Disruption in China's Pharmaceutical Market: Two Major Shifts Spark a New Five-Way Power Play

Editor’s Note: This article is reprinted from Sina Medicine, authored by Zhang Ying. VCBeat republishes it with authorization.

“Winter is coming” – this iconic line from Game of Thrones seems to be the most apt metaphor for China’s current pharmaceutical market. December 6 has become another date that sent shockwaves through the industry, following in the footsteps of July 22. What was anticipated as a “reward for early movers” has instead turned into “the lament of pioneers.” Where do we go from here? This article attempts to explore the underlying logic by examining the shifting relationships among participants in the pharmaceutical market.

For participants in the pharmaceutical market, we broadly categorize them into five roles: payers, providers, distributors, technology enablers, and regulators. The traditional pharmaceutical market is primarily composed of a “four-party relationship,” as illustrated in the figure below:

Among these factors, the multi-payer health insurance system not only involves multiple participant schemes (such as Employee Basic Medical Insurance, Urban Resident Basic Medical Insurance, and the New Rural Cooperative Medical Scheme), but also features fragmented management, with the National Development and Reform Commission overseeing pricing, the Healthcare Security Administration managing payments, and the National Health and Family Planning Commission regulating qualifications (including tendering and bidding). This fragmentation among payers has created fertile ground for the flourishing diversity of the pharmaceutical market, providing opportunities for the rise of a number of small and medium-sized pharmaceutical enterprises.

As suppliers, pharmaceutical manufacturers are responsible not only for product R&D but also for production and promotion. Due to historical factors, so-called “miracle drugs,” represented by certain adjunctive therapies, rose to prominence. In contrast to the international landscape—characterized by equitable access (including treatment and reimbursement rights for rare diseases), targeted therapy (specific indications matched with corresponding drugs), and commercial insurance coverage (involvement in drug launch negotiations and payment for high-priced patented drugs)—these “miracle drugs” featured “broad indications/therapeutic uses, ample pricing margins, and reimbursement by public medical insurance.” Such characteristics were better suited to the domestic environment at the time, particularly driving rapid growth after the new healthcare reform launched in 2009.

As channel partners, distributors have played a significant role historically. They serve as a bridge between pharmaceutical manufacturers and hospitals, facilitate access to products for physicians, and act as a gateway to securing medical insurance reimbursement or sales qualifications.

Doctors, as distinct from hospitals, are categorized here as technical support providers because they are both the actual holders of medical expertise and the practitioners who issue prescriptions directly to patients. They engage in continuous learning and drive the development of pharmaceutical products at the point of care. Furthermore, due to the “inverted pyramid” structure, physicians at tertiary hospitals wield significant authority, with prescribing privileges that span from common ailments like colds and fever to complex treatments such as oncology therapies.

Although the regulatory authority (the National Medical Products Administration, NMPA) plays a crucial role, it is not considered one of the traditional four key stakeholders. This is because the supply of drugs in the existing market is sufficiently abundant, while the approval process for new products—representing incremental market growth—is characterized by inefficiency and relatively low barriers to entry. Consequently, for most suppliers, winning bids and securing inclusion in reimbursement formularies are more critical than product development itself; a bird in the hand is worth two in the bush.

In the traditional market, the abundance of stakeholders—multiple payers, suppliers, distribution channels, physicians, and patients—has fostered a relatively balanced power dynamic among all parties. This equilibrium has promoted mutual prosperity, with a shared goal of expanding the pharmaceutical market to ensure public access to medications, where cooperation far outweighs competition. While adjustments may occur during updates to the National Essential Medicines List and through bidding processes, these changes will not fundamentally alter the existing market landscape.

In recent years, two major shifts have fundamentally transformed the landscape of China’s pharmaceutical industry: first, the philosophy of medical insurance has shifted from “broad coverage” to “cost containment”; second, the concept of healthcare has gradually evolved from a focus on “disease treatment” to “lifecycle health management.”

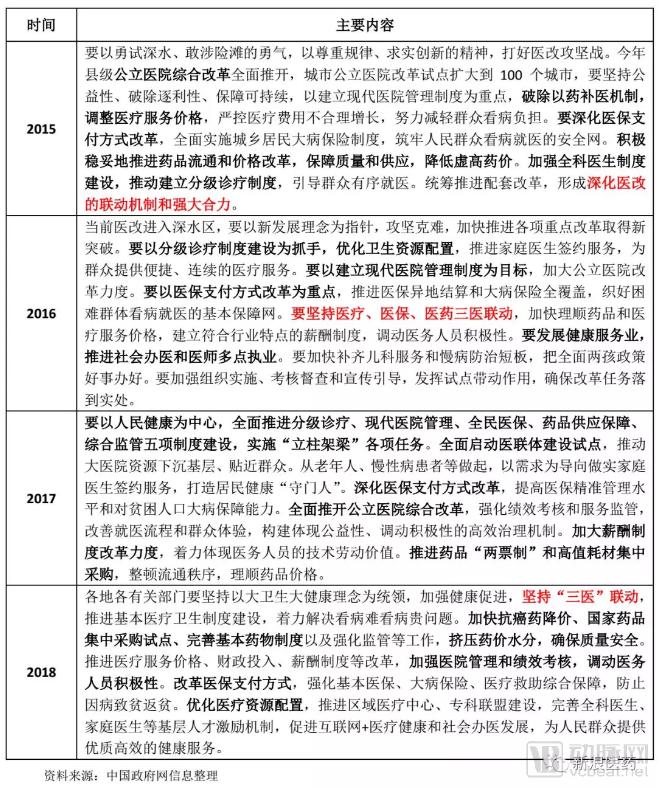

These two major changes are also in line with the spirit of the "National Teleconference on Healthcare Reform." The key points from the speeches delivered by the Vice Premier in charge of healthcare in recent years are summarized in the table below:

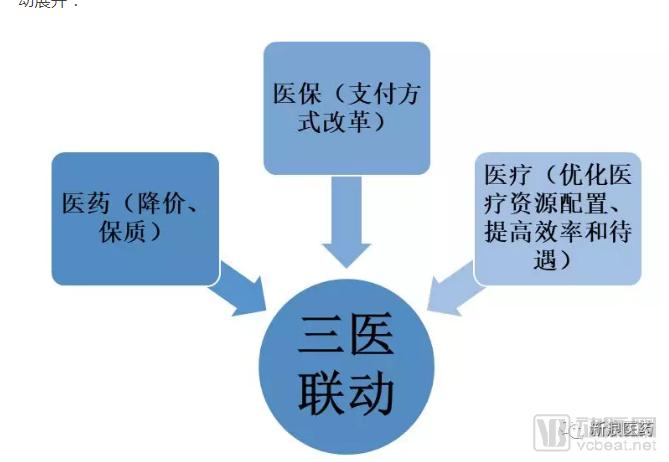

It can be seen that the keywords of healthcare reform conferences in recent years have been largely consistent, demonstrating policy consistency and coherence, all centered around the coordinated development of medical care, health insurance, and pharmaceuticals (the “Three-Medical Linkage”):

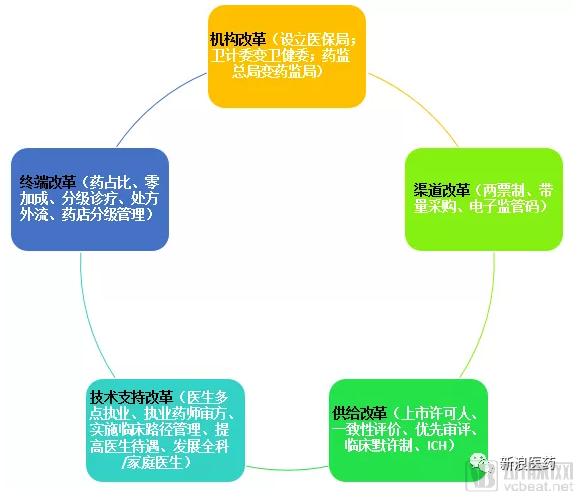

In terms of specific policies, they can be summarized as follows:

Policy changes have driven transformations among market participants, reshaping China’s pharmaceutical market into a “New Pentagon,” where collaboration has given way to strategic competition.

On the payer side, the landscape has shifted from “fragmented insurance schemes” to a “dominant national insurer.” The establishment of the National Healthcare Security Administration (NHSA) has ended the separation between pricing and reimbursement, consolidating funds from the Employee Basic Medical Insurance, Urban Resident Basic Medical Insurance, and the New Rural Cooperative Medical Scheme. Recent negotiations on anticancer drugs and the “unexpected outcomes” of the “4+7” volume-based procurement program have both underscored the NHSA’s considerable leverage. Change driven by the payer is now imperative.

On the supply side, the role of “pharmaceutical manufacturers” has transitioned to that of “Marketing Authorization Holders (MAHs).” This shift not only enables R&D institutions to concentrate their resources on core competencies while avoiding capital investment in production, but also effectively promotes specialized division of labor and enhances efficiency.

In terms of distribution channels, agents will be replaced by Contract Sales Organizations (CSOs). Historically, agents primarily represented a division of labor in business relationships. However, under current policies that encourage innovation and promote survival of the fittest, the commercial function is being deemphasized, and pharmaceutical companies’ focus is shifting from “profit-driven” to “value-driven.” In the past, competition among pharmaceutical companies centered on winning bids and price margins, amounting to fierce rivalry within the small circles of generic drugs and traditional Chinese medicine preparations. At present, the competition revolves around R&D, quality, brand strength, and addressing “unmet clinical needs” or providing “better disease-specific solutions.” This is a competition that spans both in-hospital and out-of-hospital settings and extends beyond medical insurance coverage, requiring CSOs to champion product value.

In terms of technical support, pharmacists have moved from the sidelines to center stage alongside physicians. In July 2018, three departments—the National Health Commission, the National Administration of Traditional Chinese Medicine, and the Logistics Support Department of the Central Military Commission—jointly formulated the “Specifications for Prescription Review in Medical Institutions.” The Specifications state that “pharmacists are the primary persons responsible for prescription review. Pharmacists shall conduct a item-by-item review of all content in prescriptions. Medical institutions may leverage relevant information systems to assist pharmacists in conducting prescription reviews. All prescriptions must pass review before entering the pricing, billing, and dispensing stages; prescriptions that have not passed review shall not be billed or dispensed.” A related policy is Diagnosis-Related Groups (DRGs). In the future, mainstream disease categories will have relatively standardized diagnostic and treatment pathways, testing procedures, and medication guidelines, thereby narrowing physicians’ scope for discretionary practice. China’s 450,000 licensed pharmacists will assume the critical responsibility of prescription review. These professionals serve both as a secondary check and as “cost controllers,” with the authority to reject unreasonable prescriptions issued by physicians. It is reasonable to expect that pharmacists will play a significant role when Pharmacy Benefit Management (PBM) is fully implemented in the future.

As a newly prominent stakeholder, regulators are playing an increasingly vital role in the evolving pharmaceutical landscape. By joining the International Council for Harmonisation (ICH), implementing implicit approval for clinical trials, accelerating innovative drug reviews, conducting consistency evaluations for generic drugs, and re-evaluating traditional Chinese medicines, the drug regulatory system has transformed from a mere “approver” into a “guide,” steering industry practitioners toward higher quality, better alignment with clinical needs, and healthier competition. The decision to invest in R&D and the ability to choose the right R&D directions are more critical now than ever before. Furthermore, with the advancement of new technologies, applications and ethical issues such as “gene-edited babies” are receiving unprecedented attention.

The emergence of strategic gaming implies a shift in stakeholders’ positions; the past mindset of collectively “expanding the pie” will transform, to some extent, into a “zero-sum game.” Once one party takes proactive measures, other parties will respond actively as well, leading to a new dynamic equilibrium.

Over the past week, several leading generic drug manufacturers that had passed the consistency evaluation bowed their heads in the face of the “4+7” volume-based procurement program. The magnitude of price reductions and the selection of a single winning bidder per product were largely unexpected. Key questions remain to be answered by time: how will the scope of included products expand? Will prices be further adjusted? Can procurement volumes be fully implemented? What happens after the contracted volumes are fulfilled? Can selected companies sustain their operations? Do they still have room for survival? Will their situation converge with that of foreign generic drug makers? Are pharmaceutical stocks still investable? Nevertheless, at least a few points are certain:

1. Technical Support: Regardless of whether innovation is encouraged, the domestic pharmaceutical market will maintain its generic drug-dominated structure in the medium term; [Innovation Takes Time]

2. Regulatory: Whether willing or not, the situation where survival depends on passing the consistency evaluation will not change; [Evasion is ineffective]

3. Channel Strategy: Regardless of whether volume-based procurement is implemented, the necessity of establishing a promotional team remains unchanged; [Prisoner's Dilemma]

4. Payment: Whether cost control is implemented or not, the reality that national medical insurance dominates will remain unchanged; [commercial insurance requires time]

5. On the supply side: The fundamental reality remains unchanged that product strength and academic validation, rather than merely whether prescriptions are dispensed outside hospitals, are the key factors; [Core Competitiveness]

As articulated in this article, the current landscape is characterized by a strategic interplay, wherein payers and regulators have achieved phased successes through a combination of measures. Market panic stems from uncertainty. However, viewed through the “New Pentagon” framework, volume-based procurement (VBP) is merely one policy instrument, and price reduction is not the ultimate objective; thus, excessive pessimism is unwarranted. The core national imperative is to replace high-priced imported originator drugs with high-quality, affordable generic alternatives, thereby ensuring patient access to cost-effective medications, sustaining the medical insurance system, and driving industrial upgrading. This goal represents a mutually desirable outcome for all stakeholders. It is foreseeable that the other three parties will also respond proactively, as no single policy will eliminate an industry’s viability. All parties possess both the willingness and the capacity to foster a new equilibrium and promote a more sustainably developed pharmaceutical market.

Furthermore, statistical data indicate that pharmaceutical costs and the proportion of drug revenue have been relatively effectively controlled, while total hospital revenue continues to rise. This suggests that healthcare institutions have developed more sustainable revenue streams, and “subsidizing medical services with drug profits” is no longer the primary target of current regulatory efforts.

Data Source: China Health and Family Planning Statistical Yearbook 2017

Data Source: China Health and Family Planning Statistical Yearbook 2017

Data source: China Health and Family Planning Statistical Yearbook 2017

In summary, the author believes that non-innovative drug companies should pay attention to the following trends:

1. In the medium term, injectables, non-289 listed drugs, and oral Chinese patent medicines will continue to maintain a robust market presence. Volume-based procurement (VBP) remains in the pilot phase, covering only more than 30 products. The key tasks ahead include expanding the pilot program, reviewing methodologies, and implementing VBP for the remaining varieties on the “289 List.” Adhering to a gradual policy implementation approach, a 3–5 year buffer period will be allocated to fully enact these reforms.

2. The outflow of prescriptions is urgent. Currently, medical insurance and tiered hospitals in pilot cities are phasing out adjuvant drugs and obsolete varieties within the scope of the 289 initiative. Due to issues such as information asymmetry and supply chain accessibility, the out-of-hospital market will serve as a venue for self-redemption for multiple drug varieties in the coming years. The term “out-of-hospital” here also includes the internet market.

3. Investment in active pharmaceutical ingredients (APIs) and R&D is more critical than ever before. Volume-based procurement serves as a comprehensive assessment, where price, quality, and supply stability are all indispensable. The supply of APIs determines the margin and sustainability of finished dosage forms, while investment in R&D is a prerequisite for market approval.

4. Innovation and collaboration are the only viable paths forward. Innovative drugs that align with clinical needs will be the key drivers of high pricing and high gross margins in the future; however, as most domestic pharmaceutical companies are small and medium-sized enterprises, joint R&D, shared investment, and effective utilization of CRO/CMO services are essential strategies for survival.

5. “Going global” is a viable strategy. China’s pharmaceutical market has gradually shifted from unregulated, rapid expansion to a mature and standardized landscape, fostering companies with strong comprehensive capabilities. As China’s international influence continues to grow and the benefits of its membership in the International Council for Harmonisation of Technical Requirements for Pharmaceuticals for Human Use (ICH) become increasingly apparent, overseas markets represent an accessible and lucrative opportunity.

China’s pharmaceutical market has its own unique characteristics, which have taken shape over a long period. We cannot simply replicate any other country’s healthcare system, nor will we follow the same path of pharmaceutical development as other nations. Although imperfections remain, China’s healthcare reform has been successful and is continuously improving. We also believe that the government has the resolve and wisdom to address the current challenges.

A new landscape in the pharmaceutical industry has taken shape, growing increasingly complex under the influence of shifting macroeconomic conditions. Although winter has arrived, we remain committed to the healthcare sector because it embodies both the humanitarian mission of healing and saving lives and the resilience of counter-cyclical stability; it offers the excitement of exploring life’s infinite possibilities while grounding us in policy compliance and agile adaptation to changing circumstances.

At this moment, though a thousand words spring to mind, I wish only to quote the famous line by the poet Shi Zhi: “Believe in the Future!”