Post-Traffic Dividend: How Health Management Carves a Path to Commercial Monetization — 2018 Annual Review

Health Hope

Health Management Service Provider

Ping An Healthcare

One-stop Solution Provider for Health Management

In 2016, the release of the “Outline of the ‘Healthy China 2030’ Plan” ignited China’s health management sector, as heightened public health awareness spurred the emergence of numerous business models.

In 2017, leading enterprises secured substantial financing, while tech giants, real estate developers, and insurance companies—well-capitalized players from other sectors—crossed over to capture market share. Yet, after a year, health management companies that experienced an influx of capital still faced challenges such as unclear positioning, immature business models, and unchecked, chaotic growth.

In 2018, the health management sector did not witness the rollout of major landmark policies as it had in the previous two years. With rising public health awareness, enterprises began to directly provide health management services to consumers. The fitness industry remained robust, and awareness of preventive medicine continued to gain broader acceptance.

The pre-consultation market for health management, with innovative business models as its primary entry point, remains largely in its early stages, with profitability models still under exploration. As an “imported concept,” health management has followed a distinctly different path in China compared to the United States, undergoing a localization process common to all imported practices. The year 2018 was relatively quiet for the health management sector, with most companies focusing on expanding their business lines and exploring monetization strategies. Over the next three years, what trajectory will health management follow? This article presents the following perspectives:

1. After the First Wave, Health Management Is Seeking Monetization Pathways

2. Beneath the Fog: Who Are Capital’s Favorites?

3. Offline Models Become an Experiment for Service-Oriented Enterprises

4. AI + Health Management: A New Scenario for AI Implementation

5. Health management is poised to become a key resource integrated by payers, ultimately necessitating the establishment of a closed-loop ecosystem.

After Market Education, Health Management Needs to “Drive Business Growth”

A 2017 report by IBM on population health management noted that its survey results indicated that, by the end of this decade, population health management would become the most widely accepted approach in the delivery and management of healthcare services in the United States.

For payers and healthcare providers, the importance of population health management (PHM) continues to grow, as the adoption of new payment models has shifted the focus from volume to healthcare outcomes and value. Although PHM is still in its developmental and maturation stages, it is already undergoing a transformation: placing greater emphasis on pre-disease patients to help them maintain health over longer periods, while simultaneously exploring more effective approaches to chronic disease management.

China's health management industry emerged in 2015. It is generally believed that the development of this sector has been driven by the emergence of various social issues, including the rapid aging of the population, severe natural environmental pollution, a sharp increase in chronic non-communicable diseases, and the excessively rapid growth of medical expenses.

In China, health management generally represents a form of functional medicine, with data monitoring serving as the entry point, and an ecosystem outside the scope of diagnosis and treatment is gradually being established.

Since health management does not involve core diagnostic and treatment processes, the entry barrier is relatively low. Moreover, unlike standardized, protocol-driven clinical services, health management requires tailored plans based on an individual’s physical condition and health goals. With undefined service standards and a lack of regulatory oversight regarding service qualifications, the market continues to experience unregulated, rampant growth.

Zeng Qiang, Director of the Health Management Research Institute at the Chinese People's Liberation Army General Hospital (301 Hospital) and President-Elect of the Health Management Branch of the Chinese Medical Association, once remarked while evaluating the health management industry: “Currently, there are more than 3,000 professional health management companies in China. Many hospital medical examination centers have also transitioned from offering standalone check-ups to providing comprehensive health management services. Meanwhile, numerous social institutions have used health management as a pretext to rake in money, creating a chaotic mix of quality within the industry and causing certain harm to the vital interests of the public.”

Although various business models exist—such as corporate health management, “Internet Plus” health management, health management information systems, and family doctor care—the market still lacks a clear definition of “health management.” Consequently, the wellness and healthcare service sector, which primarily focuses on health preservation and maintenance, continues to appropriate the market concept of “health management.”

Market education used to be a formidable challenge that companies had to strive hard to overcome in the evolution of health management. When interviewed by reporters, Kong Fei, CEO of More Health, remarked with evident satisfaction, “The biggest change now is that no one asks me anymore whether health management is truly an essential need.”

In a market, although enterprises face many competitors, they all reach the same goal by different routes,Market education is the most critical task for all health management enterprises. When prevention replaces treatment as the preferred approach, business models in this sector will be able to identify demand-side customers and generate revenue.

Under the Fog: Who Are Capital’s Darlings?

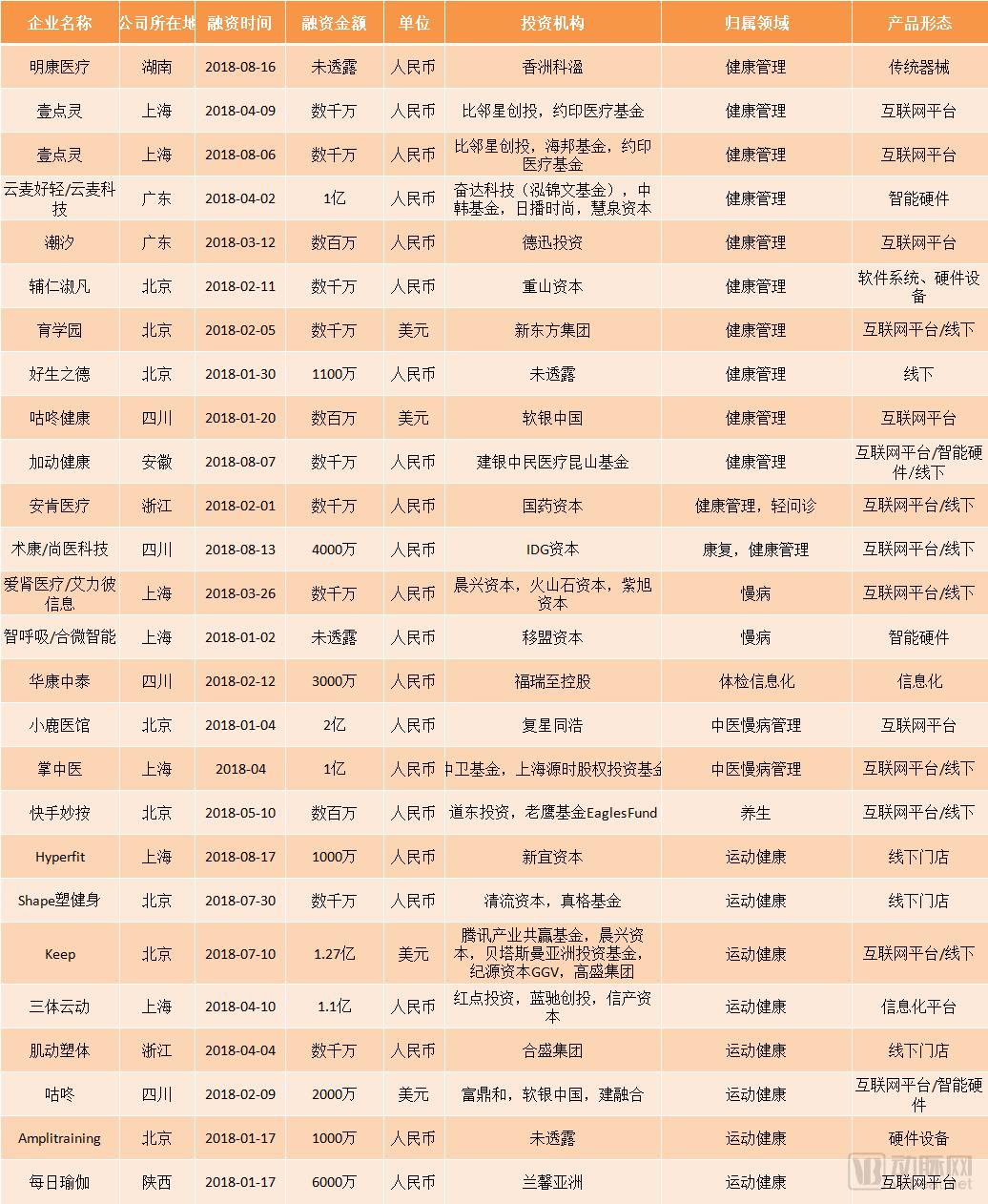

Financing Events in the Health Management Industry as of November 1, 2018; Data Source: VCBeat Database

Looking at the financing situation in the health management industry in 2018 (as of November 1), there were a total of 26 financing events this year, with a total amount exceeding RMB 1.16 billion.In contrast to the fervor seen in the sports and fitness sector last year, health management platforms have staged a resurgence this year, becoming favorite targets for capital investment. Unlike internet healthcare platforms that emphasize medical attributes, internet-based health management platforms focus more on promoting users’ healthy lifestyles. Furthermore, niche health segments such as mental health and sleep have consistently secured a share of financing over the years.

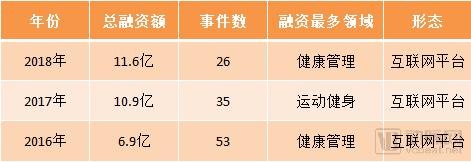

Total Financing Amount and Number of Deals in the Past Three Years, Data Source: VCBeat Database

An analysis of financing over the past three years reveals that while total funding amounts have risen year by year, the number of financing events has declined annually. From VCBeat’s database, which contains over 4,000 records of financing events, we identified companies that secured funding for three consecutive years. These companies not only reflect investor preference but also, to a certain extent, mirror market sentiment.

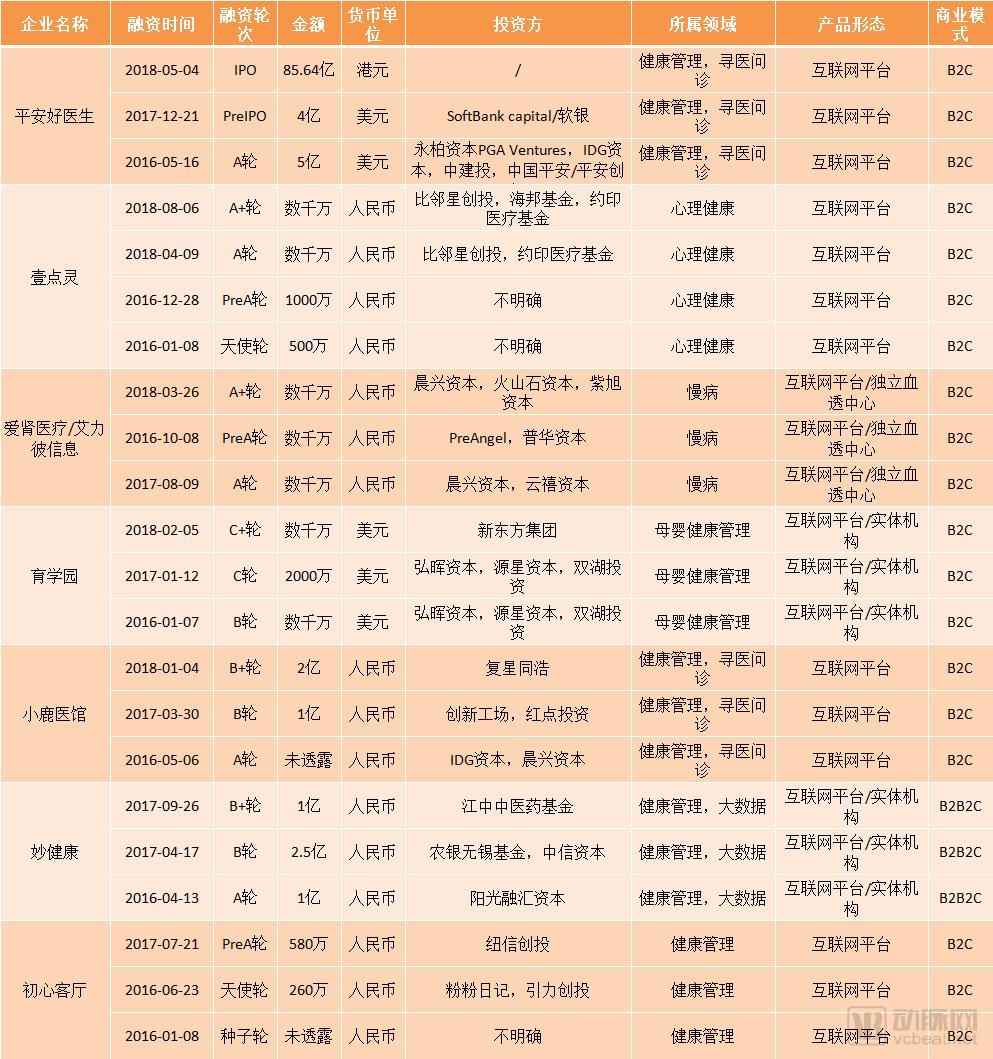

Number of financing rounds since 2016: three or more. Data source: VCBeat database

The seven companies selected above have all secured financing three or more times since 2016,In the capital markets of recent years, internet platform-based enterprises have primarily persuaded investors by highlighting their user base and monetization models, giving rise to numerous industry leaders among innovation-driven companies leveraging the internet.

Among the companies in our statistical data, with the exception of Aishen Medical, which has established physical medical institutions involving hemodialysis, the remaining enterprises primarily provide health management services through online models. Notably, Miao Health began collaborating with the Canadian Health Management Center in 2018 to establish a joint venture dedicated to developing offline health management center operations.

Since 2018, another capital winter has arrived. According to industry insiders, in the fields of chronic disease management and health management, platform-based enterprises need to find ways to increase user stickiness. The costs of acquiring and reactivating a large number of users remain high. It is now more difficult for companies to secure financing simply by presenting “attractive data,” as was common in the previous two years, because investors themselves are facing challenges in raising funds. Therefore,Corporate operations must adhere to the principle that “everything is based on genuine demand,” which also signifies that, as the era of online traffic dividends fades, healthcare services are returning to a trust-based model.

As health management moves offline, services still require medical endorsement.

In discussions on business models, two viewpoints put forward by Zhang Ying, Founding Partner of Matrix Partners China, align closely with the development of the health management industry:

First, commercial monetization methods are becoming increasingly diverse, and commercial monetization is growing in importance. With the emergence of every new entity, particularly those established as commercial enterprises, profitability remains the primary concern for both the market and capital investors.

Second, the era of focusing solely on product development to drive user growth is a thing of the past. All asset-light companies will need to transition toward an asset-heavy model—and indeed must do so. Only by adopting an asset-heavy approach can they effectively deter entry by industry giants, and only in this way can they achieve significant scale.

With this perspective in mind, we find that just as internet healthcare attempted to establish offline entry points last year, health management has also begun to adopt offline models. Essentially, this is closely related to the issue of trust in healthcare.Experiments over the past few years have demonstrated that health management must align more closely with preventive medicine and functional medicine. Consequently, providing medically related services through offline, face-to-face models has become an inevitable trend.

Here, we present examples of offline health management centers in various formats established by several companies involved in health management services.

Different corporate health management centers have different focuses (Data source: public information and VCBeat interviews)

As a leading health management platform in China,More HealthWithin four years of its establishment, it amassed over 50 million users and secured RMB 450 million in substantial financing within the first three years, becoming one of the star projects favored by both investors and users.

Kong Fei stated that Miao Health had three key priorities in 2018:

First, “scale up the business” by exploring commercial monetization strategies, building on the continuous enhancement of product traffic in the past;

Second, leverage offline capabilities in conjunction with internet technologies and the world’s premier health management institution—the Canadian Health Management Center—to genuinely shift the focus of healthcare toward prevention.

Third, leveraging the data connectivity capabilities of the Miao+ platform, we are collaborating with the China Academy of Information and Communications Technology (CAICT) under the Ministry of Industry and Information Technology, as well as the National Center for Chronic and Noncommunicable Disease Control and Prevention, to promote interoperability standards for wearable devices in China. Kong Fei told VCBeat, “If the interoperability standards for wearable devices require completion of the ‘five reviews and five meetings’ approval process, Miao Health has currently passed three reviews and three meetings.”

In preventive healthcare for the general population, the elderly are a high-risk group for chronic diseases and thus have greater need for value-based nursing and health care services, with reference to the United States’Iora HealthHaving established over 22 grassroots chain elderly healthcare institutions across the United States, this model dedicated to providing primary healthcare services for seniors has successfully completed five rounds of financing, totaling $220 million. In a market characterized by homogeneous services, differentiated offerings serve as a rapid pathway to market penetration and brand dissemination.

Jiayou Health Community Chain Health Management ClinicBy deeply empowering the real estate sector, with a foundation built on creating intelligent health communities and providing family-based preventive medical services, "Jia You Jian Kang" (Home Health) features family doctor services and children's health management as its flagship offerings. Adopting an annual service package model, it charges families an annual service fee ranging from RMB 7,000 to RMB 10,000. In the two years since its establishment, Jia You Jian Kang has served over 35,000 property owners, with 1,054 households enrolled as family doctor members. This suggests that shifting the focus of domestic healthcare services more toward the elderly and children is indeed a viable approach.

with a greater emphasis on chronic disease management7+1 Medical CenterIn terms of service delivery, the integration with medical resources is more closely aligned. “Effective Blood Glucose Control” serves as both the slogan and the core principle of 7+1’s services. Since its establishment in 2017, 7+1 has adopted a multi-to-one service model delivered by a professional healthcare team that provides holistic, end-to-end, and comprehensive care. By scientifically formulating personalized blood glucose management plans and ensuring continuous follow-up, it has achieved a 95% effectiveness rate for its glucose control programs. Currently, this service package has been incorporated into Ping An Insurance’s product portfolio, becoming a diabetes insurance product.

Innovative Models in Health Insurance: Data Monitoring-Driven Health Management

At a well-known consulting firmFrost & Sullivan’s Forecast of the Eight Major Trends in Healthcare for 2019In China, forecasts for the health data-driven insurance industry indicate that personalized health insurance, powered by lifestyle and health data, will reshape the health insurance sector.

This November,U.S. Insurance Giant John Hancock Life Insurance Announces Halt to Sales of Traditional Insurance Products, heralding the arrival of an era in which health management has become a standard feature of health insurance. All John Hancock Insurance policies will include the “Vitality Health Insurance Program,” providing customers with fitness devices from Fitbit, Garmin, and Polar. By leveraging health behavior data and health management services, the program incentivizes customers to adopt healthier lifestyles, thereby achieving cost containment.

Undoubtedly, today’s health insurance policies have become outdated and fail to meet individuals’ personalized needs. Therefore, Frost & Sullivan predictsThe growth rate of the health insurance industry in 2018 will be below 1.5%.. To ensure the growth of global insurance profits in the future, many insurance companies have begun to provide data- and digital-driven healthcare services to their policyholders and reduce potential claim costs.

By the end of 2019, 5–10% of health insurance plans will be linked in some form to interactive policies driven by lifestyle and health data.

Frost & Sullivan’s research indicates that interactive policies will continue to gain popularity worldwide, as they enable insurers to leverage personal data for personalized premiums, discounts, and rewards.

Previously, health management may not have been integrated into China’s medical culture, but Frost & Sullivan believes that it will not be long before health management becomes a “health culture.”

Domestic startups such as Miao Health and 7+1 Medical Center, as mentioned earlier, are collaborating with insurance companies to provide data support for the development of personalized insurance products based on collected health data.

AI+Health Management: A New Business Model Becomes Another Avenue for AI Implementation

On the other hand, in the realm of disease prediction and risk early warning, AI, combined with cutting-edge technologies such as health big data and wearable devices, has become a primary driver within the health management ecosystem, giving rise to new business models like “AI + Health Management.” Consequently, health management has emerged as one of the four major product lines for artificial intelligence, alongside medical imaging, clinical literature analysis, and virtual assistants.

As the first technology enterprise in China to build an open AI technology platform in the vertical field of healthcare,Health HopeFounder Li Yuxin believes that the industry's pain points can be categorized into two aspects: one at the product level and the other at the technological level.

First, at the product level. The industry is widely characterized by overly dispersed and fragmented products and services, making it difficult for consumers to identify and select those that best suit their needs. Therefore, Health Hope is currently integrating resources at the application layer. “The industry requires further consolidation, which is precisely what Health Hope is undertaking, and this also serves as the foundation of its business model.”

Secondly, at the technical level. Technology needs to be integrated with specific scenarios; however, the industry currently focuses primarily on technology output, with insufficient research into scenario-specific requirements. As AI is a general-purpose technology, addressing diverse scenarios requires the development of skill modules tailored to specific needs, such as food recognition, posture recognition, and assisted diagnosis and treatment. Therefore, Health Hope’s launch of the open healthcare AI platform, Health AI, represents an achievement in technical integration.

Meanwhile, Li Yuxin stated that the industry currently struggles to effectively bridge the gap between the technical and application layers. The level of intelligence in current scenarios is relatively low, and entry points are overly fragmented, making integration a significant challenge. However, Health Hope has developed targeted solutions to seamlessly connect scenarios with technology, such as comprehensive health management solutions for smart elderly care, smart communities, and smart homes.

Currently, Health Hope’s Health AI platform has integrated with open platforms such as Baidu, iFlytek, JD.com, and Xiaomi, filling technological gaps in the healthcare sector for these platforms. It also provides skill integration for more than a dozen mainstream smartphones from Huawei, OPPO, vivo, and other brands, as well as various smart terminals. In sectors including senior living real estate, smart communities, and traditional chain operations, Health Hope has implemented comprehensive solutions encompassing skill development, service robots, physical services, and offline centers. Its deployed smart elderly care projects have become benchmark senior living communities in first-tier cities.

In terms of business model, Health Hope adheres to a platform strategy to empower B-side enterprises. Specifically, it provides upstream companies with software and hardware enablement, management systems, and scenario-based solutions, helping them rapidly enhance the experience and efficiency of their products and services. Additionally, it integrates downstream companies’ products and services into its overall solutions.

Additionally, Li Yuxin revealed that, supported by AI technology, commercial implementation has been progressing well. Health Hope has already partnered with nearly 100 companies, including industry giants and unicorns. The company is set to announce a new round of financing by the end of the year, which is expected to exceed RMB 100 million.

Originating in Enterprise Services, Health Management Ultimately Needs to Form a "Closed Loop"

Observations of foreign health management enterprises also reveal that many such companies initially grew by providing corporate health management services. Employee health benefits have emerged as a new frontier in healthcare and serve as the primary revenue source for these firms, ultimately evolving into an HMO model that integrates medical health services with insurance coverage. Prominent examples include Kaiser Permanente and UnitedHealth Group.

From abroadOscar Health、Clover HealthJudging from the business models of unicorns, the health management industry is likely to be consolidated by the payers. Driven by large insurance companies—such as domestic enterprises like Ping An and Taikang—these insurers face weaknesses in hospital and physician channels. Consequently, their next strategic step involves the large-scale integration of medical resources.

Leading international health insurance companies exhibit three key characteristics in health management:

First, segment customer groups to provide targeted services.Foreign insurance companies typically classify customers by risk level, identify the distinct health needs of specific subgroups, and then provide targeted, appropriate health management programs.

Second, it provides closed-loop health management.Establish a closed-loop health management system through data collection, data analysis, health interventions, and evaluation feedback; actively leverage innovative technologies such as implantable medical devices, mobile health, big data analytics, and cloud computing to optimize key components within the closed loop.

3. Establish a health management ecosystem.Foreign insurance companies are increasingly engaging in collaborations with technology innovation firms, medical technology enterprises, pharmaceutical companies, healthcare institutions, and health consumer businesses through equity investments, mergers and acquisitions, and joint ventures, thereby establishing an ecosystem for health management services.

Therefore, a large number of health service providers, particularly those offering data-proven “effective” health management or chronic disease management services, are likely to be incorporated into insurance coverage. The rationale stems from the ultimate objective of health management—namely, cost containment. With the development and widespread adoption of health insurance, especially technology-driven insurance products, leveraging health management for cost control has become a key strategy for insurers to achieve their business interests.

In areas such as chronic disease management and sub-health management, it is particularly essential to build a closed-loop health management system targeting individuals with chronic conditions or sub-health status by fostering stickiness within specific diseases or population groups. In this process, human-centric services are indispensable and cannot be replaced by internet technologies.

In this ecosystem, services constitute a critical component. The core of the health management model is to build a human-centric, closed-loop ecosystem that encompasses “insurance + hospitals + internet healthcare” and “prevention + treatment + rehabilitation,” requiring collaboration and resource sharing among multiple institutions and across various stages.

While it is most likely that large health insurance companies will drive this trend in the United States, given the current situation in China, it is also plausible for pharmaceutical companies to become the payers of health services. By doing so, they can achieve patient management and carve out their own development path through the integration of upstream and downstream resources.