns remains the ultimate imperative. This reflects our observation of the secondary market.

Second Set of Data: What Is the Current Investment Pace of Mainstream Investors in the Primary Market? This is a survey and analysis of the subsequent investment strategies of the 15 most active large private equity (PE) firms and five major strategic investors in China’s capital market in 2018, and the findings are striking. First, 55% of the investment institutions explicitly stated that they would significantly scale back their investments.

Second, the neutral feedback from 20% of investors actually implies a slight contraction. Only 25% of investors have expressed an active interest in evaluating projects, and this figure already represents data from the top 20 most active institutional investors in the market this year. The stance of these key capital providers signals the imminent trend facing the market. This indicates that 70–80% of investors in today’s capital market have entered a period of inactivity, a development that will undoubtedly have a profound impact on primary market fundraising in 2019 and even 2020.

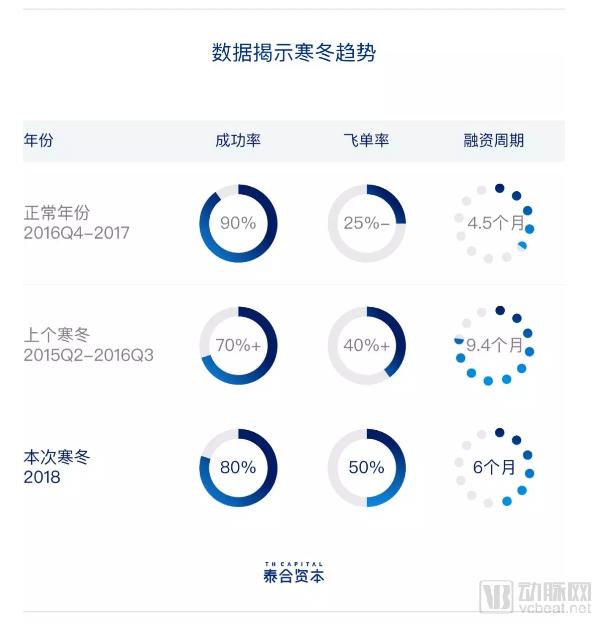

The third set of data examines actual fundraising figures for primary market projects. Taihe Capital served dozens of companies at Series C and D stages in 2018, with total funds raised exceeding RMB 35 billion to date; thus, our statistical base should possess a certain degree of market representativeness. We typically assess the smoothness of fundraising based on success rate, deal fall-through rate, and fundraising cycle. In a normal year, such as from Q4 2016 to 2017, Taihe’s projects achieved a fundraising success rate of 90%, a deal fall-through rate of less than 25%, and an average fundraising cycle of 4.5 months. However, during the previous capital winter (Q2 2015–Q3 2016), the fundraising success rate dropped to only 70%, the deal fall-through rate exceeded 40%, and the fundraising cycle extended to 9.4 months.

What is the current situation? On a positive note, the success rate has remained at approximately 80% so far, although the fundraising cycle has slightly extended to six months. However, it is worth noting that the deal-jumping rate has increased significantly. Over the past year, 50% of projects experienced deal-jumping, which indeed reflects market sentiment. In particular, over the last two to three months, we have observed a further decline in both the success rate and the duration of fundraising cycles for ongoing projects. The data for 2019 will undoubtedly be worse, reflecting the true state of the primary market.

Today, there are many entrepreneurs present. We have summarized the common characteristics of projects that experienced order diversion (“flying orders”) and a small number of unfinished projects over the past year, hoping to provide some insights for everyone.

Our statistics reveal that over 80% of order-skipping incidents stem from the following three causes:

First, valuation expectations are too high; 60% of deal losses and project failures involve this reason.

Second, continuous cash burn with an unproven business model has led to 40% of order losses and failures.

Third, policy-sensitive industries—such as entertainment, finance, and education—have seen a series of regulatory policies introduced over the past one to two quarters, significantly impacting certain sectors. This factor accounts for 15% of deal terminations and funding failures. Therefore, in the current market environment, fundraising for projects in these three categories will face even greater challenges. If your project unfortunately falls into any of these categories, please exercise caution. You may also notice that the sum of these percentages exceeds 100%, as deal terminations often result from multiple factors. If a company exhibits all three characteristics, it warrants serious reflection.

What are the causes of this year’s capital winter? If we conduct an in-depth analysis, this capital winter differs from previous ones and may be even more severe, as it results from the convergence of four cycles: the economic cycle, the industrial cycle, the capital cycle, and the policy cycle.

——Regarding the economic cycle, I will highlight just three figures: In Q3 2018, China’s year-on-year GDP growth rate fell to 6.5%, and in October 2018, the growth rate of China’s total retail sales of consumer goods dropped to 8.6%, both hitting multi-year lows. More alarmingly, in October 2018, nationwide new car sales in China declined by 13%. Although this is a micro-level indicator, it serves as an early warning sign of broader economic trends.

—The industry cycle is defined by the disappearance of dividends from the mobile internet. In September 2018, China’s monthly active users (MAU) for mobile internet grew by less than 5% compared to the previous year, down from 10% and 15% in the preceding two years, respectively. Meanwhile, the number of active users reached 1.12 billion, approaching saturation. Thus, the demographic traffic dividend has vanished, while new industrial opportunities have yet to emerge on a large scale.

—Capital Cycle: If you look at the U.S. stock market, it has experienced a prolonged bull run over the past decade, with the Nasdaq Composite Index rising 4.3-fold. However, after reaching a historic high on August 29, 2018, the index showed signs of correction and has since declined by approximately 15%. Most secondary-market institutional investors believe that downward pressure on the market remains substantial.

—There are also policy cycles, such as the restrictions on game license approvals in the culture and entertainment sector; the ban on kindergarten listings in the education sector; and a series of regulatory constraints in the financial sector. These have all had a significant impact on primary market financing.

Therefore, although every cycle is said to be different, this one is truly distinct, as the superposition of cycles will be far more severe.

Having said so much, will 2018, as mentioned at the beginning, mark the end of a golden age? This is a significant topic today. In five or ten years, when we look back on 2018, it will undoubtedly stand out as a particularly distinctive year. This year marked the end of the massive traffic dividend from the mobile internet boom. In this sense, the era when opportunities were abundant everywhere has indeed come to an end.

Over the past decade, we profited from the demographic dividend, which was “easy money.” If there are still profits to be made in the next ten years, they will certainly come from “hard-earned money,” yet this will be the most valuable and highest-barrier capital. The end of one era often signals the beginning of another. In our view, the past decade was a period of “picking up gold,” while the coming decade will be an era of “smelting silver.” In the next ten years, we will enter the “Silver Age” of entrepreneurship and investment, with industrial internet as its central thematic opportunity.

In fact, it is difficult to draw a clear line between the industrial internet and the consumer internet. In essence, many products delivered by industrial internet companies ultimately fall under the category of the consumer internet. The consumer internet has effectively created value in terms of convenience, timeliness, and diversity on the consumption side, while the industrial internet has the opportunity to create deeper value on the supply side, such as improvements in time and cost efficiency, as well as quality optimization.

For instance, the application of big data and technology across various vertical sectors can significantly enhance efficiency, including for the top-tier projects in their respective markets that Taihe Capital serves today. The integration of big data with healthcare can substantially improve the success rate of new drug development, enable more accurate insurance underwriting, and help hospitals optimize their operations. In the logistics sector, big data applications can greatly reduce the empty-load rate of trucks and lower fuel consumption. In retail, big data can enhance the timeliness and success rate of new product launches, enabling more flexible production. If China’s consumer internet is already at a university level, its industrial internet may not yet have graduated from elementary school—but this represents a tremendous opportunity.

Furthermore, the endgame of competition in the consumer internet sector is typically characterized by the dominance of one or two major players, leaving little room for additional competitors. In contrast, the industrial internet is likely to feature a landscape of vibrant competition among numerous enterprises. We believe that the “Silver Age” of the industrial internet has only just begun, representing the greatest opportunity for entrepreneurs.

Returning to the present, how should we navigate economic cycles today? I offer recommendations across three dimensions: first, discern the major trends; second, build competitive moats; and third, stockpile resources. These correspond respectively to your macro strategy, operational strategy, and capital strategy.

Why is it essential to first “grasp the macro trends”? The enterprises we serve today are growing ever larger, with many already surpassing valuations of $1 billion or even $5 billion. At this scale, companies essentially become part of society’s critical infrastructure, assuming an increasingly significant role in providing public services. In this context, entrepreneurs today must pay closer attention to China’s future economic and policy trajectories than at any other point in history. Therefore, it is crucial to place great emphasis on key economic indicators—such as automobile sales, housing market performance, foreign trade volumes, and electricity consumption—as these data points ultimately determine your growth ceiling.

This is even more true for policy. Over the past three decades, China’s development has been driven primarily by the demographic dividend and the benefits of policy deregulation. However, as regulatory frameworks and policy priorities shift, it is essential to closely monitor their impact. For instance, government regulations on ride-hailing services and bike-sharing have significantly constrained these companies’ future growth potential, forcing them to internalize social costs that were previously externalized during their expansion. Therefore, it is crucial to pay close attention to economic trends and broader policy directions, ensuring alignment and resonance with the zeitgeist.

“What does ‘building moats’ mean?” There is much discussion about asset-heavy and asset-light companies. We believe the value of asset-heavy companies will become evident, while asset-light companies face mounting challenges. For instance, paid knowledge services were extremely popular over the past two years, but very few players remain today. Why? Paid knowledge services are largely an innovation in traffic acquisition rather than a sustainable business model.

However, in terms of content production mechanisms, most companies have failed to establish their own barriers to entry, which significantly caps their growth potential and leads to exceptionally fierce competition. We favor companies that deliver substantial, “asset-heavy” value. Our clients—such as Pinduoduo, Guazi, Yunji, and SHEIN, a cross-border e-commerce player—are all increasingly deepening their involvement in the industrial chain and supply side. The value they create extends far beyond traffic acquisition; more importantly, they drive profound transformation across the entire industrial chain, enhancing both efficiency and quality, thereby building higher competitive moats.

“Stockpiling military provisions” means accumulating sufficient development capital.

First, place a high priority on managing your cash flow, especially for B2B enterprises. We have observed numerous cases this year where accounts receivable turned into bad debts. No company fails due to a lack of profits, but many are dragged under by cash flow problems.

Second, for companies that must raise capital, do not fixate on valuation. As we have previously analyzed regarding valuations in the secondary market, valuation is merely a myth.

Third, for companies that are not short of cash, we strongly advise you to raise funds. In a downturn market, fundraising inevitably exhibits the Matthew Effect. In fact, during the previous cycle, companies like Meituan and Didi raised substantial capital despite the adverse trends. We believe that leading companies will certainly secure better valuations.

For leading companies, your cash reserves can enable more aggressive investments in a downturn market, accelerating expansion against the trend. This is our advice to entrepreneurs.

We hope that at this pivotal juncture in the capital market, amidst the risks and opportunities inherent in the transition from old to new industrial drivers, everyone will persist in doing what is difficult yet right, navigate through the cycle, and stride directly into the future.