From 'Functionality' to 'Intelligence': Transformation and Investment Opportunities in the Medical Informatics Industry Led by Electronic Medical Records

Recently, the 2018 Future Healthcare Top 100 Forum, hosted by VCBeat, Eggshell Research Institute, and Future Healthcare Academy, and co-hosted by Legend Capital, BV Baidu Ventures, KPMG China, Health Intelligence Valley, and Zero2IPO Healthcare, was held at the Renaissance Beijing Capital Hotel. Yu Jurong, Partner at Zero2IPO Healthcare, was invited by VCBeat to deliver a keynote speech titled “From ‘Functionality’ to ‘Intelligence’: Transformation and Investment Opportunities in the Medical Informatics Industry, Exemplified by Electronic Medical Records.”

This article is adapted from the keynote speech by Yu Jurong, Partner at Qingke Medical, with some text abridged.

Yu Jurong: Hello, everyone. Last year, at the invitation of VCBeat, I shared insights on the evolution of hospital innovation from the perspective of ten years of healthcare investment data. It became evident that changes in hospital innovation are inextricably linked to the development of healthcare informatization. This year, we continue along this thread by focusing on electronic medical records (EMR), a typical representative of healthcare informatization, to examine the development trends in the transformation of healthcare IT and to identify potential investment opportunities. Due to the somewhat rushed preparation time, there may be imperfections in the materials presented; your feedback and corrections are greatly appreciated.

Today, we will focus on answering three core questions:

First, what is the standing of electronic medical records (EMR) within the healthcare informatization industry?

Second, we need to examine the developmental evolution of electronic medical records (EMRs) from basic functionality to intelligent systems, analyze the differences between domestic and international practices, and assess whether China has the potential to achieve leapfrog development.

Third, which enterprises are participating in the broad electronic medical record (EMR) sector, and what investment opportunities and potential exist for institutional investors?

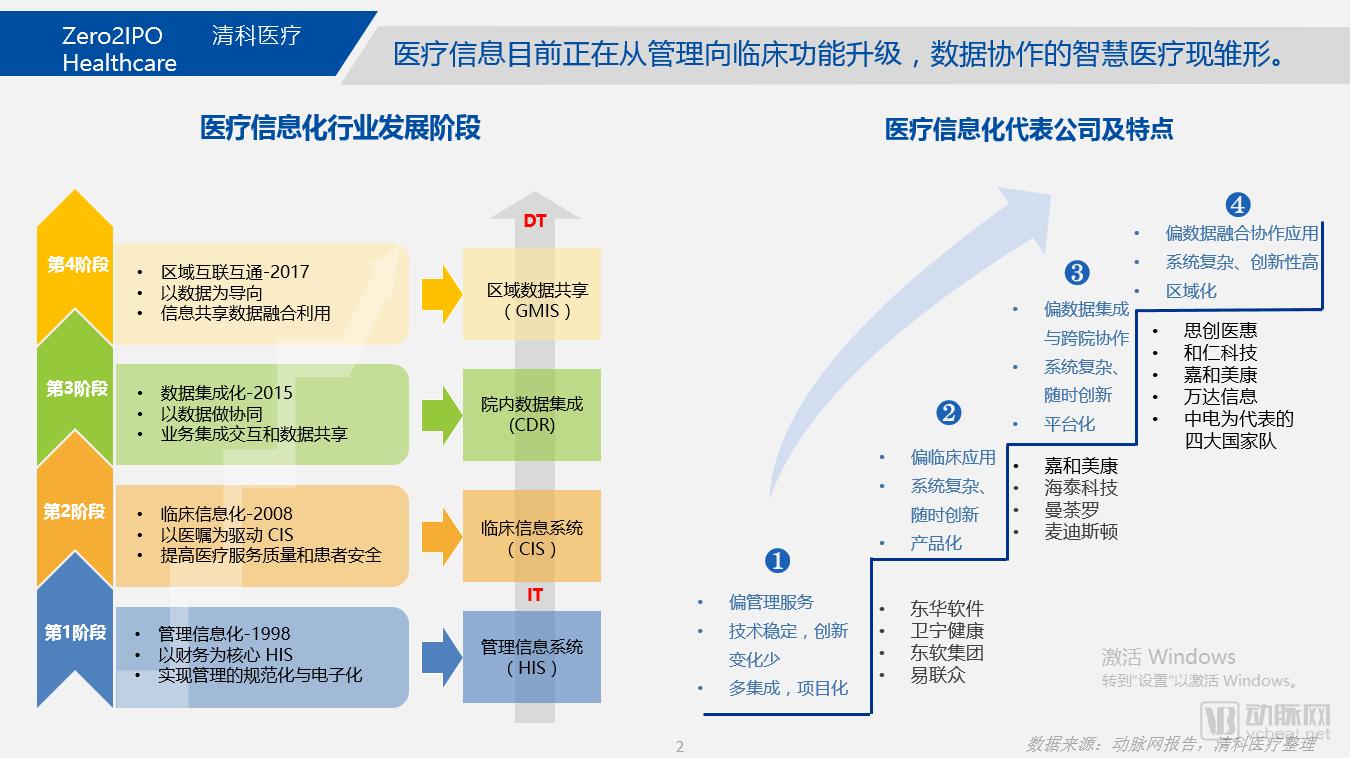

Let us now turn to the main topic. First, let us examine the overall trends in the development of healthcare informatization. In China, explorations into healthcare informatization began in the 1980s and have undergone four stages of development:

The first phase is the HIS-driven management informatization stage, which primarily focuses on the management of human resources, finances, and materials within hospitals, aiming to enhance hospital management efficiency. Representative companies include four listed enterprises: Donghua Software, Winning Health, Neusoft Corporation, and Yilianzhong.

The second stage is the development phase of Clinical Information Systems (CIS), with electronic medical records (EMR) serving as a typical representative. This stage primarily focuses on clinical medical applications as the key evaluation metric, utilizing information technology to present the entire diagnosis and treatment process. Representative companies in this phase include Jiahe Meikang, Haitai Technology, and Mandala, as well as Mediston, which specializes in specialty-specific EMRs. It is worth noting that there were relatively few publicly listed companies during this stage; currently, Mediston stands as the sole representative among listed enterprises.

The third phase is based on the Hospital Clinical Data Repository (CDR), which centralizes and integrates clinical data from various departments, enabling data interoperability within the hospital and making joint consultations possible.

The fourth stage breaks down the boundaries of hospitals, with the integration of data between hospitals as the core consideration.

The third and fourth stages are both fundamentally data-driven. We can observe that these stages involve collaborative efforts by numerous enterprises. The range of representative companies in this phase is relatively broader; in addition to the aforementioned firms, it includes Yichuang Huiyi, Heren Technology, Jiahe Meikang, Wanda Information, and China Electronics Corporation (CEC), which represents the “national team.”

Currently, most hospitals in China are transitioning from the management information stage to the clinical information stage, with smart healthcare initiatives at leading tertiary Grade A hospitals beginning to take shape.

Let us now examine the competitive landscape of electronic medical records (EMR). We can see that after more than 20 years of development, hospital management information systems have achieved a coverage rate exceeding 70%. However, the penetration of clinical information systems remains significantly inadequate. Even among tertiary hospitals, the coverage rate is only 50%, while it is extremely low in hospitals below the Grade A tertiary level. Meanwhile, there is substantial demand for upgrades in clinical informatics. There remains considerable room for enhancement, particularly in evolving from comprehensive EMRs to specialty-specific EMRs, as well as upgrading specialized software functionalities such as intelligent clinical decision support.

Electronic medical records (EMRs) serve as a pivotal link in the overall clinical informatization landscape and form the foundation of smart healthcare. For government agencies and healthcare professionals, EMRs are an invaluable tool for governmental oversight and hospital evaluation, health insurance cost containment, implementation of tiered diagnosis and treatment, and the development of primary care-based medical consortia.

For healthcare professionals, as Mr. Lu from Zechuang Tiancheng just mentioned, the electronic medical record (EMR) system is also an excellent tool for physicians to conduct scientific research.

It also serves as a strong link between the supply and demand sides of healthcare, namely hospitals and patients. Regarding pharmaceutical companies, Mr. Zhao from Taimei Medical Technology noted that integrating electronic medical records with new drug R&D data systems is indeed a promising direction for development.

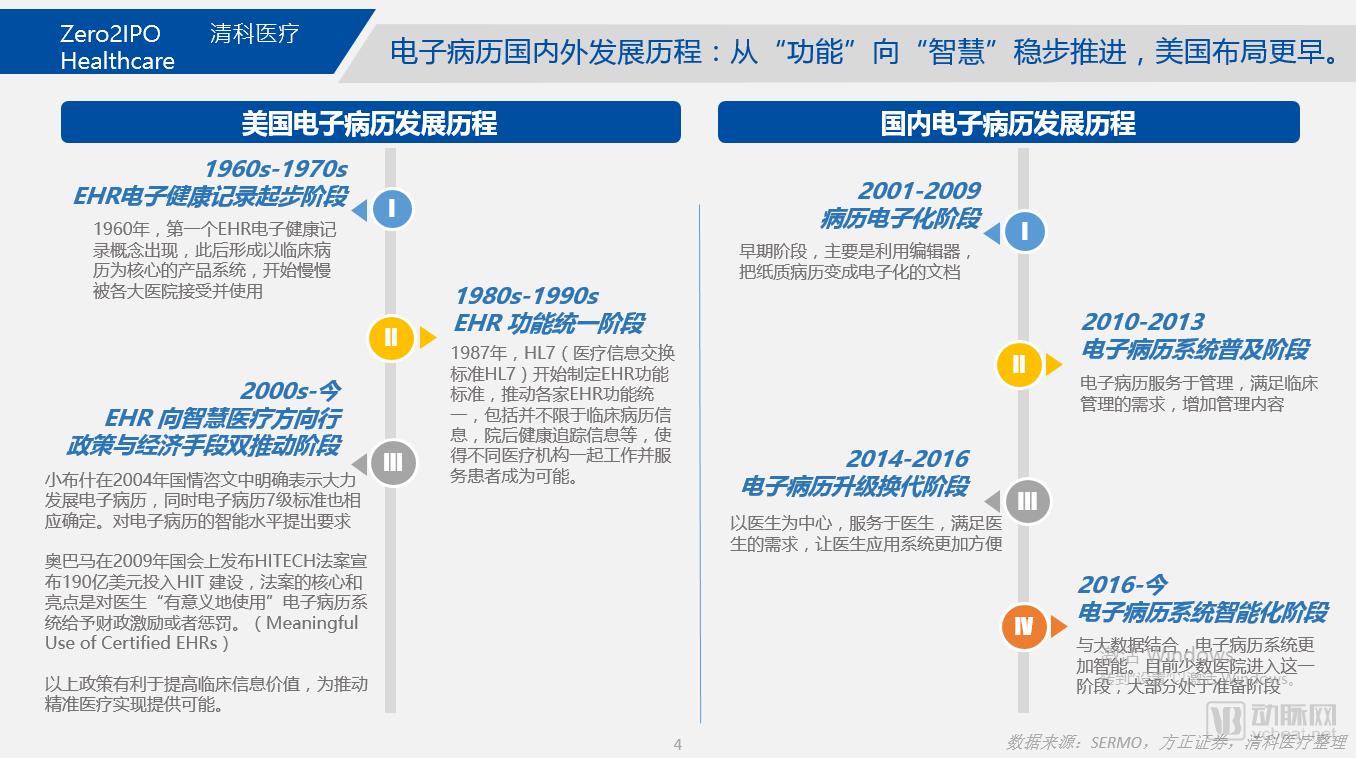

Development of Electronic Medical Records at Home and Abroad: Steady Progress from “Functionality” to “Intelligence,” with the U.S. Having an Earlier Start

Having discussed the role of electronic medical records (EMRs) in healthcare information, we now examine the developmental stages that EMRs have undergone both domestically and internationally, from basic functionality to intelligent capabilities.

Let us first examine the United States. The development of electronic medical records (EMR) in the U.S. began in the 1960s, with the first concept of Electronic Health Records (EHR) proposed in 1960. The 1960s and 1970s were primarily a trial period for healthcare institutions. In the 1980s, specifically in 1987, the Healthcare Information Exchange Standards Association began establishing standards for EHR functionalities, marking a phase focused on functional standardization. By the early 2000s, development shifted toward intelligent systems. The first core initiative was launched by President George W. Bush in 2004, who advocated for the vigorous development of electronic medical records and introduced the seven-stage EHR adoption model. Subsequently, in 2009, President Barack Obama allocated $19 billion to support EHR implementation, with the core objective of encouraging physicians to achieve “meaningful use” of EHR systems through financial incentives or penalties. These policies have been instrumental in enhancing clinical value and laying the groundwork for precision medicine. During this period, the U.S. promoted the development of electronic medical records through both economic and policy measures.

China’s development of electronic medical records (EMRs) started relatively late. The broader informatization of healthcare began in the 1980s, and the initial concept of EMRs was only proposed around 2001. Early EMR systems relied on editors to convert paper-based records into digital formats. Large-scale adoption of EMRs did not begin until 2010, driven by top-down policy implementation. Starting in 2014, greater emphasis was placed on elevating the role of EMRs, with a focus on being physician-centric—serving physicians and meeting their needs to make EMR applications more user-friendly. From 2016 to the present, with the integration of big data, hospital-based Clinical Data Repositories (CDR), and centralized data systems have gradually evolved toward intelligent solutions. Clinical Decision Support Systems (CDSS) have already been effectively implemented in large tertiary hospitals. These developmental stages are not rigid; some leading tertiary hospitals may have more comprehensive functionalities, while certain primary care institutions may lag behind the current overall trends. Nevertheless, the general trajectory shows that EMRs are evolving from basic functionality to intelligence, a trend that emerged earlier in the United States than in China.

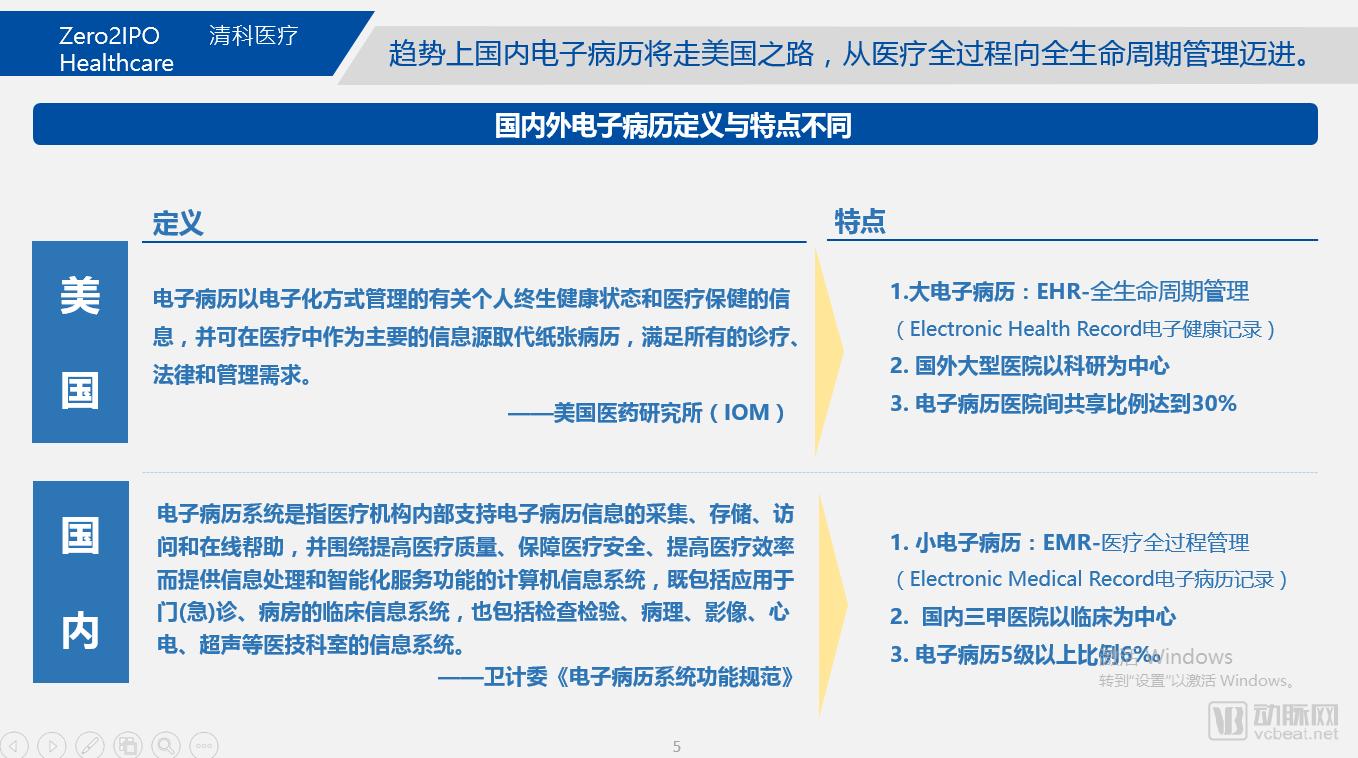

An examination of the differences in the specific definitions of electronic medical records (EMRs) domestically and internationally reveals that the United States adheres to the concept of "comprehensive EMRs." This approach primarily involves managing all information related to an individual's lifelong health status and healthcare through digital means, emphasizing full life-cycle management. Due to differences in hospital administrative systems between China and other countries, large foreign hospitals remain research-centric, focusing on advancements in personalized, one-on-one diagnostic and treatment plans. Currently, the rate of inter-hospital EMR sharing in the U.S. has reached 30%. In contrast, China is likely still in the stage of "limited EMRs," characterized by recording the entire medical process, although development has been rapid given the later start. Domestic Grade A tertiary hospitals remain clinically focused, yet there is a growing emphasis on scientific research. While no official statistical data is available for the inter-hospital EMR sharing rate among Chinese Grade A tertiary hospitals, it is reasonable to assume that this proportion is not high. According to standards for hospital EMR application ratings, only 6 per mille of hospitals have achieved Level 5 or above. Nevertheless, it is believed that China’s EMR development will follow the path taken by the U.S., ultimately progressing from recording the entire medical process toward comprehensive full life-cycle management.

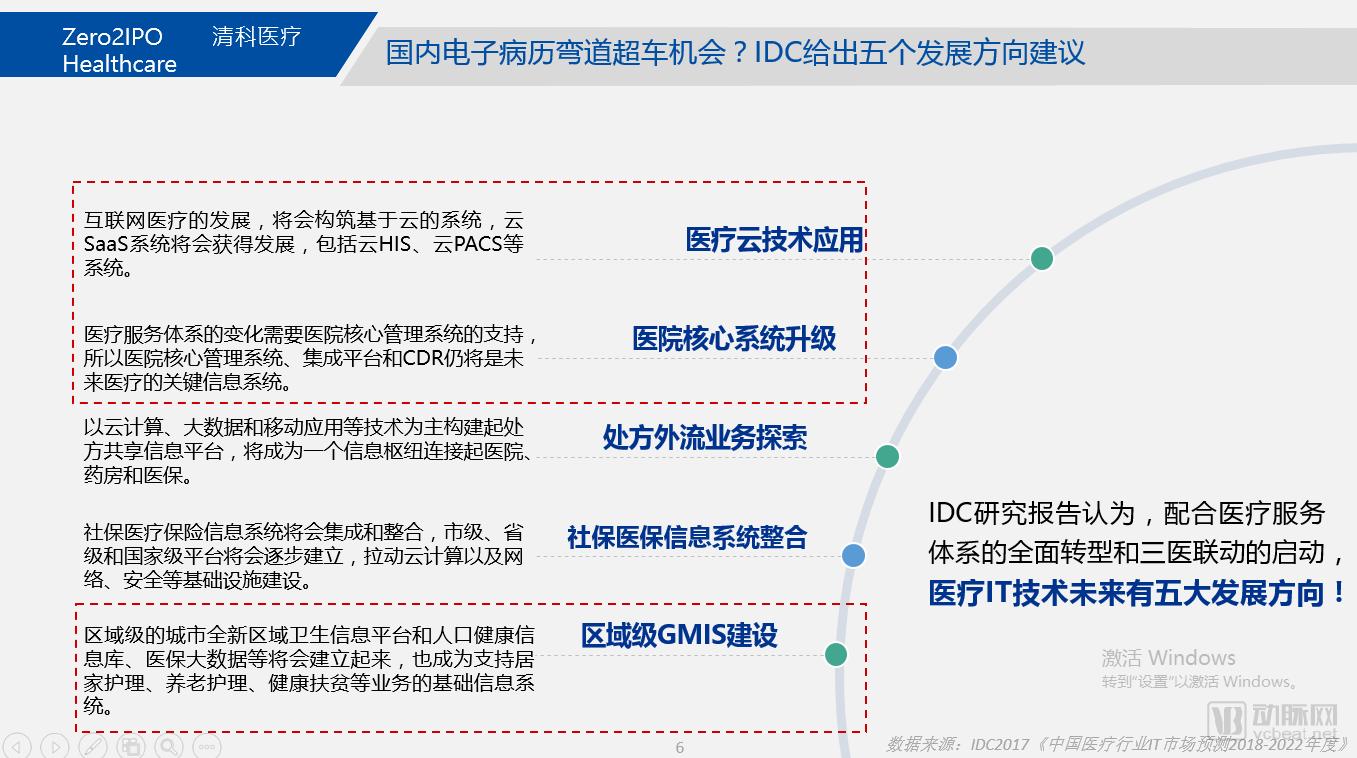

Let us re-examine whether China can achieve leapfrog development in clinical informatics. IDC has proposed five development recommendations, namely: medical cloud technology, upgrading of core healthcare systems, exploration of prescription drug management, integration of social security and health insurance information, and regional health information infrastructure construction. We believe that the gaps between China and the United States are not significant in the first, second, and fifth areas; therefore, there is still an opportunity to build robust technical expertise in these domains. Moreover, greater opportunities and potential exist during the top-down policy implementation phase.

Having reviewed the overall landscape of the industry, we will now take a closer look at the key players in the broad field of electronic medical records (EMR), analyzing them from three perspectives: in-hospital systems, inter-hospital connectivity, and big data applications.

First Direction: Within hospitals, the landscape is relatively traditional, dominated by companies specializing in health informatics and services. It requires substantial effort and time to establish a solid presence in this field for over a decade while simultaneously increasing the coverage and concentration of clinical information system adoption in Chinese hospitals. Typical representatives in this segment include companies such as Jiahe Meikang and Haitai, both of which have been operating in the electronic medical record (EMR) sector for more than ten years. Their combined market share currently approaches 30%. Jiahe Meikang has consistently made significant investments in research and development. Building upon its comprehensive EMR solutions, the company is expanding into specialty-specific EMRs, hospital clinical data centers, and clinical documentation quality control, thereby deepening its collaboration with hospitals.

Second Direction: Inter-hospital Big Data Collection and OrganizationInterconnectivity is undoubtedly an inevitable trend. This area will pose significant challenges to both technology and operations. As Mr. Lu previously mentioned, it is essential to collaborate with international best-practice clinical databases such as BMJ. Technologically, the application of Hadoop big data solutions can better support the development of healthcare big data. From an operational perspective, greater emphasis should be placed on exploring commercialization. There is a need for more business model innovations spanning from B-side enterprises to physicians and ultimately to patients. Only by making profitability feasible can we achieve deeper penetration and sustainable growth in this field.

Currently, there are several primary product forms in this field. The first is provincial-level data centers, with national-level teams undertaking more of these projects. The second is Clinical Decision Support Systems (CDSS). The third is internet hospitals. It is believed that these sectors have already entered the stage of actual operation. Representative enterprises include Huimei Medical, which explores CDSS based on the Mayo Clinic knowledge base; Baiyihui, which innovates in internet hospitals; and Community 580, which pioneers the integration of community and grassroots informatization. All are worthy of attention.

The Third Direction: Big Data Applications. This approach is quite similar to the full lifecycle management model seen in the United States. In theory, it is possible to develop products and services covering all stages of “prevention, treatment, protection, and rehabilitation.” Unfortunately, at present, we have not yet seen any company launch a comprehensive full-lifecycle management product in this field. Currently, companies with relatively higher financing or favorable valuations are mostly those that excel in specific niche segments within this domain. We encourage greater collaboration among players at this stage to foster the emergence of large-scale enterprises that can provide stronger health safeguards for the public. Notable representatives include Jiamei Online, a subsidiary of Jiahe Meikang, which has deep expertise in Clinical Decision Support Systems (CDSS); Jianyibao, which offers innovations in commercial medical insurance; Zhongpuda, specializing in clinical nursing systems; and Yunhu Technology, which is driving innovation in laboratory testing. These companies are worth watching.

Next, let us examine the market concentration of electronic medical record (EMR) systems and the level of attention from capital markets. In the United States, the combined market share of the top three EMR companies now approaches 80%, whereas in China, the combined share of the top five players remains below 50%. It should be noted that this statistic, based on IDC data derived from revenue figures confirmed via telephone interviews, is somewhat limited in robustness. We believe that when assessed by product coverage and hospital adoption, the actual market share would likely be higher. In terms of market capitalization, Epic Systems has chosen not to go public, so it lacks a fixed market valuation. However, we can refer to Cerner, the second-largest player. Although Cerner does not focus exclusively on EMRs, its EMR business has helped it command a higher premium in the capital markets, with its market capitalization nearing USD 20 billion. In China, the three representative companies in healthcare information management systems have demonstrated respectable market performance, with Donghua Software and Winning Health each achieving market capitalizations of approximately RMB 20 billion. We believe that leading EMR enterprises in China are also likely to see favorable performance in the capital markets in the near term.

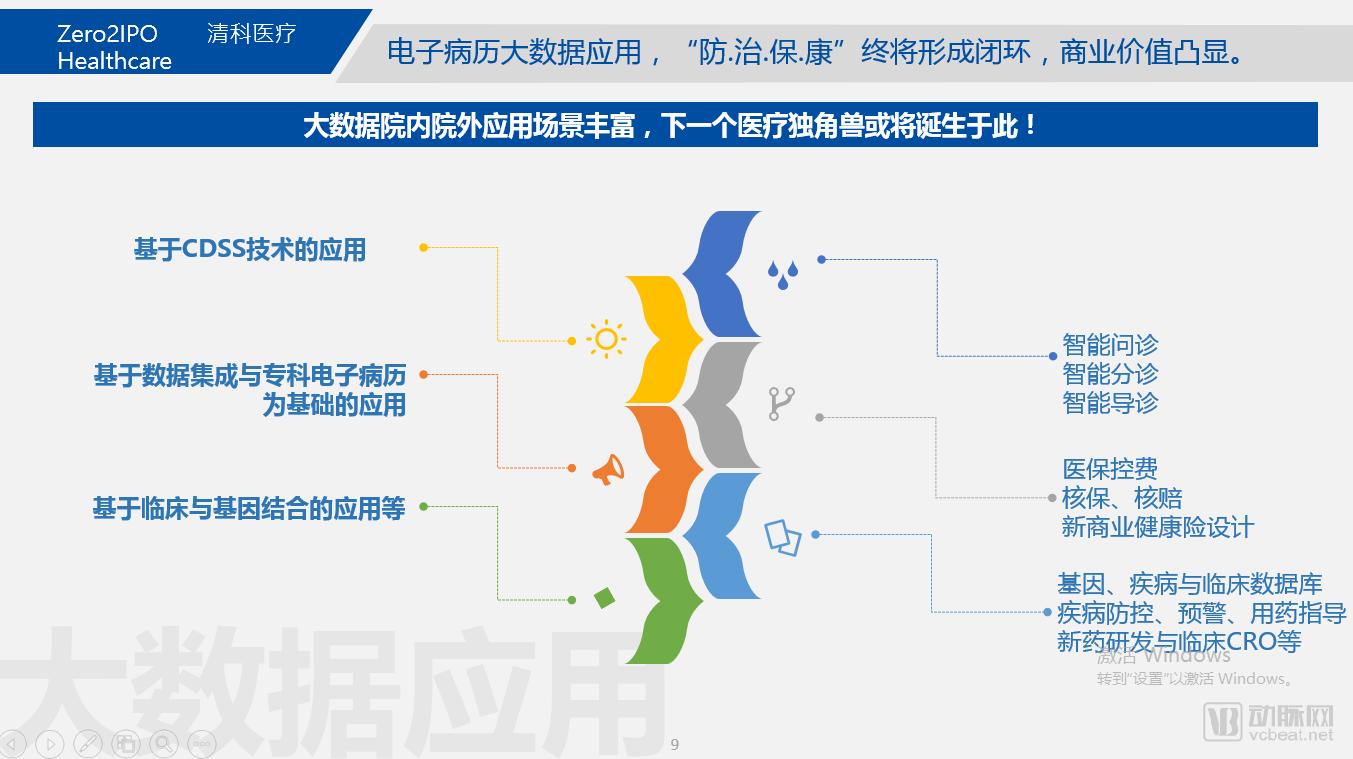

Let’s revisit the topic of big data applications. As today’s session is dedicated to big data, we will focus on the three development directions on the right, building upon the three technological foundations outlined on the left.

First, based on the application of Clinical Decision Support System (CDSS) technology, potential forms include intelligent consultation, triage, and patient guidance. This area has seen extensive exploration in internet healthcare, ranging from the early HaoDaifu triage database to later innovations such as Chunyu’s intelligent consultation services. While these efforts have paved innovative paths, we aim to foster hospital-based diagnostic and treatment innovations. By building upon in-hospital care and optimizing post-discharge follow-up and monitoring, we can achieve greater medical value and higher accuracy.

The second category comprises applications built on data integration and specialty-specific electronic medical records (EMRs), such as health insurance cost containment, underwriting, claims adjudication, and the design of new commercial health insurance products. In these areas, several relatively small startups are currently operating with rapid growth, while large insurance companies are also making substantial investments.

The third area focuses on applications based on clinical and genomic data, as well as their integration with new drug development. As mentioned by several previous speakers in their presentations, Mr. Li from Judao Technology has developed big data products that combine genomic and clinical data; Mr. Zhao from Taimei Medical Technology has explored innovations in new drug R&D; and Zechuang Tiancheng, a physician group, has been investigating how to better integrate medical big data. We believe these fields will continue to offer commercial opportunities in the future. Those who can successfully connect the entire healthcare lifecycle may well become the next generation of healthcare unicorns.

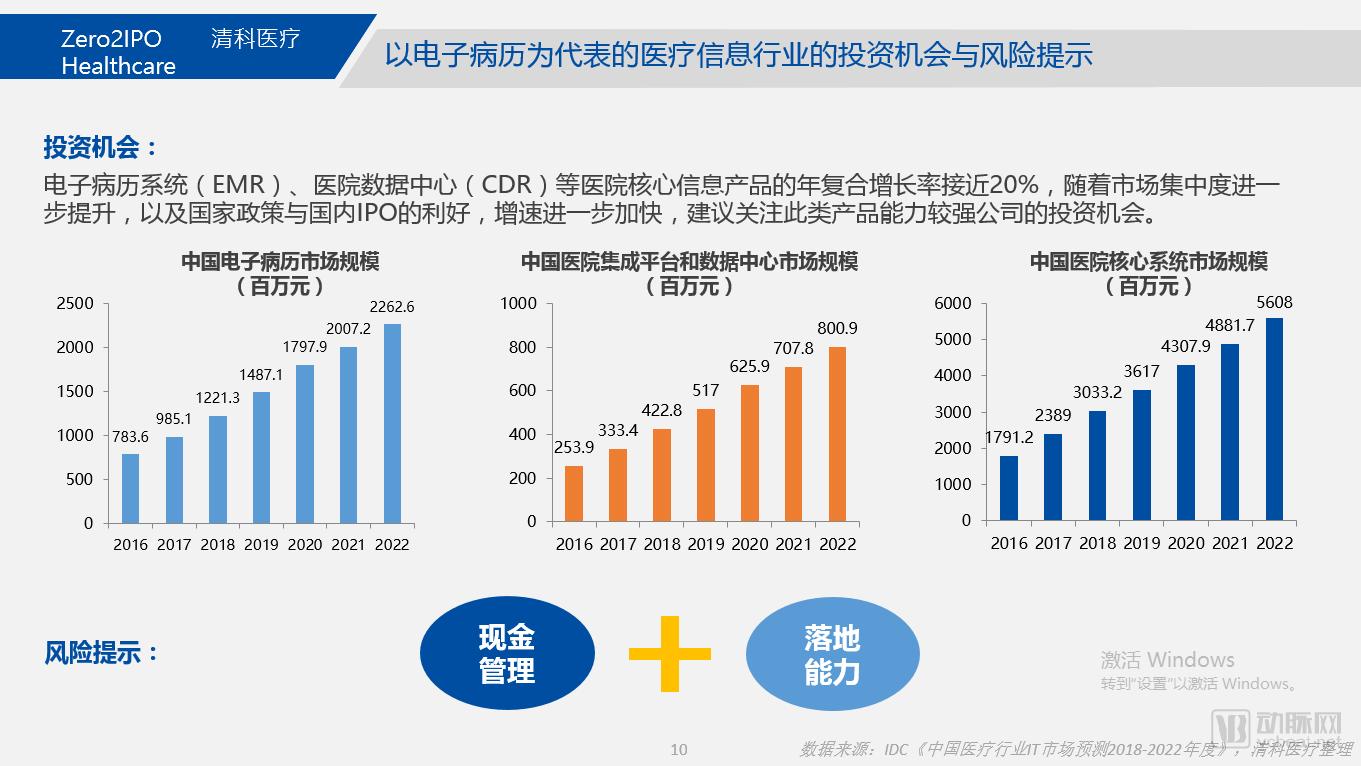

Finally, let us examine the remaining investment opportunities in the informatization sector, represented by electronic medical records (EMR). We observe that the core hospital informatization systems, such as EMR and Clinical Data Repositories (CDR), are achieving a compound annual growth rate (CAGR) of nearly 20%. With favorable policy support and further technological advancements, we believe this growth rate is poised to accelerate. Regarding risks in this sector, we highlight two key concerns: cash flow management and implementation capability. These correspond respectively to the relatively traditional software business and the more innovative big data business.

These two aspects are relatively straightforward to understand. The first concerns cash flow: the cycle from tendering to bid award and implementation in hospitals is lengthy, and hospital payment terms are also extended, posing challenges for companies in balancing their operational cash flow. The second pertains to implementation capability in big data applications. While the functionalities are comprehensive, whether they can be effectively applied in in-hospital or out-of-hospital medical scenarios still tests the team’s commercialization and execution capabilities.

We have discussed this at length, and we remain optimistic about the industry as a whole. With further policy encouragement for industry development, favorable IPO policies, and over a decade of accumulated growth in the electronic medical records (EMR) sector, we believe that now is an opportune time to invest.

Finally, allow me to introduce Zero2IPO Healthcare. As the healthcare investment and investment banking platform under the Zero2IPO Group, we integrate the Group’s four core divisions: Zero2IPO Capital, Zero2IPO Venture Capital, Zero2IPO Asset Management, and Zero2IPO Fund of Funds. Our mission is to drive the long-term development of the healthcare industry through both investment banking services and direct investments. We provide direct equity investments for early-stage and late-stage projects, while offering investment banking services for growth-stage companies.Our key focus areas include:1. Medical devices, particularly in vitro diagnostics (IVD), with an emphasis on leading market players;2. Top-tier opportunities and technological innovations in biopharmaceuticals;3. Innovations in healthcare services, specifically specialty care centers focused on single disease categories;4. Healthcare industrial internet and healthcare informatization, which remain areas of sustained interest.We look forward to collaborating with more high-quality enterprises and prestigious investment institutions. Thank you!