Current Landscape and Product Overview of the Tumor Immunotherapy Industry

Editor’s Note: This article is reprinted from Huoshi Chuangzao, authored by Zhou Hang.

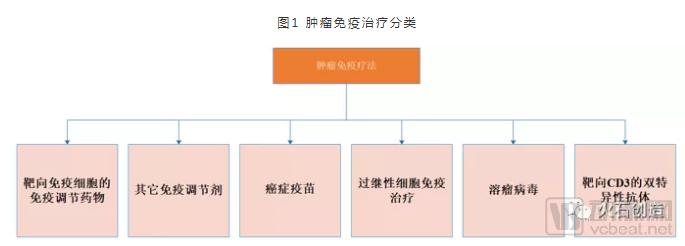

Immuno-Oncology Therapy (I-O) refers to a therapeutic approach that activates the body’s immune system to destroy tumor cells. Based on their distinct mechanisms of action, immunotherapeutic agents can be categorized into six major classes.

Source: Compiled by Huoshi Research Institute

1. The global market size for oncology immunotherapy has surpassed $50 billion, with the potential to reach the $100 billion range in the future

Among cancer treatment modalities, immunotherapy has garnered the most attention due to its advantages, including high efficacy, minimal side effects, and prevention of recurrence. The emergence of immunotherapy has not only revolutionized the standards of cancer treatment but also fundamentally transformed the conceptual approach to oncology, earning it recognition as the third revolution in cancer therapy, following traditional chemotherapy and targeted therapy. Currently, tumor immunotherapy is still in its early stages of development, representing a highly promising sector within an already burgeoning industry. According to data from EvaluatePharma, the global market size for tumor immunotherapy reached $61.9 billion in 2016. Driven by continuously rising market demand, the market size has been steadily expanding and is projected to grow to $120 billion by 2021, with a compound annual growth rate (CAGR) exceeding 14%.

Source: EvaluatePharma

2. Currently, there are few marketed products; however, with the rapid development of tumor immunotherapy, the number of global oncology immunotherapy drugs will continue to grow.

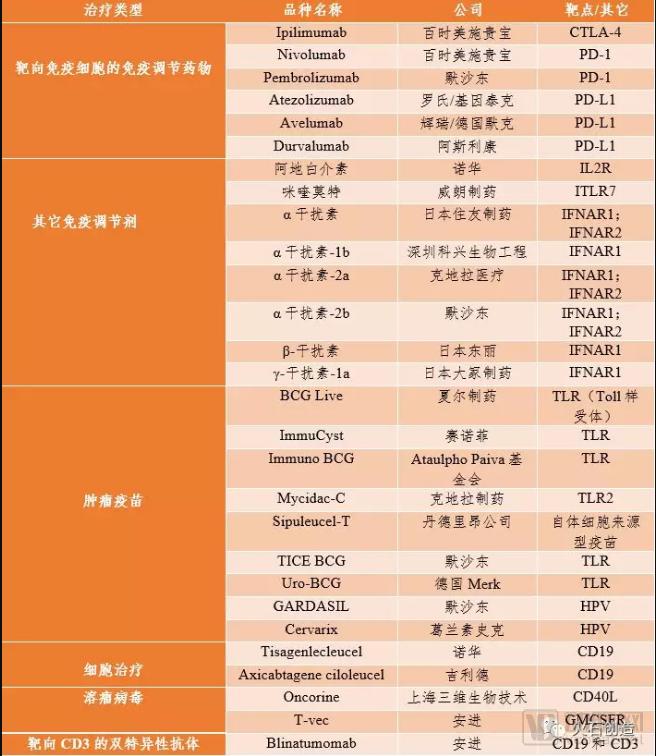

Immunotherapy is hailed as the most promising approach for conquering cancer. After a protracted 136-year journey of research and development, particularly in the past decade, technologies such as PD-1 inhibitors and CAR-T therapy have successfully transitioned from scientific achievements to clinical applications. As of September 2017, dozens of tumor immunotherapy products had received marketing approval worldwide. (Table 1-1 lists only a subset of these products: six immunomodulatory drugs targeting immune cells; eight other immunomodulators; nine cancer vaccines; two adoptive cell immunotherapies; two oncolytic viruses; and one bispecific antibody targeting CD3.) Between September 2017 and September 2018 alone, the number of global drug development projects in the tumor immunotherapy market surged by 67%, rising from 2,031 to 3,394. Among these, adoptive cell therapies exhibited the fastest growth, increasing from 400 to 851 projects, representing an approximate growth rate of 113%. Driven by growing enthusiasm from academic institutions and the industry, the development of highly promising tumor immunotherapies is expected to maintain a rapid pace of growth.

Table 1. Selected Marketed Oncology Immunotherapy Products Worldwide

Source: Public information, Firestone Creation

Source: Nature Reviews Drug Discovery

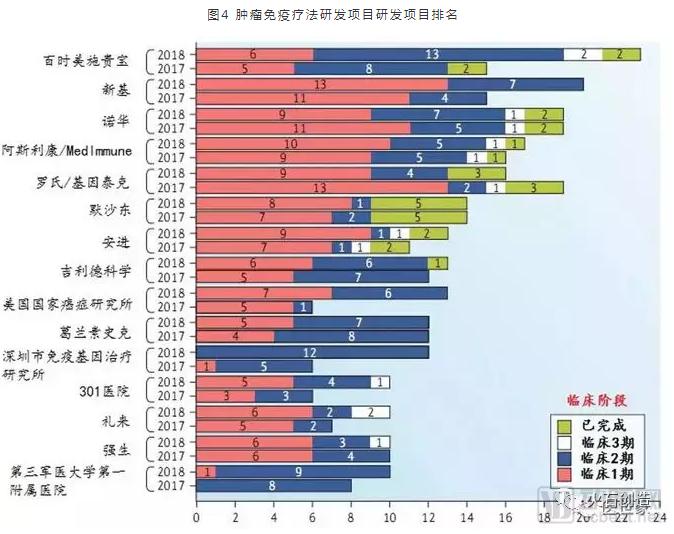

3. The number of research institutions and enterprises involved in the development of tumor immunotherapy projects worldwide continues to grow. Chinese research institutions have aligned their R&D capabilities with global standards and are emerging as prominent players in the global ranking of tumor immunotherapy R&D projects.

As of September 2017, a total of 461 academic and industrial organizations worldwide were engaged in the research and development of 964 clinical projects in cancer immunotherapy. One year later, the number of these organizations increased by 42% to 655, while the number of clinical projects rose by 34% to 1,287. Among the top 15 institutions in terms of R&D projects, large pharmaceutical companies continued to dominate, occupying the top eight positions. Four research institutions were also ranked among the top 15, three of which were from China: the Shenzhen Institute of Immune Gene Therapy, the 301 Hospital (Chinese PLA General Hospital), and the First Affiliated Hospital of the Third Military Medical University.

Source: Yi Shi Xiang, Nature Reviews Drug Discovery

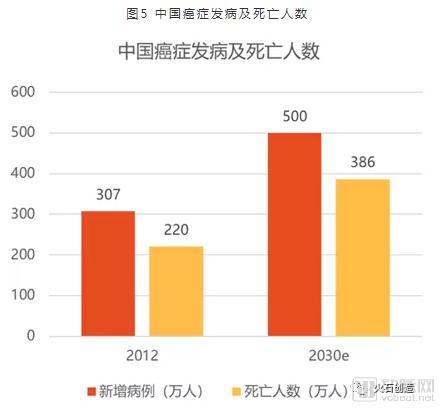

1. China has a large population of cancer patients, the market size for oncology drugs continues to expand, and the cancer immunotherapy industry is full of vitality

In 2012, the number of cancer patients in China reached 3.07 million, with 2.2 million deaths. According to global projections for cancer incidence and mortality, it is estimated that by 2030, there will be 5 million new cancer cases in China, with the number of deaths reaching 3.86 million. Between 2013 and 2017, the market size of anti-tumor drugs in China grew steadily, increasing from RMB 83.4 billion to RMB 139.4 billion, while its share of the Chinese pharmaceutical market rose from 8.4% to 9.7%. According to Frost & Sullivan’s forecasts, the compound annual growth rate (CAGR) of China’s anti-tumor drug market was approximately 13.5% from 2017 to 2022, and is projected to be around 12.1% from 2022 to 2030. The sales revenue of the anti-tumor drug market is expected to reach RMB 262.1 billion in 2022 and RMB 654.1 billion in 2030.

Source: Global cancer incidence and mortality projections, compiled by Firestone Creation

Source: Frost & Sullivan

Over the past 30 years, cancer mortality in China has increased by 80%, yet the current cancer cure rate in the country stands at only 25%, significantly lower than the 65% observed in developed nations. The rising incidence and mortality rates of cancer are driving innovation in anti-tumor therapies in China. As a cutting-edge frontier in the industry, tumor immunotherapy holds broad application prospects.

2. China’s R&D capabilities in tumor immunotherapy are aligned with global standards, offering broad development potential in areas such as adoptive cell therapy and immune modulators targeting immune cells.

Compared with traditional chemical drugs, China has a smaller gap with developed countries in the cutting-edge technology of tumor immunotherapy, and its R&D level is in line with the world. The world's first marketed oncolytic virus is H101, a genetically modified oncolytic adenovirus developed by Shanghai Sunway Biotech Co., Ltd. in China. This product was approved for marketing by the CFDA in 2005 for the treatment of head and neck tumors. Among eight other immunomodulators, one is interferon alpha-1b, which targets the IFNAR1 receptor and also comes from Shenzhen Kexing Biological Engineering Co., Ltd. in China. Currently, this drug has been approved for the treatment of indications such as chronic hepatitis B, hepatitis C, and hairy cell leukemia.

China Joins the First Tier of CAR-T Clinical Research

The United States was the first country globally to initiate clinical trials of CAR-T cell therapy; prior to 2010, all registered CAR-T clinical trials worldwide were concentrated in the U.S. Starting in 2011, Europe also began registering CAR-T clinical trials. From 2012 onward, China’s PLA General Hospital (301 Hospital) started registering CAR-T clinical trials. As of August 2017, China had registered 111 CAR-T clinical research projects on ClinicalTrials.gov, surpassing Europe in number and ranking second only to the United States. This figure accounted for more than 40% of the global total and showed a year-on-year increasing trend.

Source: ClinicalTrials.gov, compiled by Firestone Creation

The market for immune modulators targeting immune cells in China is fiercely competitive, and Junshi Biosciences' toripalimab will become the first PD-1 antibody drug to be launched domestically.

Two imported PD-1 antibodies (Opdivo/Keytruda) have already been approved for marketing by China’s Center for Drug Evaluation (CDE), marking China’s entry into a new era of cancer immunotherapy. Leveraging the country’s large population of cancer patients, these two imported PD-1 antibody drugs are priced at the lowest levels globally within the Chinese market. The official suggested retail price for Bristol-Myers Squibb’s Opdivo is RMB 9,260 per 100 mg and RMB 4,591 per 40 mg, significantly lower than its selling prices in other countries. Merck & Co.’s Keytruda has a suggested retail price of RMB 17,918 per 100 mg, which is only half of its price in the United States.

Compared with the PD-1 inhibitors already on the market, competition among those not yet launched is more intense, with more than 20 candidates in clinical stages in China alone. On December 4, 2018, Junshi Biosciences’ PD-1 antibody passed technical review and entered the administrative approval phase, positioning it to potentially be the first to market. To date, besides Junshi, the other three companies in the first tier of domestic PD-1 inhibitor development—Hengrui Medicine, BeiGene, and Innovent Biologics—have also submitted marketing applications.

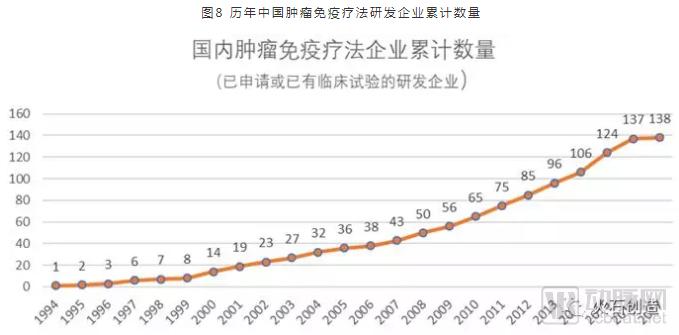

3. The number of innovative enterprises engaged in the research and development of tumor immunotherapy in China has been increasing year by year, primarily concentrated in regions such as Shanghai, Jiangsu, Beijing, and Guangdong.

In China, innovative companies engaged in the research and development of tumor immunotherapy have witnessed rapid growth this year. According to incomplete statistics, by 2017, the number of enterprises across China that had either applied for or already initiated clinical trial projects for tumor immunotherapy reached 138, showing a year-on-year upward trend.

Source: Firestone Creation

China’s oncology immunotherapy R&D enterprises are primarily concentrated in Shanghai, Jiangsu, Beijing, and Guangdong. Among them, Jiangsu is home to 33 companies, represented by Gracell Biotechnologies, Innovent Biologics, Alphamab Oncology, and Sanpower Group; Shanghai hosts 30 companies, represented by Junshi Biosciences, Cytotherapy, and Henlius Biotech; Beijing has 21 companies, represented by BeiGene, BioThera Solutions, and ImmuneOnco; and Guangdong accounts for 12 companies, represented by Source Positive Cell Therapy, Heyi Kang, and Bio-Thera Solutions.

Source: Firestone Creation