Pharmaceutical Industry Transformation: Which Companies Will Thrive in the New Era?

Editor’s Note: This article was compiled by E-Drug Manager from the Haitong Securities research report “Innovation and Non-Pharmaceutical Leaders Drive Rapid Industry Growth,” authored by Yu Wenxin.

Since the implementation of the “4+7” volume-based procurement program, there has been widespread debate and divergent views across the market. However, one point has achieved universal consensus: the policy direction—endorsed from the national level down to the National Medical Products Administration (NMPA)—of encouraging innovative drug R&D, accelerating priority review for clinically urgent medicines, and implementing consistency evaluation for generic drugs is firmly established.

Two decades of pharmaceutical industry development have demonstrated that the growth of the payer side—specifically, medical insurance—is a primary determinant of overall industry expansion. Against the backdrop of stringent cost containment, expanding revenue sources and reducing expenditures have become imperative for the medical insurance system. The establishment of the powerful National Healthcare Security Administration signals its strengthened authority in determining “what to purchase” and “at what price.” For generic drugs, pilot programs linking volume-based procurement with price reductions have been implemented, ultimately leading to the adoption of medical insurance payment standards that compel price cuts for both generics and off-patent originator drugs. Consequently, amid robust negotiations by the medical insurance authorities, innovative medicines remain the most promising direction for the pharmaceutical industry. While market concentration among domestically produced generics continues to rise, these products face significant short-term pressure from price reductions.

2015 is regarded as the inaugural year of transformative change in China’s new drug policies: beginning with the “722” self-inspection initiative, clinical data in China entered an era of standardization. In the same year, the implementation of the Marketing Authorization Holder (MAH) system marked the formal launch of innovative drug reform in China. In 2016, the China Food and Drug Administration (CFDA) issued the Work Plan for Reforming the Classification System for Chemical Drug Registration, which overhauled the existing classification framework for chemical drug registration. The reform aimed to encourage new drug development, enforce rigorous review and approval processes, enhance drug quality, and promote industrial upgrading.

In terms of review and approval, in November 2015, the former China Food and Drug Administration (CFDA) issued the "Announcement on Several Policies for Drug Registration Review and Approval," proposing a one-time approval system for clinical trials to streamline the review process. In 2016, to address the backlog of approval documents, the CFDA introduced a priority review policy, which significantly accelerated the market launch of innovative drugs with clear clinical value. In 2018, measures such as the filing system for clinical trial institutions and the default approval system for expired clinical trial applications were implemented, shifting the regulatory focus from pre-approval to process-based supervision.

In 2017, China joined the ICH, allowing MRCT data to be used for registration applications, conditionally accepting overseas clinical data, and permitting simultaneous Phase I clinical trials both within and outside China. In April 2018, the Premier of the State Council announced at the State Council executive meeting a series of measures aimed at encouraging innovative drug R&D, including granting up to five years of patent term extension for innovative drugs applying for market approval simultaneously in China and abroad, delaying the approval of generic drugs, reducing taxes on anticancer drugs, and implementing dynamic adjustments to the National Reimbursement Drug List (through pharmaceutical price negotiations). These measures further lowered barriers to the importation of foreign drugs.

The volume-based procurement initiative is widely regarded by the market as a catalyst that will enable pharmaceutical companies with strong innovation capabilities and substantial R&D investment to survive this round of industry consolidation and gradually grow stronger.

Supported by policy incentives in recent years, the domestic innovative drug environment has significantly improved. Taking domestically developed new drugs as an example, eight products are expected to gain marketing approval in 2018, far exceeding previous market expectations. The most representative among them are Anlotinib from Sino Biopharmaceutical and Fruquintinib from Hutchison MediPharma.

Data Source: CDE, Insight, Haitong Securities Research Institute

Anlotinib, a Class 1.1 novel anti-tumor drug independently developed by Chia Tai Tianqing, has seen sales volumes surge far beyond market expectations since its launch in June, positioning it as potentially the fastest-growing innovative drug in China currently. In the October national medical insurance reimbursement negotiations for anticancer drugs, Anlotinib was the only domestically developed innovative drug included. The market prospects afforded by medical insurance coverage are expected to drive further growth in Anlotinib’s sales volume.

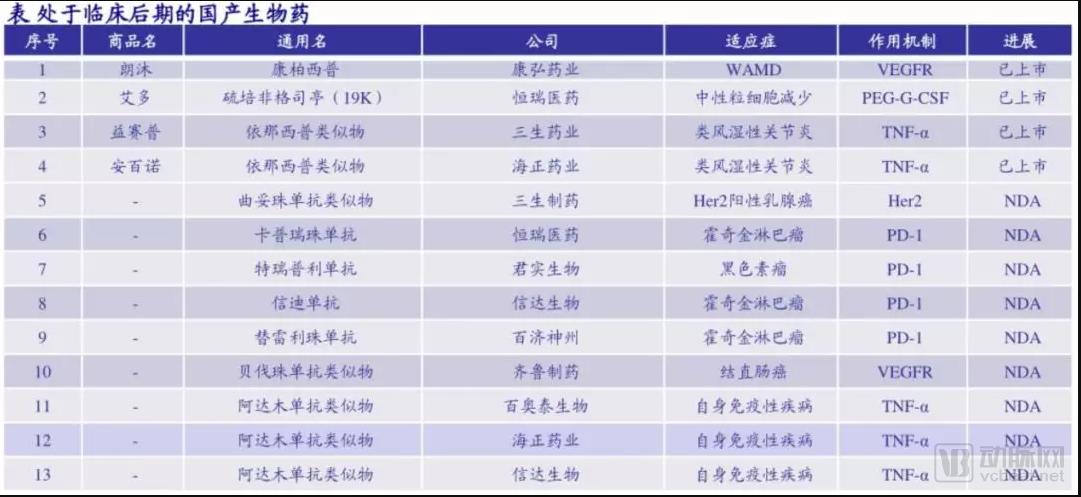

Among the domestically developed new drugs nearing approval, Innovent Biologics’ sintilimab, Hengrui Medicine’s camrelizumab, Junshi Biosciences’ toripalimab, and BeiGene’s tislelizumab are also noteworthy candidates. If successfully approved for market launch, they would become strong competitors to Opdivo and Keytruda, currently the only broad-spectrum anticancer drugs available.

Biopharmaceuticals are gaining increasing global popularity due to their superior efficacy, with top-selling drugs predominantly being biologics, including the “blockbuster” Humira and Roche’s “three major monoclonal antibodies.” Although China’s biopharmaceutical industry started late, substantial investments in capital and talent have propelled it into a phase of commercial realization. Currently, the first biosimilars of adalimumab, rituximab, trastuzumab, and bevacizumab have all submitted production applications; among these, three manufacturers have filed for adalimumab, and four have filed for PD-1 monoclonal antibodies. The first domestically produced biosimilar, rituximab, is also on the verge of approval.

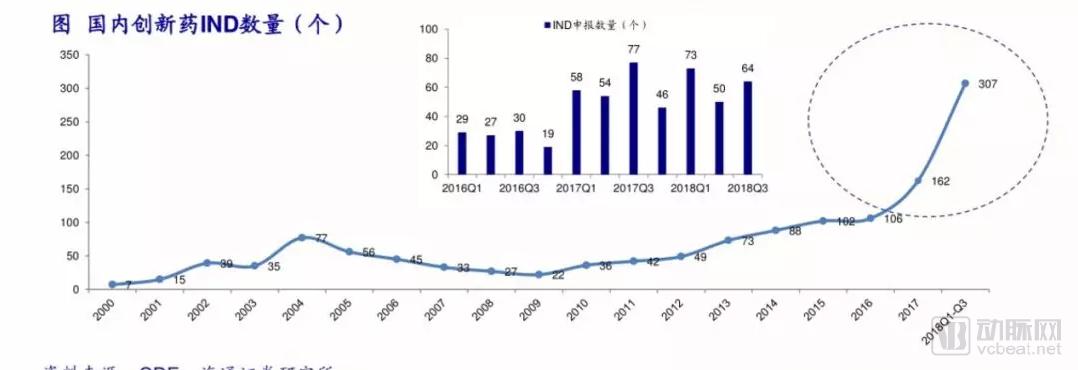

From a temporal perspective, 2015–2016 marked a new starting point for China’s innovative drug industry. In terms of the number of innovative drug applications: the period from 2003 to 2006 witnessed the first wave of application peaks, while 2013 ushered in the second major wave of applications. These candidates are expected to enter late-stage clinical trials and reach the market sequentially after 2020. Since the first quarter of 2017, the number of Investigational New Drug (IND) applications for domestically produced innovative drugs has accelerated, a trend that persisted through the third quarter of 2018 without any significant slowdown. The continuous growth in IND applications has ensured that the underlying trajectory of the innovative drug industry remains unchanged.

Source: CDE, Haitong Securities Research Institute

Investment in new drug development largely depends on financing conditions in the primary market. Since the fourth quarter of 2017, Hong Kong stock listings by biotech companies have provided an additional exit channel for primary-market investors. With the A-share market also set to allow initial public offerings (IPOs) by pre-profitability companies, both the pricing and scale of financing are expected to grow rapidly. Although financing activity in the pharmaceutical industry has cooled since the third quarter of 2018, the launch of the STAR Market is poised to further reinvigorate investor enthusiasm for sector financing.

In contrast, when looking at the U.S. stock market, innovative pharmaceutical companies demonstrate stronger market performance and higher market capitalization ceilings. Currently, there are 19 listed pharmaceutical companies in the United States with market capitalizations exceeding $40 billion, all of which are innovative drug companies. Among the 11 pharmaceutical companies with market capitalizations between $5 billion and $20 billion, seven outperformed the S&P 500 Index over the past five years, while four underperformed. The companies that outperformed the index were all innovative drug companies, including Actelion, Allergan, Incyte, Vertex, Seattle Genetics, and BioMarin. Those that underperformed were all generic drug companies: Grifols (blood products), Mylan, Dr. Reddy’s, and Perrigo.

In the realm of innovation within the pharmaceutical industry, the pharmaceutical outsourcing sector is by no means an industry reliant on cheap labor exports. It demands a substantial workforce of professionals specializing in chemistry, biology, clinical medicine, statistics, and engineering. China’s accumulated base of highly educated individuals has laid a solid foundation for the “scientist dividend” in its pharmaceutical industry. Taking science and medical talent as examples, although there remains a gap in absolute numbers compared to India, the abundant supply of high-quality, cost-effective STEM and medical professionals has kept China’s R&D costs consistently lower than those in Europe and the United States, with labor costs even undercutting those of Indian companies.

Compared with the software outsourcing industry, the unique policy environment has created higher barriers to entry. Driven by sustained increases in R&D investment for innovative drugs and a rising outsourcing rate, pharmaceutical CROs, as R&D service providers, have continued to benefit, leading to a steady improvement in industry prosperity. Over the past 20 years, the industry index has significantly outperformed both pharmaceutical companies and the S&P 500. At the company level, excluding the impact of the 2008 financial crisis on R&D spending by pharmaceutical manufacturers, leading pharmaceutical CRO companies maintained sustained and rapid growth over the more than 20-year period from 1993 to 2017.

Source: Wind, Haitong Securities Research Institute

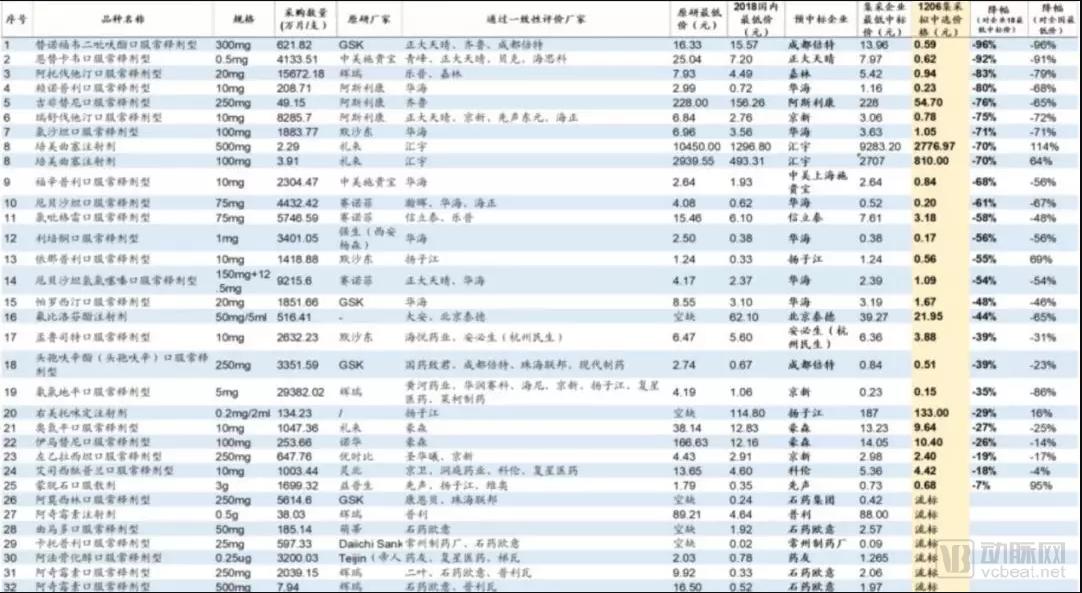

On December 6, the centralized procurement negotiations were finalized, with 25 out of 31 pilot generic drugs selected as proposed winners. Compared to the lowest procurement prices for the same drugs in pilot cities in 2017, the average price reduction for the proposed winners exceeded 50%, with a maximum reduction of 96%.

Source: Shanghai Pharmaceutical Affairs Network, PDB, CDE, Haitong Securities Research Institute

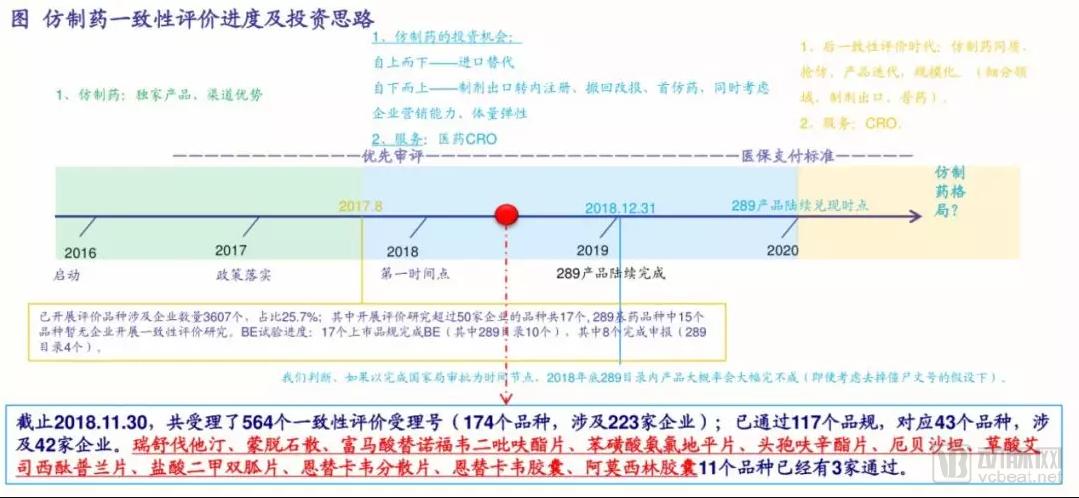

Key issues that will remain in the industry’s focus include how to align with medical insurance payment standards, whether winning bid prices will be linked to tender prices across all provinces in China, the mechanisms of such linkage, how to ensure the fulfillment of procurement volumes, and how to allocate the surplus medical insurance funds. For generic drug manufacturers that have long benefited from the “generic dividend,” competitiveness in the market will gradually erode if their product portfolios are overly concentrated and heavily reliant on a single flagship product.

The medical insurance reimbursement mechanism (payment standards) is the policy that will have the greatest impact on product pricing and market space from the payment side for varieties that have resolved quality issues through future consistency evaluations, and it will also significantly affect the profitability of pharmaceutical companies. Drawing on Japan’s experience, after re-evaluation resolves quality issues, drug prices continue to decline under the medical insurance reimbursement mechanism (the core lies in hospitals’ secondary price negotiations, similar to the GPO models in Shanghai and Shenzhen), during which process the market share of domestic generic drugs continues to rise.

Source: CFDA, CDE, Xinhu Pharma News, Haitong Securities Research Institute

Therefore, to establish a firm foothold amidst intense market consolidation, generic drug manufacturers will need to cultivate three core competitive advantages in the future: a robust product pipeline (diverse portfolio), high barriers to entry for product imitation (limited competition), and unique cost-control capabilities. Consequently, in the short term, the performance and valuations of the generic drug sector will remain under pressure, while OTC market leaders unaffected by policy changes, such as Jichuan Pharmaceutical and Pien Tze Huang, will seize new opportunities.

According to information currently available to E-managers from investment institutions and securities firms, amid the rapidly changing market environment—and particularly in light of the pessimistic sentiment triggered by the recent volume-based procurement (VBP) policy—the non-pharmaceutical segment within the healthcare industry is poised to emerge as a standout performer, with the medical device sector continuing to attract strong optimism. Unlike the pharmaceutical industry, the non-pharmaceutical sector is less susceptible to policy impacts and benefits from inherent technological or service-related “moats,” thereby offering more sustainable and predictable future growth.

In the non-pharmaceutical industry, the chain business model—encompassing chain medical services and chain pharmacies—offers the most certain growth trajectory. Among these, chain medical services exhibit the fastest growth rate and the most favorable industry environment. High fixed costs create significant barriers to entry for potential competitors, making first-mover advantage and capital investment critically important. Relevant enterprises are trending toward consolidation to achieve economies of scale, whereby acquiring new customers rapidly reduces unit fixed costs.

Taking Aier Eye Hospital as an example, from 2009 to 2017, the company’s revenue grew from RMB 610 million to RMB 5.96 billion, representing a compound annual growth rate (CAGR) of 33%; net profit attributable to shareholders increased from RMB 92.48 million to RMB 740 million, with a CAGR of 30%; net profit attributable to shareholders after deducting non-recurring gains and losses rose from RMB 91.81 million to RMB 777 million, achieving a CAGR of 31%; and its market capitalization expanded from RMB 7 billion to RMB 68 billion, marking a nearly tenfold increase over eight years. In the view of industry experts, Aier Eye Hospital has demonstrated consistent performance improvement, and its market valuation has withstood market tests. In addition to well-executed strategic layout and enhanced brand influence, the gradual realization of various incentive mechanisms has also continuously unleashed endogenous growth momentum.

Currently, the demand for ophthalmic medical care and optometry services in China is growing. Furthermore, as China gradually enters an aging society, the incidence of eye diseases such as cataracts and diabetic retinopathy is increasing day by day. In the third quarter of 2018, Aier Eye Hospital reported a year-on-year revenue increase of 31%, maintaining rapid growth. As the leading chain provider of medical services continues to expand its scale, its brand and cost advantages will become increasingly prominent, and its market share is expected to rise steadily.

The expansion capability of chain pharmacies is essentially their ability to secure resources in new regions. Companies with superior merger and acquisition (M&A) integration capabilities are better positioned to gain a competitive edge in this race for market share. Listed companies led by Laobaixing Pharmacy and Yifeng Pharmacy have demonstrated strong performance in integrating acquired stores. Lanzhou Huirentang’s revenue and profit in 2016 exceeded its performance commitments by 21% and 37%, respectively, while in 2017, they surpassed the targets by 37% and 27%, respectively. Baixinyuan’s revenue and profit in 2016 exceeded expectations by 18% and 13%, respectively, and in 2017, they outperformed the performance commitments by 30% and 6%, respectively.

In such a highly fragmented pharmacy retail industry, the core competitiveness hinges on two pillars: supply chain efficiency and specialized professional services. Modernized distribution logistics, combined with high inventory turnover and economies of scale that enhance bargaining power with upstream suppliers, enable cost compression and wider profit margins. Meanwhile, specialized professional services constitute a stronger competitive barrier. Non-service-related processes can be marginally optimized through internet technologies and information systems (such as intelligent pharmaceutical management), thereby amplifying scale effects. Regulatory trends—including the outflow of prescriptions from hospitals, tiered and classified management of pharmacies, and medical insurance policies—have raised entry barriers for smaller enterprises, further intensifying the Matthew Effect.

Generally speaking, the barriers to entry and market ceilings in the medical device sector are not as high as those in the pharmaceutical industry. Given the relatively low barriers, companies must possess sustained innovation capabilities to continuously launch new products, thereby widening the gap with competitors and mitigating the impact of price reductions. For instance, leading medical device companies continually introduce new stents; bioresorbable stents have now evolved to the fourth generation, which not only outpaces competitors but also stabilizes prices. Similarly, Sonoscape Medical persistently launches new color Doppler ultrasound systems, and Adicon introduces novel tumor detection reagents. Since blockbuster products are far less common in medical devices than in pharmaceuticals, a lower market ceiling necessitates continuous expansion of product categories. For example, leading stent manufacturers are actively expanding into cardiovascular pharmaceuticals through external growth strategies.

Among medical device companies, the most prominent is Mindray Medical, which hit multiple daily upper limits shortly after its listing on the ChiNext board and has now joined the “RMB 100 billion club.” Known as the “Huawei of Healthcare,” Mindray ranked among the top in China in 2017 for market share across its patient monitoring line (including patient monitors, anesthesia machines, and defibrillators), ultrasound product line, and in vitro diagnostics line (including clinical chemistry and hematology analyzers), thereby breaking the long-standing dominance of the “GPS” trio (GE, Philips, and Siemens). With Mindray’s technological prowess and customer reputation continuing to rise synergistically, it is well positioned to capture additional market share and become a leading force in import substitution.

Source: “Statistical Yearbook of the National Health and Family Planning Commission,” Haitong Securities Research Institute. All data are based on terminal-level figures.

As of 2017, the global medical device market was valued at approximately USD 403 billion, with an industry growth rate of 5%. In China, the market size reached RMB 458.3 billion, with an industry growth rate of 24%. As a high-end new economy manufacturing sector prioritized by the Chinese government, the medical device industry aligns with trends in industrial upgrading and benefits from policy support. Driven by the broader trends of tiered diagnosis and treatment and import substitution, medical devices offer significant long-term investment value. Since 2016, the growth rate of listed companies and large-scale enterprises has surpassed the overall industry average, indicating that import substitution is actively underway. With the rise of a cohort of outstanding domestic medical device companies, shortened technology iteration cycles, and the demographic dividend from China’s vast population, demand for medical devices in China continues to hold substantial growth potential.

Furthermore, following the major vaccine incident, market bearish sentiment has gradually been absorbed. In addition, Hualan Biological Engineering’s quadrivalent influenza vaccine was approved in June this year. Given that quadrivalent vaccines offer superior protection compared to trivalent vaccines, and the WHO first recommended prioritizing the use of quadrivalent influenza vaccines in 2018, coupled with unchanged end-user demand in the industry, short-to-medium-term channel adjustments driven by policy will not alter the long-term high-growth trajectory. Currently, the entire industry is showing signs of a moderate recovery.

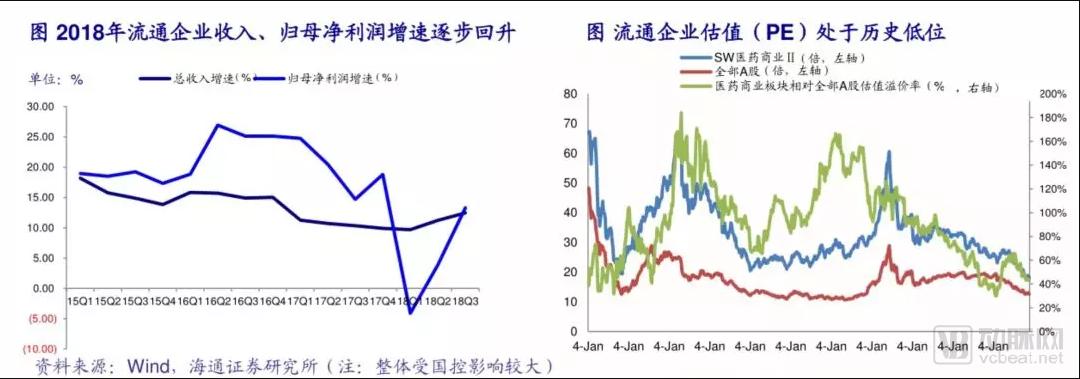

Affected by factors such as controls on the proportion of drug revenue, price reductions in centralized procurement, and the “two-invoice system,” the revenue growth of listed pharmaceutical distribution companies declined in 2017. As the negative impact of these policies gradually subsided, both revenue growth and net profit attributable to parent company shareholders for distributors began to recover in 2018, while valuations remained at historic lows. With an imminent inflection point toward accelerated industry consolidation, valuations and relative premium ratios in the pharmaceutical commercial sector are at historic lows, making it an opportune time for long-term strategic positioning.

Source: Wind, Haitong Securities Research Institute (Note: The overall performance is significantly influenced by Sinopharm)