Probevc Industry Research: China Vaccine Manufacturing Sector Report

Editor’s Note: This article is republished from Probe Capital (Probevc), authored by Huang Shan and Li Dan. VCBeat has been authorized to repost it.

Overview of the Domestic Market

China is the world’s largest vaccine producer. Due to its large population base, the annual number of vaccine batches released in China has remained between 500 million and 1 billion vials/doses since 2010.

Over 95% of the vaccines are domestically produced, with imported vaccines accounting for a relatively small share. In 2017, 39 domestic enterprises applied for lot release certification for a total of 4,237 batches, equivalent to approximately 694 million person-doses; six foreign enterprises applied for 151 batches, equivalent to approximately 18 million person-doses. A total of 50 vaccine varieties were submitted for lot release certification. State-owned enterprises are the primary suppliers of Category I vaccines, while products from private enterprises are mainly used to supply Category II vaccines.

Imported vaccines account for a very small proportion in China. In 2017, the batch release volume of imported vaccines accounted for only 2.53%, involving six companies—Merck & Co., GlaxoSmithKline, Crucell-Bernabio (Janssen), Sanofi Pasteur, Adimmune Corporation, and Pfizer Ireland—with a total of 11 product varieties. The low share of imported vaccines is primarily attributable to China’s stringent vaccine regulatory and supervision system.

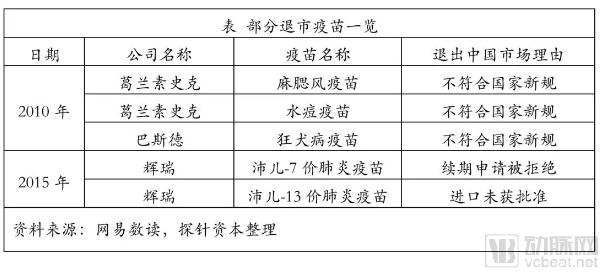

According to China’s “Measures for the Administration of Drug Registration,” imported vaccines must undergo clinical trials before they can be approved for marketing in China. Only after a review period of one to five years can an “Import Drug Registration Certificate” be obtained. The registration certificate is subject to renewal every five years; once it expires, there is a risk that the renewal will be denied. In addition to obtaining the registration certificate, importers must also comply with the requirements of the Chinese Pharmacopoeia, which is revised every five years. In October 2010, the Pharmacopoeia imposed stricter limits on antibiotic residues and Vero cell DNA residues in vaccines, significantly raising the quality threshold for market access. As a result, the share of imported vaccines in the total batch release volume dropped from approximately 10% to around 4% in 2011.

According to a report by Ren Zeping of Evergrande Research Institute, the market size of China’s vaccine industry grew from RMB 6.5 billion in 2005 to RMB 24.5 billion in 2015, representing a compound annual growth rate (CAGR) of 14%. Therefore, if this growth rate is maintained, the Chinese vaccine market is projected to reach RMB 47.2 billion by 2020.

Among these, the market for Category I vaccines is approaching saturation, with slow growth. In contrast, the Category II vaccine market still has room for expansion, driven by the recent approval and launch of novel vaccines and the upgrading of traditional vaccines into combination vaccines.

Class I Vaccine Market

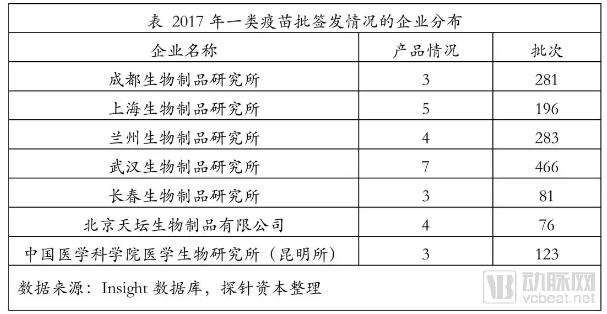

In 2017, approximately 561 million doses of Category I vaccines were approved for market release, accounting for 78.79% of all marketed vaccines. As Category I vaccines are welfare-oriented products covered by the national medical insurance and subject to mandatory vaccination, their pricing and profit margins are limited. Vaccine manufacturers in the industry are predominantly state-owned enterprises, resulting in a high degree of market concentration. The six major institutes under the China National Biotec Group (CNBG)—namely the Beijing Institute of Biological Products, Changchun Institute of Biological Products, Chengdu Institute of Biological Products, Lanzhou Institute of Biological Products, Shanghai Institute of Biological Products, and Wuhan Institute of Biological Products—along with the Kunming Institute of Medical Biology (Chinese Academy of Medical Sciences), collectively hold approximately 80% of the market share.

In 2017, the enterprise with the highest number of vaccine lot release approvals was the Wuhan Institute of Biological Products, which approved 7 varieties totaling 466 batches.

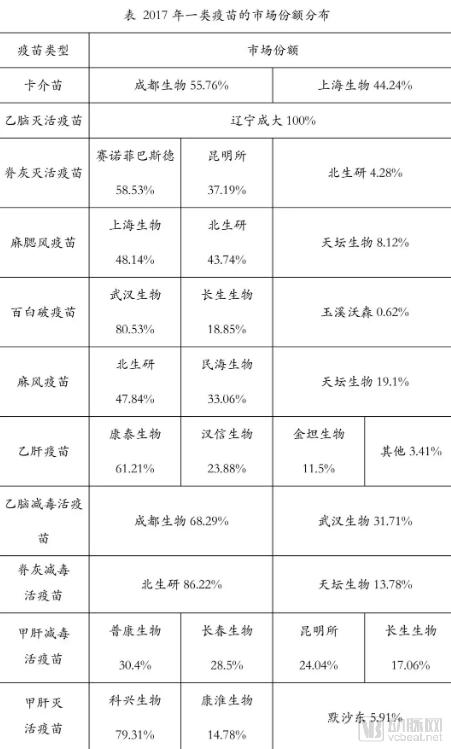

In terms of the market share of Class I vaccines in China in 2017, the DTP (diphtheria, tetanus, and pertussis) vaccine ranked first in batch release volume, with approximately 105 million doses, accounting for 17.54% of the total vaccine batch releases that year. The supply was primarily provided by Wuhan Institute of Biological Products, Changsheng Biotechnology, and Yuxi Walvax, with Wuhan Institute of Biological Products holding an 80.53% market share.

Category I vaccines have undergone three expansions in 1992, 2008, and 2016, respectively. Currently, there are 14 types included, such as the Bacille Calmette-Guérin (BCG) vaccine, diphtheria-tetanus-pertussis (DTP) vaccine, and hepatitis B vaccine, with coverage rates all exceeding 90%, and many reaching over 95%. Due to market saturation, the volume of batch releases for Category I vaccines has shown a downward trend in recent years.

In July 2018, the “Changsheng Biotechnology” incident erupted, after which its main subsidiary had its Drug Production License revoked as an administrative penalty imposed by the national drug regulatory authorities. The markets for DTP vaccine and live attenuated hepatitis A vaccine, in which Changsheng Biotechnology originally held shares of 18.85% and 17.06% respectively, would be significantly affected.

Category II Vaccine Market

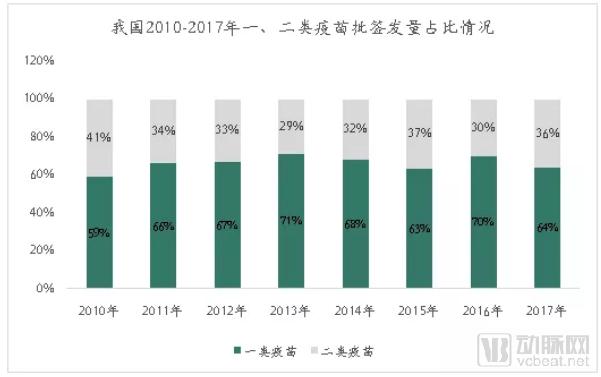

China’s vaccine market is dominated by Category I vaccines, while the market share of Category II vaccines has been relatively volatile but shows a fluctuating upward trend in the long run.

In 2015, Class II vaccines accounted for 37% of the total batch release volume. In 2016, influenced by the Shandong vaccine incident, the share of Class II vaccines in total batch releases dropped to 30%. Following the Shandong vaccine incident, the state implemented a single-invoice system for the vaccine industry to reduce intermediate distribution links. Policy reforms facilitated the gradual recovery of the Class II vaccine market, with its share of total batch releases rising to 36% in 2017.

Data source: NIFDC, compiled by Probes Capital

In China, Category II vaccines are administered on a self-pay basis and offer higher gross profit margins than Category I vaccines, with private enterprises serving as the primary market participants. In 2016, private enterprises accounted for 67.5% of the market, state-owned enterprises held only 24.4%, and foreign companies comprised the remaining 8.1%.

Data source: NIFDC, compiled by Probes Capital

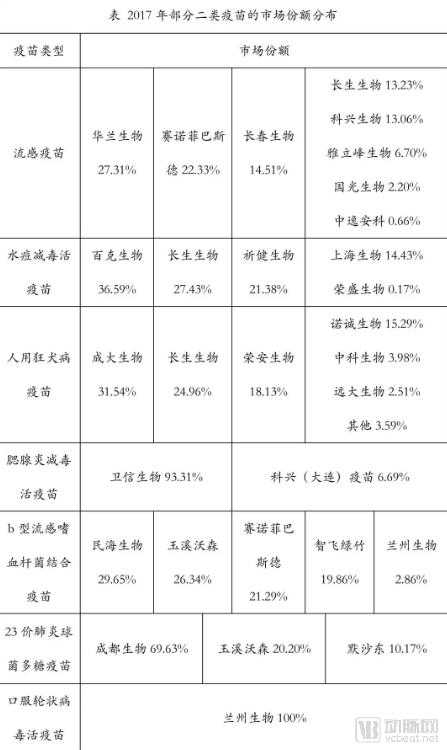

According to data from the National Institutes for Food and Drug Control (NIFDC), the Category II vaccines primarily released in 2017 included influenza vaccines, rabies vaccines, Haemophilus influenzae type b (Hib) conjugate vaccines, varicella vaccines, pneumococcal vaccines, and inactivated EV71 vaccines. Mature Category II vaccine products, such as rabies, influenza, and varicella vaccines, face intense homogenized competition. With the successive approval of novel vaccines (e.g., the 13-valent pneumococcal conjugate vaccine and HPV vaccines) and the introduction of upgraded products such as quadrivalent influenza vaccines, human diploid cell rabies vaccines, pentavalent oral rotavirus vaccines, and combination vaccines, China’s Category II vaccine market is witnessing new growth drivers.

Category II Vaccines: Rabies Vaccine Market

Rabies vaccines are a highly competitive category of Class II vaccines. Rabies is the zoonotic infectious disease with the highest number of fatalities, causing approximately 60,000 deaths globally each year. Currently, 99% of rabies cases occur in developing countries in Asia, Africa, and Latin America. India has the highest number of rabies cases worldwide, with an incidence rate of approximately 2 per 100,000 population, while China ranks second in terms of rabies incidence.

Data from the Chinese CDC’s rabies guidelines show that at the peak of the outbreak in 2007, the annual number of reported cases reached 3,300. From 2004 to 2014, rabies consistently ranked among the top three infectious diseases in China by number of deaths. Following the 2007 peak, China strengthened rabies prevention and control measures and promoted vaccination, leading to a gradual decline in incidence; by 2014, the number of cases had fallen to below 1,000.

Data source: NIFDC, compiled by Probes Capital

Currently, the main manufacturers of rabies vaccines in the market are Guangzhou Nuocheng, Liaoning Chengda, Ningbo Rongan, and Changchun Changsheng. In 2017, their total batch release volume was 53.65 million vials/doses, accounting for 91.6% of the total batch release volume of rabies vaccines.

Data Source: NIFDC, compiled by Probe Capital

Category II Vaccines: Varicella Vaccine Market

Varicella vaccine is a prophylactic vaccine primarily designed to prevent acute infectious diseases caused by primary infection with the varicella-zoster virus. Varicella is highly contagious, typically transmitted via respiratory droplets or direct contact, and predominantly affects infants, young children, and preschool-aged children, with an incidence rate exceeding 95%.

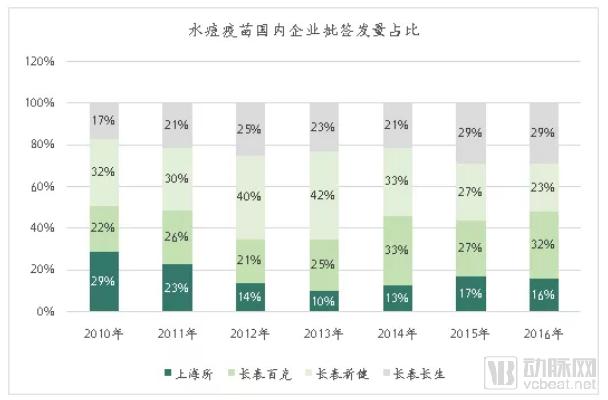

Currently, vaccination coverage in most regions of China has reached 80%–90%. The annual market growth is primarily driven by incremental demand from newborns and the widespread adoption of the two-dose regimen. According to batch release data, the varicella vaccine demonstrated robust growth from 2010 to 2015; however, in 2016, affected by the Shandong vaccine incident, the volume of batch-released vaccines dropped sharply to 13.43 million vials/doses.

Data source: NIFDC, compiled by Probe Capital

The major domestic manufacturers of varicella vaccines are the Shanghai Institute of Biological Products, Changchun Bcht, Changchun Qijian, and Changsheng Bio-technology. Among them, Changchun Bcht holds the largest market share, accounting for 32% in 2017.

Data source: NIFDC, compiled by Probes Capital

Category II Vaccines: EV71 Inactivated Vaccine Market

The inactivated EV71 vaccine is primarily used to prevent hand, foot, and mouth disease (HFMD) caused by Enterovirus 71 (EV71) infection. The incidence of this disease is highest among infants and young children under three years of age. In a small number of cases (particularly in those under three years old), the condition progresses rapidly, with complications such as meningitis, encephalitis, encephalomyelitis, pulmonary edema, and circulatory disorders emerging approximately 1–5 days after onset. A very small proportion of cases become critical and may even result in death, while survivors may suffer from sequelae.

From 2008 to 2015, China reported approximately 13.8 million cases of hand, foot, and mouth disease (HFMD), with an average annual incidence rate of 147 per 100,000 population. Approximately 130,000 severe cases were reported, resulting in more than 3,300 deaths. From January to August 2017, the number of HFMD cases reached 1.26 million.

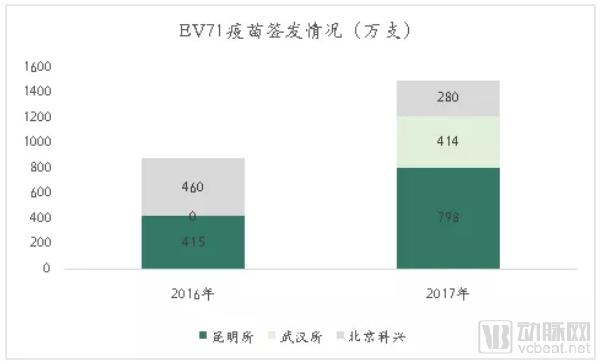

Currently, there are three enterprises in China producing EV71 vaccines. In December 2015, the products of the Kunming Institute and Beijing Sinovac were approved for market launch. The batch release of their products commenced in March and July 2016, respectively. In December 2016, the vaccine product from the Wuhan Institute was also approved for market launch, and its products began to appear in the batch release data published by the National Institutes for Food and Drug Control (NIFDC) in 2017.

Data source: NIFDC; compiled by Probes Capital

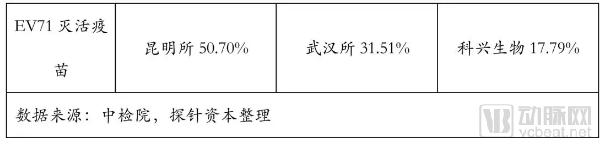

In 2016, the total batch release volume of the EV71 vaccine was 8.755 million doses, with the Kunming Institute and Sinovac releasing 4.6 million and 4.155 million doses, respectively. In 2017, the batch release volume reached 14.92 million doses, with the Kunming Institute holding the largest market share at 53.5%.

1. Zhifei Biological Products

1.1 Development History

Chongqing Zhifei Biological Products Co., Ltd. was established in 1995 and listed on the Shenzhen Stock Exchange in 2010, becoming China’s first privately owned vaccine enterprise to be listed on the ChiNext board. Its core business encompasses the research and development, manufacturing, sales, promotion, and distribution of vaccines and biological products, as well as the agency sales of imported vaccines. Currently, the company has four wholly-owned subsidiaries, including Zhifei Lvzhu and Zhifei Longcom, and one equity-participating subsidiary. Zhifei Lvzhu primarily focuses on bacterial vaccines such as those for meningitis; Zhifei Longcom specializes in tuberculosis and viral vaccines; and the equity-participating subsidiary, Ruizhi Investment (in which the Chairman holds a 90% stake), is mainly engaged in biological drugs and cell therapy.

Zhifei Biological Products started its business by distributing vaccines and adopts direct sales as its primary sales model, with the proportion of direct sales maintained at 70%-80%. Currently, the company possesses one of the most comprehensive vaccine distribution networks in China, featuring extensive coverage that reaches deep into the end-user level of the vaccine market. According to Zhifei Biological Products’ 2017 annual report, by the end of 2017, the company had 1,089 formal sales personnel. Its distribution network covered all 30 provinces, autonomous regions, and municipalities directly under the Central Government in China, including more than 300 prefecture-level cities, over 2,600 districts and counties, and more than 26,000 grassroots health service points (such as township vaccination sites and community clinics).

Data source: Zhifei Biological Products' company announcements, compiled by Probe Capital

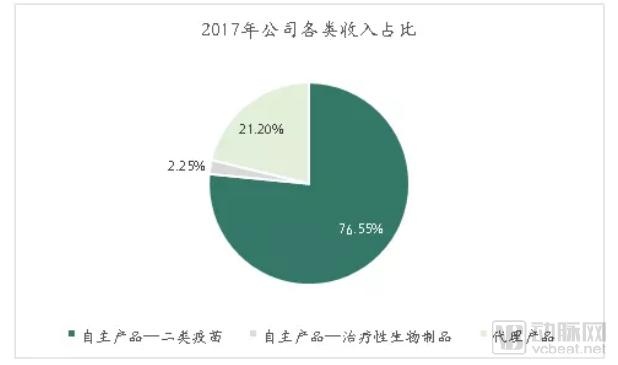

Since 2007, Zhifei Biological Products has gradually launched its independently developed products, transforming the company from a vaccine distributor into an enterprise that simultaneously advances both distribution and independent R&D. In 2017, Zhifei Biological Products reported operating revenue of RMB 1.343 billion, with revenue from its self-developed vaccine products accounting for 78.8% of the total. The distributed products were primarily those from Merck & Co. (MSD).

Data source: Zhifei Biological Products Co., Ltd. annual report; compiled by Probe Capital

1.2 Overview of Marketed Products

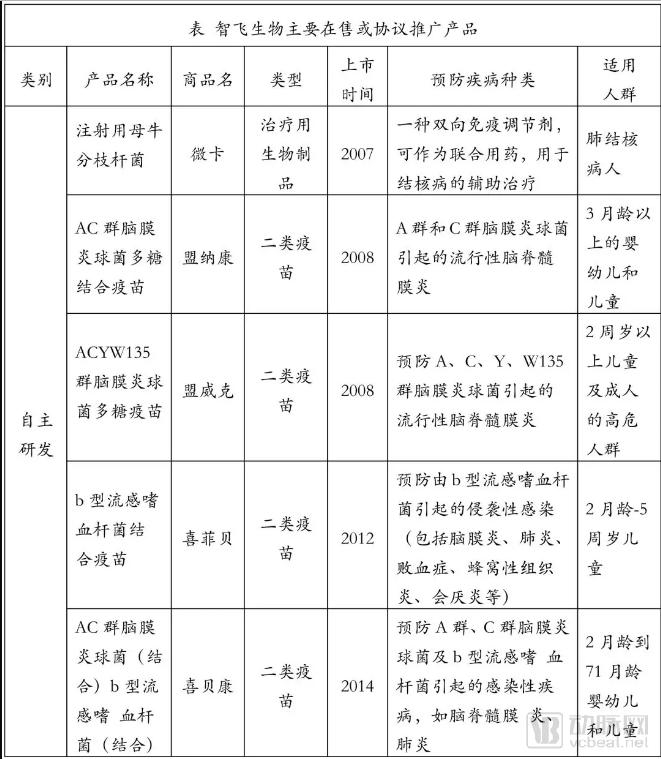

Zhifei Biologicals’ currently self-developed products mainly include five varieties: the AC-Hib combination vaccine, the ACYW135 meningococcal polysaccharide vaccine, the Hib vaccine, the AC meningococcal polysaccharide conjugate vaccine, and Microcard. Among these, the AC-Hib triple combination vaccine is a flagship product of Zhifei Biologicals, with sales volume reaching approximately 4 million doses and revenue amounting to around RMB 850 million in 2017. Meanwhile, the company is also marketing four distributed or contract-promoted products: Zhejiang Pokang’s live attenuated hepatitis A vaccine, and Merck’s 23-valent pneumococcal vaccine, inactivated hepatitis A vaccine, and quadrivalent HPV vaccine.

In addition, the company has secured distribution rights for Merck & Co.’s oral pentavalent rotavirus vaccine, with product launch expected in the third quarter of 2018. Currently, the rotavirus vaccines sold in China are still at a relatively basic level and offer limited protective efficacy; nevertheless, their annual sales reach approximately RMB 1 billion. Meanwhile, no domestically developed rotavirus vaccines have yet advanced to clinical trials for pentavalent formulations.

Source: Zhifei Biological Products’ corporate announcements and official website; compiled by Probes Capital

Data source: Zhifei Biological 2017 Annual Report, compiled by Probe Capital

1.3 Core Vaccine Products: AC-Hib Combination Vaccine

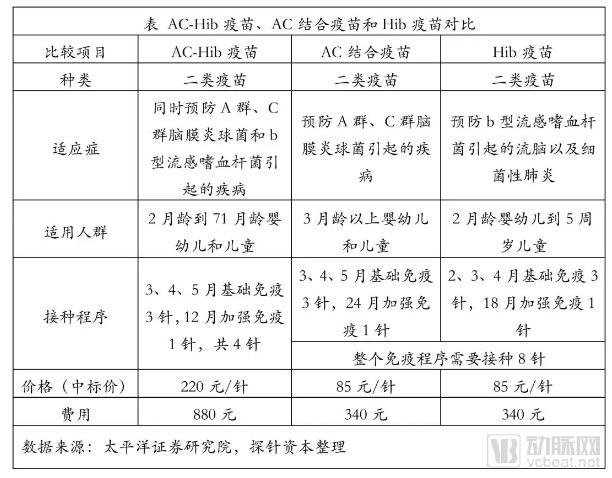

Among the products independently developed by Zhifei Biological, the AC-Hib triple vaccine is a globally exclusive blockbuster product of the company. It can simultaneously prevent meningococcal meningitis caused by Group A and Group C Neisseria meningitidis, as well as invasive infections caused by Haemophilus influenzae type b (Hib). It is an upgraded version of the existing Hib vaccines and AC group meningococcal vaccines. Zhifei Biological's AC-Hib triple vaccine was launched in 2014, officially went on sale in 2015, achieved sales of approximately 4 million doses in 2017, and generated revenue of about RMB 850 million. According to forecasts from Pacific Securities Research Institute, sales of the AC-Hib triple vaccine are expected to peak in 2022 at 10 million doses, with revenue reaching RMB 2.1 billion and contributing RMB 1 billion in net profit.

In recent years, the trend of combination vaccines replacing monovalent vaccines has been unstoppable. The trivalent AC-Hib vaccine has gradually demonstrated its substitution effect against monovalent AC conjugate vaccines and Hib vaccines. In 2017, the batch release volume of Hib vaccines was 11.45 million doses, equivalent to approximately 2.9 million person-doses, accounting for about 58% of the Hib vaccine market share. This represents a decrease of approximately 33.2% compared to the 23.6 million doses released in 2010.

Data source: Zhiyan Consulting, compiled by Probe Capital

The triple vaccine provides disease prevention efficacy equivalent to the simultaneous administration of the AC conjugate vaccine and the Hib vaccine, while significantly reducing the number of required doses: the former requires only four doses, whereas the latter requires a total of eight. Furthermore, there is minimal difference in vaccination costs between the two regimens.

Currently, other domestic companies developing triple vaccines include Luoyi Biotech, Chengdu Olin Biopharmaceuticals, and the Wuhan Institute of Biological Products. Among them, Luoyi Biotech applied for production approval as early as 2013 but remains under regulatory review; Chengdu Olin Biopharmaceuticals is in the clinical trial phase, with no publicly available updates on its research progress. It is expected that Zhifei Biological Products will monopolize the domestic triple vaccine market within the next three to five years.

1.4 Core Vaccine Products: HPV Vaccines

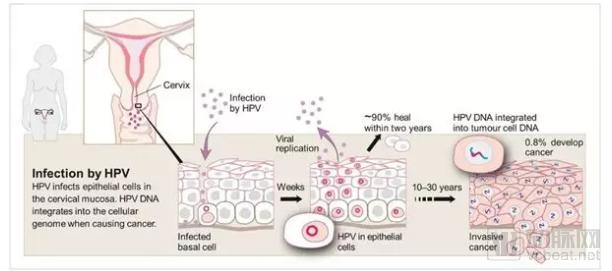

Human papillomavirus (HPV) is a virus transmitted through sexual contact and close skin-to-skin contact, capable of infecting both men and women. The prevalence of HPV infection in the general population exceeds 75%, and persistent long-term infection with high-risk HPV types is the primary cause of cervical cancer.

Schematic Diagram of Cervical Cancer Progression Following HPV Infection

Image source: The Nobel Committee for Physiology or Medicine, compiled by Probes Capital

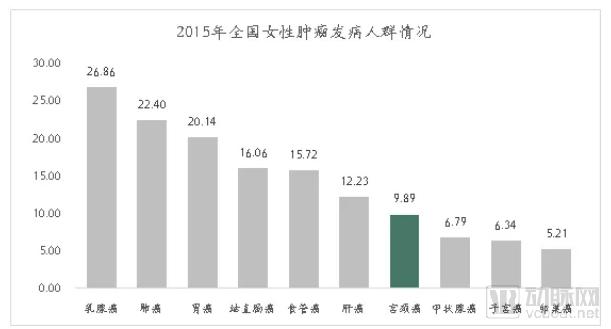

Cervical cancer is one of the most common gynecological malignancies. According to the 2015 China Cancer Statistics Report, there were approximately 98,900 new cases and about 30,500 deaths from cervical cancer in China in 2015. The incidence rate shows a trend toward affecting younger individuals, with the average age at diagnosis decreasing from 54 years two decades ago to 45 years.

Data Source: 2015 China Cancer Statistics Report, compiled by Probe Capital

Cervical cancer is currently the only cancer with a clearly identified etiology that allows for early detection and prevention. There are three types of HPV vaccines available globally: the bivalent, quadrivalent, and nonavalent vaccines. The primary manufacturers are Merck & Co. (MSD) and GSK. Merck launched its quadrivalent vaccine in 2006 and its nonavalent vaccine in 2014. Merck’s Gardasil 9 not only prevents approximately 90% of cervical cancers and 90% of genital warts, but also provides protection against 85% of vaginal cancers, 80% of cervical intraepithelial neoplasia cases, and 95% of anal cancers, making it the HPV vaccine with the broadest protective coverage to date.

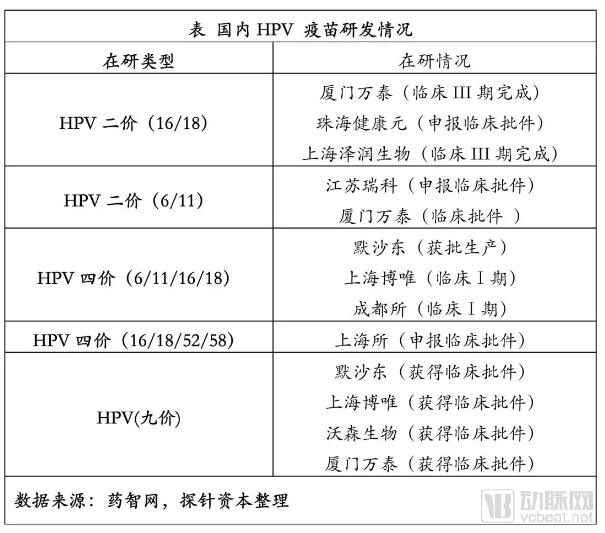

In July 2016, Cervarix received approval from the China Food and Drug Administration (CFDA) to enter the Chinese market, with sales distributed by Keyuan Xinhai, a subsidiary of Shanghai Pharmaceuticals. In May 2017, Merck’s quadrivalent Gardasil vaccine also obtained CFDA approval, with sales distributed by Zhifei Biological Products. Currently, there are no domestically produced HPV vaccines on the market; the candidates with the most advanced clinical progress are two bivalent vaccines in Phase III clinical trials, developed by Xiamen Wantai Canghai and Shanghai Zerun Biotechnology, respectively. Regarding the nine-valent vaccine, which offers the broadest protection, four companies—Merck, Shanghai Bowei, Walvax Biotechnology, and Xiamen Wantai—have obtained clinical trial approvals in China to date. In May 2018, the first doses of the nine-valent Gardasil vaccine in China were administered at the HarmonyCare International Medical Center of Hainan Boao Super Hospital. According to forecasts by Zhongtai Securities Research Institute, the market size for HPV vaccines in China reached RMB 30 billion in 2016. This market is expected to expand further with increased penetration rates and the wider adoption of the nine-valent vaccine.

In 2016, among the top ten blockbuster vaccines by global sales, Merck’s HPV vaccine generated $2.17 billion in sales, capturing over 95% of the market share and ranking second.

According to the company’s annual report, Zhifei Biological Products entered into an exclusive distribution agreement with Merck & Co. (MSD) for the quadrivalent HPV vaccine in 2012. In September 2017, the two parties signed a supplementary agreement that increased the base procurement amount. Under the procurement agreement, the company’s cumulative procurement expenditure from 2017 to the first half of 2021 amounted to RMB 6.545 billion, including approximately RMB 542 million in 2017, RMB 1.372 billion in 2018, RMB 1.784 billion in 2019, RMB 2.230 billion in 2020, and RMB 617 million in 2021. By the end of 2017, Merck’s quadrivalent HPV vaccine had won bidding in 26 provincial-level administrative regions, including Yunnan, Henan, Heilongjiang, Chongqing, Jiangxi, Guangxi, Hubei, Hunan, Sichuan, Fujian, Jiangsu, Guangdong, Shandong, Zhejiang, Jilin, Inner Mongolia, Beijing, Hebei, Tianjin, and Shanghai.

In November 2017, Zhifei Biological signed a Strategic Cooperation Agreement with Meinian Onehealth to leverage synergies by integrating with Meinian Onehealth’s health examination resources. The two parties planned to jointly establish adult vaccination clinics, work together to obtain vaccination qualifications from the National Health and Family Planning Commission, pilot vaccination services at Meinian Onehealth’s examination centers, and carry out promotion and marketing of Zhifei Biological’s products. Vaccination qualifications have currently been obtained in Taiyuan, Changsha, and Wuhan.

2. Walvax Biotechnology

2.1 Development History

Yuxi Walvax Biotechnology, established in 2001, was listed on the ChiNext board in November 2010. The company is primarily engaged in the research and development, manufacturing, and sales of biopharmaceuticals, including human vaccines and antibody drugs. It holds a leading position in niche sectors of the biopharmaceutical industry, particularly in novel vaccines.

In 2001, Walvax Biotechnology was established. In 2004, Walvax Biotechnology received RMB 10 million in venture capital (VC) investment and concurrently planned and implemented its industrialization strategy, commencing the construction of the “Yuxi Vaccine Production Base.” In 2007, Walvax Biotechnology completed its first Good Manufacturing Practice (GMP) workshop for vaccines. Its “Haemophilus influenzae type b (Hib) conjugate vaccine” was launched and achieved profitability, contributing over RMB 30 million in net profit during its first fiscal year of sales. In 2008, Walvax Biotechnology secured angel-round investment from Chang’an Private Capital and initiated its initial public offering (IPO) process. From 2009 to 2012, the successive market launches of products such as the freeze-dried Group A and C meningococcal polysaccharide conjugate vaccine, the Group A and C meningococcal polysaccharide vaccine, and the ACYW135 group meningococcal polysaccharide vaccine enabled Walvax Biotechnology to successfully enter China’s Category I vaccine market. In November 2010, Walvax Biotechnology went public on the ChiNext board, raising RMB 238 million.

Since 2012, Walvax Biotechnology has expanded into the fields of novel vaccines, monoclonal antibodies, blood products, and pharmaceutical distribution through external mergers and acquisitions. In 2012, Walvax Biotechnology entered the novel vaccine sector by acquiring Shanghai Zerun Biotechnology to strengthen its capabilities in novel (recombinant) vaccines. From 2013 to 2014, the company entered the vaccine and pharmaceutical distribution sectors by acquiring equity stakes in Ningbo Punuo, Shandong Shijie, Putian Shengtai, Beijing Ruiermeng, and Chongqing Beining; entered the monoclonal antibody sector by acquiring Jiabao Biotherapeutics; and entered the blood products sector by acquiring Hebei Da’an. In 2015, its subsidiaries, Shanghai Zerun and Shanghai Jiabao, received RMB 1.4 billion in investment from institutions including Sunshine Insurance Group and ChinaVest.

In 2016, Shandong Shijie was implicated in the “illegal vaccine trading case,” resulting in the revocation of its Drug Operation Permit and the termination of its listing on the National Equities Exchange and Quotations (NEEQ). Watson Biopharma transferred its equity stake in the company, which significantly impacted its operating revenue. In September 2016, Watson Biopharma strategically introduced Yunnan Provincial Industrial Investment Holding Co., Ltd. as a strategic investor. During the same period, the clinical trial application for the 9-valent HPV vaccine developed by its subsidiary, Shanghai Zerun, was accepted. In April 2017, the 23-valent pneumococcal polysaccharide vaccine received production approval, and sales commenced in August. In January 2018, the 9-valent HPV vaccine obtained approval for clinical trials. In April 2018, the 13-valent pneumococcal conjugate vaccine was officially included in the priority review list, while the bivalent HPV vaccine from subsidiary Shanghai Zerun entered a critical phase of Phase III clinical studies.

2.2 Overview of Marketed Products

Walvax Biotechnology’s main marketed products include: Haemophilus influenzae type b (Hib) conjugate vaccine (in vial and pre-filled syringe formulations), 23-valent pneumococcal polysaccharide vaccine, Group A and Group C meningococcal polysaccharide conjugate vaccine, ACYW135 group meningococcal polysaccharide vaccine, Group A and Group C meningococcal polysaccharide vaccine, and adsorbed diphtheria-tetanus-acellular pertussis combination vaccine, totaling six products across seven specifications. In 2017, sales revenue from these products accounted for approximately 77% of total operating revenue, amounting to RMB 515 million, with a gross profit margin of 80.77%. Among them, the Hib vaccine contributed the largest share of sales revenue, accounting for 37.34% of total sales revenue, with a gross profit margin of approximately 89%.

2.3 Core Vaccine Products: 23-Valent Pneumococcal Vaccine

Streptococcus pneumoniae is the most common cause of pneumonia, bacteremia, sinusitis, and acute otitis media, with young children and the elderly being the populations most commonly affected. According to WHO data, more than 1.2 million children worldwide die from pneumonia each year, with 90% of these deaths occurring in developing countries.

23-Valent Pneumococcal Polysaccharide Vaccine (PPV23) is primarily used for the prevention of pneumococcal disease in adults. The vaccine is licensed for use in adults with underlying medical conditions (particularly those aged ≥65 years) and children aged ≥2 years, targeting 23 serotypes (1, 2, 3, 4, 5, 6B, 7F, 8, 9N, 9V, 10A, 11A, 14, 15B, 17F, 18C, 19A, 19F, 20, 22F, 23F, and 33F).

Currently, three companies are marketing the 23-valent pneumococcal vaccine in China: Chengdu Institute of Biological Products (72% market share), Merck & Co. (16%), and Walvax Biotechnology (12%). Walvax’s 23-valent vaccine was launched in August 2017. Its quality standards exceed those of the European Pharmacopoeia, and its winning bid price is higher than that of typical domestic manufacturers. It is currently the only fully pre-filled syringe-packaged 23-valent pneumococcal polysaccharide vaccine in China, offering convenience during administration. Additionally, it is the world’s first preservative-free 23-valent pneumococcal polysaccharide vaccine.

In recent years, with rising public awareness of vaccination and a slight increase in newborns driven by the two-child policy, the market size for this product is expected to gradually expand in the coming years. According to forecasts from Dongxing Securities Research Institute, the total terminal sales volume of Walvax Biotechnology’s 23-valent pneumococcal vaccine is projected to exceed RMB 2 billion.

2.4 Core Vaccine Product: 13-Valent Pneumococcal Polysaccharide Conjugate Vaccine

The 13-valent pneumococcal polysaccharide conjugate vaccine is known as the global “king of vaccine sales” and is currently produced exclusively by Pfizer. In 2016, Pfizer’s 13-valent pneumococcal vaccine (brand name: Prevnar 13™) topped the list of the world’s ten best-selling vaccines, with sales revenue of approximately USD 5.72 billion. This vaccine has been included in the national immunization programs of more than 100 countries worldwide. Currently, there are three types of pneumococcal conjugate vaccines globally: the 7-valent, 10-valent, and 13-valent vaccines. European and American countries have largely completed the replacement of the 7-valent vaccine with the 13-valent vaccine, while the 10-valent vaccine is primarily marketed in continental Europe.

Source: Pfizer Annual Report; compiled by Probe Capital

Pfizer received approval from the China Food and Drug Administration (CFDA) in November 2016 to market the vaccine in China for children aged 6 weeks to 15 months. Batch release data has been available since March 2017.

The main companies in China developing 13-valent pneumococcal vaccines include Walvax Biotechnology, Minhai Biotechnology, Beijing Sinovac, Lanzhou Institute of Biological Products, and Chengdu Antaijin. In April 2018, Walvax Biotechnology’s 13-valent pneumococcal conjugate vaccine was officially included in the priority review list, making it the company with the most advanced progress in China. It was expected to be launched for sales in early 2019. Minhai Biotechnology was in Phase III clinical trials, while Lanzhou Institute, Beijing Sinovac, and Chengdu Antaijin were in the early stages of clinical development. Walvax Biotechnology was projected to become the second company globally to market this blockbuster vaccine. According to forecasts by Dongxing Securities Research Institute, assuming a unit price of RMB 650 and a net profit margin of 50%, sales of the 13-valent pneumococcal vaccine from 2019 to 2021 could reach RMB 2.2 billion in 2019, generating approximately RMB 1.1 billion in net profit.

3. Kangtai Biological

3.1 Development History

Shenzhen Kangtai Biological Products Co., Ltd. was established in 1992 and listed on the ChiNext Board of the Shenzhen Stock Exchange in 2017. Du Weimin, the Chairman and General Manager, holds a direct stake of 54.46%, making him the actual controller of the company. Its core business involves the research and development, production, and sales of human vaccines. It is the largest manufacturer of hepatitis B vaccines in China and the sole domestic producer of the quadruple combination vaccine. In its early years, Kangtai Biological primarily relied on hepatitis B vaccines and Haemophilus influenzae type b (Hib) vaccines to achieve steady revenue growth. With the launch of the quadruple combination vaccine in 2013, the company entered a phase of rapid expansion. In 2017, it reported operating revenue of RMB 1.164 billion, a year-on-year increase of 110.95%, and net profit of RMB 218 million, a year-on-year increase of 152.32%.

Source: Kangtai Biological 2017 Annual Report, compiled by Probe Capital

Kangtai Biological currently has three wholly-owned subsidiaries: Minhai Biological, Xintaikang, and Kangtai Technology. Among them, Minhai Biological serves as the core of the company’s vaccine business; Xintaikang is primarily engaged in the research, development, and application of pharmaceutical technologies; and Kangtai Technology mainly focuses on the development, production, operation, and import-export business of hepatitis B vaccines and other medical biological products.

3.2 Overview of Marketed Products

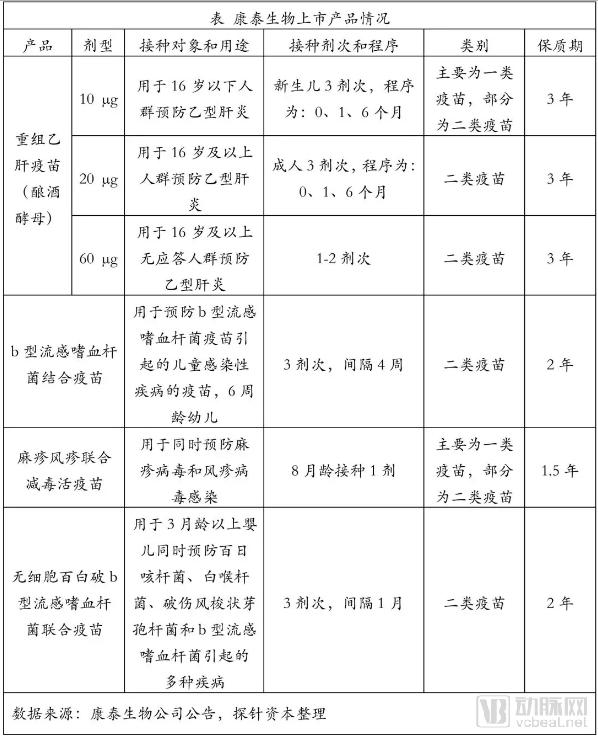

Currently, the products marketed by Kangtai Biological include four varieties with six specifications: hepatitis B vaccine, DTP-Hib quadrivalent vaccine, Hib vaccine, and measles-rubella bivalent vaccine.

Among these, the DTP-Hib quadrivalent vaccine and the 60 μg hepatitis B vaccine are exclusive products of Kangtai Biologicals, which holds the largest market share in China for both hepatitis B vaccines and Hib vaccines.

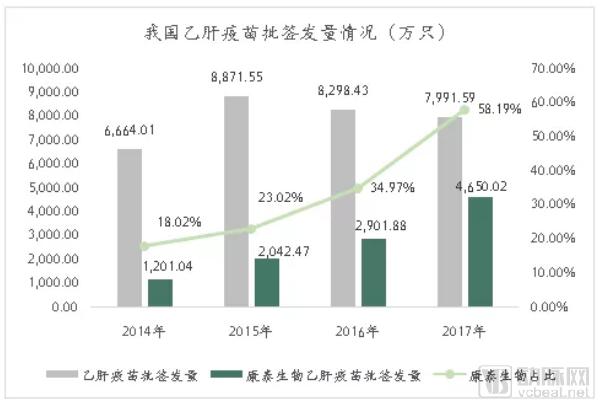

In recent years, the proportion of batch release volumes for hepatitis B vaccines produced by Kangtai Biological Products has gradually increased. By 2017, its batch release volume reached 46.5002 million doses, accounting for 58.19% of the total national batch release volume, ranking first in market share and far exceeding the 25% market share of Dalian Hissen, which held the second position. Notably, the 60 μg dosage form is an exclusive product of the company, with a batch release volume of 630,200 doses in 2017.

Data source: NIFDC, compiled by Probes Capital

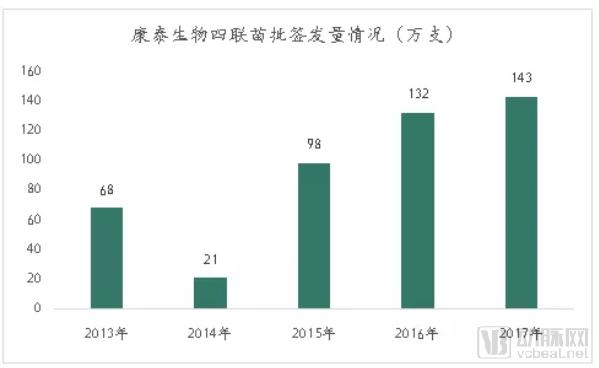

3.3 Core Vaccine Products: DTaP-Hib Quadrivalent Vaccine

The DTaP-Hib quadrivalent vaccine can simultaneously prevent pertussis, diphtheria, tetanus, and diseases caused by Haemophilus influenzae type b (Hib), such as meningitis, pneumonia, pericarditis, bacteremia, and epiglottitis. It is formulated by integrating the Hib vaccine with an acellular diphtheria-tetanus-pertussis combined vaccine (DTaP), which is produced from processed Bordetella pertussis, Corynebacterium diphtheriae, and Clostridium tetani.

In 2013, Kantaibio’s quadrivalent vaccine was officially launched in the market. From 2013 to 2015, Kantaibio experienced continuous volume growth and rapid performance expansion. In 2016, affected by the Shandong vaccine incident, the growth rate of Kantaibio’s batch release volume slowed down. In 2017, following industry rectification, sales of the quadrivalent vaccine surged, with sales revenue exceeding RMB 400 million.

Data source: NIFDC, compiled by Probes Capital

1. CanSino

Tianjin CanSino, established in 2009, is a leading high-tech biopharmaceutical enterprise in China dedicated to the research and development, production, and commercialization of high-quality human vaccines for the prevention of infectious and communicable diseases. The company primarily manufactures ten advanced vaccine products with independent intellectual property rights, including recombinant Ebola vaccine, recombinant broad-spectrum pneumococcal protein vaccine, multivalent meningococcal conjugate vaccine, component-based diphtheria-tetanus-pertussis combination vaccine, and novel tuberculosis vaccine, with planned production commencement in 2019.

Source: CanSino Biologics Official Website

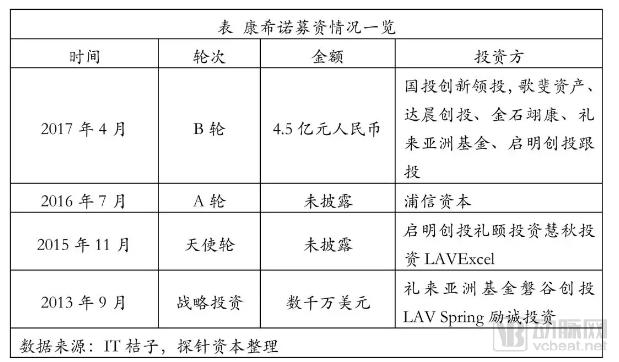

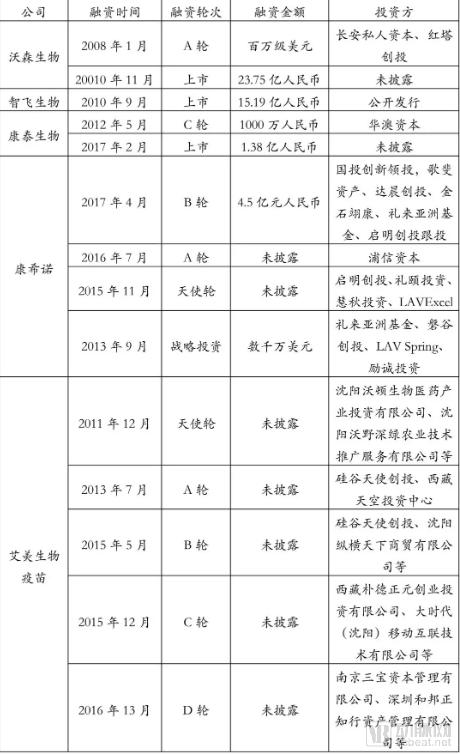

The company has secured successive rounds of financing from numerous well-known domestic and international venture capital firms, including Lilly Asia Ventures, SDIC Innovation, Qiming Venture Partners, and Fortune Capital, with total funds raised exceeding RMB 750 million. On July 10, 2018, CanSino Biologics updated its prospectus, proposing to raise between USD 343 million and USD 457 million. The public offering was scheduled for July 20–25, with listing on August 1, positioning it to become Hong Kong’s first unprofitable biotechnology stock.

2. Oxford Lycopodium Bio

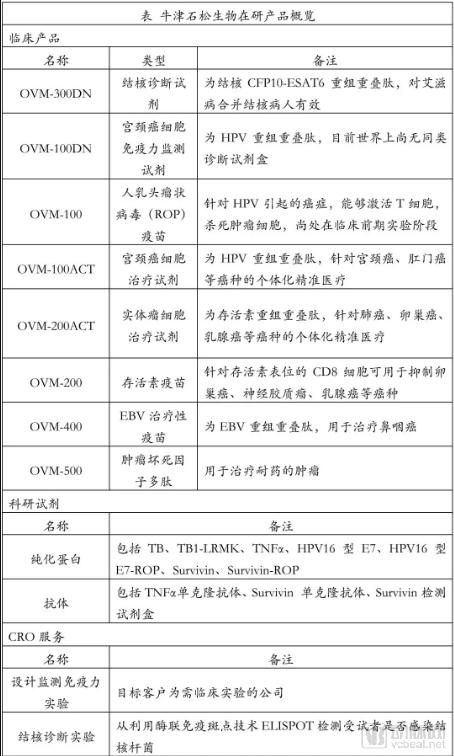

Changzhou Oxford Lycopodium Biotechnology Co., Ltd. was established in 2012. Its main products under development are therapeutic vaccines for cervical cancer and advanced-stage tumors, as well as diagnostic kits for tuberculosis. Leveraging recombinant overlapping peptide technology, the company operates five major platforms: therapeutic vaccines, veterinary vaccines, research reagents, active pharmaceutical ingredients (APIs) for targeted cell therapy, and immune diagnostics.

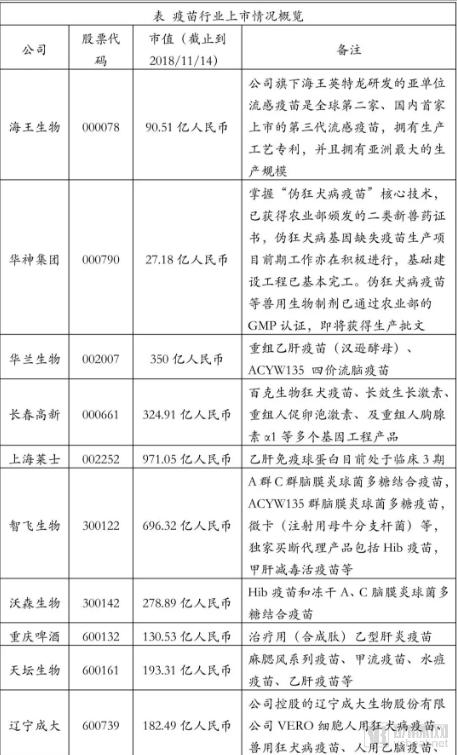

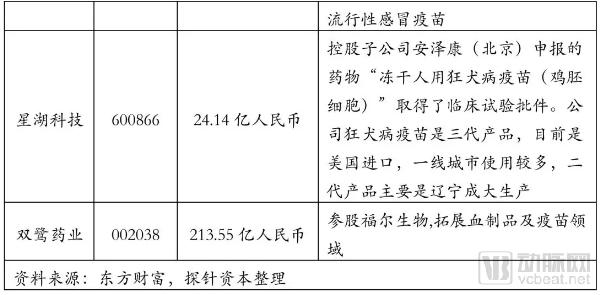

1. Overview of Listing Status

2. Overview of Mergers and Acquisitions

1. Investment Distribution

2. Investment Risks

• Vaccine products boast exceptionally high gross profit margins. It is reported that in the first quarter of 2018, Changsheng Biotechnology’s core business achieved a gross profit margin of 91.59%. The high profitability prevalent in the existing market has maintained a relatively stable industry landscape, thereby limiting growth opportunities for emerging vaccine manufacturers.

• The clinical development of new vaccine products requires substantial investment, faces high technical barriers, and is associated with significant uncertainty in research outcomes. It is reported that South China Vaccine’s operating revenue in 2017 was RMB 3.4184 million, while its R&D expenses reached RMB 11.4462 million, resulting in a net loss. In contrast to the high gross margins characteristic of the existing vaccine industry, the high investment coupled with low returns in vaccine R&D has, to some extent, hindered the development of novel vaccines.

• Affected by malignant vaccine incidents such as the Changchun Changsheng Bio-technology case, the vaccine industry is likely to enter a policy “frost period.” According to the Regulations on the Administration of Vaccine Circulation and Preventive Vaccination, a single-invoice system is implemented for vaccine distribution; wholesalers of Category II vaccines are no longer permitted to engage in vaccine operations. Vaccination units are required to ensure consistency among invoices, accounts, goods, and payments, achieve full-process traceability throughout the distribution chain, and face stricter penalties and accountability measures for violations.

• Trust crisis hampers the development of China’s domestic vaccine industry. According to the “Analysis Report on Parents’ Vaccination Attitudes and Behaviors Before and After the Vaccine Incident,” published by Xiao Dou Miao, 64.16% of parents indicated they would prefer imported vaccines for their children in the future. How domestic vaccine manufacturers can rebuild market confidence is currently the greatest challenge facing the industry.