China Pharma Innovation Surges: A Breakthrough Year for Domestic R&D

Editor’s Note: This article is republished from 36Kr, authored by Mengxiangjia Caicai. VCBeat has been authorized to repost it.

Pharmaceuticals are the most standout segment within the healthcare and wellness sector this year.

If we were to summarize China’s pharmaceutical industry in 2018 in one sentence, we would describe it as “a year of explosive growth in independent R&D and innovation.” This is evidenced by trends across capital markets, policy landscapes, talent dynamics, and secondary market performance.

This article will discuss the following topics:

How Is the Pharmaceutical Sector Faring in Investment and Financing Amid the Capital Winter?

“The Wave of Returnees” Has Formed: How Will It Impact Capital Market Dynamics?

Judgment: Innovative Drugs Enter the Harvest Period

Mixed Signals in the Macro Environment: Where Is Policy Headed?

Amidst Dramatic Changes, What New Trends Will Emerge in 2019?

The golden decade of entrepreneurship in the mobile internet sector ended in 2018. However, the pharmaceutical sector presents a completely different landscape—with news of major funding rounds emerging almost every one to two weeks. The golden age of the pharmaceutical industry has only just begun.

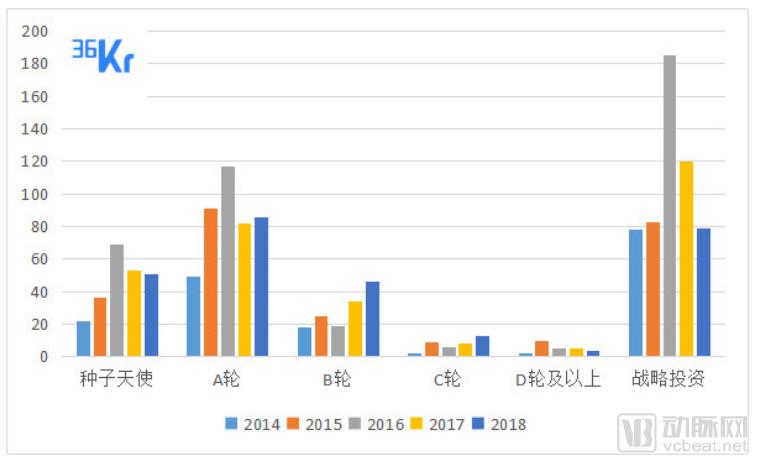

The author has compiled data on investment and financing events in the pharmaceutical sector from 2014 to 2018. We observe that the number of financing events was merely 171 and 254 in 2014 and 2015, respectively. Starting in 2016, the sector experienced a sudden surge in activity, with the number of financing events peaking at 401. Despite the onset of a capital winter, the figures for 2017 and 2018 did not decline significantly, standing at 302 and 279, respectively, thereby maintaining overall stability.

It is not entirely without impact.

Shi Guomin, Managing Director of Huagai Medical Fund, told the author, “The capital winter is reflected not only in project financing but also in fund fundraising, and even in funds of funds. The entire year of 2018 saw a significant decline, with many projects and funds under considerable pressure.”

“Financing pressures will compel funds to adjust their investment strategies,” he said. “Regarding strategic adjustments, first, they will act more rationally and have greater discretion in project selection. With valuations declining—a trend already evident in many projects recently contacted—many projects are now prioritizing survival.”

“Second, it influences whether funds maintain consistency with their previous strategies or make adjustments. This may include shifts in the selection of specific investment sub-sectors, moving away from merely chasing concepts that sound sophisticated but represent what is known as ‘high-level repetition.’ The pace of investment is also expected to slow down. However, many funds continue to pursue high-quality, differentiated projects that align with their strategies. There is a clear divergence in the market, both among funds and projects. Furthermore, both funds and portfolio companies are placing greater emphasis on internal capabilities, including post-investment value-added services, resource integration, and the achievability of future corporate expectations,” analyzed Shi Guomin, Managing Director of Huagai Medical Fund.

Li Yingjie of Inno Angel Fund told the author, “The capital winter will not slow down our investment pace. Against this backdrop, talented individuals who dare to embark on entrepreneurship are worth investing in, though we will exercise greater caution in our investment decision-making process. As for our investment strategy, there will be no significant overall change during the capital winter; we will continue to focus on early-stage investments and the translation of original innovations into commercial applications. However, we will place greater emphasis on elite-led startups, with an increased allocation to hard technology and biopharmaceuticals.”

Elysium VC, a venture capital firm based in Silicon Valley, primarily invests in projects in Silicon Valley and Europe. However, the current “capital winter” has prompted the firm to adjust its strategy for helping its portfolio companies enter the Chinese market. Jackie, a partner at Elysium VC, stated, “This year’s fundraising efforts have indeed been affected by the capital winter, and we believe it will become even more challenging starting next year. Accordingly, we will make certain adjustments to the strategies our portfolio companies use to enter the Chinese market. Meanwhile, given the visible downturn in global economic expectations, we are exercising greater caution with early-stage investments than in the past. In the long run, this is merely a minor inflection point rather than a major turning point, and abundant opportunities remain.”

Among them, one niche sector has performed particularly notably—innovative drug R&D.

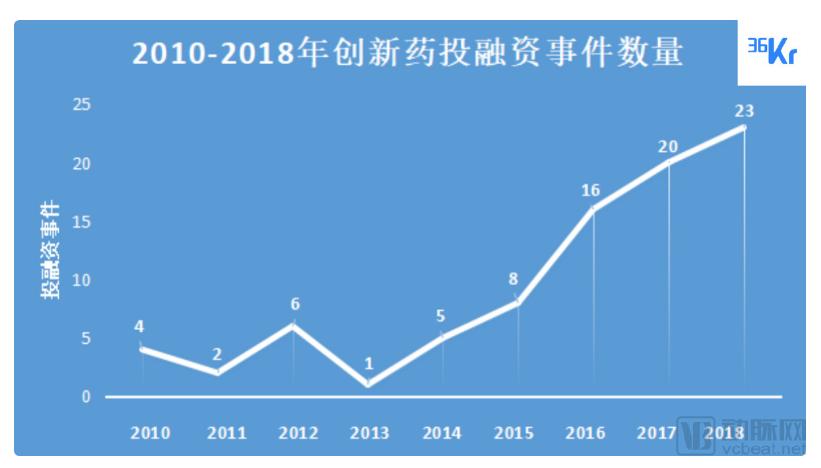

In terms of the number of investment and financing events, domestic innovative drug R&D was merely “scattered sparks” before 2014, with only 1–6 investment deals occurring annually; after 2016, it began to “ignite into a flame,” with the number surging to 16; in the past two years, the growth momentum has been robust, reaching a peak of 23 investment deals in 2018.

In 2018, despite the capital winter facing innovative drug projects, financing amounts did not decline but instead continued to grow. This year, the financing scale for seed and angel rounds has generally been around tens of millions of RMB, while Series A rounds have often reached over 100 million RMB, with Series B and later rounds also starting at over 100 million RMB.

Although the pharmaceutical industry is characterized by long development cycles, the rapid pace of financing in recent years underscores strong investor confidence in this sector. Since 2016, there have been cases of companies completing multiple rounds of financing within a single year. In 2016, both Chengzhi Share and Hua Medicine completed two rounds of financing; Hua Medicine has since listed on the Hong Kong Stock Exchange, with further details on its IPO provided later in this article. In 2017, I-Mab Biopharma and CanSino Biologics each secured two rounds of financing, while Shengshi Taike completed three rounds. In 2018, Lisheng Pharmaceutical and Xinkanghe Biology also each completed two rounds of financing within the year.

Many entrepreneurs and investors have also strongly felt this wave of trends in innovative drugs. Sun Binyuan, founder of Nuoling Biopharma, stated, “Two events that occurred in the pharmaceutical industry in 2018 will have a significant impact on the future development of the entire biopharmaceutical sector: first, healthcare system reforms have facilitated the rapid introduction of original research products; second, the price of imported PD-1 inhibitors in China is lower than that in the United States and Hong Kong, making it the lowest globally. These two events are not coincidental; they likely mark a turning point for China’s pharmaceutical industry, shifting its focus from imitation to differentiation.”

Zhou Mi, Managing Partner at Puhua Capital, believes that from the perspective of national policy, the government is curbing low-level imitation and redundant construction, while also squeezing out inefficiencies in the distribution chain. However, the state has remained highly proactive in encouraging innovation, which overall creates a favorable environment for venture capital and innovation incubation. This precisely presents opportunities for investment institutions focused on early-stage ventures and advanced technologies.

At the beginning of the year, the Hong Kong Stock Exchange (HKEX) launched a “race” to attract biotechnology companies by implementing unprecedented reforms to its listing rules—“allowing innovative companies to list with dual-class share structures” and “permitting pre-revenue or unprofitable biotechnology companies to list in Hong Kong.”

These two regulations effectively open the door for innovative biotechnology enterprises, as the development of novel drugs is an industry characterized by extremely high upfront investments and exceptionally long cycles, often described as requiring “ten years and one billion dollars.” Previously, many biotech companies with significant technical barriers were unable to go public due to their lack of revenue.

Currently, companies listed on the Hong Kong Stock Exchange (HKEX) include Hua Medicine, Innovent Biologics, BeiGene, and Ascletis Pharma. Among them, Hua Medicine completed a Series E financing round worth up to $117.4 million in March this year, with investors including Blue Pool Capital, Allspring Healthcare Investments, K11 Investments, and WuXi AppTec, followed shortly by its listing in Hong Kong. Biopharmaceutical companies currently preparing for IPOs include Ascentage Pharma, Junshi Biosciences, CStone Pharmaceuticals, MicuRx Pharmaceuticals, Mabspace Biotechnology, and CanSino Biologics. However, market performance indicates that only high-valuation pharmaceutical companies have successfully listed on the HKEX.

Following their public listings, innovative drug companies have been able to raise substantial capital, which has significantly advanced their R&D processes and accelerated commercialization.

In addition to the Hong Kong Stock Exchange giving the green light to biotech IPOs, the Shanghai Stock Exchange has also announced positive developments for innovative pharmaceutical companies. At the China International Import Expo in late November, the state announced the establishment of the STAR Market on the Shanghai Stock Exchange and the pilot implementation of a registration-based IPO system. Its positioning is very clear: it is designed specifically to serve technology-driven, innovative enterprises. The creation of the STAR Market sends a strong signal encouraging the research and development of innovative drugs, serving as a significant boost of confidence for innovative pharmaceutical companies.

Domestic policies incentivizing pharmaceutical innovation, coupled with China’s vast market size, are attracting an increasing number of highly experienced overseas talents to return home. Indeed, these returnees have coalesced into a powerful “wave of overseas talent returning to China.”

Data shows that the Chinese Biopharmaceutical Association (CBA) is the largest Chinese-American biopharmaceutical association in the United States, with more than 5,000 registered members. In 2018, approximately half of its members had their own entrepreneurial ventures or collaborative exchange projects in China, frequently traveling between China and the United States. Among the more than 6,000 members of the China Chapter of the Sino-American Pharmaceutical Professionals Association (SAPA), nearly 2,000 have returned to work in China.

Through discussions with several U.S. dollar-denominated funds, the author has learned that American pharmaceutical companies with Chinese heritage are highly favored. These companies possess leading U.S. pharmaceutical technologies, enabling them to effectively penetrate the U.S. market, while the Chinese background of their core teams helps them establish a foothold in the Chinese market. As a result, such enterprises can simultaneously access both the U.S. and Chinese markets and gain recognition from investment institutions in both countries.

Regarding pricing, some market views suggest that China’s biopharmaceutical sector has developed a bubble, making overseas projects more affordable. However, an anonymous investor interviewed by the author noted that project valuations in the United States are actually polarized: while average-priced projects tend to be cheaper than their Chinese counterparts, those with truly leading-edge technologies command prices far higher than those in China.

Shi Guomin, Managing Director of Huagai Medical Fund, told the author, “The wave of overseas returnees is unlikely to have a substantial impact on investment amounts; valuations still depend on the intrinsic quality of the projects. For projects involving U.S. dollars, if they continue to adopt an offshore corporate structure and require capital outflows, this will affect their valuations.”

Li Yingjie of Inno Angel Fund also expressed a similar view, stating, “Our investment strategy and ticket size for ‘returnee’-founded companies are not deliberately differentiated from those for domestic enterprises. While prestige universities provide a foundation, specific valuations ultimately depend on the individuals and the projects themselves.”

As for investment priorities, the author believes that focus should be placed on independent innovation and R&D, rather than on licensing-in overseas products. To illustrate with some projects previously covered by the author: Deepwise Medical has recently obtained FDA clearance for its self-developed AI-based image acquisition technology and has secured investments from domestic and international institutions such as ZhenFund, Baidu Ventures, and Facebook investor Jim Breyer; Nuoling Biotechnology independently developed ADC polymer conjugation technology in the United States and entered the Chinese market, completing a RMB 50 million Series A financing round; IDbyDNA launched its patented clinical metagenomic analysis platform and established relatively mature market channels in the United States, South America, Europe, and China.

Shi Guomin, Managing Director of Huagai Medical Fund, believes that “the wave of returnees is inherently a positive development. Moreover, the new cohort of returning overseas professionals is more goal-oriented than in the past, as evidenced by the quality of projects they bring and their practical operational capabilities in running enterprises. We are even seeing some non-Chinese foreigners joining Chinese teams. This trend provides investment funds with additional options, and funds are more inclined to consider collaboration opportunities for projects that effectively leverage overseas resources to tap into the Chinese market.”

Meanwhile, Shi Guomin also analyzed the implementation status of “returnee-founded enterprises.” He stated, “Under the policy openness that aligns China’s pharmaceutical innovation with international standards, this wave of returnee talent will enjoy greater advantages. However, the greatest challenge for these overseas-introduced projects remains their concrete implementation in China, including advancing clinical trials, future production and sales, collaborative transactions involving specific new drug candidates, and cooperation, mergers, and integration with industrial companies.”

"Based on this year's R&D achievements, the author believes that domestic innovative drugs have entered a harvest period."

Thanks to the priority review and approval system, a large number of imported new drugs and domestically produced new drugs have been rapidly approved for market launch. The fastest record was set this April, when Merck & Co.’s nine-valent human papillomavirus vaccine (9-valent HPV vaccine) received conditional marketing approval in just nine days.

In 2017, only one domestically developed Class 1 innovative drug (the recombinant Ebola virus disease vaccine) was approved for market launch. By 2018 (as of December 24), this number had surged to five. This year, the National Medical Products Administration approved a record-high number of innovative drugs, bringing 48 new molecular entities to China, including six drugs that received global first-time approval.

Another development that has drawn particular attention is the launch in May of Hengrui Medicine’s self-developed 19K (pegteograstim), the first long-acting formulation in China designed to help reduce infections following chemotherapy. In December, another blockbuster drug made its debut: Junshi Biosciences’ anti-tumor PD-1 antibody was approved for marketing, becoming the first domestically produced PD-1 antibody drug to reach the market. The PD-1 sector has been exceptionally active this year. Hengrui Medicine, Innovent Biologics, and BeiGene have already submitted new drug applications for their respective PD-1 inhibitors. Following Junshi Biosciences, products from these three companies are also expected to hit the market soon—possibly next year, or perhaps even before the end of this year.

From the broader macroeconomic environment, this year has exhibited a mixed trend of both cold and hot conditions.

The fervent enthusiasm for the pharmaceutical sector, which surged last year, persisted into the first half of this year. During this period, star stocks in the secondary market—such as BGI Genomics, GenScript, and Hengrui Medicine—bolstered market confidence significantly. However, in the second half of the year, this heightened enthusiasm was dampened by a series of setbacks. The emergence of the Changsheng Biotechnology rabies vaccine fraud scandal, followed by a broad decline in the stock market, left pharmaceutical stocks no exception to the downturn.

The pharmaceutical industry is highly susceptible to policy-driven fluctuations, making policy trends particularly critical. Where will policy guidance lead us in the future? This year, three aspects deserve special attention:

Policies supporting innovative drugs are further extended: on one hand, the drug review and approval system encourages innovation by streamlining processes and accelerating reviews; on the other hand, the state will implement tax reductions on corporate R&D expenditures, helping R&D-focused pharmaceutical companies increase their profits.

Centralization of Authority in the National Healthcare Security Administration: This year’s government institutional reform has been extensive, involving the dissolution of the China Food and Drug Administration (CFDA) and the Office of the Leading Group for Deepening Medical Reform, and the establishment of the National Healthcare Security Administration (NHSA). These institutional changes have consolidated most pharmaceutical- and healthcare-related functions under the NHSA, including formulating medical insurance policies, overseeing medical insurance funds, setting prices for pharmaceuticals and medical services, developing bidding and procurement policies for drugs and medical services, and supervising healthcare institutions within the scope of medical insurance coverage.

“4+7” City Centralized Procurement Program: At year-end, the national government rolled out this landmark policy in the pharmaceutical sector, requiring explicit procurement volumes for centralized drug purchasing in four municipalities directly under the central government and seven provincial capitals/cities with independent planning status. This marks the first nationwide attempt at joint tendering and procurement.

The accelerated review process, streamlined procedures, and reduced taxes and fees for innovative drugs, coupled with the continued implementation of policies encouraging innovation, constitute a significant boon to the future development of novel therapeutics. The consistency evaluation of generic drugs has raised standards for pharmaceutical companies in the market, thereby driving improvements in drug quality. Meanwhile, the combination of zero tariffs on imported anticancer drugs and the “4+7” city-based centralized procurement program poses substantial challenges to drug pricing, potentially squeezing pharmaceutical companies’ profit margins and leading to lower drug prices.

As discussed above, in 2018 we witnessed new policies in the pharmaceutical sector, new trends in capital flow, and also observed the “capital winter” in the external environment. Where will these dramatic changes lead us? The author would like to offer some predictions for 2019 for joint discussion with readers.

1. Competition in the PD-1 sector has become intensely fierce. Junshi Biosciences’ PD-1 inhibitor has already been launched, while Hengrui Medicine, Innovent Biologics, and BeiGene have submitted new drug applications for their respective PD-1 inhibitors. Consequently, industry focus must shift beyond R&D to encompass market strategies as well.

2. AI’s application in pharmaceutical R&D remains relatively underdeveloped across the three key stages: preclinical research, clinical trials, and regulatory approval for market launch. These stages are characterized by extensive repetitive experimentation, prolonged timelines, and high costs, creating significant opportunities for AI integration in the future. The reliability of AI-driven pharmaceutical technologies still requires further validation over time, with a major breakthrough expected to emerge in the coming years.

3. The “returnee wave” will continue to expand, with more highly experienced overseas talents bringing their expertise back to China; they will become a cohort highly favored by capital. Meanwhile, more investors will begin to allocate resources to projects in the United States or the United Kingdom. The emergence of this “returnee wave” also raises the bar for technical capabilities among domestic enterprises.

4. As pharmaceutical policies advance, future market demands for technical barriers will rise, which is a significant boon for innovative drugs, while the outlook for generic drugs is likely to become increasingly challenging.

Overall, the capital winter of 2018 posed challenges to the pharmaceutical sector, and polarization is expected to become more pronounced in the future. High-quality innovative projects will remain favored by investors, albeit with potentially lower valuations; whereas projects with low technical barriers may need to undergo transformation to survive. The tide of the times is pushing companies toward a day of explosive innovation.