Sword of Heroes in Troubled Times: A Navigation Guide for Healthcare Entrepreneurship in an Era of Fragmented Markets

In China’s investment community, Mr. Lu Gang, a partner at Legend Star, is renowned for his rigorous and comprehensive logic as well as his sharp, independent judgment. Due to his outstanding investment performance, Mr. Lu was named one of the “Top 10 Early-Stage Investors in China in 2018.” His investment philosophy enjoys widespread recognition and circulation within the venture capital (VC) circle.

2018On December 19, Mr. Lu Gang delivered a keynote speech at the “2018 Top 100 Future Healthcare Forum.” Breaking from his usual approach, he eschewed the investor’s perspective on capital and instead spoke from the standpoint of an entrepreneur. He openly shared his years of insights into the healthcare industry ecosystem and business logic, discussing how heroes emerge in turbulent times and offering guidance to entrepreneurs on survival and growth.

This article is compiled based on his insightful speech, originally titled “Cutting Through the Fog: Exploring the Underlying Simple Business Logic Behind Innovation Models.”

Highlights:

*What are many “Internet + Healthcare” initiatives actually doing? The “+” is merely adding tools, without integrating into the core essence of business. AI companies have turned into software companies. This reflects a flawed business logic.

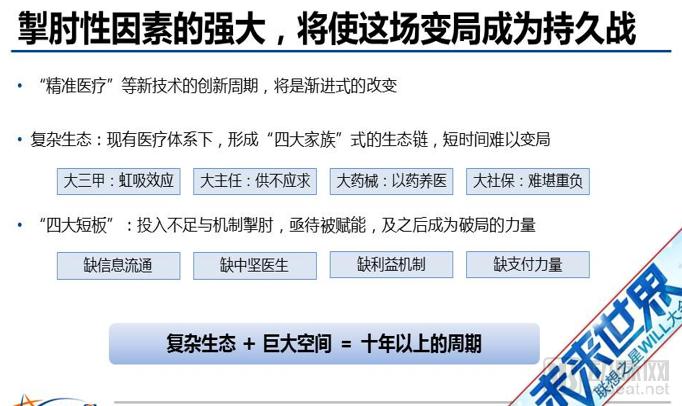

*The ecosystem of the new healthcare services industry is extremely complex, dominated by an ecological chain led by the “Big Four”: large tertiary Grade-A hospitals, influential department heads, major pharmaceutical and medical device manufacturers, and the national health insurance system. This structure is unlikely to change in the short term. Transforming the industry will inevitably be a protracted struggle; without the mindset for such a long-term effort, players may well fail along the way.

*The previous model of “funding healthcare through drug sales” will inevitably be dismantled, and efforts will be made to strengthen the four major shortcomings—a key initiative being pursued by the Communist Party of China. In the healthcare sector, which involves both commercial interests and social equity, how could one possibly deviate from the Party’s leadership?

*Since the model of subsidizing healthcare through pharmaceutical sales has proven unsustainable, the inevitable post-reform approach must be to sustain medical practice through service fees; otherwise, physicians will cease to work.

*The current issues in China’s healthcare system stem from the supply side, not the demand side. If supply-side problems remain unresolved, the root causes cannot be addressed. Therefore, certain mobile health models that focus on addressing demand-side issues—such as direct-to-consumer (2C) services, physician social platforms, and acquaintance-based doctor-patient models—may prove ineffective.

*In the healthcare services sector, fragmentation is a relatively long-term phenomenon, and market consolidation is unlikely. Moreover, given the substantial size of this market, there are abundant opportunities even without achieving dominant market share.

*We are currently in the first phase, known as the “Linkage and Empowerment” stage. However, this phase is drawing to a close, and we will soon enter the second phase, namely the “Transaction and Stickiness” stage, where the profit model will become clearly defined. Over the next five to ten years, a healthcare system sustained by service revenues is expected to take shape.

*The primary care sector represents an incremental market that requires capacity-building enhancements; those who can provide such empowerment will be poised for growth.

*Where is innovation heading in primary healthcare? The answer lies at the intersection of three key circles: grassroots care, payment models, and data. Innovations that do not fall within this intersection generally adhere to traditional models and practices, lacking significant disruptive potential.

*Different intersections exhibit varying potential for value explosion and practical monetization, thereby attracting different types of investors.

For startups, times of peace and prosperity offer few major opportunities, as industry giants hold a tight grip on the market. Chaos breeds heroes. In the healthcare sector, particularly in healthcare services, we are currently witnessing such a period of upheaval—a time for heroes to step forward.

Unfortunately, few startups in the healthcare sector achieve success. They either go astray in their business models, lack a clear understanding of the industry ecosystem, or adopt an inappropriate mindset...

Legend Star has cumulatively invested in more than 200 companies. We frequently engage in business discussions with various types of early-stage entrepreneurs, and here we share some of the insights we have accumulated.

In recent years, the healthcare industry has remained highly dynamic. 2014 was dubbed the “Year One of Internet + Healthcare,” 2015 became the “Year One of Physician Groups,” and 2016 marked the “Year One of AI + Healthcare.” All three “Year One” designations are closely related to healthcare services.

2017In recent years, the gene sector has been in the spotlight. In 2018, innovative biopharmaceuticals gained renewed momentum. The past two years have seen technology take center stage.

I have a question: Many “+” enterprises are often reported to have achieved significant accomplishments in recent years, but have they actually become profitable by now? I can state with certainty that they have made money—by taking investors’ money.

Some internet healthcare companies are valued at billions of dollars, but do you know what their revenues actually are? Amidst the hype surrounding medical AI, how many companies have generated revenues exceeding RMB 10 million? They are all struggling, surviving on investors’ money rather than genuine profits. This raises a core question: after years of integrating “+” into various sectors, why have we failed to address the critical pain points in the healthcare market? Why have we been unable to generate revenue across all segments of the industry?

I have a more moderate conclusion: the business logic is wrong, and the “+” is wrong!

Why is the business logic flawed? As we all know, what are many “Internet + Healthcare” companies doing today? They are opening offline clinics and hospitals, moving toward physical operations, in what is termed online-offline integration. Why integrate? It has become evident that online solutions alone cannot address the issues; they must also encompass the surrounding ecosystem. Ultimately, these companies find themselves becoming offline entities, reverting to traditional models.

“AI + Healthcare” was originally an asset-light sector. However, as companies flocked to develop solutions for pulmonary nodules, breast cancer, and fundus diseases in a herd-like manner, their detection rates eventually converged. Consequently, AI became merely software, and AI companies turned into software vendors. When hospitals procure software, they typically choose the lowest bidder. Can you still charge on a per-capita basis? In the end, hospitals either purchase your software outright or bundle it with hardware, causing AI companies to revert to traditional business models that cannot sustain the high valuations typical of AI firms.

Why is the business logic flawed? This endless addition of “+” merely piles on tools, without adding anything that touches upon the essence of business.

New medical services constitute one of the two key focus areas for Legend Star in the healthcare sector, with the other being the emerging technology segment centered on biotechnology and genetic engineering. At Legend Star’s WILL Conference in 2016, I discussed trends in medical services; these insights remain relevant today and warrant revisiting.

At the time, it was noted that entrepreneurship in new medical services might rapidly heat up. However, the ecosystem of this industry is extremely complex, and the supply chain dominated by the “four major families”—large tertiary Grade A hospitals, senior department directors, major pharmaceutical and medical device manufacturers, and the national basic medical insurance system—is unlikely to change in the short term. Although there are four major shortcomings, namely “lack of information flow, shortage of core physicians, absence of incentive mechanisms, and insufficient payment power,” these forces remain very weak.

This ecosystem dictates that industry transformation will inevitably be a protracted struggle. The future is bright, but the path is tortuous; without the mindset for a long haul, one may falter midway, as it is akin to running a marathon with the mentality of a sprinter.

Looking back at the past two years, many enterprises have poured substantial capital into the sector, yet progress has been arduous. Why have they failed to generate profits? This is directly attributable to the constraining factors mentioned above.

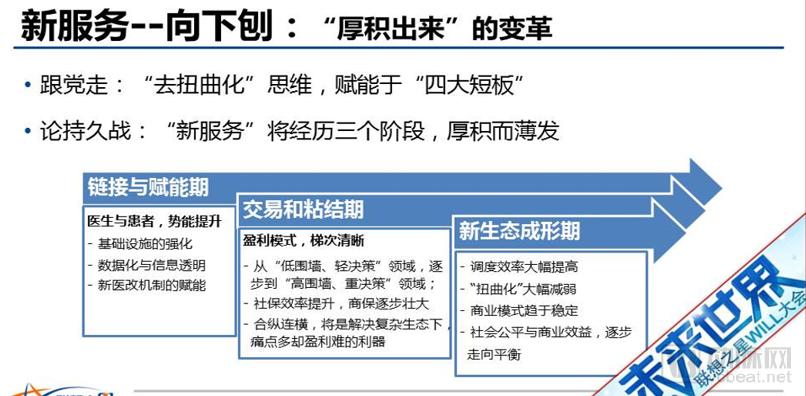

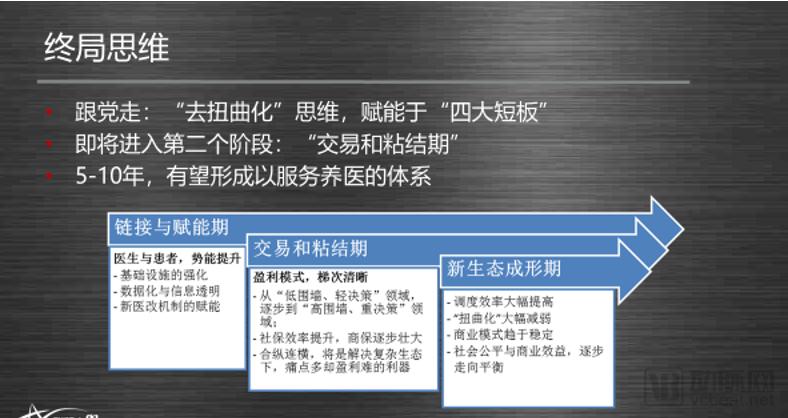

However, we must also recognize future trends: such changes are inevitable. First, distortion will be reduced; in particular, the previous model of “subsidizing healthcare through drug sales” will definitely be dismantled, and resources will be directed to strengthen the four key areas of weakness—a priority being pursued by the Communist Party of China. Therefore, aligning with the Party’s direction is the correct path. In an industry like healthcare, which involves both commercial interests and social equity, how could one possibly succeed without following the Party’s leadership? Moreover, the sector is subject to stringent regulation.

Second, it was proposed at the time that the transformation of this industry would undergo three stages. The first stage is called the “Linkage and Empowerment Phase,” the second stage is the “Transaction and Stickiness Phase,” and the third is the “New Ecosystem Formation Phase.” This progression is common to many industries undergoing change and is not unique to the healthcare services sector. Looking back now, which stage are we in today? We are still in the first stage.

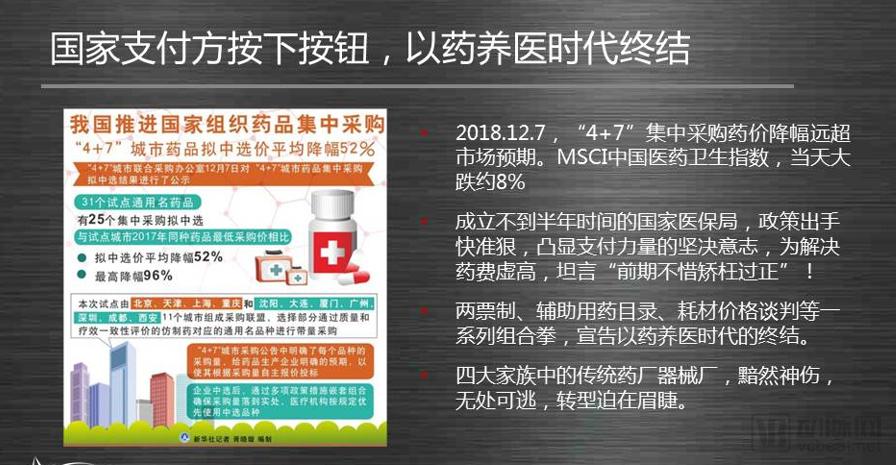

Everyone is aware of major recent developments such as the “4+7” centralized drug procurement program. Do you understand what this signifies? In May 2018, the National Healthcare Security Administration was established. What do its series of resolute and incisive reform measures imply? What does it mean to “spare no effort, even if it means overcorrecting”?

It signals a “sea change”: the era of subsidizing healthcare with drug profits is coming to an end. This is a positive transformation. The practice of relying on drug sales to fund medical services has led to widespread distortions, affecting not only drug prices but also the entire system of medical service fees. Those who fail to recognize this reality and continue to operate under outdated mindsets and rules are destined to be phased out.

“Distortion” is reflected in the fact that current healthcare issues in China stem from the supply side, not the demand side. If supply-side problems are not resolved, the root causes cannot be addressed. Therefore, certain mobile health models aimed at solving demand-side issues—such as B2C platforms, physician social networks, and acquaintance-based doctor-patient models—may prove unviable.

So, what will emerge after this impasse is broken? Since the model of subsidizing healthcare with drug profits has proven unviable, the system must inevitably shift to one where medical services sustain healthcare providers; otherwise, physicians would cease to practice. At this juncture, it is crucial to recognize that the institutional framework for service-based compensation has yet to be established. For instance, the commercial insurance system remains undeveloped, cost-containment measures within basic medical insurance are inadequate, and the private hospital ecosystem has not been fully formed. In short, none of these essential components are yet in place.

What does this mean? A time of upheaval. It is a favorable period of upheaval, offering abundant opportunities for innovation; it marks the rise of an era.

Many companies, in an effort to boost their valuations, frequently claim they aim to “dominate the entire market.” Let me be clear: forget about it. In the healthcare services sector, a fragmented landscape characterized by regional players is likely to persist for the long term, making nationwide consolidation highly unlikely. Moreover, the market is sufficiently large that you do not need to achieve total dominance to find abundant opportunities.

Entrepreneurs frequently consult us on whether to target the existing market or the incremental market. We believe that if an incremental market exists, it should be prioritized before competing for share in the existing market. Healthcare services represent an incremental market. Where should the cost savings from reduced drug expenditures be directed? These funds should be allocated to healthcare institutions and to companies that help these institutions improve operational efficiency and enhance physicians’ professional capabilities.

Second, why is the competitive landscape likened to the Spring and Autumn and Warring States periods? Consider that historical context: it involves complex multi-party gaming. In the “+Healthcare” sector, services possess regional attributes, leading to a fragmented market akin to feudal warlords vying for territory. A few days ago, I invested in a teleconsultation project that was engaging in department co-construction at the primary care level in East China. The founder expressed intentions to expand into Beijing, but I advised them to immediately refocus on East China; establishing a dominant position there would be highly advantageous. Only by clarifying this strategic direction can one achieve true focus.

As previously mentioned, we are currently in the first phase, known as the “Linkage and Empowerment Phase.” However, this phase is drawing to a close, and we will soon enter the second phase, the “Transaction and Stickiness Phase,” during which profit models will become clearly defined. In the first phase, with boundary conditions still unclear, it is premature to discuss profit models. In the second phase, some profit models will emerge quickly while others will take longer; most importantly, social insurance efficiency will improve, and commercial health insurance will gradually expand—both of which are critical factors. How long will this phase last? At least five to ten years, by which time a healthcare system sustained by service revenues is expected to take shape.

After understanding the ecosystem and trends, what strategic goals should entrepreneurs choose? What kind of business model? And at what pace should they achieve their business model? I have discussed these aspects extensively with investors, and I would like to share them with everyone.

First, stop using the “+” approach mentioned earlier and switch to a different “+” strategy. In this new approach, the primary focus should be on opportunities driven by essential needs.

Secondly, the healthcare service market is relatively complex and will inevitably undergo stratification, primarily into two tiers: the primary care level and the upper-tier level. The primary care segment represents an incremental market that requires empowerment-driven enhancement. As it remains relatively underdeveloped, those who can empower and strengthen this sector will gain a competitive advantage. In contrast, the upper-tier healthcare segment is a stock market with substantial opportunities. It necessitates structural adjustments, particularly in the relationship between commercial health insurance and basic medical insurance. For instance, determining where common diseases should be managed versus where complex and rare conditions should be treated constitutes such structural realignment, a trend that has already become irreversible. The stratification of the healthcare service market will continue to deepen, which is highly beneficial as it leads to clearer market positioning. Therefore, it is crucial to clearly identify whether your services target the primary care level or the upper-tier level.

Third is the issue of core drivers. Whether at the grassroots or upper levels, the core drivers consist of three parties: payers, providers, and enablers. Who are the payers? There are three: basic medical insurance, commercial insurance, and individual demand driven by consumption upgrades. Providers refer to physicians and medical institutions, while enablers encompass all stakeholders supporting their activities. Examining the core drivers in depth, they essentially comprise these three components.

We have a three-ring model for primary healthcare that we’d like to share with you. The three rings are primary care, payment, and data. In this model, where does innovation head? The answer is toward the intersection of all three rings. If it’s not within this triple intersection, it generally represents traditional models and businesses, which lack significant explosive potential. If it lies at the intersection of two rings, it may hold considerable energy—a point that should be clarified at the outset of any venture. And if it falls within the intersection of all three rings, then congratulations are even more in order.

In various intersections, there are differing levels of commercialization potential (forming a closed business loop and generating sufficient revenue) and value explosion potential (valuation). We conducted a quick statistical analysis and made some interesting findings.

Let us examine three of these intersections. The “Primary Care + Data” segment exhibits moderate monetization potential. The segment with the strongest practical monetization capability is “Payment + Primary Care,” as current policies favoring payment mechanisms in primary care are highly supportive, making it the most effective for revenue generation; however, it has the weakest explosive growth potential. Consequently, industry investors favor this sector due to its visible and predictable revenue streams.

As we can see, some AI companies fall within the intersection of “payment + data,” exhibiting high potential for value explosion but limited ability to achieve practical monetization. Consequently, many AI companies command high valuations and are favored by venture capital firms with TMT backgrounds. These AI companies also strive to secure funding as early as possible.

Venture capital firms specializing in healthcare tend to favor investments with strong growth potential, yet their approach is often relatively cautious due to the industry’s numerous entrenched challenges. This is an intriguing observation. Such a model can help us cut through the ambiguity and, from another perspective—namely, the dimension where startups and investors commit capital for commercial exploration—inspire us to reflect on the fundamental nature of business in this sector.

The entire industry remains in its first stage. Regardless of how individual companies perform or what their valuations are, I consider this merely a warm-up round; apart from investors’ capital, no real profits have been generated.

But now that the official competition has begun, we must have a clear and rhythmic understanding of it. Although some leading enterprises have certain advantages, they are far from forming dominance. Everyone should have firm confidence to engage in competition.

Some people ask, "What gaps remain for entrepreneurship in the healthcare and medical sector?" I believe that, in terms of broad categories or tracks, there are virtually none left. However, from the perspectives of technological and business model innovation, numerous market problems and pain points persist, presenting abundant opportunities for innovation.

Everyone has been talking about the “capital winter” lately. I have a saying: a capital winter does not necessarily mean a winter for entrepreneurship; it may still present good opportunities. For entrepreneurs in the healthcare services sector, this winter belongs to others, not to you.

Wishing everyone success and joy in your entrepreneurial ventures!