Only Two Multinational Pharma Companies Among 31 Winners in China's '4+7' Volume-Based Procurement Preliminary Results

According to VCBeat (WeChat ID: vcbeat), the preliminary winning bid results for the “4+7” volume-based procurement were announced as scheduled on December 6, with only one company selected as the winner for each of the 31 procured drug varieties.

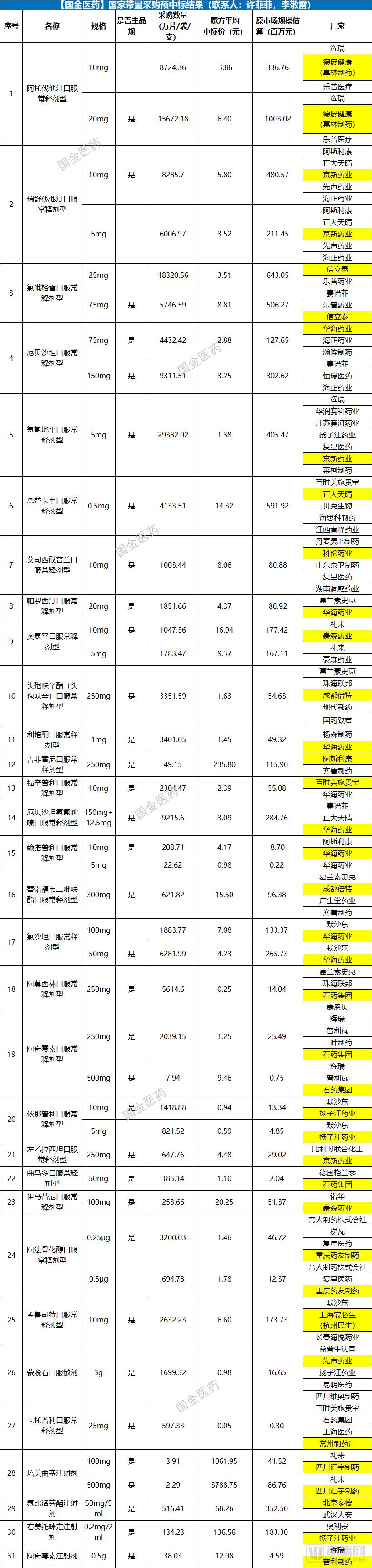

Preliminary Selection Results of Volume-Based Procurement:

Source: Guojin Securities

In terms of bidding rules, a "volume-price linkage" approach is adopted. First, provisionally selected products are determined; once the provisionally selected enterprises and products are identified, they uniformly enter the price negotiation and confirmation process.

The main content of this article is:

1. Origins, Rules, and Impact of the Volume-Based Procurement Policy;

2. Generic drugs replace originator drugs, with priority evaluators benefiting;

3. The pharmaceutical industry is undergoing accelerated consolidation, with enhancing innovation capability being the key.

Volume-based procurement or Group Purchasing Organizations (GPOs) are not new concepts in China. As early as July 2017, Guangzhou and Hubei Province successively expressed their intent to pilot the GPO procurement model in government documents. Even earlier, Shanghai and Shenzhen had already begun exploring the implementation of volume-based procurement.

Discussions on this round of volume-based procurement began on November 15, when the “Document for Centralized Drug Procurement in ‘4+7’ Cities” (hereinafter referred to as the “‘4+7’ Document”) was officially released. The national government organized a pilot program for centralized drug procurement in 11 cities: Beijing, Tianjin, Shanghai, Chongqing, Shenyang, Dalian, Xiamen, Guangzhou, Shenzhen, Chengdu, and Xi’an.

The “4+7 Document” specified the drug varieties and volumes for centralized procurement, enterprise eligibility criteria for bidding, and the procurement cycle. Subsequently, the Shanghai Medical Centralized Bidding and Procurement Administration Office issued the “Supplementary Document on Centralized Drug Procurement in the 4+7 Cities—Shanghai Region,” which established regulations on enterprise bidding, drug distribution, quality monitoring, and payment for goods.

On November 26, Bozhou, Anhui Province, released a work plan for the centralized volume-based procurement of drugs by public medical institutions, becoming the second city in China to announce detailed rules for volume-based procurement. Notably, Bozhou is not among the “4+7” pilot cities. Its adoption of this approach suggests that the volume-based procurement model may be rolled out nationwide.

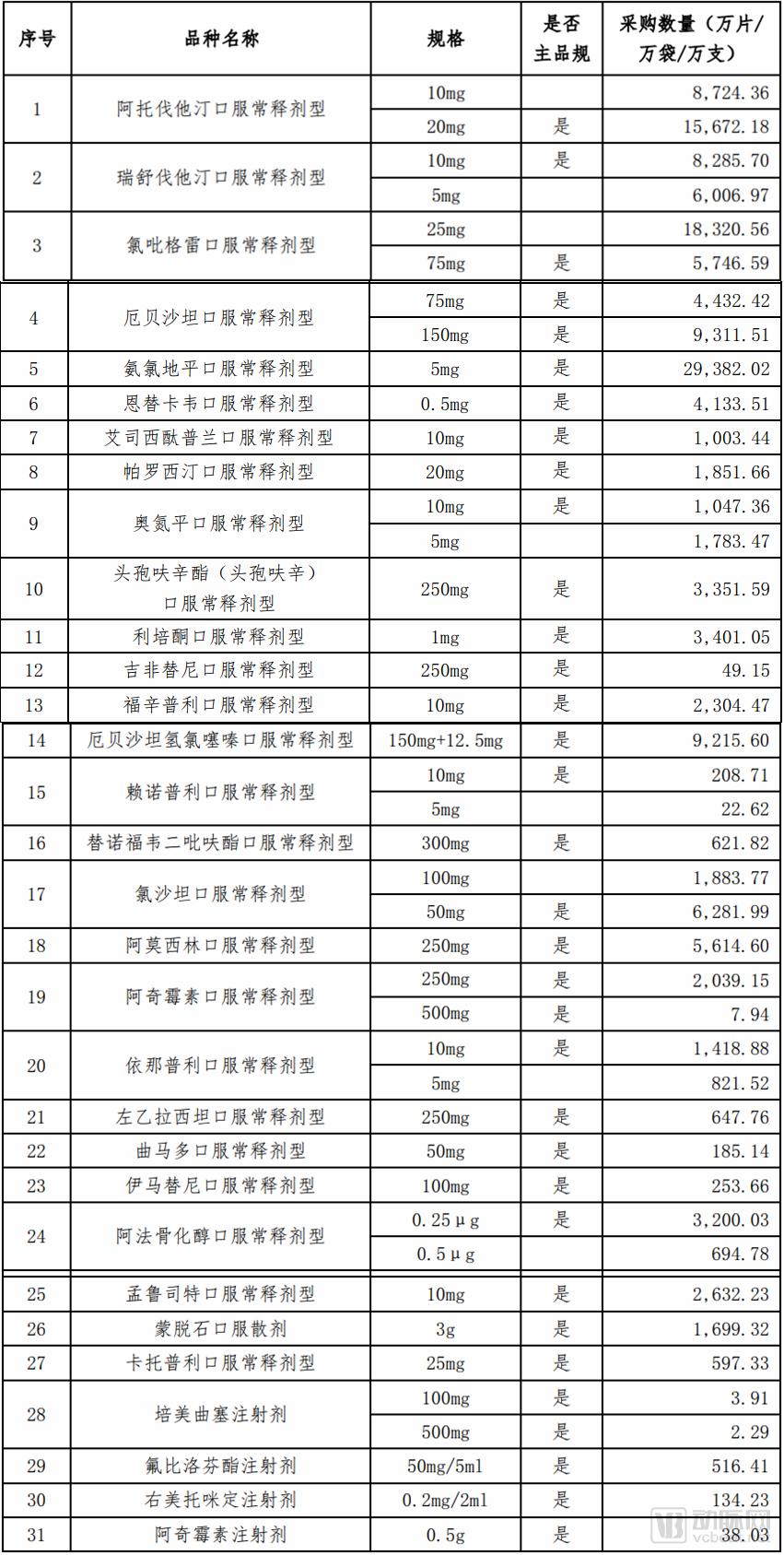

The “4+7 Document” covers 31 drug varieties, which are basically commonly used medications. Based on the previous national winning bid prices, the procurement amount is approximately RMB 7 billion.

Volume-Based Procurement Items and Procurement Volumes

Data source: 4+7 document

Regarding the procurement schedule, this centralized procurement adopts a 12-month procurement cycle starting from the date of implementation of the results. If the agreed procurement volume is completed ahead of schedule within the procurement cycle, any excess quantity shall still be procured at the selected bid price until the expiration of the procurement cycle.

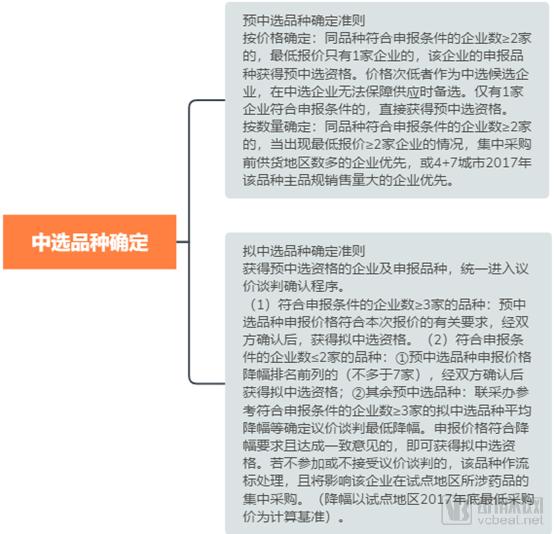

Regarding the bid-winning rules, a “volume-price linkage” approach is adopted. First, the provisionally selected products are determined; once the provisionally selected enterprises and products are identified, they uniformly enter the price negotiation and confirmation process.

Rules for Determining Selected Products

Data Source: 4+7 Document

Among enterprises meeting the filing requirements, 17 product specifications had three or more eligible companies, and 23 product specifications had two eligible companies, indicating relatively intense competition. (A single drug product may have multiple product specifications.)

Regarding the impact of “bidding,” Shanghai Securities Research Institute holds that: 1) For varieties with large market sizes and high market shares held by originator companies, such as atorvastatin calcium tablets, considering the principle of awarding bids to the lowest prices in this volume-based procurement, coupled with factors such as the potential further spread of declared prices to other regions across China, originator companies may forgo price reductions and participation in the volume-based procurement in order to preserve their profits in the national market;

2) For varieties with small market sizes and low procurement volumes, such as azithromycin injection, the profit margin for originator companies to reduce prices and be included in volume-based procurement is limited, which may lead them to abandon these niche products;

3) For generic drug products that have passed the consistency evaluation and are exclusively manufactured by a single generic company, the generic manufacturer only needs to compete with the originator. Considering factors such as low-price bidding and the generally higher prices of originator drugs compared to generics, generic manufacturers tend to offer smaller price reductions than originators at similar price levels, thereby gaining a certain competitive advantage;

4) For products with intense market competition, such as amlodipine besylate tablets, montmorillonite powder, and cefuroxime axetil tablets, generic drug manufacturers with low market share exhibit lower price sensitivity compared to originator pharmaceutical companies. Exchanging price for volume not only enables generic drug manufacturers to rapidly capture market share but also facilitates cost savings for medical insurance funds.

A key prerequisite for participating in volume-based procurement (VBP) bidding is passing the consistency evaluation. As indicated in the “4+7 Document,” there are numerous policy incentives for products that have passed this evaluation. First, no distinction is made between originator and generic drugs, with encouragement given to substituting generics for originators, which helps alleviate the financial pressure of high-priced originator drugs on medical insurance funds.

Secondly, price reductions are inevitable for all drug categories. For generic drugs, winning the bid in centralized procurement may be the optimal strategy; those that fail to win must compete with originator drugs and other generics in the remaining 30%–40% of the market outside the centralized procurement system.

In the future, an increasing number of drug products will pass the consistency evaluation, the scope of volume-based procurement (VBP) will continue to expand, and those failing to meet the consistency standards will be directly eliminated. For originator drugs, current market share, procurement volume, and confidence in the market will determine whether price reductions are implemented.

The final winning bid prices from this centralized procurement are highly likely to serve as the basis for establishing medical insurance payment standards. These payment standards will fundamentally alter physicians’ prescribing incentives, transforming healthcare institutions into a force that drives down drug prices, thereby triggering deep-seated structural changes across the entire pharmaceutical market, particularly in the generics sector.

Therapeutic products with high quality and effectively controlled costs will enjoy long-term benefits in the future. In addition, the consistency evaluation will compel domestic pharmaceutical companies to select high-quality excipients, while volume-based procurement will drive the realization of performance for excipient manufacturers. Leading enterprises in oral formulation excipients will benefit with certainty.

Conducting consistency evaluations for generic drugs that have already been approved and marketed is a remedial measure to address historical gaps. In the past, there was no mandatory requirement for consistency evaluation against originator drugs for medications approved in China, leading to discrepancies in efficacy between some generics and their originator counterparts. Historically, countries such as the United States and Japan have undergone similar processes; Japan, for instance, spent over a decade advancing the consistency evaluation of generic drugs.

Conducting consistency evaluations for generic drugs ensures that they match originator drugs in quality and efficacy, allowing them to serve as clinical substitutes. This not only reduces medical costs but also enhances the quality of generic drugs and the overall development level of China’s pharmaceutical industry, thereby ensuring safe and effective medication for the public. In China, the consistency evaluation of generic drugs represents both a remedial measure and an innovation. By achieving parity with originator drugs in quality and efficacy, we are moving closer to the independent development of new drugs.

The National Medical Products Administration’s interpretive document posits that consistency evaluation is a matter of survival for pharmaceutical companies, representing a process of natural selection where the number of approval documents held is irrelevant; only products whose quality and therapeutic efficacy are consistent with those of the originator drugs possess market value. Companies should select products with a high likelihood of success, conduct robust foundational research on crystal forms, excipients, and manufacturing processes, perform in vitro dissolution testing, and then proceed to bioavailability clinical trials to avoid unnecessary detours. By having several products complete consistency evaluation, coupled with the implementation of the Marketing Authorization Holder (MAH) system, a company can gain a competitive advantage.

China faces severe overcapacity in pharmaceutical production, with an excessive number of enterprises; it is therefore not surprising that some companies fail to pass the consistency evaluation. Pharmaceutical companies that have passed the consistency evaluation can act as Marketing Authorization Holders (MAHs) and commission other enterprises to manufacture their products. Companies that have not passed the evaluation can leverage their respective advantages to engage in contract manufacturing. The key lies in enterprises accurately identifying their strategic positioning.

Certainly, the consistency evaluation is also an important strategy for companies to capture market share. Currently, multiple local governments have successively introduced policies related to tender procurement and pricing for products that have passed the consistency evaluation. These policies mainly include priority procurement and use by medical institutions, as well as support in terms of medical insurance payment. Among them, from August to November 2018, some regions issued documents to further implement the rule that "once three manufacturers of the same product pass the consistency evaluation, the online procurement eligibility of manufacturers that have not passed will be suspended."

According to research reports from the Shanghai Stock Exchange, there are currently 109 approval numbers that have passed the consistency evaluation (including those deemed equivalent), of which 78 have passed the consistency evaluation and 31 are generic drugs approved under the new registration classification for chemical drugs. In terms of product specifications, five specifications have been approved for consistency evaluation by three or more enterprises, 13 specifications by two enterprises, and 65 specifications by one enterprise.

As the quality of generic drugs improves, achieving clinical interchangeability with originator drugs will drive structural reforms in pharmaceutical manufacturing. This shift will alter the current situation where originator drugs account for up to 80% of pharmaceutical sales in some large hospitals, help reduce overall healthcare expenditures, facilitate the elimination of outdated production capacity, and enhance the competitiveness of generic drugs. Furthermore, conducting consistency evaluations of generic drugs encourages innovation among pharmaceutical enterprises. Since drug formulations are an integrated combination of active ingredients, excipients, and packaging materials, consistency evaluations will prompt companies to conduct more comprehensive research on manufacturing processes, excipients, and packaging materials, thereby comprehensively improving formulation standards.

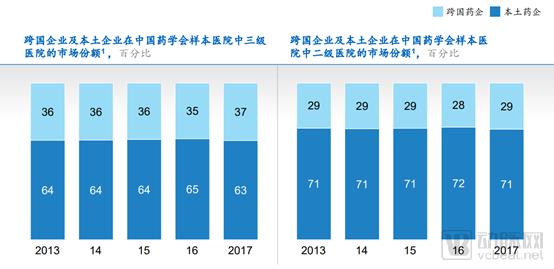

“Overview of the Chinese Hospital Pharmaceutical Market” shows that the market sales share of multinational enterprises in hospitals at all levels and cities has been slowly declining since 2013, but rebounded in 2017, indicating that the investments made by multinational enterprises in recent years to expand market coverage and launch new drugs are beginning to pay off. In 2017, the market sales share of multinational enterprises in tertiary hospitals (37%) was higher than that in secondary hospitals (29%).

Market Share of Multinational and Domestic Pharmaceutical Companies in Tiered Hospitals

Source: Chinese Pharmaceutical Association; McKinsey analysis

The rapid growth in market share of multinational pharmaceutical companies is directly related to reforms in the review and approval system and accelerated medical insurance negotiations. Statistical data show that since the second half of 2017, imports of more than 40 original new drugs have been approved, while five domestically produced Class 1 new drugs have also gained marketing approval.

The pace at which innovative drugs are included in the National Reimbursement Drug List (NRDL) is also accelerating. Recently, the Shenzhen Human Resources and Social Security Bureau published a list of proposed additions to its local reimbursement catalog, with blockbuster anticancer drugs launched in 2018—such as Keytruda (pembrolizumab), alectinib, and olaparib—expected to be included. Gilead’s sofosbuvir/velpatasvir has been added to the National Essential Medicines List, while several other products, including osimertinib mesylate tablets, have gained NRDL coverage through national price negotiations.

Data Source: Shenzhen Municipal Human Resources and Social Security Bureau

As the consistency evaluation progresses and volume-based procurement is launched, the accelerated review and approval of new drugs will shape a pharmaceutical market landscape that places equal emphasis on innovative drugs and high-quality generic drugs.

Innovative drugs are accelerating their market entry and gaining reimbursement support. Price reductions for off-patent branded drugs are inevitable, allowing the competitive advantages of domestic enterprises to gradually emerge. As first-to-file generics become a key strategic target, the era of cutthroat competition in the generic drug sector is unsustainable, and the market will rapidly consolidate among a select few high-quality companies.

With the introduction of medical insurance payment prices, drug prices will decline through market forces. In the future, the expenditure structure of medical insurance funds will shift: the proportion allocated to pharmaceuticals will decrease, while that for medical services will increase. Within pharmaceutical spending under medical insurance, the share of high-quality generic drugs will rise, while the consumption of funds by high-priced off-patent drugs and adjuvant therapies will be compressed, thereby freeing up payment capacity for innovative drugs and medical services.

Furthermore, the demand for high-quality innovative drugs, branded pharmaceuticals, and premium medical services will drive the rapid growth of commercial health insurance, while simultaneously spurring the swift development of PBM (Pharmacy Benefit Management) and DTP (Direct-to-Patient) pharmacy models.

From the perspective of innovative drug investment, a significant current challenge is the duplication of product pipelines. For instance, in the PD-1 sector, numerous companies—including Hengrui Medicine, Junshi Biosciences, Innovent Biologics, and BeiGene—are actively establishing their presence. From the standpoint of medical insurance reimbursement, the availability of multiple companies’ products for the same indication inevitably leads to a certain degree of “price war.” This situation prolongs the payback period and increases uncertainty for capital returns, which in turn affects investors’ assessment of the innovative drug sector.

Volume-based procurement will also impact distribution enterprises. Taking Shanghai’s supplementary documents as an example, each winning bid product must be distributed by only one designated pharmaceutical distribution enterprise, with a distribution fee rate set at 6% of the winning bid price. The designated distribution enterprise must have covered all districts in the city within its drug distribution scope in 2017 and possess the capability and conditions to deliver winning bid products to all medical institutions designated for medical insurance across the city within 24 hours. Distribution enterprises are prohibited from purchasing winning bid products through third parties. These requirements favor leading circulation enterprises with comprehensive distribution networks. Meanwhile, some small-scale distribution enterprises will lose market share, accelerating mergers and acquisitions within the distribution sector.