Sinic Holdings Releases '2018 White Paper on China's Innovative Drug Industry Development'

Preface: Innovative drugs have become the hottest topic in the healthcare industry. In recent years, driven by policy reforms and incentives, heightened corporate awareness and investment, a significant influx of overseas talent returning to China, rapid advancements in biotechnology, and strong capital interest and pursuit, the entire healthcare ecosystem has been paving the way for innovation.

Source: Huaxia Jishi. Republished with authorization from VCBeat.

As healthcare reforms deepen, major policies impacting the pharmaceutical industry—such as the “Two-Invoice System,” “Generic Drug Consistency Evaluation,” “Medical Insurance Cost Containment,” and “Restrictions on Adjunctive Medications”—have been continuously introduced. In particular, the recently implemented “Volume-Based Procurement” policy has placed immense survival pressure on traditional generic drug companies driven by marketing. The era of extensive growth dividends in the pharmaceutical industry has largely come to an end, and a new era characterized by innovation-driven “product supremacy” is imminent, making industrial transformation and upgrading an inevitable trend.

Based on in-depth industry research, Huaxia Jishi released the "White Paper on the Development of China's Innovative Drug Industry in 2018." The white paper is divided into five sections: Overview of Innovative Drugs, Chemical Innovative Drugs, Antibody Innovative Drugs, Cell Therapy Innovative Drugs, and Traditional Chinese Medicine (TCM) Innovative Drugs. It conducts separate studies on the four most significant and highly watched sub-sectors of the pharmaceutical industry—chemical drugs, antibody drugs, cell therapy drugs, and TCM—with content covering:

(1) Registration Status (Clinical Trial Application, Manufacturing, Approval Status, and International Regulatory Filings)

(2) Profile of Representative Drugs (R&D Costs and Market Sales Performance)

(3) R&D Status of Key Enterprises (R&D Expenditure and Product Pipeline Distribution)

(4) Market and Policy Environments for Development

(5) Opportunities, Challenges, and Future Trends in Development

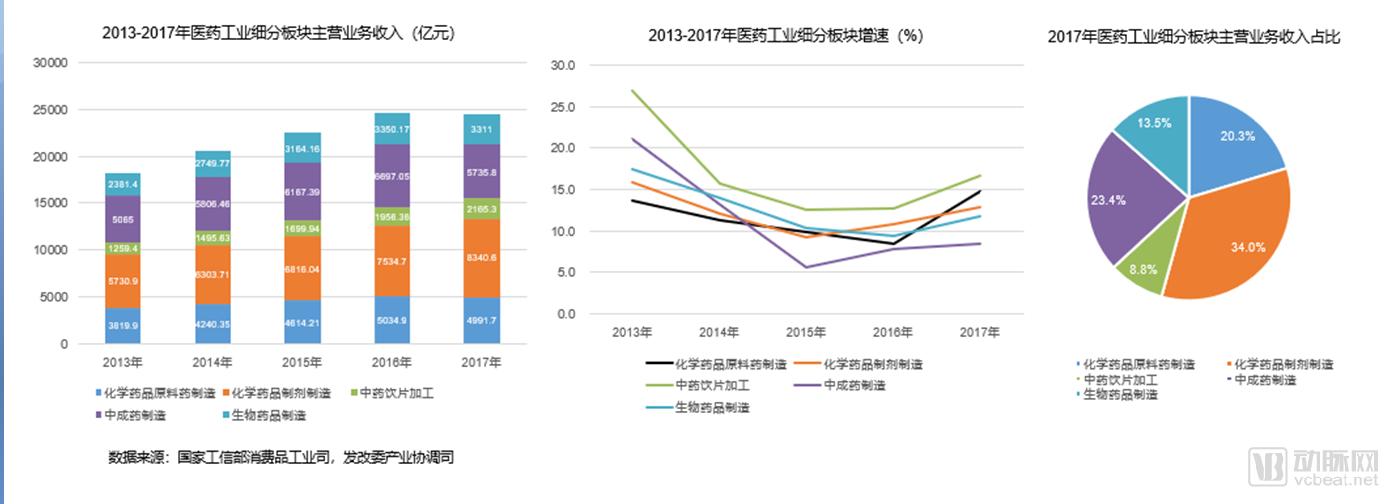

According to data released in recent years by the Consumer Goods Industry Department of the Ministry of Industry and Information Technology (MIIT) and the Industrial Coordination Department of the National Development and Reform Commission (NDRC), chemical pharmaceutical preparations account for the largest share among the subsectors of China’s pharmaceutical industry, followed by the manufacturing of traditional Chinese medicine (TCM) proprietary medicines and biological products. Within these subsectors, TCM decoction pieces and the manufacturing of chemical pharmaceutical raw materials have exhibited relatively rapid growth. Due to tightening regulatory policies, TCM injections have experienced a significant decline, resulting in slower growth for the manufacturing of TCM proprietary medicines.

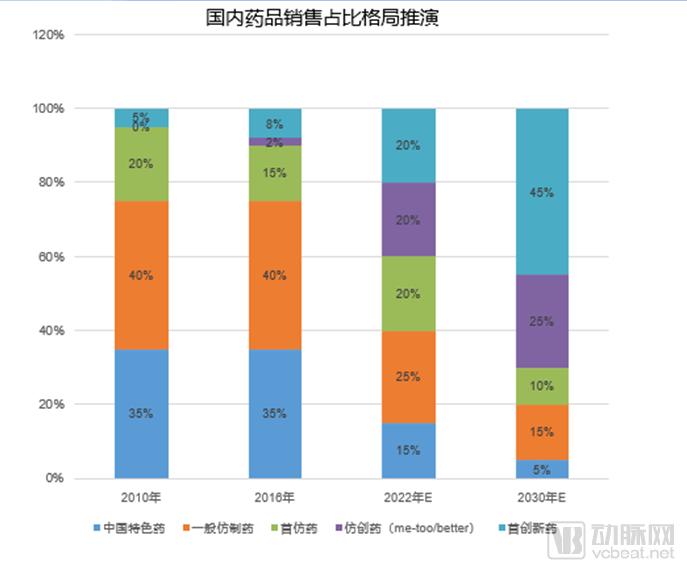

In the current landscape of China’s pharmaceutical market, traditional Chinese medicine (TCM) proprietary products and generic drugs—distinctive to China—account for nearly 90% of the market share. In the future, the overall market share of innovative drugs will gradually increase, while generics and follow-on innovations will remain mainstream in the short to medium term. Over the long term, as international competition intensifies within the pharmaceutical industry, original new drugs will constitute the largest proportion. Meanwhile, the market shares of TCM injections and adjuvant therapies are expected to decline gradually.

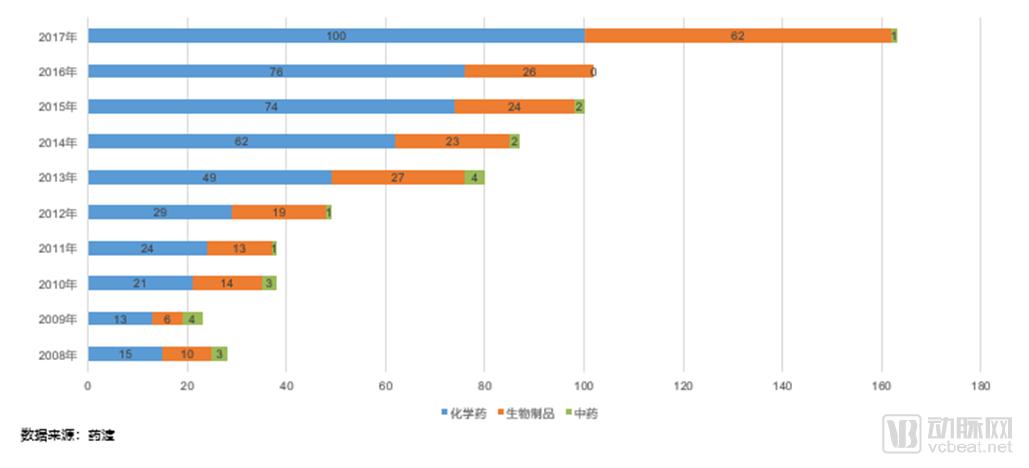

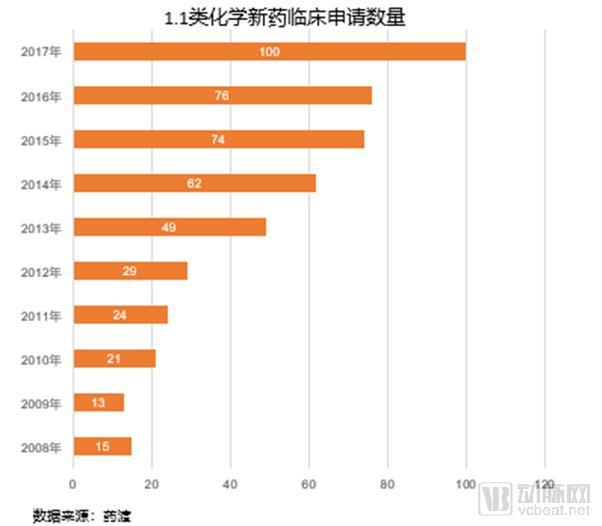

In recent years, the number of innovative drugs in China’s Class 1 chemical and biological drug sectors has experienced explosive growth, rising from 29 and 19 in 2012 to 100 and 62 in 2017, respectively. In contrast, applications for innovative traditional Chinese medicine (TCM) drugs have remained largely stagnant.

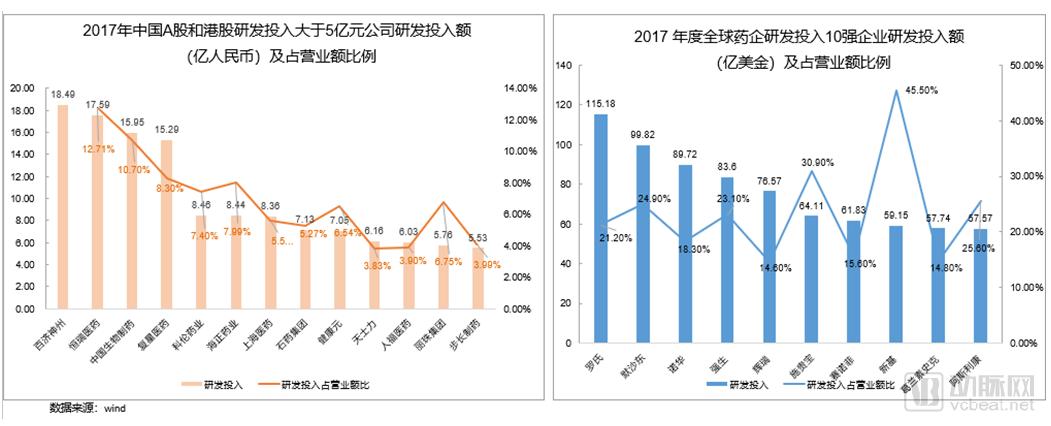

Chinese pharmaceutical companies have significantly increased their R&D innovation investment in recent years. However, compared with leading international pharmaceutical innovation giants, China’s pharmaceutical innovation remains in its early stages, both in terms of resource accumulation and actual investment. According to the Shenwan Industry Classification from the Wind database, the total R&D expenditure of all pharmaceutical and biotechnology companies listed on China’s A-share market in 2017 amounted to RMB 32 billion, which was less than the R&D spending of a single multinational corporation. This disparity is also attributable to the fragmented nature and insufficient scale of China’s pharmaceutical industry, which comprises more than 5,000 enterprises above designated size, compared with just over 200 in the United States.

Currently, the main entities of pharmaceutical innovation enterprises in China can be divided into four categories: clusters of large enterprises, clusters of innovative small companies, clusters of specialized R&D firms, and clusters of research institutes.

The number of registration applications for Class 1.1 chemical drugs in China maintained rapid growth from 2011 to 2016, making them the primary category for clinical trial applications of Class 1 new drugs. In 2017, Class 1 new chemical drug applications accounted for 61.3% of all Class 1 new drug applications.

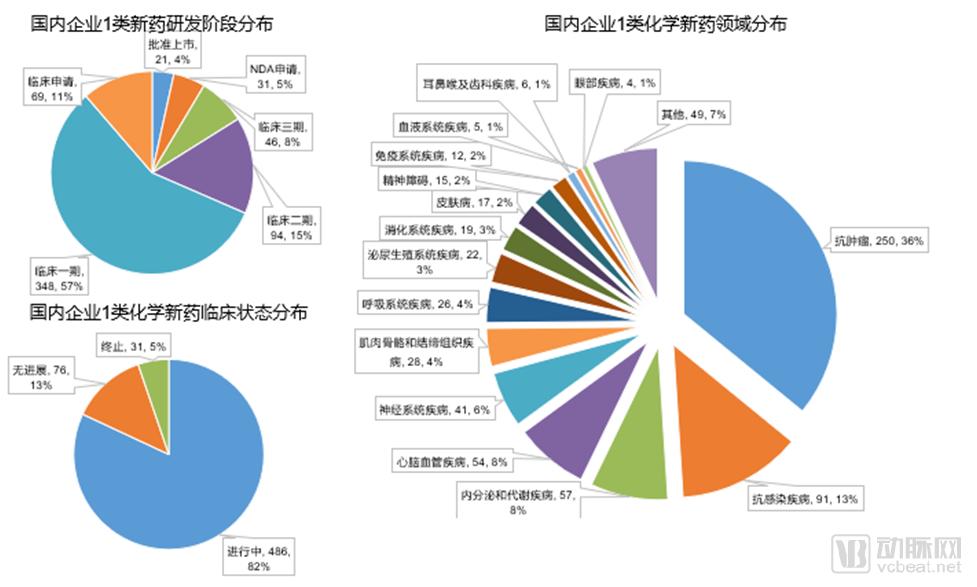

As of October 2018, there were a total of 610 Class I chemical drug projects submitted for clinical trials in China. Currently, 57% of these projects are in Phase I clinical trials, with 21 new drugs approved, accounting for 4%.

Domestic enterprises’ Class 1 new chemical drug applications are gradually entering the harvest period, with 31 at the New Drug Application (NDA) stage and 46 in Phase III clinical trials.

Among Class 1 new chemical drugs filed by domestic companies, 82% of the projects are in clinical development, and approximately 5% have been terminated.

The therapeutic areas with a high proportion of Class 1 novel chemical drugs are oncology, infectious diseases, endocrine disorders, and cardiovascular diseases, which correspond to the most prevalent diseases in China.

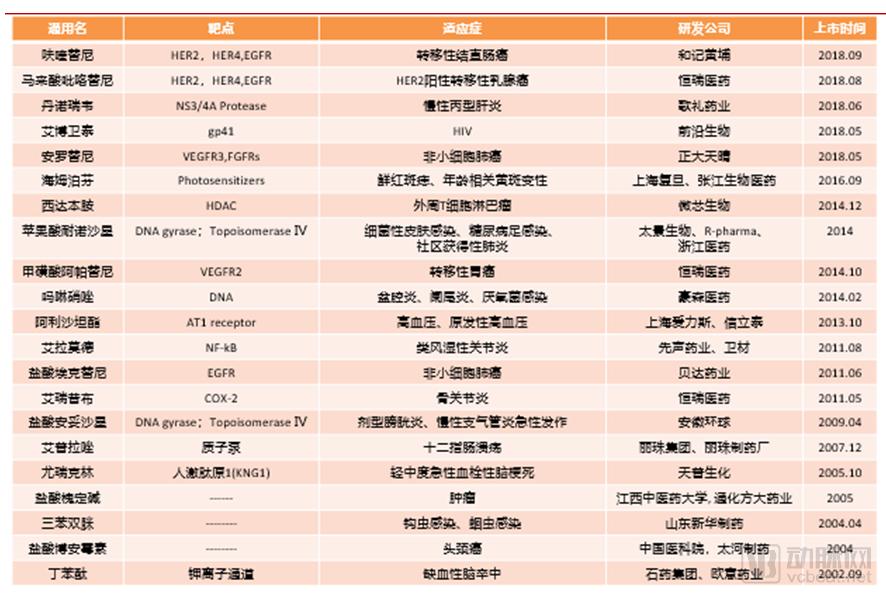

Since 2002, 21 Class 1.1 innovative chemical drugs have been approved for marketing in China. An analysis of their characteristics reveals that early approvals were predominantly me-too innovative drugs, which benefited from relatively robust foundational research, rapid clinical trial progress, high success rates, and lower R&D costs. In recent years, approved agents such as anlotinib and albuvirtide have evolved into the me-better category, while apatinib, pyrotinib, and chidamide have emerged as best-in-class novel drugs. However, there remains a lack of breakthrough first-in-class agents.

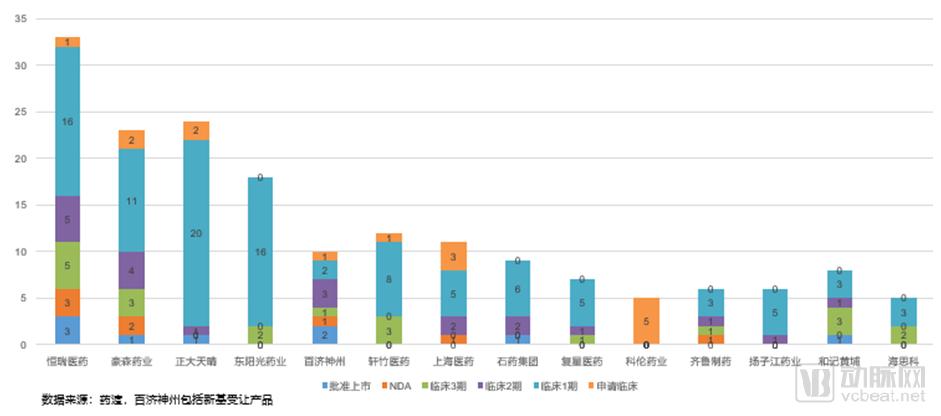

In terms of the number of Class 1.1 innovative chemical drug candidates, the top three domestic companies with the largest portfolios are Hengrui Medicine, Hansoh Pharmaceutical, and Chia Tai Tianqing. Additionally, Dongyangguang Pharmaceutical, BeiGene, Xuanzhu Pharmaceutical, and Shanghai Pharma each have more than 10 candidates.

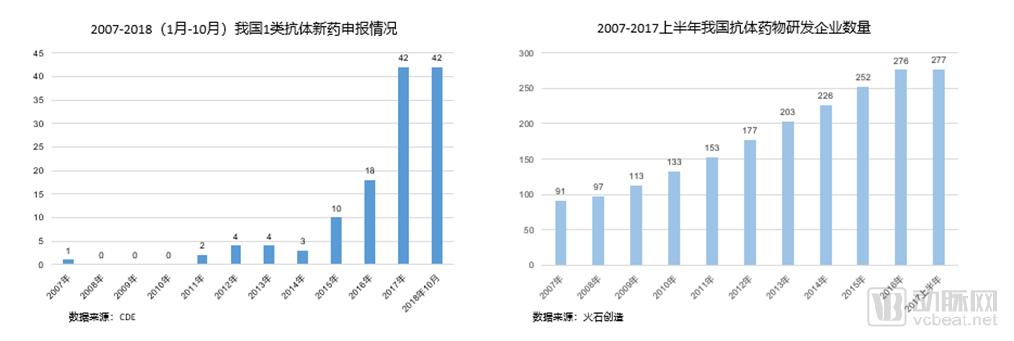

Since 2015, the number of antibody drug applications in China has experienced explosive growth. In 2017, the Center for Drug Evaluation (CDE) accepted 42 new Class 1 antibody drugs (by product type). From January to October 2018, 42 new products had already been accepted, surpassing the 2017 figure and setting a new record. Since 2007, the number of companies engaged in antibody drug research and development has continued to grow, reaching 277 by the first half of 2017. Although many products are filed as Class 1 new drugs, similar products have already been marketed abroad, indicating that the proportion of truly innovative products remains low.

Monoclonal antibody R&D in China is still in its early stages. As of October 2018, only 10 antibody drugs had been approved for domestic companies. Except for Conbercept from Kanghong Pharmaceutical, the approved products lacked advanced technology, comprising four fusion proteins, four murine monoclonal antibodies, one chimeric monoclonal antibody, and one humanized monoclonal antibody.

The product targets submitted by domestic companies are highly concentrated, with dozens of enterprises filing applications for each of the six major hot targets: VEGF(R), TNF-α, PD-(L)1, CD20, EGFR, and HER2. As of October 2018, antibody drugs in the Biologics License Application (BLA) stage included anti-PD-(L)1 monoclonal antibodies from Hengrui Medicine, Junshi Biosciences, Innovent Biologics, and BeiGene; adalimumab biosimilars from Hisun Pharmaceutical and Bio-Thera Solutions; trastuzumab from 3SBio; a bevacizumab biosimilar from Qilu Pharmaceutical; and a rituximab biosimilar from Henlius Biotech.

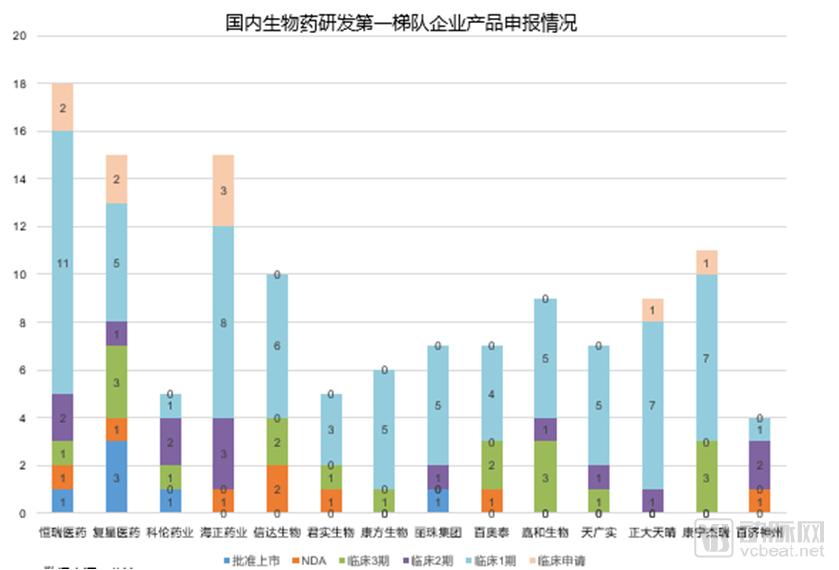

In China, companies represented by Hengrui Medicine, Qilu Pharmaceutical, Hisun Pharmaceutical, Genor Biopharma, and Bio-Thera Solutions have approximately 30 products in Phase III clinical trials. Among these, competition is particularly intense for VEGF monoclonal antibodies and TNF-α monoclonal antibodies, with 10 and 5 candidates respectively in Phase III trials. If these antibody drugs successfully enter the market within the next two to three years, the antibody drug market will face fierce competition.

Currently, a number of companies in China have emerged as prominent innovators in the field of biologics. In terms of the number of product candidates, the top three domestic companies with the most extensive pipelines are Hengrui Medicine, Fosun Pharma, and Hisun Pharmaceutical. Additionally, Innovent Biologics and Alphamab Oncology each have more than 10 products in their portfolios.

From the perspective of the R&D stages of biological drug products, most are still in the early stage of Phase I clinical trials. The companies with more products in Phase III clinical trials are Fosun Pharma, Genor Biopharma, and Alphamab Oncology.

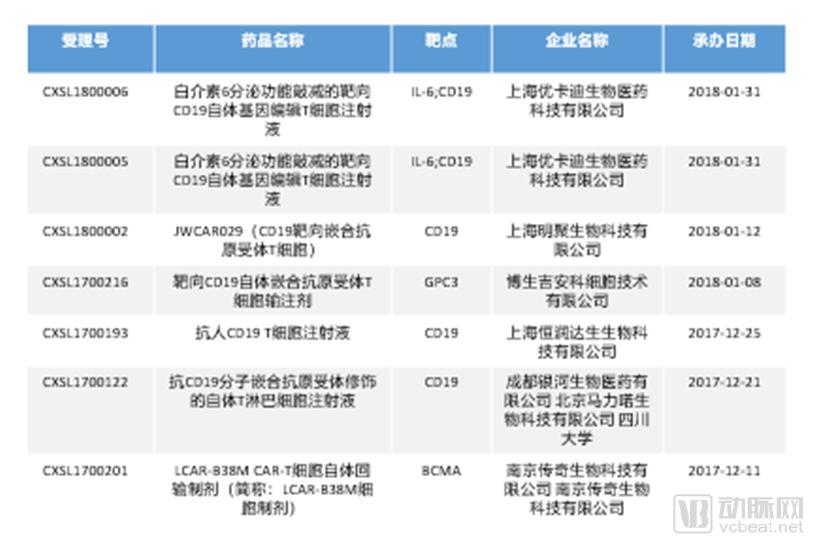

In 2017, after the U.S. FDA approved two CAR-T therapies for hematologic and lymphoid malignancies, CAR-T cell therapy garnered significant global attention. At the end of 2017, the China Food and Drug Administration (CFDA) issued the Technical Guidelines for Research and Evaluation of Cell Therapy Products (Trial), which provided clearer and more explicit acceptance criteria for clinical trial applications of CAR-T products. Drawing on many concepts from the FDA’s regulatory framework, these guidelines clarified the standards for domestic CAR-T products seeking approval as pharmaceuticals. By November 2018, the National Medical Products Administration (NMPA) had accepted 30 clinical trial applications for CAR-T products and 4 for TCR-T products.

In terms of the targets of accepted products, among the 30 CAR-T products, 23 target CD19 and 3 target BCMA.

In terms of the therapeutic areas of the accepted products, all are focused on oncology treatment, with a concentration on hematologic malignancies and limited involvement in solid tumors.

From the perspective of the location of the enterprises accepting the products, most are Shanghai-based companies, among which Shanghai U-CAR-T and Shanghai Hengrunda Biotechnology submitted 4 and 3 applications, respectively.

Although the domestic CAR-T industry is booming, its progress remains sluggish. Possible reasons include:

① Regulatory aspect: Previously, cell therapy was regulated by the National Health Commission as a medical technology; in recent years, it has been determined to be regulated by the National Medical Products Administration as a drug.

② Data submitted by the IND sponsor may have quality and management issues, resulting in unsatisfactory outcomes during regulatory inspections.

③ Experience in the industrialization of cell therapy still needs to be explored and accumulated; a cGMP-compliant cell therapy manufacturing facility is currently under construction.

④ There is a shortage of talent; there is a need to cultivate experienced professionals in areas such as process development and stringent CMC quality control. ⑤ Clinical practices may be non-standardized, particularly for paid treatments, and investigator-initiated studies also require further validation.

Stem cells hold promise for curing many diseases, including Alzheimer’s disease, cancer, diabetes, and arthritis. Since the end of 2017, when cell therapies were officially classified as drug applications, the National Medical Products Administration (NMPA) has accepted five stem cell product applications filed as Class 1 biological drugs.

Based on the five product indications accepted by the National Medical Products Administration (NMPA) in 2018, which include wound repair, arthritis, periodontitis, and graft-versus-host disease (GVHD), four of the applications were filed as Class 1 new drugs, while the Human Dental Pulp Mesenchymal Stem Cell Injection was filed as a Class 3 biological product.

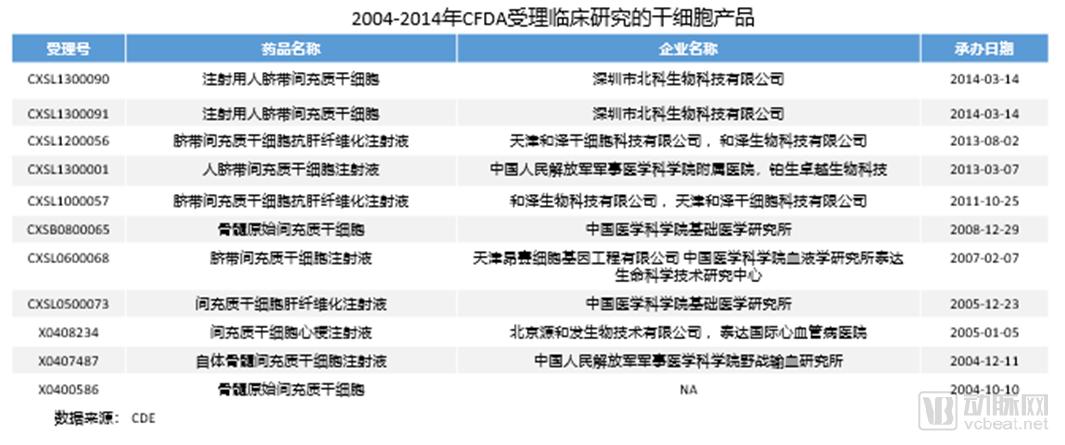

From 2004 to 2014, the national drug regulatory authorities accepted 11 applications for stem cell products, none of which have been approved to date. All were submitted as Class 3 biological drugs. In addition, there were 34 clinical trials filed with the National Health and Family Planning Commission.

In recent years, the total number of traditional Chinese medicine (TCM) registration applications and new drug applications has continued to decline. A significant drop occurred starting in 2015, particularly in manufacturing applications, which decreased from over 30 in 2011 to nearly zero in 2016–2017. The proportion of TCM new drug applications submitted as Investigational New Drug (IND) and New Drug Application (NDA) filings was 17.4%, while supplementary applications accounted for 71.1%.

Reasons for the Decline in Reported Volumes Include:

① The issuance of the State Council’s 2015 “Opinions on Reforming the Review and Approval System for Drugs and Medical Devices,” along with a series of policy documents concerning reforms to the drug review and approval system, tightened standards for registration acceptance and approval, and strengthened regulatory oversight and penalties.

② In July 2015, the China Food and Drug Administration (CFDA) issued a series of announcements requiring drug registration applicants to conduct self-inspections and verification of clinical trial data.

Between 2007 and 2010, a total of 14 Class 1 traditional Chinese medicine (TCM) products were submitted for clinical trial approval, while only two varieties received approval during the same period, reflecting increasingly stringent regulatory review for Class 1 TCMs. Starting in 2016, the number of Class 1 TCMs approved for clinical trials surged, with seven varieties approved in 2017 alone; meanwhile, the number of submissions for clinical trials dropped sharply to just one during the same period.

Based on the timeline for clinical trial approvals of Class 1 traditional Chinese medicine (TCM) products: An analysis of the approval durations (calculated as the difference between the status start date and the acceptance date) for the 12 approved products reveals an average timeframe of approximately 6.5 years. Products approved between 2007 and 2011 had relatively shorter approval times, averaging around 3 years, whereas those approved in recent years (2016–2017) experienced significantly longer approval periods, averaging approximately 10 years.

An analysis of R&D investment and sales performance for innovative traditional Chinese medicine (TCM) products approved in recent years reveals that the high difficulty of obtaining regulatory approval and modest return on investment are significant contributing factors. Data disclosed in the annual reports of listed companies for four products indicate that R&D expenditures for Class 5 and Class 6 TCM products amount to approximately RMB 60 million, with a prolonged development timeline requiring roughly ten years from clinical trials to market approval. However, their sales performance has been unsatisfactory.

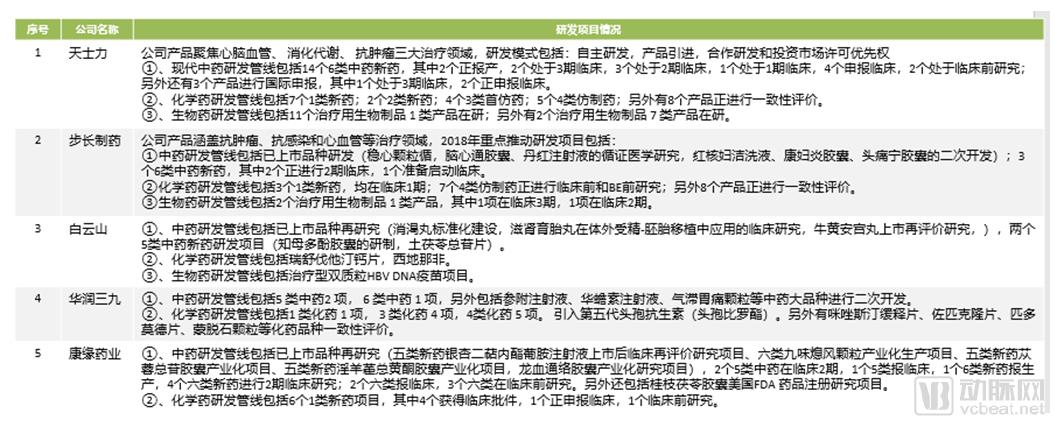

While innovation in traditional Chinese medicine (TCM) has been relatively sluggish, leading domestic TCM enterprises have made significant strategic investments in the research and development (R&D) of novel chemical drugs and biologics. Among the 70 listed companies specializing in traditional Chinese medicine, more than 10 have annual R&D expenditures exceeding RMB 200 million. Four of the top five companies—excluding Baiyunshan—have established R&D pipelines for Class 1 novel chemical drugs. Tasly and Kanion Pharmaceutical boast relatively robust TCM new drug R&D pipelines, whereas Buchang Pharmaceuticals, Baiyunshan, and China Resources Sanjiu primarily focus on post-marketing re-evaluation and secondary development within the TCM sector. Additionally, Tasly, Buchang Pharmaceuticals, and Baiyunshan have extensively expanded into biologic drug development.

Report Download Link: http://ofile.c-cmc.com:2222/admin/reportMaterial/downFiles.jhtml?id=4