The Trend Continues: 2018 Yiou Greater Health Innovators Conference Ushers in a New Era of Medical Entrepreneurship

On November 30, the 2018 Yiou Big Health Innovators Annual Conference, hosted by Yiou, was successfully held at the China World Hotel in Beijing. The summit centered on topics such as consumer-grade genetic testing, pharmaceutical retail, medical aesthetics and health checkups, optometry and vision care, and dental healthcare, bringing together industry professionals to discuss the future trajectory of the big health industry amid new policies and opportunities.

In addition to entrepreneurial leaders such as Yu Rong, Chairman of Meinian Onehealth; Li Bin, Chairman of United Beauty Group; Pan Zhongying, Vice President of United Family Healthcare; Wang Zhimin, Chairman of Xingchuang Vision; Kang Kai, CEO of Kangfu Home; Song Dawei, Partner and COO of Meivie Dental Care; and Chen Gang, CEO of WeGene, the summit was also attended by prominent healthcare investors, including Fang Xianyun, Partner at Chengcun Capital, and Sun Chao, Founding Partner at Chongshan Capital.

Furthermore, at this annual conference, YiOu also prominently released the “2018 Consumer-Grade Genetic Testing Market Research Report,” providing an analysis of DTC market trends.

Those Health-Tech “Innovators” Who Dare to Explore Emerging Trends

With the advancement of the times, as well as shifts in societal needs and the disease spectrum, the concept of “Big Health” is gradually gaining social acceptance. The policy orientation set by “Healthy China 2030” has directly driven the continuous expansion of a trillion-yuan market. Furthermore, the “Several Opinions on Promoting the Development of the Health Service Industry” have also provided clear direction for the Big Health industry.

In niche sectors such as tech-enabled living and health management, innovators continue to emerge. On November 29, YiOu proudly released the “Top 20 Most Innovative Companies in China’s Big Health Industry 2018,” featuring 20 companies from diverse fields including AI-powered big health, internet healthcare, pharmaceutical e-commerce, health management, and new-type clinics. This list demonstrates that the big health industry’s ability to buck the trend during the “capital winter” stems from companies’ clear positioning and sustained innovation capabilities.

When it comes to innovation, the digital transformation of Star Vision serves as a prime example. Wang Zhimin, Chairman of Star Vision, believes that the essence of the eyewear industry lies in optometric healthcare services. As the gateway for 70% of human information intake, integrating eye care with overall health aligns with the industry’s fundamental purpose. By collaborating with healthcare enterprises such as Chunyu Doctor and Airdoc, Star Vision’s optical retail stores have successfully expanded their scope from traditional eyewear dispensing to preliminary screening and initial diagnosis, thereby empowering the broader health and wellness ecosystem.

It is not only Star Vision that has fully leveraged digital assistants. In his keynote speech titled “The Next Outlet for Pharmaceutical and Healthcare Retail: New Retail 3.0,” Kang Kai, CEO of Kangfu Zhijia (Rehabilitation Home), emphasized the need to carry out a reconstruction of “people,” “goods,” and “scenes” underpinned by data-driven operational capabilities. “The capability to digitize business operations and the capability for data-driven operations are two distinct competencies. The former serves as the foundation, while the latter represents its application. Without the former, the latter cannot be discussed; without the latter, the former holds no meaningful value,” said Kang Kai.

Undoubtedly, the integration of technology is reshaping the broader healthcare industry. Innovators such as Union Beauty and Meiwei Dental Care have also championed the banner of “new business models.” In recent years, Union Beauty has gradually expanded its network of novel medical aesthetic institutions across China. Li Bin, Chairman of Union Beauty, believes that new-type medical aesthetic institutions must be supported by four pillars: a symbiotic philosophy, customer value orientation, breakthroughs in medical technology, and matrix management. Similarly, Meiwei Dental Care has introduced the “business partner” model, delivering outputs across three dimensions—strategic investment, standardization, and brand management—thereby accelerating the development of the “third business model” in oral health management.

Policy initiatives have not only spurred the emergence of new market segments but also enabled traditional sectors such as health checkups and private hospitals to flourish. Yu Rong, Chairman of Meinian Onehealth, stated in his keynote speech titled “The Super Ecosystem of the Medical and Health Industry” that health checkup services must keep pace with the times, and extending into upstream and downstream segments of the industrial chain is a major trend in the broader health industry. Pan Zhongying, Vice President of United Family Healthcare (UFH), hailed as “the pioneer of foreign-invested hospital management in China,” also shared on-site how UFH has leveraged favorable policies and innovative models to steadily build its high-end medical healthcare business.

H2 2018: How Is AI in Healthcare Faring?

As we entered 2018, with the gradual maturation of AI technology, the broader healthcare industry also began to move towards intelligent development. The "2018 White Paper on Medical Artificial Intelligence Technology and Applications" pointed out that the application of AI-assisted diagnostic technology can significantly improve the work efficiency of medical institutions and doctors. Perhaps because AI technology differs from the disruption and empowerment brought by "Internet+", many AI healthcare projects gained public attention in 2018.

EO Intelligence’s Healthcare Division previously noted in the first half of this year that 35 AI healthcare companies have clustered in the field of assisted diagnosis, highlighting the market potential of this sector. In terms of business data, China’s medical imaging data is growing at an annual rate of approximately 30%, far outpacing the annual growth rate of radiologists, which remains around only 4.1%. This gap has undoubtedly further stimulated the application of AI in fields such as medical imaging.

However, in the second half of 2018, many AI healthcare projects disappeared from public view. Part of the reason is that AI medical models require large-scale data training, but on the other hand, data sampling standards across many hospitals and other medical institutions are not uniform, leading to poor interoperability and causing many AI devices deployed in hospitals to gather dust.

However, has AI in healthcare truly reached a dead end? Fang Xianyun, Partner at Chengcun Capital, believes that China’s relatively scarce medical resources, coupled with high patient demand and an insufficient supply of medical personnel, have created substantial market demand for AI applications in the healthcare sector. This underlying business logic is sound. For enterprises, accurately defining their role within the healthcare landscape and identifying unmet clinical needs will pave the way for innovative development and breakthroughs.

Furthermore, in the field of AI-assisted diagnosis, obtaining regulatory approval is also key to development. Currently, only Lepu Medical’s AI-ECG Platform has received FDA clearance. Successfully replicating this experience would significantly drive progress across the industry.

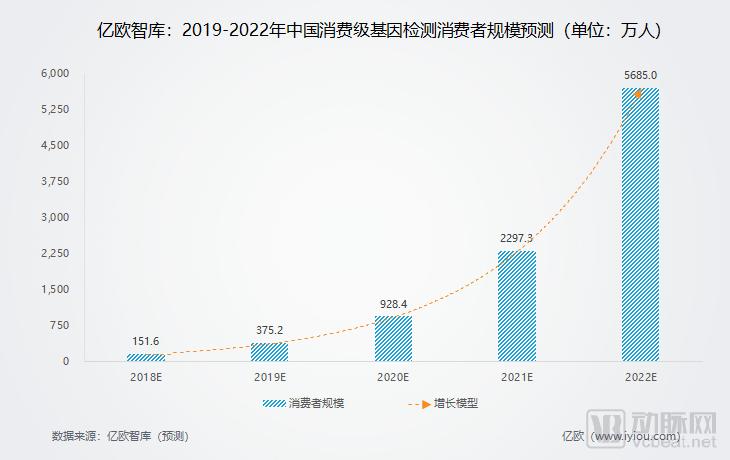

“2018 Consumer-Grade Genetic Testing Market Research Report” Released

Since 2014, the consumer-grade genetic testing industry has seen development, with direct-to-consumer (DTC) genetic testing startups represented by WeGene experiencing rapid growth. However, the industry remains in its early stages, with a total user base of nearly one million, and consumers’ awareness and understanding of genetic testing knowledge and products remain relatively low.

How Can We Promote the More Robust Development of DTC Genetic Testing? In light of this, at this summit, EO Intelligence and WeGene jointly released the “2018 Consumer-Grade Genetic Testing Market Research Report.”

Through research, EO Intelligence has found that online shopping is the mainstream purchasing channel for DTC genetic testing products. However, as an emerging product category, genetic testing still requires attention to offline channels. Establishing product experience stores in high-traffic areas of first- and second-tier cities is a viable option worth considering. Additionally, genetic testing companies can leverage tech products such as smart bands, sports-oriented Bluetooth earphones, and smart speakers to drive customer traffic to their offerings.

VBInsight predicts that China’s consumer-grade genetic testing market will enter a period of rapid and sustained growth over the next five years. The number of consumers is projected to exceed 3.5 million in 2019 and surpass 55 million by 2022, meaning that all core potential consumers and approximately 90% of secondary-tier potential consumers will convert into actual customers.

However, in the face of a vast consumer market, how to avoid the industry falling into a “price war” is a question that genetic testing companies need to consider together. Although price reductions are, to some extent, the result of product scaling and technological advancements, genetic testing products and services must ultimately return to their intrinsic value. In other words, as the incremental market continues to grow, it will eventually compel governments, enterprises, and related institutions to jointly reflect on the position and development direction of genetic testing.