Is the Medical Robotics Business Profitable? Insights from 'Da Vinci' Earning $3.1 Billion Annually

Editor’s Note: This article is reprinted from 36Kr, authored by Mengxiangjia Caicai and Dun Yuting. VCBeat republishes it with authorization.

Replacing medical staff with robots is no longer a myth, as domestically produced medical robots are increasingly making their presence felt.

During surgical procedures, Tinavi’s “Tiandi” third-generation robotic system assists surgeons in performing surgeries for extremity and pelvic fractures, as well as full-segment spinal procedures, resulting in reduced soft tissue injury, less blood loss, faster patient recovery, and decreased surgeon fatigue.

The gastroscopy, which strikes fear into the hearts of most people, can now be completed quickly by simply swallowing a capsule. Inside the stomach, the capsule transforms into a “robot” that performs spiral scanning and transmits images in real time to the physician’s computer.

In hospital outpatient departments, iFlytek’s “Xiao Yi” has been deployed in nearly 100 hospitals across China, providing patients with services such as appointment registration, inquiries, intelligent triage, pathway guidance, and report retrieval, thereby alleviating the triage workload for hospitals.

In the context of in-hospital logistics, Teammi has developed China’s first logistics robot capable of entering operating rooms, which not only assists medical staff in transporting supplies but also enables refined management of hospital logistics.

In the pharmacy preparation room, robots also automatically complete the compounding of liquid medications, sparing healthcare workers from contact with pharmaceutical agents and thereby preventing contamination of the solutions and injury to personnel.

Medical robots, a miraculous species once confined to science fiction novels and films, are gradually permeating our daily lives and emerging as a new hotspot for entrepreneurship and investment.

According to incomplete statistics, at least 100 medical robot startups emerged in China between 2014 and 2017, with over 40 publicly disclosing their financing activities. In addition, many listed companies have expanded into the medical robotics sector in recent years, including Boshi Shares, Jinming Precision Machinery, Keyuan Shares, Fosun Pharma, Dima Shares, and Midea Group. Furthermore, some industrial robotics companies (such as UAI Intelligence) and medical device companies (such as Perlove Medical) have also extended their business operations into the field of medical robotics.

Behind the strategic investments by multiple companies lies the enormous market potential of medical robots. According to the latest report from Grand View Research, the global market for medical robots (devices) was valued at USD 8.737 billion in 2014 and is projected to reach USD 17.9 billion by 2020, representing a compound annual growth rate (CAGR) of 12.7%. As a high-value-added category, when combined with auxiliary equipment and consumables, it is expected to evolve into a trillion-dollar industry chain in the future. The most renowned company in this field, Intuitive Surgical Inc. (ISRG), achieved revenues of USD 3.1 billion in 2017 thanks to its “da Vinci Surgical System,” effortlessly capturing half of the current medical robot market and injecting greater confidence into the industry’s development.

In light of this, this article aims to clarify several key issues:

How Did the “Da Vinci” Wealth-Creation Myth Achieve Early Dominance? What Lessons Can Be Drawn?

What Factors Are Propelling Medical Robots into the Spotlight?

How should we carve out a share of this market?

In China, How Do We Find the Next “Da Vinci”?

In the eyes of healthcare professionals, "Da Vinci" is an "industry legend."

The da Vinci Surgical System, a minimally invasive surgical robot developed in the United States, was launched as early as 1999, with its competitors emerging several to over ten years later.

Why Is the da Vinci Surgical System Considered the Dominant Player in the Field of Surgical Robotics? Since its market launch, it has monopolized the industry for two decades, with its leading position remaining unchallenged. To date, it continues to maintain a gross profit margin as high as 70% and a net profit margin of 30%, with a total market capitalization approaching $60 billion.

According to 2017 data, a total of 4,149 da Vinci Surgical Systems were sold or leased worldwide, with a market share far exceeding that of other competitors, thereby maintaining a high-priced monopoly on the market.

In 2006, surgical robots were still a novel and rare phenomenon. That year, Beijing’s PLA General Hospital (301 Hospital) introduced and deployed the first da Vinci Surgical System, marking the beginning of the “da Vinci” decade-long journey in China. For a long period, the domestic market was monopolized by its high price. While each unit cost approximately RMB 10 million abroad, it could sell for around RMB 20 million in China.

It was only in recent years, as domestic technologies gradually matured and an increasing number of Chinese-made robots entered the market competition, that the situation began to change slightly.

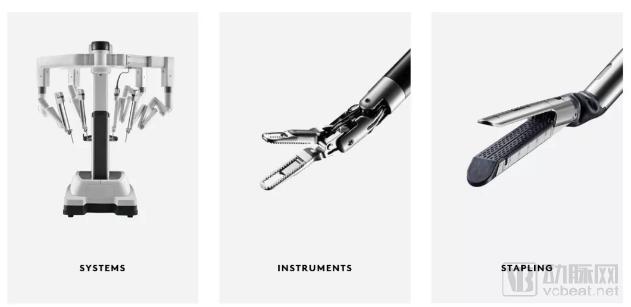

Da Vinci Surgical Robot (Image from the official website)

So, why has the da Vinci Surgical System become the dominant leader in its industry? We attempt to summarize several key reasons, with the hope of anticipating the next “da Vinci phenomenon.”

First, it entered the market at an early stage, being among the first generation of surgical robots in human history, thus enjoying a first-mover advantage. In 1997, AESOP, the first FDA-approved surgical robot featuring a camera-holding robotic arm, was launched in the United States. Subsequently, in 1999, the da Vinci Surgical System was developed by Intuitive Surgical, Inc. in the U.S. The United States can be regarded as the birthplace of surgical robots, with the earliest pioneers in this field all originating from there.

Secondly, it meets the needs for reducing incision size, improving surgical precision, and shortening operation time. Surgical robots have significant advantages over manual procedures. Primarily designed to assist physicians in performing surgeries, a surgical robot system typically consists of a console, robotic arms, and a 3D imaging platform. Instead of directly touching the patient, the surgeon sits before a computer display and controls the robotic system to perform the procedure. The advantages of surgical robots include greater precision than manual surgery, more accurate incisions, minimized trauma, and faster patient recovery. Compared with 2D visualization, the system provides a 10–15x magnified field of view, overcoming issues such as poor precision in traditional surgery, the lack of 3D depth perception for surgeons, and prolonged operative times.

To cite a specific example, for the same surgical procedure, traditional methods require a laparotomy with an incision extending from the sternum to the pubic symphysis, necessitating the exteriorization and subsequent repositioning of the entire large intestine; postoperative recovery takes several months. In contrast, using a surgical robot allows for an incision of only a few centimeters, enabling discharge within just a few days after surgery and full recovery within a few weeks.

Third, the da Vinci Surgical System is applicable to a wide range of medical departments, offering broader market potential. It currently boasts the widest applicability among surgical robots, suitable for general surgery, urology, cardiovascular surgery, thoracic surgery, gynecology, otolaryngology, and pediatric surgery, among others.

Fourth, the key to the success of the da Vinci Surgical System lies in its technological leadership, which has established high technical barriers. It features three core technologies: the highly dexterous EndoWrist robotic arms, 3D high-definition imaging technology, and an intuitive master console that enables seamless human-machine interaction. It can be said to represent the leading level of minimally invasive surgical technology.

Fifth, over the past two decades, the technology of the da Vinci Surgical System has continued to evolve rapidly. To date, it has been used in more than 5 million procedures, during which time minimally invasive surgical solutions have been continuously optimized to reduce procedural variability. Currently, its latest technological advancements include a new generation of integrated systems and single-port capabilities.

In fact, the da Vinci Surgical System is a typical representative of Western robotics technology. Similarly, many robotic technologies from Western countries once monopolized the global market at high prices for a certain period.

At the heart of the matter, technological leadership is the key to success. So, how does technology influence the commercialization pathway of medical robots?

Looking a century into the future, the ultimate goal of medical robotics may be to achieve 100% replacement of human labor, thereby creating a fully instrument-based healthcare ecosystem. Currently, the focus of medical robotics is to identify which processes can be automated by robots and which tasks can be performed more effectively by robots than by humans.

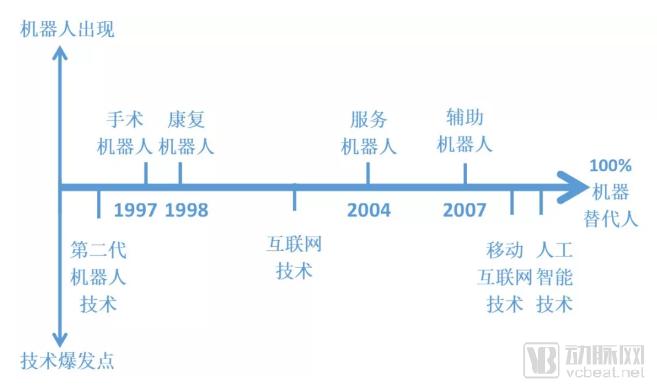

This is a timeline for medical robots presented by the author. The author believes that many factors influence the commercialization process of medical robots, including policies, demand, and technology. Therefore, we aim to explore how these elements affect the “timeline.”

Surgical Robot

Medical robots first appeared in the operating room. In 1985, in an operating theater at a hospital in Los Angeles, USA, the world’s first surgical robot, Puma 560, participated in a neurosurgical brain biopsy procedure. At that time, it successfully assisted physicians in guiding and positioning the needle during the brain tissue biopsy.

In fact, the Puma560 was not a medical robot; it was actually an articulated-arm industrial robot. This represented a “crossover” application for industrial robotics. Later, due to safety concerns, the manufacturer of the Puma560 temporarily prohibited the use of this robot in surgical procedures. Nevertheless, the strong demand for robotic assistance among surgeons was clearly evident.

This period marked more than two decades since the emergence of the first generation of industrial robots, a time when their technology was gradually maturing, and also coincided with the advent of the second generation of industrial robots (adaptive robots). It was precisely because robotics had entered a phase of explosive growth in the industrial sector that it was introduced into the healthcare industry.

In 1997, AESOP, a voice-controlled “camera-holding” robotic arm operated by surgeons, was developed in the United States, becoming the first surgical robot approved by the FDA for debridement procedures. In 1999, Intuitive Surgical, a U.S. company, developed the da Vinci Surgical System, marking the beginning of its dominance in the surgical robotics market.

Turning our attention to the domestic market, the “Da Vinci” surgical system, after its initial entry into China in 2006, long maintained a high-priced monopoly over the country’s surgical robot market. It is only in recent years that domestic technologies have begun to advance rapidly, enabling Chinese entrepreneurs to achieve breakthroughs. Multiple domestically produced robots have progressed from research and development to clinical trials and subsequently obtained certification from the China Food and Drug Administration (CFDA), including those developed by Huazhi Micro-Invasive and Baihui Weikang’s Remebot, among others.

Rehabilitation Robots

Three years after the emergence of surgical robots, rehabilitation robots also began to come into public view. Their origin likewise stems from the explosion of industrial robot technology mentioned above. Rehabilitation robots primarily utilize second-generation robotic technology (adaptive robots), which was introduced in the late 1980s and soon thereafter applied to medical rehabilitation.

The function of rehabilitation robots is to help individuals with mobility impairments regain the ability to "stand." They primarily serve people with disabilities, stroke patients, and those injured during physical activity, for whom rehabilitation therapy is an essential need.

The world’s first commercialized rehabilitation robot was launched by Switzerland’s Hocoma in 1999. Subsequently, Israel’s ReWalk also introduced its rehabilitation robot in 2001. Following these two pioneers, an increasing number of rehabilitation technologies have entered this field.

Rehabilitation robots in China have also seen robust development, characterized by a flourishing and diverse landscape. Several technologically leading companies have emerged, with standout projects including those from Harbin Institute of Technology Robotics, Jinghe Robotics, and Ruihan Medical.

Assistive Robots and Service Robots

The last to emerge are likely assistive robots and service robots. This is because these two categories rely more heavily on technologies such as the internet, big data, artificial intelligence, and mobile internet, and they primarily address enhancement-oriented needs, resulting in their later appearance.

The sectors of assistive robots and service robots are still in their early stages. A wide variety of robots have already emerged, being deployed across diverse medical scenarios. We believe that even more novel forms will appear in the future.

Common assistive robots include intravenous medication compounding robots that support medical staff; “robot nurse” care robots that monitor patients’ health conditions after discharge; and therapeutic robots for the prevention and treatment of Alzheimer’s disease, which interact with patients to help them recall past enjoyable experiences, life events, and feelings of guilt, thereby providing psychological intervention through reminiscence therapy.

Service robots include transport robots, disinfection robots, and others. Transport robots primarily provide logistics services to hospitals, reducing the workload of medical staff and lowering hospital logistics costs.

Notably, there has been significant buzz this year in China regarding the deployment of transport robots: Shanghai Children’s Hospital announced in July that it would introduce transport robots, and Noah Hospital announced a collaboration with the Worcester Polytechnic Institute in the United States to establish a research and development center focused on hospital logistics robots.

Currently, there is minimal homogenization among assistive robots and service robots, and the industry landscape remains far from mature. With their share of the domestic market standing at only 17%, there are significant opportunities for new entrants.

In summary, driven by a combination of technological, demand-side, and policy-related factors, the development trajectory of medical robots has generally followed the sequence: from surgical robots to rehabilitation robots, and then to assistive and service robots.

Throughout history, the emergence of most new innovations has hinged on the urgency of demand and the accessibility of technology, and medical robots are no exception. The severe imbalance between the supply side of medical resources and the demand side from patients has generated intense market demand.

Accordingly, it has become a near-consensus within the industry that medical robots will become a “standard feature” of future healthcare. Many investors I have recently spoken with stated that “the replacement of manual labor or traditional instruments by medical robots is akin to automobiles replacing bicycles in the early days; they will become ubiquitous in the future.”

In fact, as early as 1985, the PUMA 260 became the first “pioneer” robot. Researchers utilized it to perform robot-assisted stereotactic neurosurgical biopsies, marking the dawn of medical robotics development. However, it is only in recent years that a large number of startups have entered the field in China, which remains in an initial stage focused on collectively “expanding the market.”

Why Have Medical Robots, Which Have Been Around for Over Three Decades, Experienced Rapid Development in China in Recent Years? What Are the Industry Variables?

First, many national-level policies have proposed key support for medical robots, positioning them as a crucial component of China’s Industry 4.0 strategy; meanwhile, the advancement of tiered diagnosis and treatment systems and the significant shortage of primary care physicians have become strong drivers for robot research and development.

Furthermore, with the intensifying aging of society and the evolving disease spectrum, the volume of tumor-related surgeries and the demand for rehabilitation are expected to rise further. According to data from the National Health and Family Planning Commission, China currently has over 200 million people aged 60 and above. It is projected that by 2050, individuals aged 60 and older will account for 35% of the population, making China the country with the most severe aging problem in the world. The elderly population is particularly prone to diseases, with significantly higher prevalence rates of chronic conditions and hospitalization rates compared to other demographic groups. Medical robots can effectively provide precise surgical services and shorten postoperative recovery time for elderly patients, thereby meeting these growing needs.

From the payer perspective, as medical insurance coverage and reimbursement rates continue to rise, the localization of high-end medical devices has become a trend. The National Health Commission has recently issued standards that explicitly require tertiary rehabilitation hospitals to be equipped with such devices, further catalyzed by these favorable policies.

From the perspective of funding sources, the R&D of domestically produced medical robots in China has primarily benefited from support by national science and technology projects in the past. In recent years, capital investment has begun to flow into this sector, making it one of the hotspots pursued by investors.

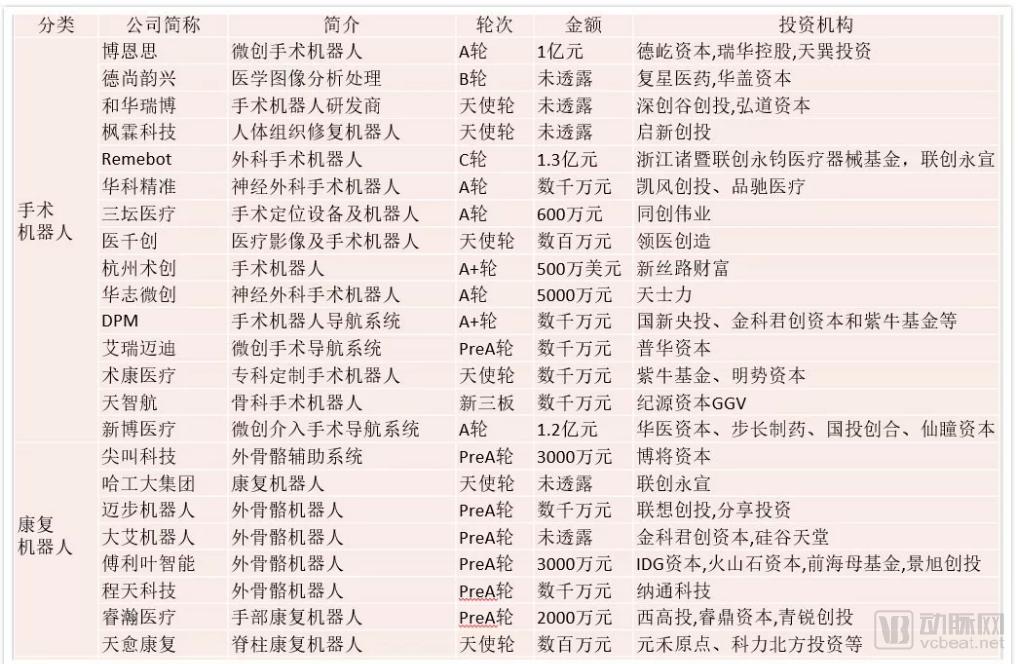

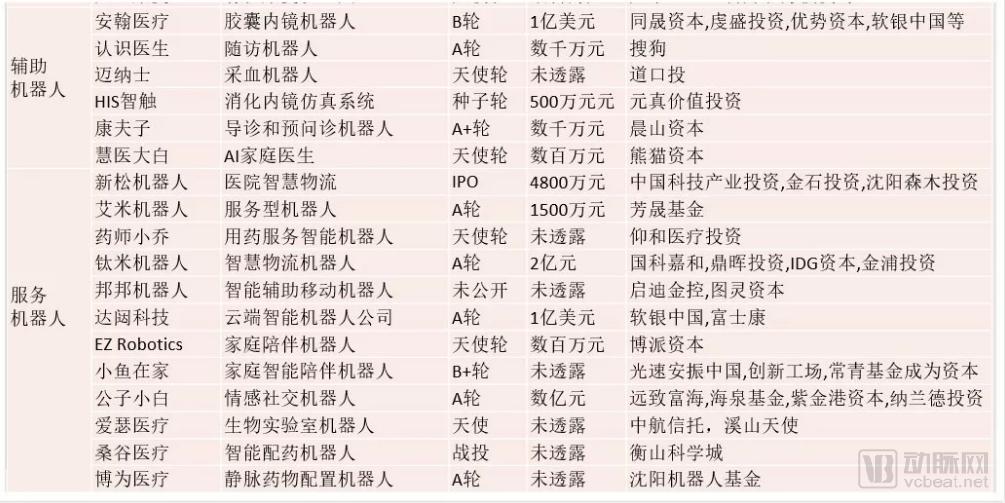

Data compiled from Jingzhun, VCBeat, and publicly available online sources

However, regardless of the specific field, most medical robots in China are still in the research and development or clinical trial stages and have not yet formed a large-scale industry. After all, the journey from laboratory to commercialization typically involves five stages: concept evaluation of innovative research, experimental validation or prototype development based on preliminary findings, clinical studies and regulatory approval for market entry, manufacturing, and market launch with market cultivation. This process often takes more than ten years and involves numerous implementation details.

"Build a Solid Product"

Medical robotics is an emerging interdisciplinary field that integrates medicine, biomechanics, mechanics, mechanical engineering, materials science, computer graphics, computer vision, mathematical analysis, and robotics. Therefore, whether the first hurdle can be overcome depends on whether the team is complete.

From a technical perspective, most companies still have many fundamental core issues that have not been perfectly resolved. These include new mechanisms and configurations for performing delicate operations; flexible control issues, such as the precise sensing and control of multi-media liquids and soft tissues, which remain unresolved; and challenges related to rigid-flexible transformation, motion planning, multi-information integration, visualization, and sensing, as well as how to achieve the most comprehensive human-machine interaction.

Capital Support

The research and development cycle for medical robots is also exceptionally long, typically spanning 6 to 10 years, requiring sustained capital investment in the early stages. Funding constraints have become a major bottleneck restricting the rapid growth of companies. It is reported that many small and medium-sized enterprises (SMEs) centered on the concept of medical robots are currently facing significant difficulties in securing financing. From an investment perspective, institutional investors favor companies that are future-oriented, preparing for initial public offerings (IPOs), and pursuing internationalization. Among these factors, independent research and development (R&D) capability is particularly critical; without it, even amidst a capital boom, companies will struggle to achieve sustainable success.

Close Collaboration with Hospitals

R&D requirements are proposed by physicians. Translating their pain points into technical language, and then into product specifications, requires prolonged use and iterative refinement to enhance practicality and functionality. It is essential to approach clinical needs and technical challenges from an engineering perspective. An investor who had previously invested in neurosurgical surgical robots told the author, “Without sufficient follow-up cases and clinical trials, you simply cannot support the product’s market launch.”

Establishment of Operational Standards

Take surgical robots as an example. Operating them is a highly technical task that requires professional training. Intuitive Surgical, Inc. (ISRG), the company behind the da Vinci Surgical System, maintains its own dedicated professional training team. However, even in this relatively advanced field, neither industry standards nor national standards have been established, and rehabilitation robotics lags even further behind in this regard. I believe that as more participants enter the market and capital continues to flow in, the formation of a closed-loop market ecosystem will make the establishment of relevant standards imperative.

Access Target Markets

A prevailing consensus in the industry is to recognize the power of the “template market,” which involves leveraging leading hospitals as pilot sites to demonstrate efficacy. Taking surgical robots as an example, while there is a widespread rush to secure placements in large Grade 3A hospitals, non-Grade 3A institutions will become the primary battlefield for future surgical procedures under the trend of tiered diagnosis and treatment; HuaZhi Micro-Invasive has strategically positioned itself in this segment ahead of time. As for rehabilitation robots, with the rapid expansion of private rehabilitation facilities, targeting the non-public healthcare system will be key to their development. Regarding assistive robots, the medical service industry chain is becoming increasingly specialized, with “outsourcing” emerging as a prominent industry trend. In the future, third-party institutions are likely to constitute their main market. For instance, Anhan Medical has achieved large-scale sales by leveraging the testing network of Meinian Onehealth.

Who Pays the Bill?

It is reported that the da Vinci Surgical System is priced at approximately RMB 10 million abroad, while its domestic price in China reaches around RMB 20 million. Such high costs naturally deter both hospitals and patients. Currently, as surgical procedures involving these robots are not covered by medical insurance, their clinical application remains very limited. Although the "Robotics Industry Development Plan (2016–2020)" proposes supporting the promotion and application of medical robots through an insurance compensation mechanism for the first set(s) of major technical equipment, the lack of detailed implementation rules has led to some delays in policy execution. In addition, the Chinese government is focusing on establishing physiotherapy departments in community hospitals, expanding medical insurance coverage to include rehabilitative therapy, and other measures, which will pave the way for the broader adoption of rehabilitation robots.

Can China Catch Up with and Surpass the UK and the US?

Ultimately, a major backdrop to the gradual commercialization of domestically produced medical robots in China is the significant gap with developed countries. It is reported that since the introduction and first use of the da Vinci Surgical System in China in 2006, the market was monopolized by its high price (around RMB 20 million) for a long period. The situation has only begun to change in recent years with the entry of domestic robots into market competition. The cost-performance advantage brought by localized research and development and production will further enhance patient acceptance, driving strong market growth. Coupled with continuous policy support for import substitution, domestically produced medical robots hold the promise of “catching up with the UK and surpassing the US” over time. If technological limitations can be overcome, replicating the wealth-creating myth of the “da Vinci” system will no longer be an unrealistic expectation.

Medical robots have been under development for over a decade. From the perspective of the industry life cycle, they are currently in the introduction stage, characterized by strong demand and rapid growth, with the potential to become a massive industry in the future. Industry insiders generally agree that medical robots will remain a focal point for technological R&D and equity investment both domestically and internationally over the next ten years, entering a phase of leapfrog development. This advancement will be driven not only by market expansion but also by functional enhancements, including improved human-machine interaction experiences, as well as greater dexterity and convenience.

From a historical perspective, the medical robotics industry is still in its “infancy” as an emerging sector. Given the supply-demand imbalance in China’s healthcare resources and the aging population, the market size in China is expected to expand rapidly. Coupled with increased government healthcare spending and healthcare system restructuring, there is hope that domestically produced medical robots will achieve leapfrog development.