Dancing with the Bubble, Being Time's Friend: New Perspectives on Targeted Therapy and Technology Investment

VCBeat (WeChat ID: vcbeat) has learned that the “2018 Healthcare Industry Investment and Financing Summit” opened in Shanghai on December 7, 2018. Attendees discussed topics such as investment in precision medicine and the emerging trend of “AI + Healthcare.” Leng Yan, Partner at Legend Star, attended the summit and delivered a speech titled “Dancing with Bubbles, Being Friends with Time: New Perspectives on Targeted Therapy and Technology Investment.”

Leng Yan, Partner at Legend Star

The following is a summary of Leng Yan’s speech:

Since the second half of 2018, many funds have adopted a strategy of strengthening their internal capabilities. This so-called “internal strengthening” generally manifests in two ways: first, observing more while investing less; and second, actively participating in industry conferences. Consequently, we have observed that the quality of many conferences held in the second half of this year has been quite high. Meanwhile, certain terms have appeared with high frequency, such as “market downturn,” “capital winter,” and “counter-cyclical investment.” So, what is the current situation in the pharmaceutical and healthcare industry?

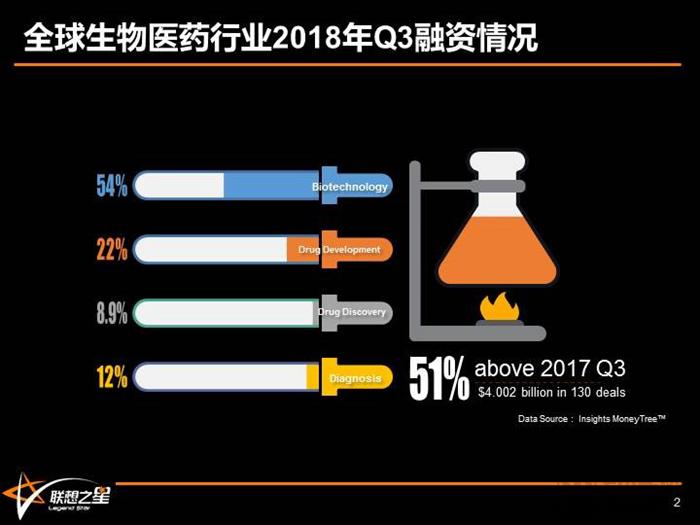

Driven by the closing of several mega-deals, the global biopharmaceutical industry completed 130 venture capital transactions in the third quarter of 2018, raising a total of $4.002 billion, a year-on-year increase of 51%.Top Projects Show Significant Capital-Attraction Effect。

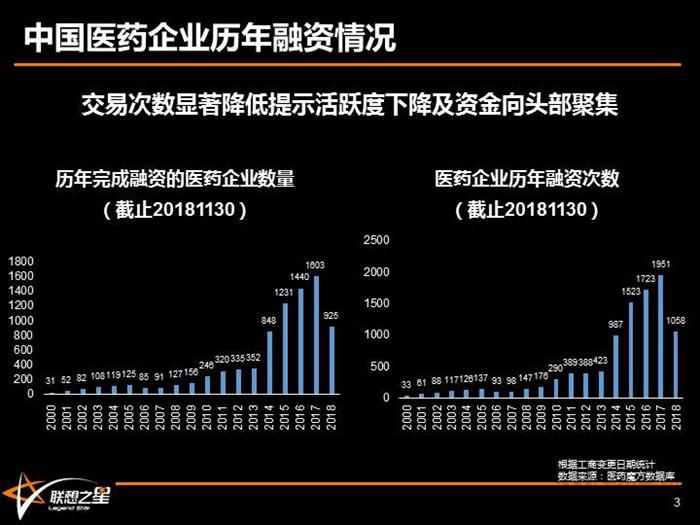

Let us examine the situation in China. In China, this cycle of the biopharmaceutical industry began around 2014 and lasted for four years, with adjustments starting to emerge this year. This data is current as of the end of November; even including December,The number of pharmaceutical companies that completed financing in 2018 was certainly significantly lower than that of the previous year, and even fell below the 2015 level.After four years of intense hype, the industry has spawned a series of high-valuation companies, many of which have entered Series D or E funding rounds this year. The result is an overall increase in funding amounts; while transaction values do not reflect capital tightness, the significant decline in the number of transactions indicates reduced market activity and a concentration of capital among top-tier players.

Navigating the Bubble: A Mandatory Course for Domestic Pharmaceutical Investment Firms

When the market is thriving, investment institutions often actively chase and participate in creating bubbles; when the market turns sour, they begin to worry that the bursting of these bubbles will adversely affect them. In fact, investment, as an economic activity,Bubbles are an unavoidable element in its lifecycle.。

What Is a Bubble? An economic bubble refers to the inflation of asset prices (particularly those of virtual capital), characterized by a substantial increase over a continuous period, causing market prices to far exceed their intrinsic value. The two primary causes of economic bubbles are: first, speculation becomes a prevailing trend, driving asset prices upward continuously; second, assets yield excessive and abnormal valuation returns.

Such inflated valuation gains cause the market price of assets to deviate significantly from their intrinsic value, i.e., the real economic fundamentals. In economics, “bubble” is a neutral term; when kept within moderate limits, it can help stimulate market activity. Only when economic bubbles become excessive, expand uncontrollably, and seriously diverge from the needs of real capital and industrial development do they evolve into illusory prosperity.

To determine whether a bubble exists, one must assess whether market prices have far exceeded the actual underlying value. From this perspective, the answer is almost certainly yes for the biopharmaceutical industry. What we need to be wary of is innovative drugs becoming upgraded versions of “generic drugs”—products that take longer and cost more to develop, yet offer insignificant differentiation from competitors. In innovative drug R&D, lengthy approval cycles and high risks do not necessarily translate into high returns. High returns primarily stem from whether the product holds a unique and scarce position in the market; only secondarily do they arise from temporary monopoly power (such as rapid launch and patent protection). Monopolies without scarcity hold no commercial value.

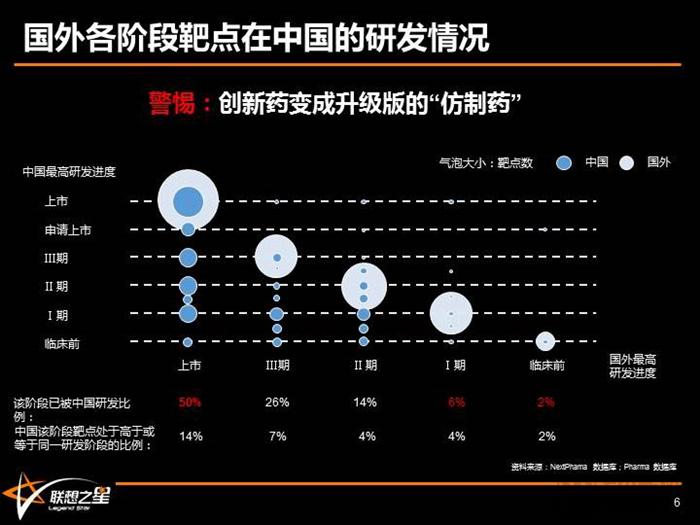

An analysis of the development status in China of drug targets at various stages abroad reveals that Chinese R&D of new drug targets is primarily follow-on in nature. While Chinese enterprises have covered half of the new drug targets already marketed abroad, the coverage rate for targets still in Phase I clinical trials or earlier stages abroad is less than 10%.

Competition and Opportunities from a Target Perspective: These two charts outline the number of drugs in development for oncology-related targets. The top chart lists the top 10 most popular targets, while the bottom chart highlights the top 10 targets with more development activity abroad than in China. We observe that for hot targets such as CD19 and PD-1/PD-L1, the number of drugs under development in China far exceeds that in the United States. In China, there are two imported PD-1 drugs and four domestically produced PD-1 drugs that have submitted marketing applications; Junshi Biosciences has already entered the administrative approval stage, and more than 70 other companies are conducting clinical trials.

Therefore, I suggest that these 70-plus companies reconsider whether to continue their efforts, as subsequent costs will be significantly higher than initial investments. If all of them do proceed, existing marketed PD-1 inhibitors would face an awkward situation, since a substantial proportion of patients would be diverted into clinical trials offering free medication.

From a target perspective, potential opportunities may lie in targets that are already well-developed in the United States but face relatively limited competition in China. However, for such drugs, market potential must also be considered, such as the number of biomarker-defined patients. Last month, the FDA approved a TRK inhibitor; many will recall the widely circulated sensational headline touting it as a “pan-cancer drug” with a 75% cure rate upon launch.

First, in the oncology treatment industry, there is no precise definition of “cure rate.” It is generally assumed that survival beyond five years equates to a cure. However, an examination of clinical study data reveals that the 75% figure actually refers to the objective response rate (ORR), defined as tumor shrinkage of more than 30% or complete disappearance. Moreover, only 39% of patients maintain a durable response for over one year. Second, NTRK gene fusions primarily occur in certain rare cancer types. Even within these rare cancers, the mutation rate is less than 10%, and in lung cancer, it is below 1%. Therefore, the population that can benefit is quite limited, contradicting the “broad-spectrum” claim often sensationalized in headlines. The accurate statement is that 75% of patients with such mutations respond to the treatment. Nevertheless, the market launch of any targeted therapy clearly benefits sequencing companies, as patients who develop resistance will seek testing to determine whether they remain eligible for the medication.

The Inevitable Path for Chinese New Drug R&D Enterprises to Complete Their Initial Capital Accumulation: The top 10 pharmaceutical companies in the United States have a combined market capitalization of $1.93 trillion, while the top 10 listed pharmaceutical companies in China have a combined market capitalization of approximately $150 billion. The combined market capitalization of the two largest U.S. pharmaceutical companies is approximately $640 billion, roughly equivalent to the scale of China’s healthcare expenditure in 2016.

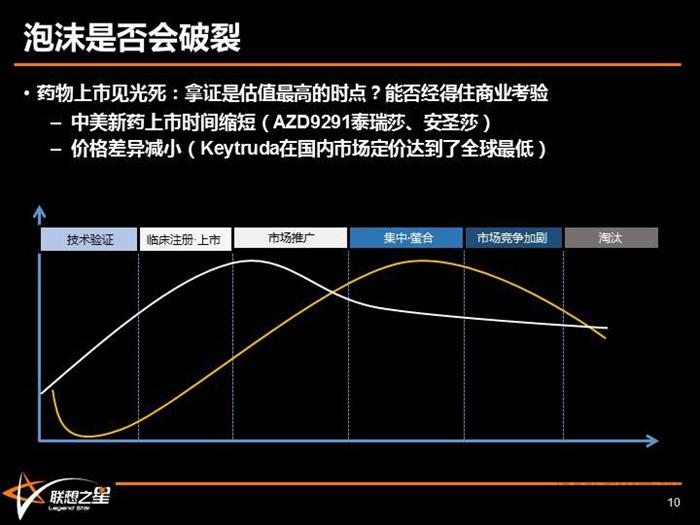

Will the bubble burst when drugs and companies go public?

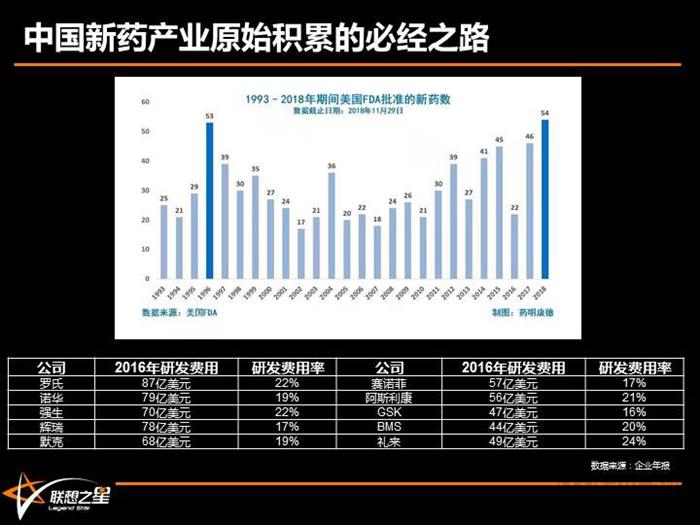

Discussing these figures is not merely to highlight the gap between China and the United States. As we all know, so-called technological upgrades and innovation-driven development must be built upon substantial foundational accumulation. For instance, the U.S. benefits from a $3 trillion market and $50 billion in R&D spending, jointly supported by large pharmaceutical companies and venture capital (VC) firms. We are aware that the R&D expenditure ratio of major U.S. pharmaceutical companies reaches or exceeds 20%, whereas the foundation of China’s pharmaceutical industry is incapable of sustaining R&D investment at this magnitude.

Since joining the WTO in 2001, China has largely fulfilled its commitments in the realm of intellectual property rights related to the pharmaceutical industry. This has compelled China’s pharmaceutical sector to pursue a development path distinct from that of India. Given the weak foundation of its initial capital accumulation, bridging the resulting gap has largely relied on investment institutions driven by government initiatives. The current bubble in China’s biopharmaceutical investment sector is an essential lesson for Chinese investors and an inevitable stage in building the foundational capital base for the innovative drug industry. Without cultivating a sufficiently large pool of capital, it is impossible to nurture major industry players.

Will the Bubble Burst? In addition to pipeline selection and development progress, innovative drug R&D companies face two challenges: drug commercialization and corporate IPO.

Do Drugs Fail Upon Market Launch? Typically, a product’s value follows such a fluctuating curve; however, for certain innovative drug developers, the moment of regulatory approval may represent the peak valuation. Due to the lengthy R&D cycle for new drugs, this issue could previously be obscured or temporarily set aside. Yet, with the shortening time to market and narrowing price differentials between China and the United States, whether a company’s products can withstand commercial scrutiny has become an unavoidable challenge.

Shortened Time to Market for Drugs:For new drugs launched in the past two years, the time lag between their market approvals in China and the United States has narrowed to 1–2 years, or even a few months. For example, Tagrisso (AZD9291), which was included in the Priority Review list in September 2016, was approved in March 2017, only 1 year and 4 months later than in the United States. Recently, the new lung cancer drug Alecensa (alectinib, a second-generation ALK inhibitor) received approval from the China Food and Drug Administration (CFDA) just nine months after its approval in Europe and the United States.

Drug Prices:Due to advancements in the development and approval processes for innovative drugs in China, foreign pharmaceutical companies have adopted a strategy of low pricing to seize market share early upon entry. For instance, with domestic PD-1 inhibitors poised for launch, Keytruda was priced at its lowest global level in the Chinese market, with an annual treatment cost of RMB 304,606—only 54% of its price in the U.S. market. We have all heard founders tout the narrative of cost advantage, arguing, “Imported drugs are so expensive; my domestically produced alternative is cheaper, thereby significantly expanding the market.” However, if imported drugs proactively reduce their prices from launch, realizing the commercial value of domestic “me-too” drugs becomes a substantial challenge.

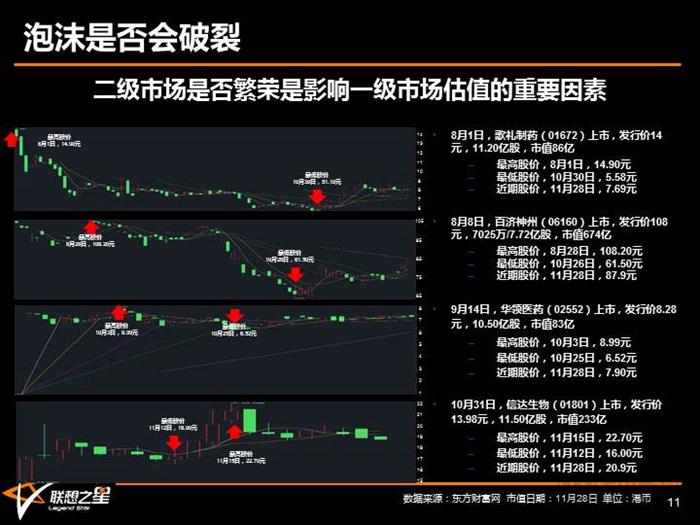

Do IPOs Lead to Immediate Failure Upon Exposure? Another factor is the secondary market. As of the end of November, among unprofitable new drug R&D companies listed in Hong Kong after the implementation of the new regulations, only Innovent Biologics has avoided breaking its issue price. Whether subsequently listed R&D enterprises can withstand the valuation pressures of the secondary market will become a significant factor influencing valuations in the primary market.

Legend Star is an early-stage investment firm specializing in angel and Series A rounds. We currently manage angel investment funds with a total size of approximately RMB 2.5 billion, having invested in over 260 startups. Among these, 52 are in the healthcare sector and around 20 in biopharmaceuticals, making this segment the highest-yielding within our healthcare portfolio. As an early-stage investor, our strategy avoids chasing market trends; instead, we aim to position ourselves ahead of them. We focus on identifying the fundamental laws governing enterprise value development and refrain from pursuing projects with valuations that significantly deviate from their intrinsic worth. This approach allows us to remain unafraid of market bubbles and maintain greater patience.

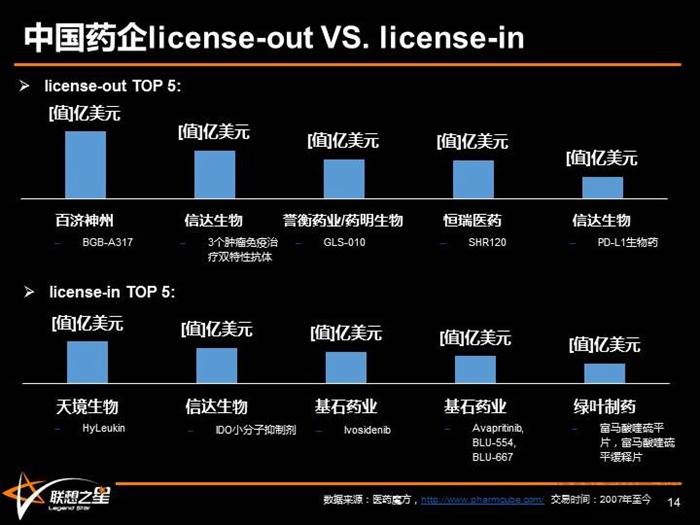

Evolution of Legend Star’s Technology Investment Strategy: This chart illustrates the landscape of domestic and international co-development. In terms of financial value, the total contract amount for license-out deals in China generally exceeds that of license-in deals, which to some extent reflects the substantial improvement in China’s new drug R&D capabilities in recent years, enabling meaningful international dialogue.

Our investment strategy has evolved from a pre-2013 focus on domestic market size and technological leadership to a greater emphasis in the past five years on innovation that can be validated through international collaboration (innovativeness), founders and teams with drug development experience (speed), and whether products address unmet clinical needs (uniqueness).

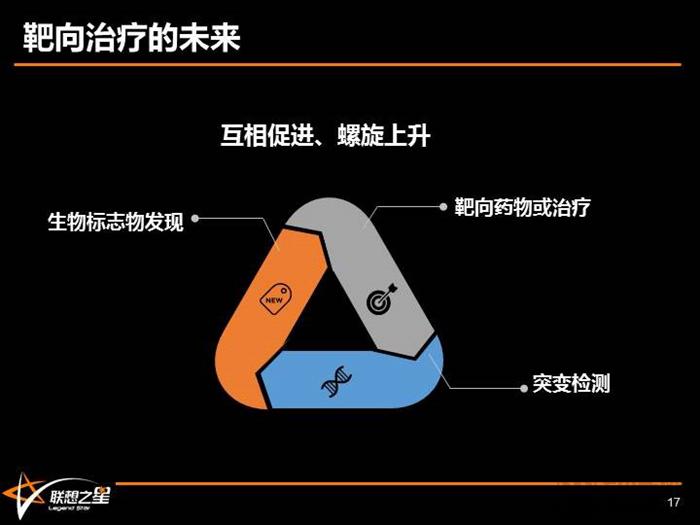

In the realm of targeted therapy, a closed-loop ecosystem will emerge in the future, encompassing biomarker discovery, accelerated market approval of targeted drugs, and patient stratification/testing. This loop will foster mutual reinforcement and spiral upward progress. Whether for startups or investments, activities will likely revolve around this closed loop. In fact, early-stage investors’ criteria for selecting projects should align closely with founders’ rationale for choosing their ventures. I am particularly keen to engage with founders in discussions on the meanings of “innovation,” value, and return potential. I believe that achieving win-win outcomes for both entrepreneurship and investment is a hallmark of the industry’s growing maturity. Finally, I wish you all success in your entrepreneurial endeavors and smooth fundraising. Thank you.