2018 Future Healthcare Industry Report: A Five-Year Review of Medical Innovation Practices

On December 18, the 2018 Future Healthcare Top 100 Forum, hosted by VCBeat, Eggshell Research Institute, and Future Medical Academy, and co-hosted by Legend Capital, BV Baidu Ventures, KPMG China, and Health Intelligence Valley, will grandly open at the Renaissance Beijing Capital Hotel. This is an annual branded forum event organized by VCBeat and stands as one of the most influential forums in the innovative healthcare industry.

The theme of this forum is “Trend ING,” aiming to bring together the most leading healthcare innovation enterprises, listed companies, financial institutions, and medical organizations from both domestic and international markets. The forum will explore the future direction of the healthcare wave from perspectives such as industry transformation trends, technological evolution, edge innovation, traditional sector transition, and capital flow dynamics.

The Future Healthcare Top 100 Forum attracted over 2,500 participants and featured 12 themed forums, namely: the Main Forum on Future Healthcare, the Internet + Smart Hospital Forum, the Innovative Health Insurance Forum, the BIO/NGS Frontier Forum, the Forum on Innovation in Health Management Models, the Forum on Innovative Practices in Intelligent Imaging, the Super Unicorn Forum, the Forum on Innovative Development of Specialty Chain Services, the Forum on the Development of the Innovative Oncology Drug Industry, the Forum on Medical Big Data Technology and Industrial Applications, and the Third-Party Medical Services Forum, covering the top 10 most watched sectors in 2018.

At this forum, VCBeat released the “2018 Internet Hospital Report” and the “2018 Future Healthcare Industry Report.” At the event, Li Datao, founder of VCBeat, and Wang Xiaocen, partner at CEC Health Industry Fund, shared their insights. This article is an excerpt from the “2018 Future Healthcare Industry Report,” which will be officially released on December 18, 2018. Instructions for accessing the full report are provided at the end of this article.

Table of Contents

Chapter 1: Five-Year Development Trajectory in the Medical and Health Sector

I. Policy Context: Five Achievements of Healthcare Reform Over the Past Five Years

II. Capital Trajectory: Significant Progress Over Five Years, 2018 Was a Challenging Year

2014: The Emergence of Internet Healthcare and Rapid Growth in the Genomics Sector

2015: A Flourishing Healthcare Sector and the Prime Window for Startups

2016: Marginal Expansion, Internet Healthcare Gains Attention

2017: Model Falsification, Growth-Stage Companies in High Demand

2018: The Biological Sector Gains Attention as Artificial Intelligence Rises

III. Industry Context: Five Years of Development, with Technological Innovation as the Greatest Driving Force

Internet Healthcare

Biotechnology

Artificial Intelligence

Chapter 2: Transformation—Five Major Trends in Healthcare in 2018

Policy Changes in the Pharmaceutical Sector in 2018

Payment Reform

Channel Transformation

Technological Transformation

Service Transformation

Chapter 3: Release of the Future Healthcare Top 100 List

I. 2018 Future Healthcare 100 · China Healthcare List TOP 100

II. 2018 Future Healthcare 100 · Top 100 Chinese Pharmaceutical Companies

III. 2018 Future Healthcare 100 · China Health List TOP 30

Chapter 4: Analysis of the Growth Trajectories of the Top 100 Companies

I. Interpretation of the Top 100 List Data

II. Growth Pathways of the Top 100 Enterprises

III. Analysis of Key Elements of Competitiveness for Large Enterprises

1. The key elements of competitiveness in the startup phase are technological strength and first-mover advantage

2. The key element of competitiveness for growth-stage enterprises is the possession of effective medical resources

3. The key element of competitiveness for mature-stage enterprises is how to build a closed-loop business model

4. Key Factors Model for the Growth of Healthcare Enterprises

2018 was a year of transformation in the healthcare sector, with China achieving a series of accomplishments in its reforms. Healthcare service capacity was strengthened, public health service capabilities were improved, management of medical institutions became increasingly standardized, coverage of medical insurance services was further expanded, regulatory authorities continuously increased their support for innovative drugs, and healthcare-related innovative technologies emerged in rapid succession.

At the policy level, the development of private medical institutions has been supported by national policies, with further liberalization in the establishment and approval of clinics. On the domestic regulatory front, the market launch process for innovative and imported drugs has been accelerated, with green channels established for the approval of innovative drugs, thereby shortening the R&D and approval cycles. The PD-1 inhibitors Opdivo and Keytruda have been approved for marketing in China, significantly improving access to these therapies for Chinese cancer patients. Meanwhile, adjustments to the National Reimbursement Drug List have created favorable conditions for domestically produced innovative drugs to be included in the reimbursement list.

From a technological perspective, new technologies and therapies in the pharmaceutical field are emerging one after another. The application of emerging treatments such as PD-1 inhibitors, breakthroughs in gene therapy, and the successive approvals abroad of RNAi drugs and antisense RNA drugs have significantly increased the likelihood of conquering cancer within the biotechnology sector. AI-powered healthcare products are gradually reaching maturity, with multiple AI solutions being implemented across various hospital departments and application scenarios. Advances in information technologies, including artificial intelligence, smart hardware, the Internet of Things (IoT), and 5G, enable these digital tools to play a substantial role not only alongside pharmaceuticals but also in early disease screening, treatment, and rehabilitation.

In terms of payment, the National Healthcare Security Administration (NHSA) was established in 2018, assuming critical responsibilities for the management of medical insurance funds and cost containment. The number of medicines included in the National Essential Medicines List (2018 Edition) increased from 520 to 685, with new additions comprising 12 oncology drugs and 22 other varieties, such as clinically urgent pediatric medications. Under the new essential medicines system, generic drugs that have passed the consistency evaluation will be prioritized for inclusion in the list, encouraging healthcare institutions to prioritize their procurement and use. Meanwhile, import tariffs on oncology drugs were abolished, and the NHSA included 17 anti-cancer drugs in Category B of the National Basic Medical Insurance, Work-Related Injury Insurance, and Maternity Insurance Drug Catalogs. These measures reflect the focus of medical insurance on common diseases, chronic conditions, and critical illnesses among residents.

At the capital level, the macroeconomic situation slowed down in 2018, accompanied by policy and funding tightening, as well as trade frictions between China and the United States. The capital market became more cautious; although the total investment amount increased year-on-year, it tended to favor more stable mid-to-late stage projects. Companies in the healthcare sector demonstrated strong financing demands, with their business models gradually taking shape. In terms of IPOs, the Hong Kong Stock Exchange launched a special channel for biotechnology companies, allowing pre-revenue biotech firms to apply for listing.

However, transformation is never achieved overnight. Over the past five years, continuous changes in policy and technology within the healthcare sector have given rise to new opportunities in the health industry, and the ongoing transformation in healthcare will undoubtedly drive further development of the industry. VCBeat has summarized the transformations in the healthcare sector in recent years, with a particular focus on analyzing the changes that occurred in 2018. We have identified Chinese innovative enterprises that truly represent the future of healthcare by screening non-listed companies (including those listed on the New Third Board) in China’s healthcare sector. Accordingly, we have released multiple rankings for 2018 covering medical services and medical technology, pharmaceuticals, and general health, with the aim of uncovering the core forces shaping the future of healthcare in China.

VCBeat was founded in 2014, amid the rapid expansion of mobile internet. By 2018, it had been exactly five years. Over this period, we have had the privilege of witnessing the swift development of the healthcare sector through more than 20 million words of written records. Every industry follows its own developmental patterns. In the face of disruptions from emerging trends, technological advancements, and shifting policies, disruptive innovators are breaking free from the constraints of traditional healthcare. In this report, we attempt to trace the evolution of the healthcare sector across policy, industry, and capital dimensions by reviewing our past archives, observe the changes over these five years, and summarize the underlying patterns.

Policy Context: Five Achievements of the Five-Year Healthcare Reform

Since the 18th National Congress of the Communist Party of China, the CPC Central Committee has adhered to a people-centered development philosophy, issued the great call to build a Healthy China, and made systematic arrangements for deepening healthcare reform. In accordance with the strategic deployment for building a Healthy China outlined at the Fifth Plenary Session of the 18th CPC Central Committee, the “Outline of the ‘Healthy China 2030’ Plan” was released in 2016, establishing specific strategic objectives for the construction of a Healthy China.

The 19th National Congress of the Communist Party of China explicitly called for the comprehensive establishment of a basic medical and health system with Chinese characteristics, a medical security system, and a high-quality, efficient medical and health service delivery system. The National Health Commission has diligently implemented the decisions and deployments of the CPC Central Committee and the State Council, taking the protection of people’s health and safety as its fundamental starting point and ultimate goal. Adhering to the basic approach of coordinated design with emphasis on key priorities, and focusing on both objectives and problem-solving, the Commission has strengthened top-level design and overall planning. It has formulated and facilitated the issuance of numerous major policy documents on healthcare reform, thereby basically establishing the main framework of the basic medical and health system with Chinese characteristics. The comprehensiveness, systematicity, and synergy of healthcare reform have been significantly enhanced, leading to substantial phased achievements. Through five years of reform and development, difficulties in accessing medical care have been considerably alleviated, and the quality of medical services and public health capabilities has steadily improved.

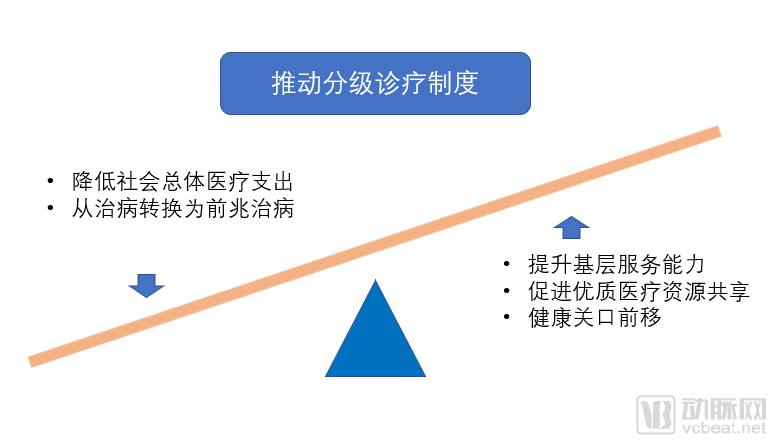

First, a tiered diagnosis and treatment system is taking shape.

Aiming to achieve the goals of “initial diagnosis at primary care facilities, two-way referrals, differentiated treatment for acute and chronic conditions, and coordinated care between upper- and lower-level institutions,” we leverage initiatives such as the development of medical consortia, telemedicine, and family doctor contract services to promote the sharing of high-quality medical resources and enhance primary care service capacity. Medical consortia serve as an institutional approach to empower primary healthcare by breaking down vertical and horizontal barriers among healthcare institutions, establishing mechanisms for the circulation of medical resources, and optimizing resource allocation. The improvement and upgrading of telemedicine technologies, coupled with the establishment of the family doctor system, shift the focus of healthcare upstream, positioning family doctors as “health gatekeepers” for residents. This facilitates a transition from treating diseases to early intervention, thereby reducing overall societal healthcare expenditures. Supporting policies are continuously refined, including increasing the reimbursement rate for outpatient services at primary care facilities under basic medical insurance, implementing cumulative deductibles for referred patients, and ensuring the implementation of long-term and extended prescriptions to strengthen the alignment of medication availability between primary care institutions and higher-level hospitals.

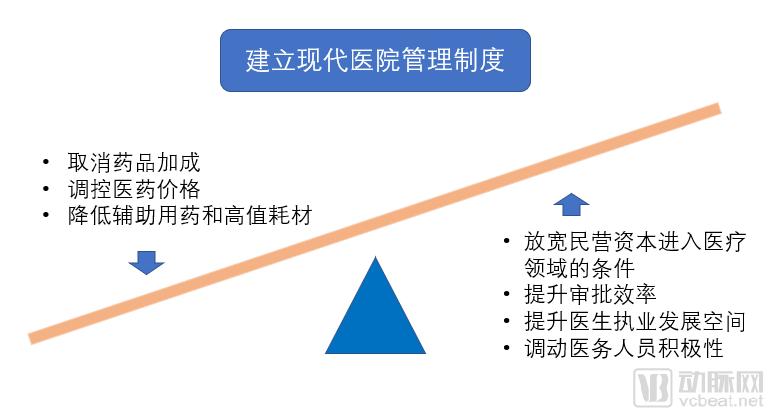

Second, the establishment of a modern hospital management system has progressed steadily.

Comprehensive reforms have been fully rolled out across all public hospitals in China, with the complete elimination of drug markups to gradually dismantle profit-driven mechanisms and uphold the public welfare nature of public hospitals. The compensation model for public hospitals has been restructured from three channels—service fees, drug markup revenue, and government subsidies—to two channels: service fees and government subsidies. Medical service practices have been standardized through the implementation of clinical pathway management, while tracking and monitoring systems have been established for adjuvant drugs, abnormally high hospital drug usage, and high-value consumables. Adhering to the "triple-medical linkage" strategy, medical resources are being rationally allocated, and pharmaceutical prices are being regulated. Initiatives have been taken to fully motivate medical personnel by improving their compensation, career development opportunities, and practice environments. Meanwhile, in the medical services sector, social capital is being encouraged to establish medical institutions; conditions for Sino-foreign joint ventures and cooperative medical practices have been relaxed; the development of private clinics has been promoted; and the efficiency of administrative approvals for privately run medical institutions has been improved.

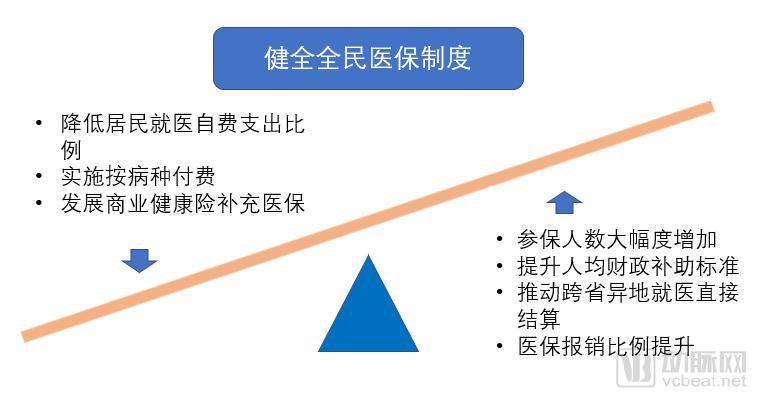

Third, the universal health insurance system has been gradually improved.

The number of participants in basic medical insurance exceeded 1.3 billion. By the end of 2017, there were 1.177 billion participants in urban resident and employee medical insurance, and 133 million participants in the New Rural Cooperative Medical Scheme (NRCMS), with the participation rate steadily maintained at over 95%. The per capita fiscal subsidy standard for basic medical insurance for urban and rural residents increased from RMB 240 in 2012 to RMB 490 in 2018. The reimbursement rates for outpatient and inpatient expenses within the policy scope remained stable at approximately 50% and 70%, respectively. The basic medical insurance systems for urban and rural residents have been largely integrated, achieving unified coverage, financing policies, benefit packages, medical insurance catalogs, designated institution management, and fund management. Direct settlement of cross-provincial medical expenses for non-local treatment has been promoted. As of the end of September 2018, the number of designated medical institutions for cross-provincial non-local treatment reached 13,995, with a cumulative total of 1.063 million direct settlements completed. The total medical expenses amounted to RMB 25.61 billion, with the fund payment ratio standing at 58.6%. Critical illness insurance has achieved full coverage. In 2017, the reimbursement rate for compliant medical expenses of critically ill patients increased by an average of 12 percentage points on top of the basic medical insurance benefits. Over the past five years, more than 17 million person-times have benefited from this program. Medical assistance for major and critical diseases and emergency disease relief have been fully established, and commercial health insurance has developed rapidly.

Reforms to healthcare insurance payment methods have been continuously advanced. Most pooled funding regions have implemented reforms such as diagnosis-related group (DRG) payments, capitation, and per-service-unit payments. In over 200 cities, the number of disease categories covered under diagnosis-based payment has exceeded 100. Pilot programs for DRG-based payment reforms have been launched, accompanied by the implementation of clinical pathway management to ensure the quality and safety of medical care. The Health Poverty Alleviation Project has been deeply implemented, carrying out the “Three Batches” action plan: centralized treatment for major diseases, contracted service management for chronic diseases, and basic security coverage for severe illnesses.

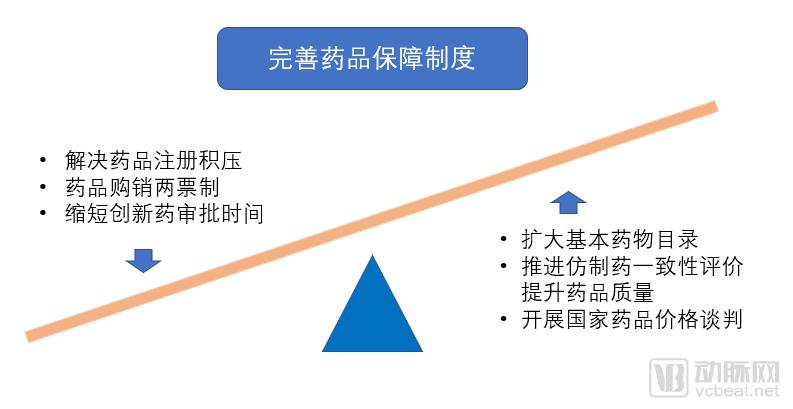

Fourth, the system for ensuring the supply of pharmaceuticals is becoming increasingly robust.

In the realm of pharmaceutical R&D, the "Guidelines for the Development Planning of the Pharmaceutical Industry" were formulated, setting forth development goals for China’s pharmaceutical industry during the 13th Five-Year Plan period across dimensions such as industry scale, technological innovation, product quality, green development, intelligent manufacturing, supply assurance, organizational structure, and internationalization. Reforms were promoted in the processes governing drug production, distribution, and usage rights to continuously enhance drug supply assurance capabilities. Multiple policies were issued to encourage the R&D of high-quality innovative drugs and medical devices, improve the quality of drug approval processes, address registration backlogs, advance the consistency evaluation of generic drug quality, accelerate the review and approval of innovative drugs, and refine technical guidelines for overseas clinical trial data of drugs.

Abolish government-set prices for the vast majority of pharmaceuticals and establish a new market-driven price formation mechanism. Implement zero tariffs on imported drugs, promote reductions in procurement prices for anticancer drugs, and conduct national drug price negotiations. The distribution channel for pharmaceuticals has become increasingly standardized; the “two-invoice system” for drug purchasing and sales has been implemented in 11 comprehensive medical reform pilot provinces and 200 pilot cities to enhance transparency in markups. The National Essential Medicines System has been further strengthened. The “Opinions on Improving the National Essential Medicines System” were reviewed and approved by the Executive Meeting of the State Council. The 2018 edition of the National Essential Medicines List has been issued, with the number of medicines increased from 520 to 685, broadly covering major clinical disease categories and better meeting basic healthcare needs. Centralized procurement of 31 drug categories in the “4+7” cities has been completed through bidding, aiming to lower drug prices, reduce transaction costs for enterprises, and guide hospitals toward standardized medication practices.

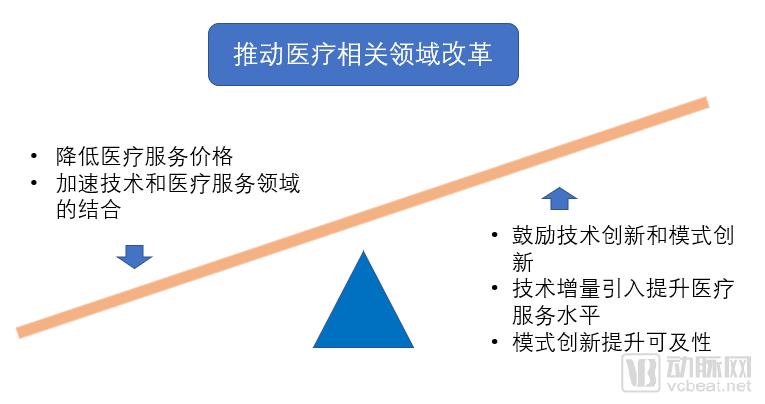

Fifth, accelerate reforms in healthcare-related fields.

Promoting the Development of “Internet + Healthcare”: Emphasizing a Policy Orientation That Encourages Innovation and Adopts an Inclusive Yet Prudent Approach, and Fostering the Integrated Development of the Internet with Services in Medical Care, Public Health, Family Doctor Contracted Services, Pharmaceutical Supply Assurance, Medical Insurance Settlement, Medical Education and Popular Science, and Artificial Intelligence Applications. Currently, “Internet + Healthcare” is demonstrating robust growth momentum. The introduction of new technological advancements has played a positive role in enhancing the quality of medical services, reducing medical service prices, and improving the accessibility of medical care.

Capital Trajectory: Significant Progress Over Five Years, 2018 Was a Challenging Year

An analysis based solely on the policy direction of the past five years reveals only the state’s support for various medical sectors and its determination to reform healthcare and pharmaceuticals. A review of national policies governing the reform of medical institutions shows that the most significant impacts have been felt in relatively traditional areas: hospitals, physicians, health insurance, medical devices, and pharmaceuticals. Although startups can seek opportunities within these transforming sectors, their actual scope for participation remains limited. With technological advancements, the scope of medical services has expanded considerably. Specialized fields such as biology, IT, chemical engineering, and finance have become integral components driving change in medical technology and the healthcare industry. Therefore, it is more essential to examine the transformations in the healthcare sector over the past five years through the lens of changes in capital, industry, and technology.

In 2018, the prevailing sentiment in the industry was the chill of the capital markets, particularly in early winter December. This easily evoked memories of the 2016 capital winter.

“It’s different; the capital markets in 2016 were vastly different from those in 2018. In 2016, startups found fundraising difficult, but in reality, investment institutions had simply become more cautious in their selection of companies compared to 2015, and many business models that had been disproven no longer attracted market attention. By 2018, however, you would find that investment institutions themselves were short of cash. Many firms that could previously close a fund round within two weeks had still not done so after three months.” This description of the industry landscape in 2018 was provided by a financial professional to VCBeat Research Institute, and it accurately reflects the real state of the financial markets in 2018.

Capital is a key driver propelling the healthcare industry forward, and the impact of global financial market fluctuations on capital, as well as the influence of capital on the development of healthcare enterprises, are intensifying. The recovery in exports was one of the primary drivers of China’s economic growth in 2017; however, as the world’s largest trading nation, China’s economy remains highly susceptible to the global environment. The Sino-U.S. trade friction accelerated the decline of China’s stock market and further impacted the venture capital/private equity (VC/PE) market and the fate of startups.

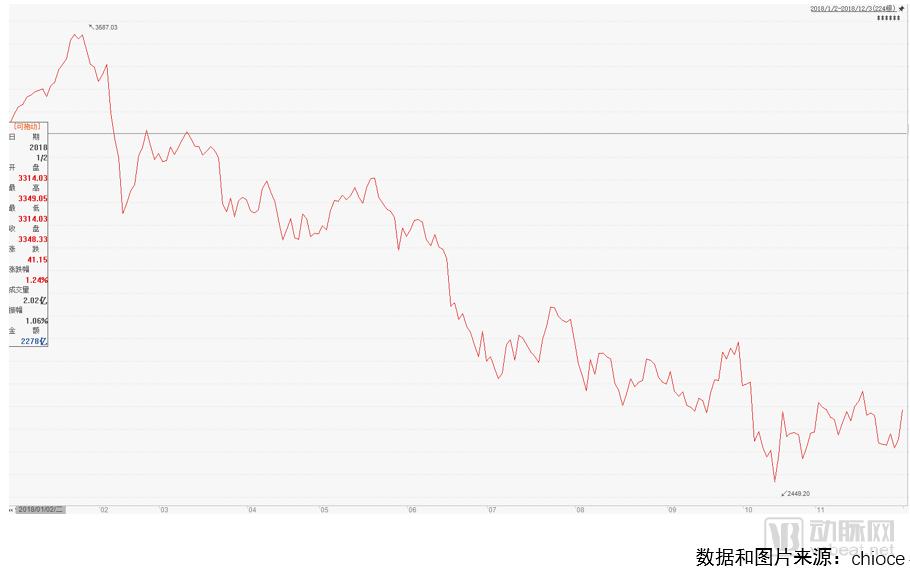

From the year’s opening level of 3,314 points, the Shanghai Stock Exchange A-share index briefly rose before embarking on a sustained decline, with a maximum drop of nearly 1,000 points to close at 2,588 points by November 30. This represents a decline of over 20%, making it one of the worst-performing stock markets globally. The poor performance of the A-share market has left many institutional investors trapped, including limited partners (LPs) of venture capital and private equity funds. As another key group of LPs, listed companies also face cash flow pressures to mitigate the risk of forced liquidation from stock pledge defaults amid continuously falling share prices, further exacerbating liquidity constraints for venture capital funds. Meanwhile, the emergence of Sino-U.S. trade friction has prompted some LPs of U.S. dollar-denominated funds to consider withdrawing their commitments. Consequently, amid these broader shifts in the financial environment, venture capital firms are tightening their purse strings and exercising greater caution in selecting investment targets.

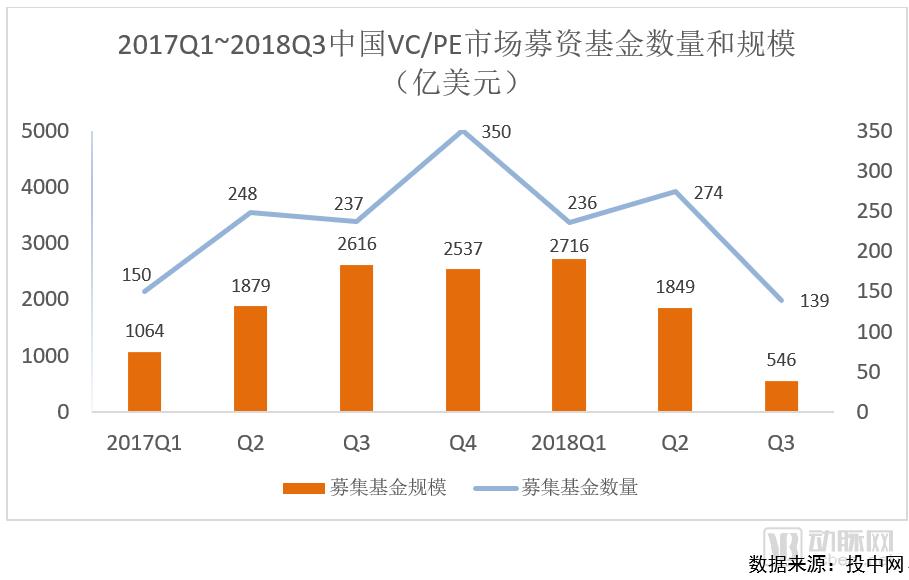

According to data from CVSource, only 139 funds entered the fundraising stage in Q3 2018, a year-on-year decline of 41.35%. The total amount raised stood at merely $54.553 billion, representing a year-on-year drop of over 70%. The VC/PE market was significantly impacted, with increased difficulty in fund raising and a substantial contraction in capital scale. Consequently, this capital winter in the second half of 2018 will continue to affect the venture capital and private equity market in 2019. As institutional investors drastically reduce their fund raising activities, they will undoubtedly exercise greater caution, allocating their limited resources to high-quality projects.

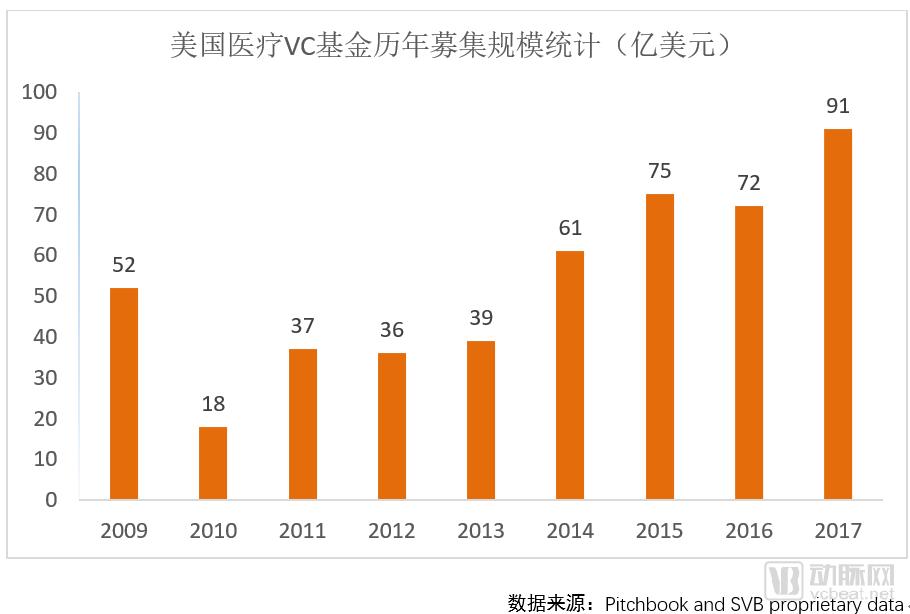

Regarding the U.S. market, a report by Silicon Valley Bank indicates that venture capital fundraising in the healthcare sector began to grow from 2014 onward. The areas attracting the most investor attention in the U.S. market are innovative biopharmaceuticals and physician diagnostic tools. Physician diagnostic tools were not the focal point in previous years; however, with the maturation of artificial intelligence technology, this trend reversed in 2017, mirroring similar shifts observed in China’s healthcare industry market.

In addition to the financial environment, the tightening of fund regulatory policies is also a significant factor contributing to the market downturn. Since 2017, regulatory bodies such as the People’s Bank of China and the three major commissions have issued the strictest regulatory policies for the financial industry, with deleveraging and risk prevention becoming the primary themes. The subsequent effects began to manifest in 2018. In the first half of 2018, the China Securities Regulatory Commission (CSRC) conducted special inspections on 453 private equity firms, including 281 managers of private equity and venture capital funds. The inspections revealed that 139 private equity firms had engaged in illegal or non-compliant activities.

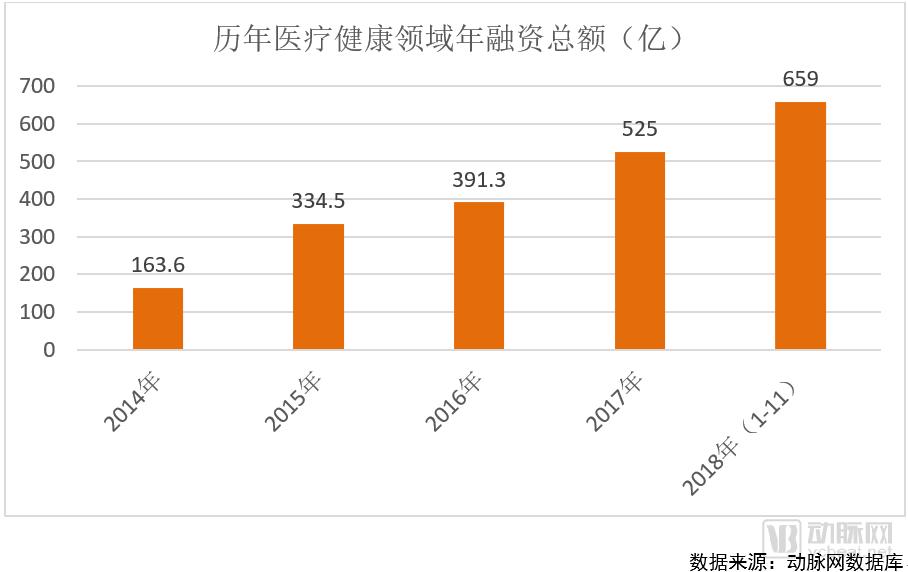

Next, VCBeat reviewed investment data from 2014 to 2018 based on VCBeat’s database. Although fundraising has become challenging for investment institutions, statistical data show that the healthcare venture capital market continued to grow against the trend in 2018. The total amount of funds raised in just 11 months already far exceeded the full-year total of 2017. As one of the most stable industries, healthcare remained a key focus area for investors in the venture capital market. However, the data indicate that VCs and PEs were more willing to invest in later-stage companies with proven revenue-generating capabilities, while opportunities for angel-round startups significantly decreased. Having suffered losses during previous hype cycles, VCs and PEs have taken lessons from cases like ofo, aiming to reduce risks while also preparing for the possibility of having no capital available for investment in 2019. Given the significant decline in fund-raising amounts in 2018, it is highly likely that the venture capital market will face even greater challenges in 2019.

According to the VCBeat database, total financing in the healthcare industry climbed steadily from 2014 to 2018 (January–November), surging significantly from RMB 16.36 billion to RMB 65.9 billion, with a compound annual growth rate (CAGR) of 41.7%, indicating very rapid growth. Even during the capital winter of 2016, the sector still recorded a 16.9% increase. Amid the capital downturn in 2018, we continued to witness substantial growth in investment amounts. As a stable sector, healthcare remains highly attractive to investors.

2014: The Emergence of Internet Healthcare and Rapid Growth in the Genomics Sector

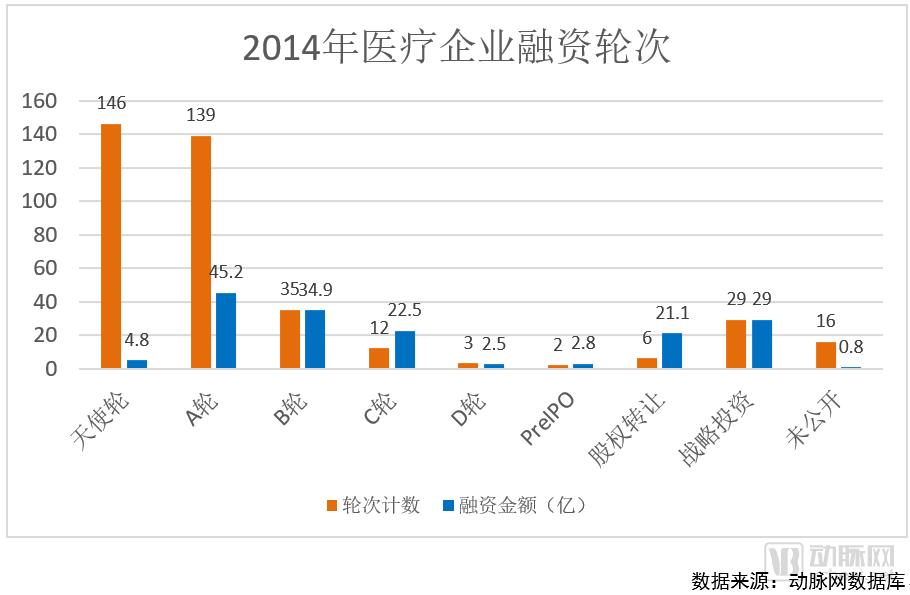

2014 marked the nascent stage of internet healthcare, witnessing the emergence of numerous startups focused on online medical consultation and diagnosis. These companies sought to transform healthcare service delivery or connect patients and providers through technological means via mobile internet. Angel-round investments peaked in 2014, reaching 146 deals, while Series A financings also hit a high of 139 transactions. Drawing on development experience from the TMT (Technology, Media, and Telecom) sector, startups identified opportunities in the healthcare industry, with venture capital firms providing substantial financial support. The subsectors attracting the largest funding volumes were predominantly those achieving breakthroughs in information technology and internet-based applications.

A surge of startups emerged in the fields of internet healthcare and e-commerce. Pharmaceutical e-commerce platforms, health informatics companies, and online medical consultation services all secured early-stage financing. Mobile internet has not only transformed people’s lives but also reshaped medical consultation processes and scenarios. Online appointment scheduling and online pharmacy services were among the internet healthcare segments that attracted significant funding in 2014, aiming to change people’s healthcare-seeking habits through digital solutions. Startups in the genetic testing sector also began to gain momentum in 2014. Notably, BGI Genomics, a unicorn company at the time, was highly sought after by investors, completing multiple rounds of financing and raising over RMB 2 billion on its own. The future prospects of genetic technology have been widely recognized by the investment community.

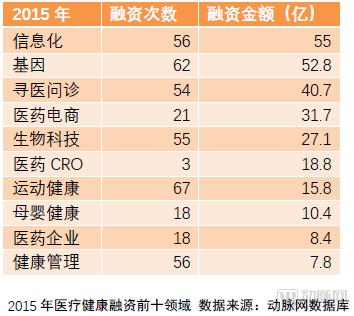

2015: A Golden Age of Innovation in Healthcare—The Prime Window for Startups

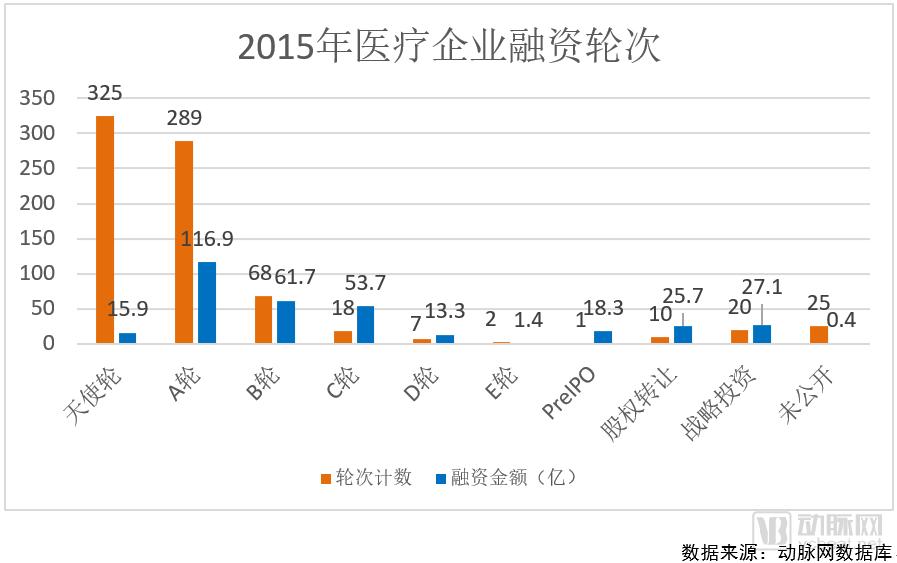

2015 was a year of significant growth for the healthcare industry, as evidenced by the number of companies receiving investment and the total amount of capital raised. There were 765 financing rounds in 2015, compared to 388 in 2014. This substantial increase in financing activity led to a corresponding surge in total funding volume. The number of angel financing rounds reached a multi-year high of 325, while Series A financings totaled 289. A large number of startups emerged, securing early-stage financial support, while business models continued to innovate.

2015 was a golden period for the development of internet healthcare, with medical informatics companies and online medical consultation platforms ranking among the top three in terms of financing amounts. Key sectors such as medical informatics, online medical consultations, pharmaceutical e-commerce, fitness and wellness, maternal and child health, and health management represent the primary scenarios where internet technology has been integrated. Startups have leveraged internet-based approaches to transform healthcare service processes and enhance the quality of medical care.

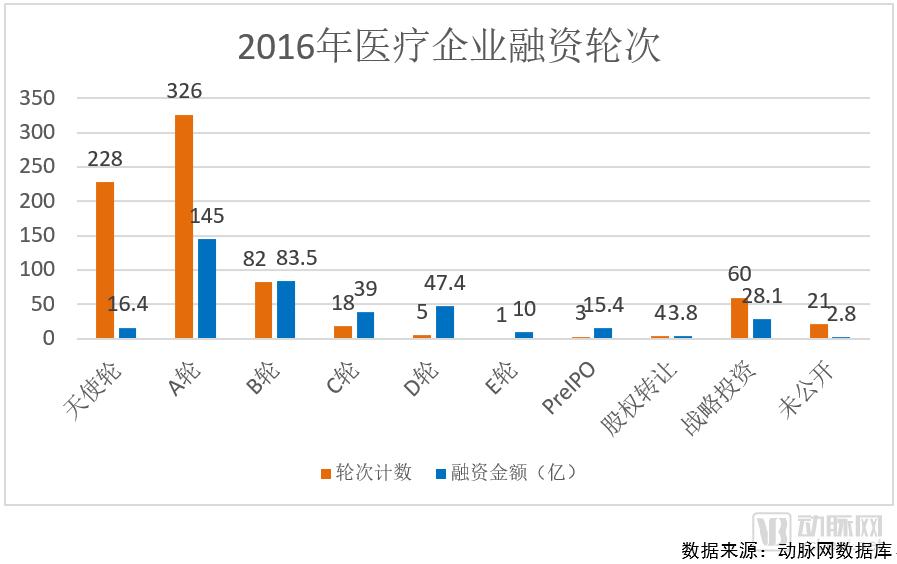

2016: Marginal Expansion, Internet Healthcare Gains Attention

After two years of development, startups gradually enter the second stage, with products becoming mature and corporate commercial value on the rise. In 2016, Series A financing became the most frequent funding round in the primary market, reaching 326 deals, with the total amount raised hitting a peak of RMB 14.5 billion. Although the number of angel funding rounds decreased to 228, startups still had opportunities to identify market gaps, and the total amount raised reached RMB 1.64 billion, the highest level for angel rounds in the past five years. In 2016, an increasing number of companies entered the growth stage; after validating their business models, they identified profitable revenue streams. As a result, the number of Series B funding rounds rose to 82, with the total amount raised increasing to RMB 8.35 billion.

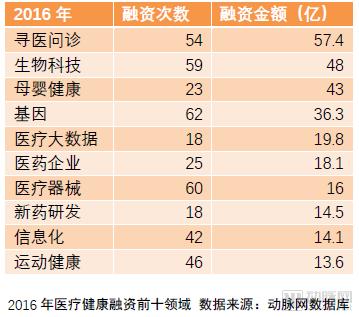

Internet healthcare companies focused on online medical consultations and appointments seized the best development opportunities in 2016, with total financing reaching RMB 5.74 billion. These enterprises have been rapidly expanding, exploring new models to transform healthcare services through mobile internet technologies across all stages of care—pre-diagnosis, during diagnosis, and post-diagnosis. Meanwhile, their disease focus has shifted from comprehensive, portal-style platforms to specialized, niche disease areas. In contrast, total financing for medical informatics and pharmaceutical e-commerce sectors has begun to decline due to earlier industry maturation or policy-related factors. Startups are identifying market gaps and intervening through innovative business models and emerging technologies, thereby expanding the boundaries of healthcare delivery.

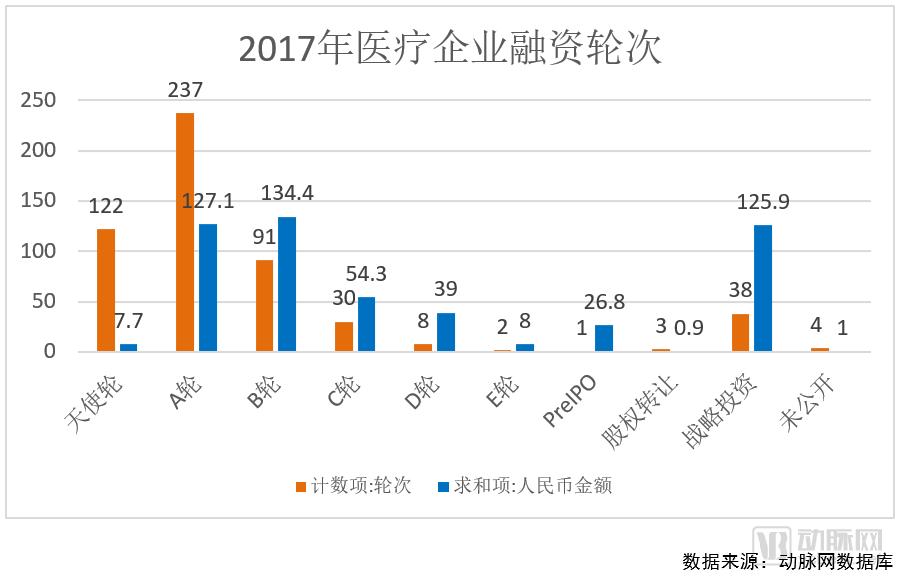

2017: Model Falsification, Biotech Companies in High Demand

The 2017 financing data clearly reflects the capital market’s preference for startups. The total amount raised in Series B rounds was the highest among all stages, reaching RMB 13.44 billion. Moreover, strategic investments typically occur in companies at the growth stage; although there were only 38 strategic investment deals, the total amount reached RMB 12.59 billion. The number and value of financings in Series C and D rounds also increased significantly. In contrast, the number of angel funding deals dropped sharply, with the total amount declining to RMB 770 million.

After many business models were proven unsustainable, capital in 2017 primarily focused on niche sectors with growth potential and validated business models. Gene technology and biotechnology rose rapidly. Although online medical consultation companies ranked third in terms of financing amount, the number of financing deals dropped significantly to just 11, as investors shifted their attention to more mature companies at Series B, C, and D stages. Both gene technology and biotechnology fall under the broader life sciences sector; together, they secured over RMB 12 billion in funding, ranking first and second respectively. The vast future growth potential of biotechnology has been clearly demonstrated by investment and financing data.

2018: Drug Development in the Spotlight as Artificial Intelligence Rises

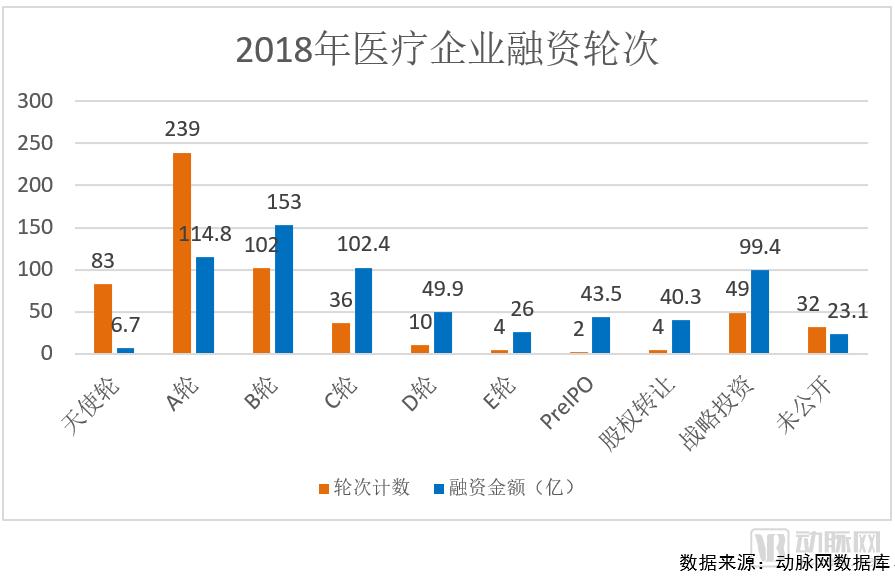

By 2018, as the capital market grew increasingly cold, opportunities for early-stage startups dwindled. The number of angel funding rounds not only fell below that of Series A rounds but was also surpassed by Series B rounds, with total angel funding further declining to RMB 670 million. Series B funding amounted to RMB 15.3 billion, the highest among all stages, while Series A and Series C funding each exceeded RMB 10 billion. In 2018, amid a challenging macroeconomic environment, investors exercised greater caution, prioritizing leading companies in mature niche sectors.

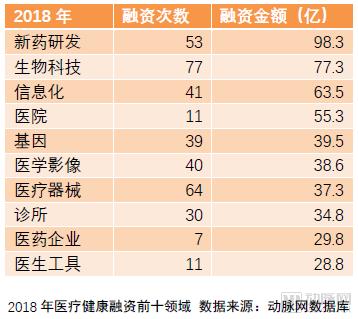

From a sector-specific perspective, biotechnology and genetics—fields closely related to biotech—have attracted particularly high attention. Moreover, a significant proportion of companies engaged in new drug development are focused on the research and development of biologics. Consequently, the top two sub-sectors by financing amount are both related to biotechnology. Among the top ten sectors, traditional healthcare areas such as hospitals, clinics, pharmaceutical companies, and medical devices are experiencing a resurgence, with healthcare entities whose profitability and business models are easily verifiable receiving greater attention. Additionally, most companies securing financing in the medical imaging field are those providing AI-based imaging decision support. After gaining momentum in 2017, this sector continued to attract substantial financing rounds in 2018.

The above is a preview of the "2018 Future Healthcare Industry Report." The full report will be released on December 19, 2018. Please scan the following mini-program code at that time to access the report.