Gene Sector Secures $986 Million in Funding, Matching Last Year—Gene Therapy Wave on the Horizon [2018 Annual Review]

In 2018, the world was undergoing a severe capital winter. Difficulty in fundraising and financing, along with shrinking valuations, were the most profound experiences for many investors and entrepreneurs. Nevertheless, despite these challenging times, the genomics sector still achieved a high financing volume of approximately $986 million, remaining largely flat compared to the $1 billion raised in 2017.

Over the past year, the NMPA approved the first NGS-based cancer diagnostic kit, granting Burning Rock Biotech China’s “first NGS cancer test certification”; during this period, prices for consumer-grade genetic sequencing dropped again, ushering in an era where consumer products entered the “100-yuan range”; meanwhile, gene therapy sparked an investment boom...

As per tradition, VCBeat has compiled a review of the gene industry based on 2018 investment and financing data, major events, and policies. The difference this year is that we have incorporated some international data.

Data as of November 3, 2018

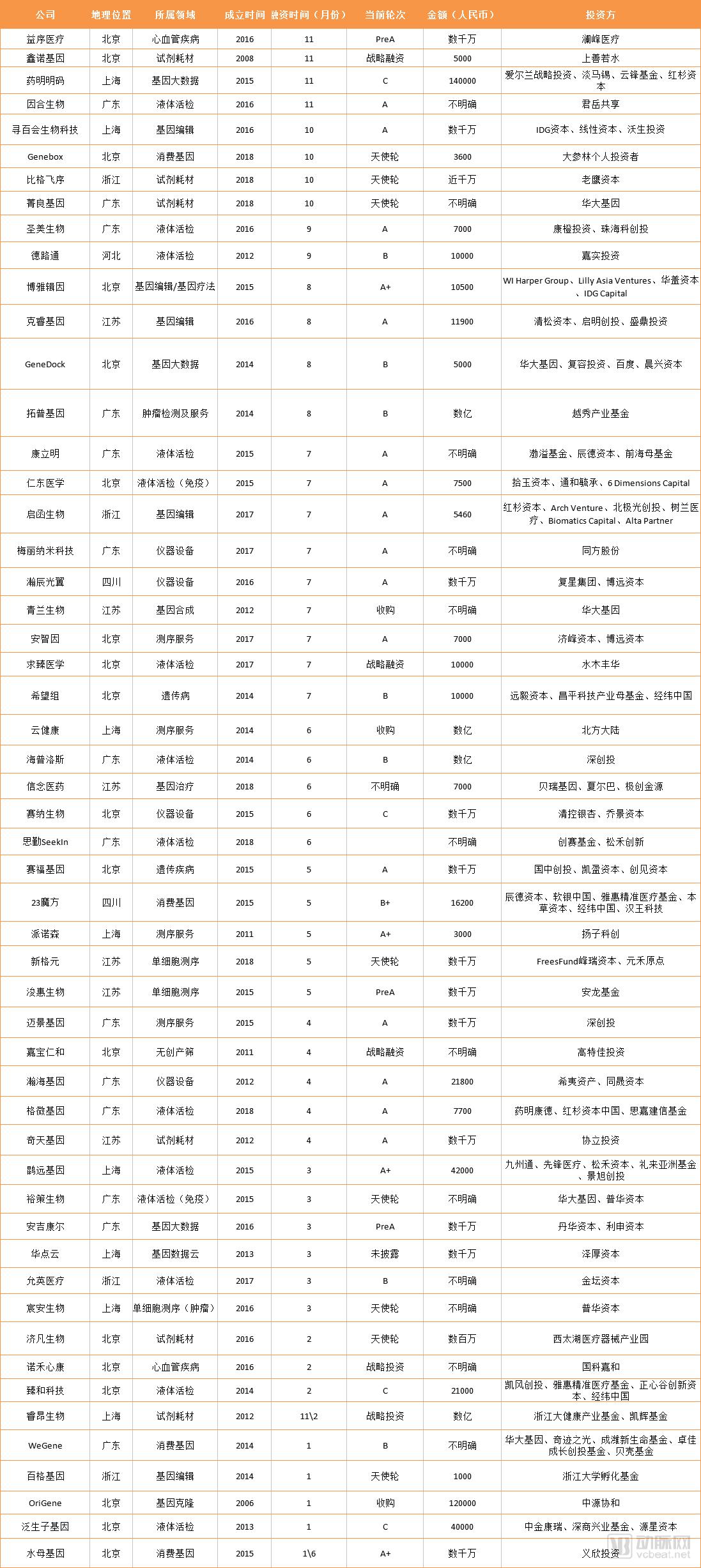

In 2018, total financing in the genomics sector amounted to approximately $986 million, remaining largely flat compared with 2017. Among the 53 companies that secured funding, the average deal size was $24.0404 million. Amid a capital winter, investment firms faced relatively greater difficulties in raising funds and therefore allocated capital more cautiously, favoring industry leaders with technological advantages and more stable growth trajectories.

Note: "Several million" is calculated as 3 million, "tens of millions" as 30 million, and "hundreds of millions" as 100 million; the same applies below.

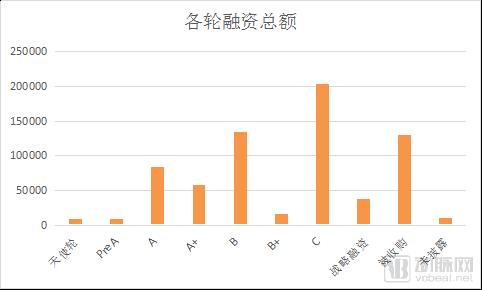

The data reveals that 51.26% of invested capital went to companies at Series B and beyond. These enterprises have entered the mid-to-late stages of development, characterized by relative stability. Naturally, these companies command substantial valuations.

These companies account for the majority of financing deals exceeding RMB 100 million. Of course, a small number of companies at Series A and Series A+ stages have also secured substantial funding; even during a capital winter, strong technologies remain worth investing in.

Of the $986 million in total transaction value, more than RMB 1.3 billion came from M&A deals. Among these, Yunjiankang Gene and OriGene were acquired by Northern Continent Group and Vcanbio Cell & Gene Engineering Corp., respectively, with transaction amounts of several hundred million RMB and RMB 1.2 billion. In addition, Wuxi Qinglan Biotechnology was acquired by BGI Genomics in July 2018, with the transaction amount not yet disclosed.

For most startups, in addition to developing their corporate markets, they also need to consider exit channels for investors. Following the successive IPOs of BGI Genomics and Berry Genomics, many other companies have begun to plan their own paths to going public. However, not all companies will ultimately list on the stock exchange; for some, being acquired by larger corporations is a viable alternative.

2014 and 2015 witnessed a startup boom in the genomics sector, and most of these companies have now reached later-stage financing rounds, such as Series B and Series C. Perhaps the industry is on the verge of a wave of initial public offerings (IPOs) and mergers and acquisitions (M&A).

In 2018, four companies in China engaged in the research, development, and manufacturing of instruments and equipment secured financing, three of which were involved in the development of sequencers. Meili Nano Technology is one of the few domestic manufacturers of nanopore sequencers, utilizing nanopore technology to detect various types of tumor-related biomarkers.

Oxford Nanopore announced in March 2018 that it had raised £100 million (approximately $139 million) in its latest round of financing. Investors participating in this round included the Government of Singapore Investment Corporation (GIC), CCB International (CCBI), the Australian pension fund manager HostPlus, and certain existing shareholders.

SBB: Omniome, an innovative company developing next-generation sequencing platforms, secured $60 million in Series B financing in July 2018. Investors included Cheng Capital, Hillhouse Capital Group, Lam Research Capital, and Nan Fung Life Sciences. Founded in 2013 by Dr. Kandaswamy Vijayan after his departure from Illumina, Omniome aims to develop next-generation sequencing platforms that enhance sequencing throughput while reducing turnaround time and costs.

Notably, a similar pattern is evident in the upstream sequencer sector, where financing disparities between China and other countries are strikingly alike. Chinese companies in this field remain relatively nascent, with their R&D efforts still in the early to mid-stages. In contrast, two sequencer companies that secured financing abroad in 2018 were already highly mature.

The most sensational event in the upstream sector this year was undoubtedly Illumina’s acquisition of Pacific Biosciences. Illumina is a giant in second-generation sequencing, while Pacific Biosciences is a highly representative company in the field of third-generation sequencers. Pacific Biosciences’ third-generation sequencing platform leverages its unique SMRT (Single Molecule Real-Time) technology to analyze individual DNA molecules, enabling high-accuracy decoding of longer DNA fragments. This transaction has further strengthened Illumina’s position, complementing its short-read sequencing technology with Pacific Biosciences’ long-read sequencing capabilities.

In 2018, domestic liquid biopsy companies raised RMB 2.452 billion in financing. This figure fell far short of the $1 billion record set in 2017, partly due to the impact of the capital winter; moreover, several companies had already secured substantial funding rounds in 2017.

Nevertheless, the liquid biopsy sector remains the most heavily funded, with a total of 13 companies.

Influenced by the entry of PD-1/PD-L1 inhibitors into the Chinese market, a wave of immunotherapy companion diagnostics has swept through the liquid biopsy sector. Companies such as Genetron Health, RenDong Medicine, Zhenhe Technology, and Yuce Bio have successively launched immunodiagnostic products. At the 2018 CSCO Annual Meeting in Xiamen, immunotherapy and its companion diagnostics had become a major trend; failing to discuss immunology seemed outdated.

The successive entry of Opdivo and Keytruda into the Chinese market signifies that China has truly entered the era of cancer immunotherapy. However, as is well known, the response rate to immune checkpoint inhibitors is only 20%–30%. Indiscriminate use of these agents not only imposes a financial burden on patients but may also delay appropriate treatment.

“The current situation in China is that the drug has been launched, but the companion diagnostic product has not,” an entrepreneur described.

Not only are there no liquid biopsy products for immune companion diagnostics, but currently, no liquid biopsy-based product has received approval in China. However, since July 2018, the NMPA approved four tumor NGS kits within five months, providing significant encouragement and confidence to the industry.

On July 23, the National Medical Products Administration (NMPA) approved Burnt Rock Medicine’s “Combined Detection Kit for Human EGFR/ALK/BRAF/KRAS Gene Mutations (Reversible Terminator Sequencing Method)” for market launch, making it China’s first approved NGS-based gene detection kit for tumors. In the following five months, the NMPA successively approved tumor NGS gene detection kits from Novogene, Geneseeq, and AmoyDx.

This marks the formal opening of the floodgates by the NMPA for tumor gene detection products based on NGS. Although only small-panel products have been approved so far, the significantly accelerated approval process will greatly promote the clinical application of NGS-based tumor detection products.

Another area of research application for liquid biopsy is early cancer screening, which involves detecting trace amounts of circulating tumor DNA (ctDNA) and circulating tumor cells (CTCs) in blood and exosomes to identify signs of tumors at an early stage.

Methylation sequencing technology has long been regarded as the most promising approach for early cancer screening. Kun Yuan Genomics’ founders, Zhang Kun and Gao Yuan, jointly developed the first large-scale targeted DNA methylation sequencing technology, which was featured as the cover article in Nature Biotechnology. In a 2016 multicenter comparative study on global methylation sequencing published in Nature Biotechnology, Zhang Kun’s methylation sequencing technology ranked first overall. Consequently, Kun Yuan Genomics has consistently been recognized as a leader among domestic and international players in the field of early cancer screening.

In March 2018, Kunyuan Gene completed a $60 million Series A+ financing round, with investors including professional investment firms and strategic industry partners such as Jointown Pharmaceutical Group, Pioneer Medical, Sinowood Capital, Lilly Asia Ventures, and Jingxu Venture Capital.

Yuxun Medical has established China’s only dual-platform liquid biopsy system for both ctDNA and CTC, enabling the simultaneous detection of ctDNA and CTC from a single blood sample. Leveraging this platform, Yuxun Medical delivers a comprehensive cancer precision diagnostics service line encompassing “early screening and diagnosis, personalized treatment guidance, and continuous dynamic monitoring.”

Based on low-coverage whole-genome sequencing (WGS), Yoxun Medicine has developed a cost-effective, pan-cancer CCeS three-dimensional early tumor screening and subtyping method. It is reported that data from the company’s Phase I clinical trial have already demonstrated the superiority and feasibility of using low-coverage WGS for cancer screening. The technology has been protected by domestic and international patents.

In late 2017, Berry Genomics spun off its original oncology division to establish Huirui Gene. In November 2017, the company secured a total of RMB 800 million in investment. Leveraging Berry Genomics’ industrial resources and intellectual property, Huirui Gene rapidly emerged as a promising contender in the oncology field from an exceptionally high starting point.

In April 2018, Huirui Gene invested RMB 100 million and, in collaboration with the National Center for Liver Cancer Science, launched a prospective cohort project involving 10,000 participants. This is currently the largest prospective liver cancer cohort study underway in China, marking a pioneering shift in China’s liver cancer prevention and control efforts into the stages of ultra-early prevention and clinical validation.

“Without ultra-large-scale prospective cohort studies, early diagnosis and screening for cancer would be impossible,” explained Professor Chen Lei from the National Center for Liver Cancer.

Prior to launching large-scale prospective studies, Huirui Genomics had already initiated the preliminary pilot study project, PreCar. The project enrolled 1,500 volunteers, including over 500 patients with hepatocellular carcinoma (HCC) and more than 1,000 individuals from non-tumor high-risk or healthy populations.

In September 2018, Huirui Gene announced the results of its pilot study at the CSCO Congress. The data showed that the sensitivity for liver cancer detection exceeded 90% at a specificity of 95%; even when the specificity threshold was set at 99%, the sensitivity reached 87%.

In addition to Huirui Gene, the U.S.-based early cancer screening company GRAIL launched two large-scale clinical studies in the past two years, namely CCGA and STRIVE. At the American Association for Cancer Research (AACR) annual meeting in April, GRAIL announced preliminary results. By analyzing data from three prototype assays, the GRAIL research team demonstrated that it is feasible to develop a multi-cancer early detection blood test with specificity exceeding 99%.

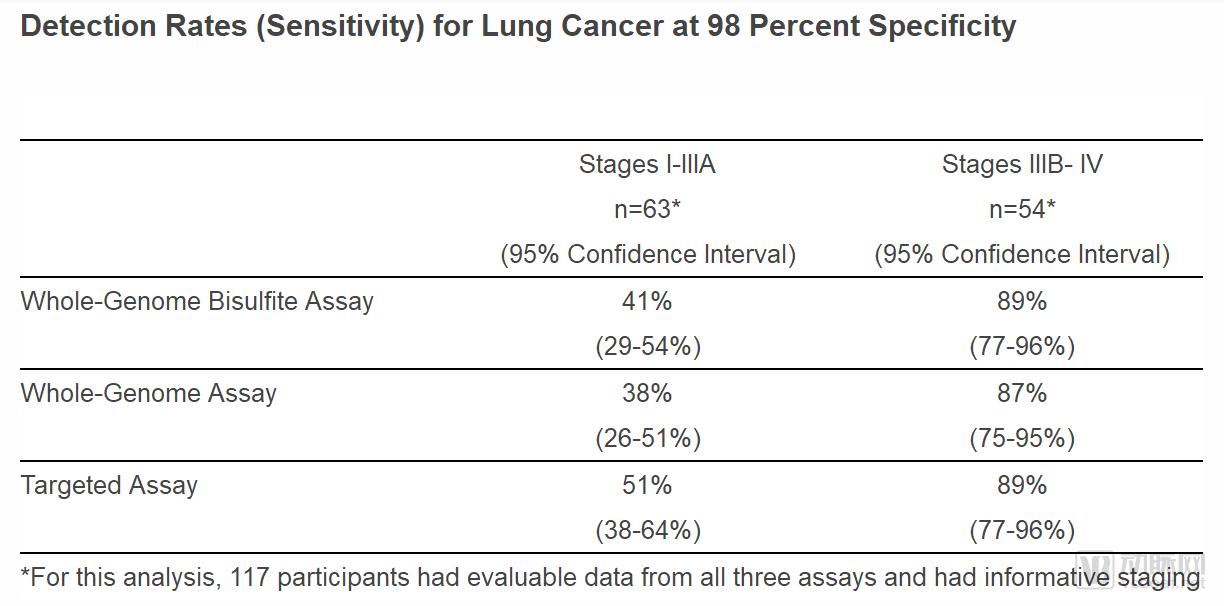

At the ASCO meeting in June of the same year, GRAIL presented the latest results from the CCGA study. This current study enrolled 127 lung cancer patients and employed three detection methods to achieve early cancer screening. These three methods include: targeted sequencing to detect somatic mutations, such as single-nucleotide variants and small insertions and/or deletions; whole-genome sequencing (WGS) to detect changes in somatic gene copy numbers; and whole-genome bisulfite sequencing (WGBS) to detect abnormal cfDNA methylation patterns (epigenetic changes).

The results indicated that the detection rate was 38%–51% (with 98% specificity) in patients with early-stage (Stage I–IIIA) lung cancer, and 87%–89% in patients with advanced-stage (Stage IIIB–IV) lung cancer, as detailed in the table below:

NGS-based early screening products are still some distance away from clinical application, but PCR-based detection technologies have taken the lead in making this step. In November 2018, Kangliming’s independently developed Human SDC2 Gene Methylation Detection Kit (Fluorescent PCR Method) (trade name: “Chang’an Xin”) passed the review by the NMPA and officially obtained a Class III Medical Device Registration Certificate.

Kangliming, positioned as China’s counterpart to Exact Sciences in the United States, is a company specializing in early cancer screening using exosomes. The product recently approved by the NMPA is a colorectal cancer screening test based on fecal DNA, while screening products for other cancer types are currently under development.

2018 was also a landmark year for the development of consumer genomics, with the user base doubling as the average transaction value decreased. According to 23Mofang, its sales volume nearly quadrupled after the product price was reduced to RMB 299.

Over the past year, two leading companies in the consumer genomics sector, 23Mofang and WeGene, have successively completed financing rounds. After completing its Series A and Series B funding in 2017, 23Mofang secured additional Series B+ and B3 rounds in 2018, raising a total of RMB 162 million. WeGene completed its Series B financing in January 2018, with investors including BGI Genomics and Miracle Light, although the specific investment amount was not disclosed.

Genebox, founded in 2018, also secured RMB 36 million in angel-round funding from Dashenlin (as a personal investment). Its founder, Li Zhi, previously served as a Vice President at Warburg Pincus and as a Vice Director at the Hong Kong office of UBS Investment Bank. Targeting young consumers, Genebox places emphasis on internet-based marketing. Additionally, with its network of 3,600 stores and 28 million active users, Dashenlin Pharmacy will leverage its store footprint and membership system as one of its customer acquisition channels.

Based on the moves made by various companies in 2018, downward market penetration is the major future trend in the consumer-grade genetic testing sector.

Jellyfish Genomics completed two rounds of financing in 2018. What sets Jellyfish Genomics apart from other consumer-grade genetic testing companies is its persistent emphasis on empowering health with data and ensuring that data serves the users. In product development, Jellyfish Genomics prioritizes delivering appropriately tailored services through meaningful content, rather than merely pursuing a broad quantity of offerings.

In early 2018, Jellyfish Genes joined forces with Chinese National Geography magazine to launch China’s first “Chinese Surname Genetic Mapping Project” and the “Life Atlas™” product, initiating a journey for Chinese people to trace their roots and explore the familial histories behind different surnames.

“China is different from the United States. The U.S. is a nation of immigrants, whereas China is a relatively homogeneous country dominated by the Han ethnic group. Our ancestors have been rooted here for over 5,000 years, but having undergone multiple episodes of ethnic integration and population migration, mapping these migratory patterns is far more challenging,” said Zhao Nan, Chief Scientist at Jellyfish Gene. “Moreover, China’s history is far more extensive; tracing lineage changes over its 5,000-year span is considerably more complex than studying a single ancestral migration event.”

Another product, “Life Coach,” pioneers the concept in China of “designing healthy lifestyles for users based on applied genetics.” In addition to personal genomic testing, internationally advanced gut microbiota testing, and non-invasive early disease screening, Jellyfish Genetics has assembled a “Life Coach” team comprising professionals from diverse fields such as medicine, exercise science, nutrition, and genetics. This team tailors health knowledge and courses to users’ genetic profiles and precisely recommends products and services best suited to their individual needs.

Certainly, in addition to refining its products, this midstream company in the industrial chain is also actively seeking expansion upstream. In November 2018, Jellyfish Genomics and Thermo Fisher Scientific jointly announced that they had established a “core strategic partnership” and would engage in extensive and in-depth collaboration in the field of genetic testing in the future.

This collaboration marks a new phase in the relationship between the two parties. In addition to introducing Thermo Fisher Scientific’s complete gene chip analysis system, Jellyfish Genomics will also introduce the Ion GeneStudio™ S5 Plus next-generation sequencing platform technology. Jellyfish Genomics will localize this technology through domestic research and development and manufacturing in China, launching the locally produced equipment to clinical testing centers at various medical institutions for in vitro diagnostics in clinical microbiology. By integrating genetic testing data with clinical data, the solution will provide a more comprehensive reflection of the health status of individuals undergoing testing.

Moreover, iCarbonX, a unicorn enterprise, is also engaging in similar explorations. In July 2018, iCarbonX signed a strategic cooperation agreement with the COFCO Nutrition and Health Research Institute to collaborate on research into dynamic blood glucose management and its related applications. Subsequently, the company entered into an agreement with a wholly-owned subsidiary of Dachen Food, establishing a new joint venture named “Better Me.” Leveraging iCarbonX’s technological support and grounded in biotechnology and artificial intelligence, the joint venture customizes and conducts core diagnostic tests tailored to consumers’ needs for precision nutrition. It then generates personalized nutrition analysis reports aligned with individual consumer profiles and provides customized dietary solutions.

Better Me will leverage iCarbonX’s technological support and DACHAN Food’s full-industry-chain advantages in raw material procurement, product R&D, supply chain management, and comprehensive sales channels to transform precision nutrition dining solutions into food products, while conducting online and offline marketing promotions, thereby establishing a closed-loop industrial ecosystem.

In addition to iCarbonX, WeGene has also engaged in collaborations with COFCO Group. Initially, an interactive marketing campaign featuring Honeywell masks provided WeGene with fresh insights. Subsequently, beyond emulating internet companies by selling mooncakes, WeGene’s more significant downstream exploration was the launch of a gene-customized weight management solution in partnership with COFCO Group.

COFCO Group has introduced cutting-edge nutritional science from Harvard and Cambridge Universities, collaborating with experts from renowned domestic and international institutions such as the National Institute for Nutrition and Health of the Chinese Center for Disease Control and Prevention (CDC). By establishing a 16-dimensional model of obesity factors for multi-dimensional assessment and incorporating WeGene genetic testing data, COFCO provides users with customized 14-day lightweight body plans.

The comprehensive solution includes not only WeGene’s sequencing products and the meal replacement combo produced by COFCO Group, but also one-on-one private nutritionist services.

In December 2017, Luxturna (voretigene neparvovec-rzyl), an innovative gene therapy from Spark Therapeutics, a leader in the field of gene therapy, was approved by the U.S. FDA for marketing. It is primarily indicated for the treatment of adult and pediatric patients with specific inherited eye diseases. As the first “direct-administration” gene therapy targeting specific genetic mutations to be approved in the United States, its approval led to 2018 being regarded as the inaugural year of gene therapy.

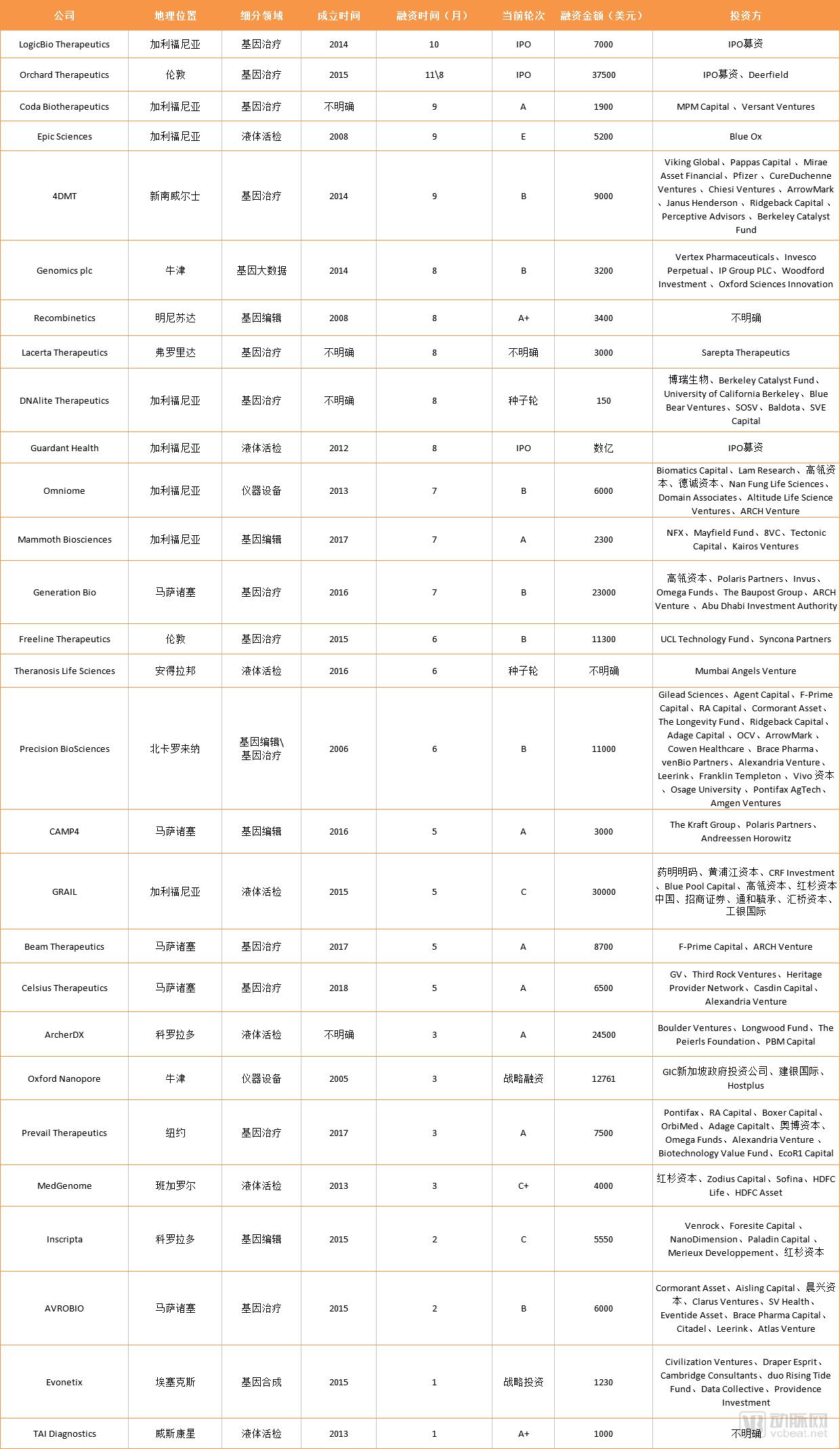

Based on overseas financing data, gene therapy and gene editing are quite hot. Among the 29 companies we counted that received financing, 13 were engaged in gene therapy business, while 5 provided gene editing services. In contrast, only 7 companies in the liquid biopsy sector, which saw frequent financing activities in 2017, secured funding.

In the field of liquid biopsy, Foundation Medicine went public early on and was acquired by Roche in 2018; star company Guardant Health listed on the NASDAQ in 2017; when GRAIL announced its Series C financing, there were also rumors of an impending IPO. In short, foreign liquid biopsy companies, primarily based in the United States, have largely entered the late stage of development, with a wave of IPOs and mergers and acquisitions already underway and relatively low financing frequency; whereas gene therapy is currently the hot sector.

However, in China, liquid biopsy continues to dominate financing activities, with five and two companies securing funding in gene editing and gene therapy, respectively.

Nevertheless, a number of outstanding enterprises have emerged in China. In 2017, the founding team of eGenesis (Luhan Yang and George Church) established Qihan Biotechnology in Hangzhou. As a sister company to eGenesis, the team aims to create a new entrepreneurial innovation model featuring synchronized R&D and mutual resource sharing between China and the United States.

Qihan Bio announced a $7.8 million Series A financing round in July, led by Sequoia Capital China, with participation from ARCH Venture Partners, Northern Light Venture Capital, Shulan Medical Capital, Biomatics Capital Partners, Alta Partners, and others. Moving forward, Qihan Bio will accelerate the development of its gene-editing platform to advance research and development in xenotransplantation.

Wei Wensheng founded Edigene in 2015. In addition to being a researcher at Peking University, he serves as Deputy Director of the Gene Editing Branch of the Chinese Society of Genetics and as an expert on the Center for Drug Evaluation’s (CDE) Expert Committee for Drug Registration Review.

After three years of growth and development, Edigene has accumulated more than ten patented technologies centered on platforms such as gene editing technology, T-cell and stem cell processes, and high-throughput genetic screening. The company has been certified as a National High-Tech Enterprise and received the China Patent Excellence Award. In 2017, Edigene was listed by Nature Biotechnology, a top-tier biotechnology journal, as one of the ten capital-favored, technology-intensive startups. Notably, it was the only Asian company among them.

In August 2018, Edita Gene completed a Pre-B round of financing amounting to hundreds of millions of yuan, with participating investors including Lilly Asia Ventures, IDG Capital, and China Healthcare Capital.

Although innovative models tailored to local conditions are emerging across various sectors, technological trends remain led by overseas players. Overall, China’s genomics sector is still in a “follow” phase in terms of development trajectory.

BGI Genomics and Berry Genomics are currently the only two listed companies specializing in next-generation sequencing (NGS) technology. Since going public, they have begun leveraging capital markets to strategically position themselves within the industry. However, their approaches differ significantly.

In 2018, BGI participated in investments in four companies: Geneseeq Technology (Jingliang Gene), GeneDock, YuCe Bio, and WeGene. Among these firms, the founding teams of YuCe Bio and WeGene both originated from BGI; GeneDock had already established a strong partnership with BGI as early as 2017; and Geneseeq Technology is itself an enterprise under BGI Group’s Blue Rainbow Innovation and Entrepreneurship Center.

The companies invested in by BGI Capital are involved in businesses including reagents and consumables, liquid biopsy, consumer genomics, and genomic big data. The business scopes of these companies basically revolve around the core operations of BGI Genomics, forming a circular layout.

In 2018, Berry Genomics invested in only one company—Belief Medicine, a startup engaged in gene therapy research. Coupled with its investment activities in late 2017 in Bionano, the Gene Big Data Industrial Park, and Herui Genetics, Berry Genomics’ investment logic extends beyond supporting its core business; more importantly, it reflects a strategic vertical integration.

What were the hottest technologies in the global biotechnology sector in 2018? Monoclonal antibodies, CAR-T, or liquid biopsy? Capital investment data indicates that gene editing and gene therapy have emerged as the new trends. This field has also attracted numerous leading figures in biotechnology.

Prominent figures such as Feng Zhang, Emmanuelle Charpentier, George Church, Jennifer Doudna, and David Liu have all founded their own commercial ventures. As the technology has matured, gene editing has begun its transition from research to clinical applications. These applications primarily include the treatment of genetic disorders and rare diseases, as well as xenotransplantation.

Even after commercialization, the attitude of capital continues to influence industry development. Judging from this year’s investment and financing data, gene editing and gene therapy have garnered significant attention.

Beam Therapeutics, a startup co-founded by three CRISPR luminaries—Feng Zhang, David Liu, and J. Keith Joung—is the world’s first innovative company to develop precision genetic medicines using single-base editing technology, securing $87 million in its Series A financing round. Precision BioSciences also raised $110 million in its Series B funding, attracting interest from industrial investors such as Gilead Sciences and Amgen.

Prominent investors such as Google Ventures, ARCH Venture Partners, Hillhouse Capital, F-Prime Capital, and IDG Capital have all begun to position themselves in gene-editing technology. In China, although liquid biopsy technology remains mainstream, the domestic biotechnology sector is still in a follow-up phase; cutting-edge trends emerging in the United States are inevitably expected to take hold in China in due course.

Another trend is that companies building gene big data-related databases and developing analysis and management tools may attract attention. In the future, the core competitiveness in the healthcare sector will stem from two aspects: technological breakthroughs and data.

Berry Genomics invested over RMB 2.8 billion in 2017 to build a genomic big data industrial park; WuXi NextCODE, dedicated to improving human health through precision medicine big data, raised $240 million in financing in 2017 and subsequently closed a $200 million Series C round in 2018, with continued participation from Temasek, Yunfeng Capital, and Sequoia Capital China.

Midstream sequencing is the most mature segment in China, where nearly all major companies are concentrated. This sector is the most likely to produce the next publicly listed company, but it may also be the first to witness consolidation, with larger players acquiring smaller ones.

Roche made two major acquisitions in 2018: in February, it announced the $1.9 billion acquisition of New York-based health company Flatiron Health; in June, it acquired Foundation Medicine for $3.44 billion. Of these two companies, Flatiron Health primarily focuses on systematically collecting cancer clinical data from oncology centers and other healthcare institutions across the United States and building tumor data analysis models; Foundation Medicine is a leading company in the field of cancer diagnosis and treatment, dedicated to gaining a deep understanding of genetic variations in each cancer patient.

Many industry experts have pointed out that these acquisitions will further expand Roche’s footprint in precision oncology. By acquiring the two companies, Roche has strengthened its capabilities in both clinical data and molecular diagnostics, thereby completing its strategic layout in these critical areas.

Tempus, co-founded by billionaire Eric Lefkofsky and the team behind Groupon, aims to improve cancer treatment by integrating clinical and molecular testing data. The company collects molecular testing data and clinical data from hospitals across China, analyzes both datasets within a unified database, and seeks to enhance the standard of care for cancer patients. In 2018, Tempus completed a $110 million Series E financing round, achieving unicorn valuation status.

The integration of multi-omics data has become a trend abroad, which is bound to influence the domestic industry. The arrival of this trend will not be immediate, but it is unlikely to take too long either.