China's Healthcare Policy Turning Point: A 2018 Review of Pharmaceutical, Medical Services, and Insurance Reforms

In recent years, it seems that every year has been a significant year for pharmaceutical policies, with profound policies affecting the industry's development being introduced annually. Regulatory authorities have issued documents, and various regions have followed suit, leading to continuous interpretations and ongoing impacts.

Based on the different regulatory authorities, we categorize policies into three groups: pharmaceuticals, medical services, and medical insurance. The following is the table of contents:

Pharmaceutical Policy: Innovative Drugs Are Imperative, While Generic Drugs See a Return to Value;

Healthcare Services: Comprehensive Reforms Advance in Public Hospitals, While Private Healthcare Accelerates Its Pace;

Healthcare Insurance Policy: Increase Revenue and Reduce Expenditure, Carry Out Payment Method Reform to the End.

In recent years, pharmaceutical policies have followed two main threads. One is encouraging innovation, involving reforms in the review and approval system, the Marketing Authorization Holder (MAH) system, Contract Research Organizations (CROs), Contract Manufacturing Organizations (CMOs), and the inclusion of innovative drugs in national medical insurance negotiations. This approach provides incentives across the entire spectrum of innovative drug development, market access, and payment. The other thread focuses on consolidating existing resources, such as consistency evaluations, the new Good Manufacturing Practice (GMP) standards, the two-invoice system, control over the proportion of drug costs, and restrictions on antibiotic and auxiliary drug usage. These measures primarily affect generic drug manufacturers, aiming to restore the value of generic drugs.

Incentive policies for innovative drugs are not limited to domestic enterprises; foreign companies are treated equally, allowing multinational pharmaceutical firms to benefit from priority review and approval. First, the importation of new foreign drugs has been accelerated. For instance, on July 10, 2018, the National Medical Products Administration issued the Technical Guidelines for Accepting Overseas Clinical Trial Data for Drugs, which conditionally accepts overseas clinical trial data.

On August 8, 2018, for 48 new drugs urgently needed in clinical practice that had not yet been submitted for approval or were undergoing clinical trials in China, if the applicants determined through research that there were no ethnic differences, they could submit or supplement all overseas research data and supporting materials demonstrating the absence of ethnic differences, and directly file marketing applications. The China Food and Drug Administration (CFDA) would expedite the review and approval process under the priority review and approval procedure.

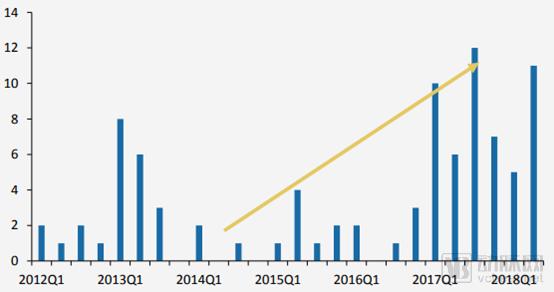

Under the “Green Channel” for Imported Innovative Drugs, the Number of Imported New Drugs Has Significantly Increased. According to a research report by GF Securities, the time lag between new drug approvals by the U.S. Food and Drug Administration (FDA) and the National Medical Products Administration (NMPA) has markedly shortened since 2000. Since 2012, a total of 91 imported new drugs have been approved for entry into the Chinese market; notably, the number of imported new drugs approved for the domestic market has increased substantially since 2017.

Imported New Drugs Approved by the NMPA Since 2012

Source: NMPA, GF Securities Development Research Center

Furthermore, national health insurance has strengthened its coverage of innovative drugs. Since 2016, three rounds of national health insurance negotiations have been completed: in May 2016, three drugs were included; in July 2017, the Ministry of Human Resources and Social Security added 36 drugs to Category B of the National Basic Medical Insurance, Work-Related Injury Insurance, and Maternity Insurance Drug List; in October 2018, the National Healthcare Security Administration incorporated 17 anti-cancer drugs into Category B of the same drug list. The inclusion of therapeutic products such as innovative drugs in health insurance is being accelerated, and a dynamic adjustment mechanism for incorporating innovative drugs into health insurance may be established in the future.

Many of the anticancer drugs newly included in the national medical insurance reimbursement list in October 2018 were recently launched in China within the previous two years. Moreover, the time lag between their initial overseas launch and domestic availability has been significantly shortened for many imported products. Their inclusion in the reimbursement list through price negotiations has greatly improved Chinese patients’ access to internationally first-line therapies for relevant diseases. Furthermore, the reimbursement prices established through these negotiations generally represented a reduction of more than 50% compared with the previous listed market prices, with some products seeing price cuts of up to 80%.

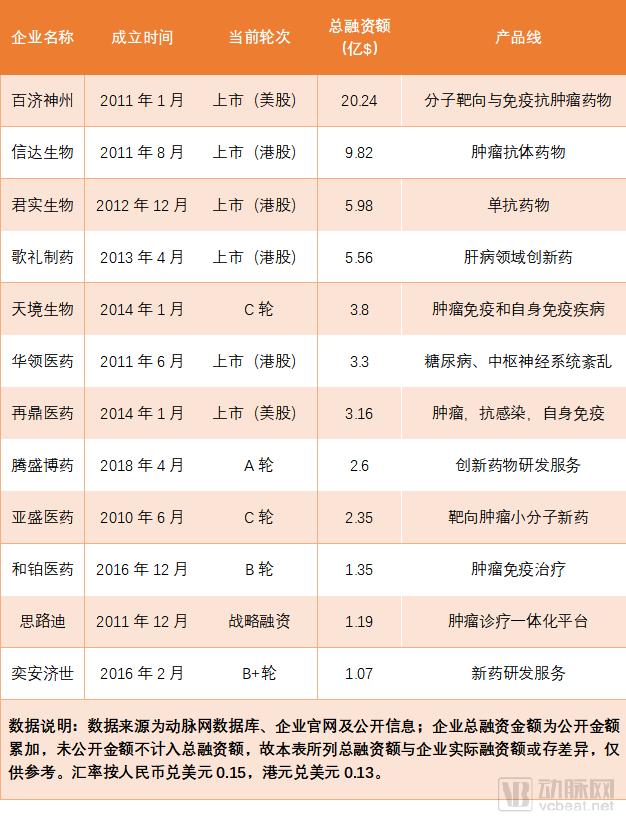

Domestic companies are also actively advancing their innovative drug portfolios, with capital support being a significant indicator. According to data compiled from the VCBeat database and public sources, there have been over 300 financing events in China’s new drug sector since 2014, involving a total amount of approximately RMB 32 billion, with an average single financing round nearing RMB 100 million. Emerging leaders in the innovative drug field include BeiGene, Innovent Biologics, Junshi Biosciences, and Ascletis Pharma.

Statistics on Financing for Innovative Enterprises in the Pharmaceutical and Biotechnology Sector (Partial)

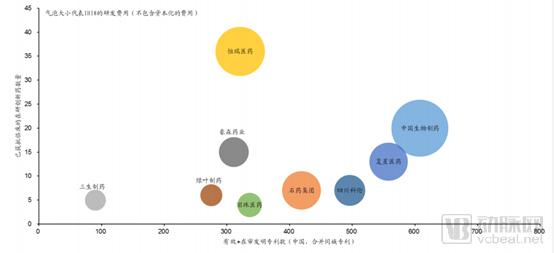

Established pharmaceutical giants such as Hengrui Medicine, CSPC Pharmaceutical Group, and Kanghong Pharmaceutical have already developed mature pathways for innovative drug development. By continuously increasing investment in their R&D pipelines and improving R&D efficiency, they have secured high-quality pipelines under development. Furthermore, they are actively expanding into overseas markets and leveraging license-in/out strategies to strengthen their innovative drug portfolios.

Despite the aggressive emergence of innovative drugs, drug development is characterized by long cycles and substantial investment, resulting in a limited number of currently approved products. Taking PD-1 inhibitors as an example, only those from Junshi Biosciences and Innovent Biologics have received approval. Therefore, the “fundamentals” of generic drugs in China’s pharmaceutical market remain solid. According to IMS data, in 2017, branded generics accounted for 20% (RMB 181.4 billion) and ordinary generics accounted for 58% (RMB 526 billion) of the hospital market, collectively representing approximately 78% of the hospital pharmaceutical market.

Comparison of R&D Capabilities Among Pharmaceutical Companies

Data sources: PDB, company materials, GF Securities Development Research Center

The greatest challenge currently facing generic drugs stems from volume-based procurement. On December 6, 2018, the proposed winning bid results for the centralized drug procurement in the “4+7” cities were announced. Among the 31 products subject to volume-based procurement, 25 secured winning bids, while 6 were abandoned. The winning bid prices saw declines exceeding prior market expectations (which had anticipated price reductions of 30%–40%). Specifically, 10 products experienced price cuts of over 70%, 8 saw reductions between 40% and 70%, and only 7 had price decreases of less than 40%.

The original intent behind the design of the volume-based procurement (VBP) policy is to exchange price for volume, leveraging generic drugs that have passed the consistency evaluation to replace originator drugs, while simultaneously reducing artificially inflated generic drug prices and saving medical insurance funds. In the future, the VBP policy may be rolled out nationwide. Beyond the policy level, pharmaceutical companies such as Yangtze River Pharmaceutical Group and Hengrui Medicine have proactively aligned their procurement prices in regions not yet implementing VBP with the centralized procurement prices, serving both as a model and as an indicator of future trends.

Volume-based procurement will also impact distribution enterprises. Taking Shanghai’s supplementary documents as an example, they require that each winning bid product be distributed by only one designated pharmaceutical distribution enterprise, with a distribution fee rate set at 6% of the winning bid price. The designated distribution enterprise must have had its pharmaceutical distribution coverage spanning all districts of the city in 2017 and possess the capability and conditions to deliver winning bid products to all medical institutions designated for medical insurance across the city within 24 hours. Distribution enterprises are prohibited from purchasing winning bid products through third parties. These requirements favor leading circulation enterprises with comprehensive distribution networks. Conversely, some smaller distribution enterprises will lose market share, accelerating mergers, acquisitions, and consolidation within the distribution sector.

With the advancement of consistency evaluations and the launch of volume-based procurement, the review and approval process for new drugs has accelerated, shaping a pharmaceutical market that places equal emphasis on innovative drugs and high-quality generics. Innovative drugs are entering the market more rapidly and receiving support from medical insurance schemes. Price reductions for off-patent drugs are inevitable, allowing the competitive advantages of domestic enterprises to gradually emerge. As first-to-file generics become a strategic target for companies, the era of cutthroat competition in the generic drug sector is unsustainable, and market share will quickly consolidate among a select few high-quality enterprises.

2018 Review of Pharmaceutical Policies

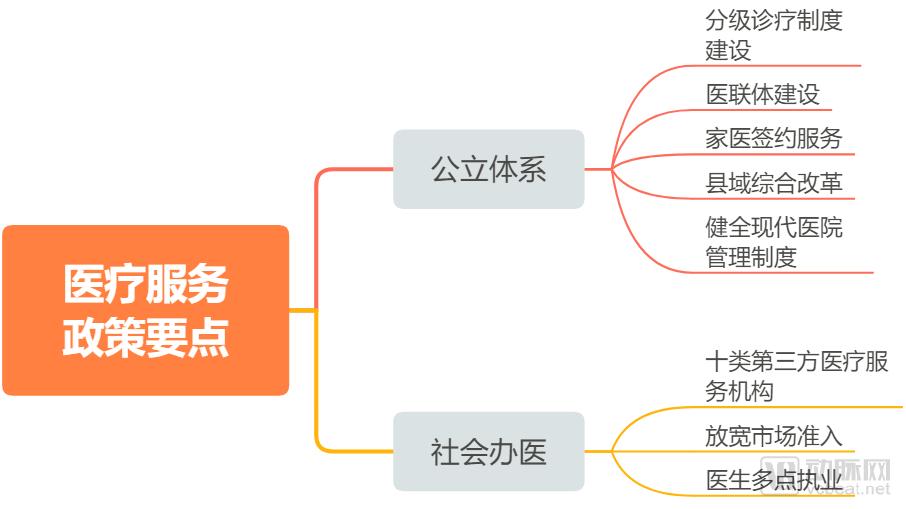

The healthcare services sector continues to adhere to two main thrusts: comprehensive reform of the public healthcare system and encouraging private capital to enter the healthcare services sector.

First and foremost, there have been changes in regulatory functions. In March 2018, the institutional reform plan was announced, establishing the National Health Commission (NHC). Its responsibilities include formulating national health policies, coordinating and advancing the deepening of healthcare system reforms, organizing the development of the national essential medicines system, supervising and managing public health, medical services, and health emergency response, overseeing family planning management and services, and formulating policy measures to address population aging and integrate medical care with elderly care. While the NHC’s functions were slightly adjusted from those of its predecessor, the National Health and Family Planning Commission (NHFPC), it largely continued the previous mandates, thereby maintaining continuity in policy direction.

“Healthcare reform” is a long-term process that is always ongoing, with no definitive endpoint. The comprehensive reform of the public healthcare system constitutes the core task of “healthcare reform,” with its primary logic centered on establishing a tiered diagnosis and treatment system to achieve “initial consultations at the primary care level, two-way referrals, coordination between different levels of care, and separate management of acute and chronic conditions,” thereby addressing the inverted triangle structure in healthcare delivery. Tiered diagnosis and treatment, supplemented by family doctor contracting, medical consortia, and comprehensive county-level reforms, ultimately aims to realize an orderly and stratified healthcare system.

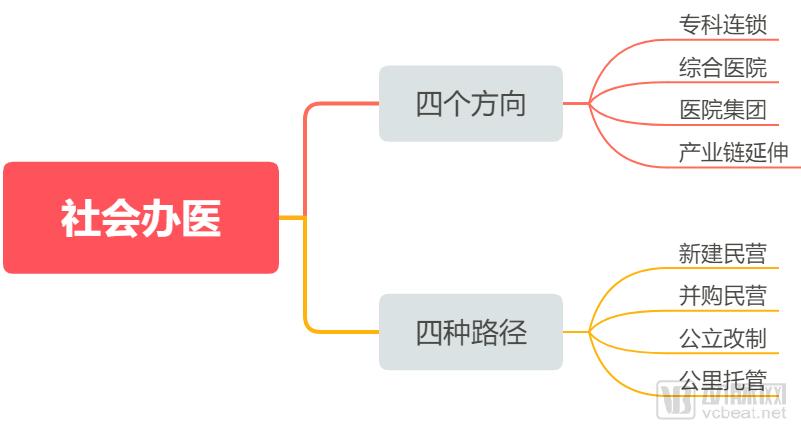

Promoting the development of private healthcare can be interpreted through three key points: First, demand-driven growth, as residents’ healthcare needs are increasing day by day, and the existing medical service system can no longer meet these demands. Second, rigid and insufficient supply from public medical institutions; with rising patient demand, the public healthcare system, as the primary provider of medical services, is overwhelmed, necessitating the introduction of social capital in healthcare to “divert” some of the demand. Third, industrial development needs; policies often lag behind reality. The principle of “entry allowed unless explicitly prohibited” has led to the proliferation of third-party medical institutions, particularly third-party laboratories and imaging centers, fostering the emergence of multiple listed companies and industry leaders. Policies merely clarify standards further, guiding the industry toward healthy and robust competition.

Overview of Medical Service Policies in 2018

However, the most prominent policies in the healthcare services sector this year are the three policy documents related to “Internet-based Diagnosis and Treatment.” These mark the first time that national-level regulatory authorities have issued detailed regulatory guidelines for the “Internet + Healthcare” industry, particularly for Internet hospitals, which have finally seen a policy breakthrough after years of exploration.

Key provisions include classifying “Internet + Healthcare Services” into three categories based on the personnel involved and service delivery models: telemedicine, online diagnosis and treatment activities, and internet hospitals; clarifying the nature of internet hospitals and their relationship with physical medical institutions; specifying the access procedures and regulatory oversight for internet hospitals and online diagnosis and treatment activities; and defining the legal liability frameworks for internet hospitals. These measures effectively establish a national standard for the industry. In the future, internet hospitals will become a standard component and foundational infrastructure of healthcare services, truly realizing the goal of “letting data do more running so that patients have to run less.”

According to statistics compiled by VCBeat Eggshell Research Institute from publicly available information, the number of internet hospitals in operation across China had expanded to 119 as of November 2018, representing a fourfold increase over two years. Benefiting from favorable policies, internet hospitals are experiencing a third wave of development, with enterprises bearing the name “internet hospital” growing rapidly at a rate of two per week. The first half of 2019 will see concentrated construction of provincial-level regulatory platforms, while the second half will witness a surge in the establishment of internet hospitals by public hospitals.

The entities responsible for the construction and operation of internet hospitals are predominantly funded by private capital, which to some extent reflects the enthusiasm of private investors entering the healthcare services sector. In broader areas—such as specialized clinic chains, general hospitals, and hospital groups—private capital is also well represented, including Aier Eye Hospital (ophthalmology), Topchoice Medical (dentistry), and Meinian Onehealth (health checkups). More capital is flowing into the healthcare services sector: Yihua Health, Changbao Shares, Fosun Pharma, Kangmei Pharmaceutical, and others.

Four Major Directions and Four Pathways for Private Healthcare

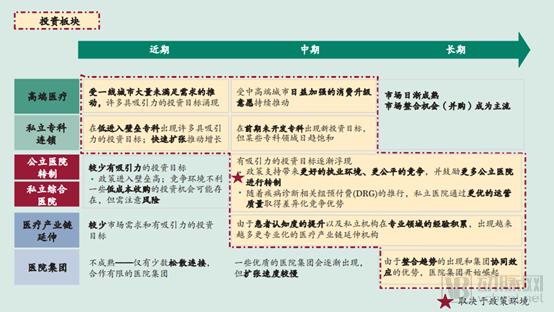

Boston Consulting Group believes that investment opportunities in China’s healthcare services sector are unfolding sequentially: in the near term, high-end medical care and private specialty hospital chains will lead the first wave of investment; in the medium term, these segments will expand geographically and across specialties, while general hospitals (including private general hospitals and public general hospitals undergoing restructuring) will become a key focus, with gradual emergence of extensions along the healthcare industry chain; in the long term, general hospitals will further develop, potentially evolving into hospital groups, and industry consolidation through mergers and acquisitions will begin to emerge.

Evolutionary Pathways of the Private Healthcare Sector

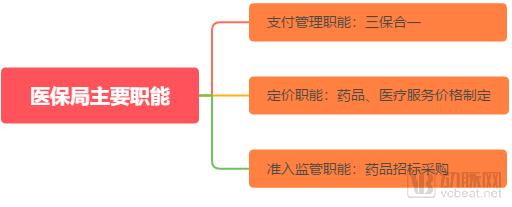

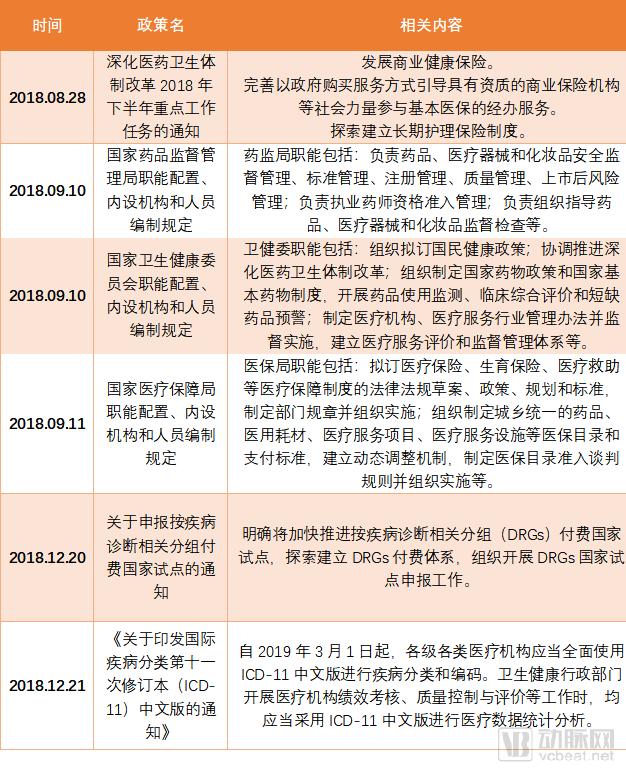

The most significant change in medical insurance this year is the establishment of the National Healthcare Security Administration (NHSA). Its primary functions include payment management—overseeing basic medical insurance for urban employees and residents, maternity insurance, and the New Rural Cooperative Medical Scheme; pricing—setting prices for pharmaceuticals and medical services; and market access regulation—managing drug tendering and procurement. The NHSA has ended the previous “tripartite governance” of medical insurance fund management, emerging as the most powerful payer in the healthcare industry, thereby ushering in a new era of medical insurance cost containment.

Following the period of dividends from universal health insurance coverage, the medical insurance fund will face long-term pressure due to an aging population and a gradual slowdown in revenue growth. Under the principle of "expenditure determined by revenue," limited funds will increasingly prioritize essential medications for basic public healthcare needs and innovative drugs with clear clinical value. Meanwhile, healthcare-side reforms—such as the elimination of drug markups and controls on the proportion of drug costs—are continuously advancing, intensifying downward pressure on drug prices. Whether through price reductions for negotiated drugs entering the national reimbursement list or significant price cuts for generic drugs under volume-based procurement, drug prices will face further pressure in the context of cost containment within the medical insurance system.

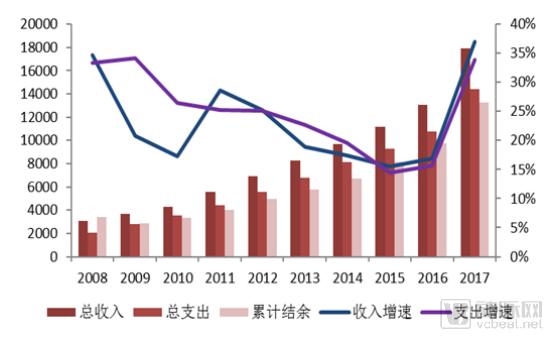

Surplus of Urban Basic Medical Insurance Fund Revenues and Expenditures, 2008–2017 (in billion yuan)

Source: Ministry of Human Resources and Social Security, Wanlian Securities Research Institute

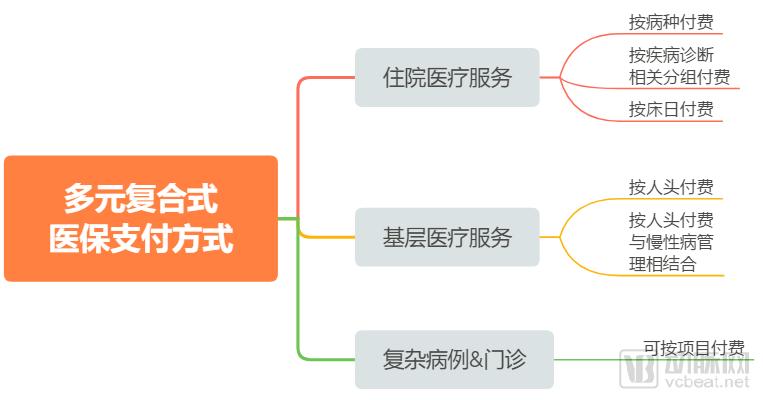

In terms of healthcare payment method reform, Diagnosis-Related Groups (DRGs) have recently become a focal point. DRG-based payment is an advanced healthcare reimbursement model already adopted by countries such as the United States, Australia, Germany, and France. This approach comprehensively analyzes patients’ clinical conditions to assign them to specific diagnostic groups for bundled treatment, thereby standardizing care pathways and ensuring controllable treatment costs.

From a historical perspective, starting in 2017, the National Health Commission launched pilot programs for DRG-based payment and charging reforms in Sanming City (Fujian Province), Shenzhen City (Guangdong Province), Karamay City (Xinjiang Uygur Autonomous Region), and three medical institutions in Fujian Province. In January 2018, Sanming City, Fujian Province, officially launched and began operating its DRG payment and charging system.

On December 20, 2018, the National Healthcare Security Administration issued the “Notice on Declaring National Pilot Programs for Diagnosis-Related Groups (DRG)-Based Payment,” deciding to organize and carry out the application process for national DRG pilot programs. The objective is to formulate and improve nationally basic unified policies, procedures, and technical standards for DRG-based payment, thereby creating pilot outcomes that are referenceable, replicable, and scalable. In terms of pilot scope, each province may, in principle, recommend one or two cities (with municipalities directly under the central government participating as a whole) as candidate cities for the national pilots.

On December 21, 2018, the National Health Commission issued the "Notice on Printing and Distributing the Chinese Version of the International Classification of Diseases, 11th Revision (ICD-11)," stipulating that as of March 1, 2019, medical institutions at all levels and of all types shall fully adopt the Chinese version of ICD-11 for disease classification and coding. When health administrative departments conduct performance assessments, quality control, and evaluations of medical institutions, they shall use the Chinese version of ICD-11 for statistical analysis of medical data.

Diversified Composite Health Insurance Payment Methods

Chuancai Securities’ research report suggests that the implementation of DRG-based payment has significantly curbed the growth rate of per capita medical expenditures, benefiting healthcare service providers with high operational efficiency. DRG-based payment helps avoid issues such as overprescribing and overtreatment associated with fee-for-service models, thereby effectively controlling the rise in treatment costs. In the United States, the growth rate of per capita medical expenditures was significantly restrained following the adoption of DRGs.

Meanwhile, the DRG-based reform of public hospitals is not merely about cost containment; rather, it prioritizes enhancing the operational efficiency of public hospitals. Instead of indiscriminately cutting hospital funding, the reform takes into account the interests of multiple stakeholders, including payers and patients. This approach facilitates further standardized operations for high-performing, high-efficiency hospitals, while exerting certain pressure on low-performing institutions to stimulate their development and improve efficiency.

A research report by Essence Securities pointed out that in cities with a solid foundation of medical informatization and advanced hospital medical concepts, such as Shanghai, DRGs have been gradually implemented in small batches at the hospital level since 2018. In the future, with the national health insurance payment reform and the rising demand for quantitative healthcare within hospitals themselves, DRGs will become increasingly widespread. According to grassroots survey data, it is estimated that the market size for DRGs on both the hospital side and the health insurance side ranges from 2.4 billion to 8.5 billion yuan, indicating significant potential.

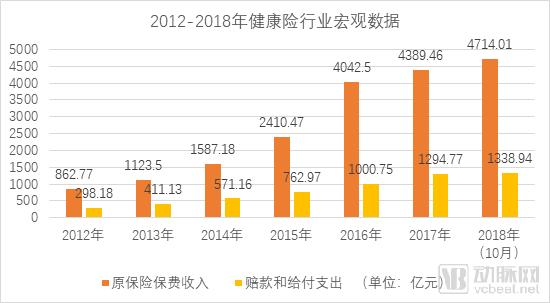

Cost containment in basic medical insurance represents “expenditure reduction,” while the expansion of commercial health insurance serves as “revenue generation.” According to data from the China Banking and Insurance Regulatory Commission (CBIRC), the compound annual growth rate (CAGR) of original premium income in the health insurance market reached 40.6% from 2013 to 2017, significantly higher than the overall insurance market’s average growth rate of 20.7%. In terms of health insurance density and penetration, the density stood at RMB 316 per capita, and the penetration rate was 0.53% in 2017. With rising household incomes, heightened insurance awareness, and innovations in insurance products and distribution channels, substantial growth potential remains. Based on these trends, it is projected that original premium income for health insurance will reach RMB 1.3 trillion by 2020.

Data source: CBIRC

From the perspective of health insurance subcategories, critical illness insurance and medical insurance took the lead. In 2017, the original premium income for critical illness insurance reached RMB 249.4 billion, accounting for 56.8% of the total, while that for medical insurance was RMB 141.5 billion, representing 32.3%. The original premium income for long-term care insurance stood at RMB 47.5 billion, whereas disability income insurance generated only RMB 50 million. Growth rates varied significantly across these categories: critical illness insurance saw the fastest growth at 46.9%, medical insurance increased by 25.0% year-on-year, and long-term care insurance experienced a decline of approximately 60%.

This year, the health insurance sector saw both strengthened regulation and favorable policies: In April, the China Banking and Insurance Regulatory Commission (CBIRC) released the “Negative List for the Development and Design of Life Insurance Products,” intensifying regulatory oversight over short-term medical insurance products such as “Million Medical Coverage”; in October, draft regulatory measures for internet insurance were issued for industry consultation, facilitating smaller health insurers to conduct business nationwide via online platforms.

Medical Insurance Related Policies

In addition to the policies mentioned above, there has been continuous policy follow-up in pharmaceutical distribution, medical devices, and innovative medical products. Healthcare is an industry critical to national welfare and people’s livelihoods, characterized by stringent regulation. Policy serves as a bellwether for industry development and can drive or precipitate sector-wide adjustments.

In the pharmaceutical distribution sector, chain pharmacies warrant close attention. Driven by the trend of "prescription outflow," substantial capital has flowed into the chain pharmacy industry, with investors such as Hillhouse Capital, CDH Investments, and GF Xinde joining the fray. Internet healthcare companies like Alibaba Health and Ping An Good Doctor are also entering the competitive landscape through investments and empowerment initiatives.

The most significant change in the pharmaceutical distribution and retail sectors this year stems from the tiered management system for pharmacies. Under this system, retail pharmacies are classified into three categories based on operational conditions and compliance status: Class I pharmacies are permitted to sell Category B over-the-counter (OTC) drugs; Class II pharmacies may sell OTC drugs, prescription drugs (excluding prohibited and restricted medications), and traditional Chinese medicine (TCM) decoction pieces; Class III pharmacies are authorized to sell OTC drugs, prescription drugs (excluding prohibited medications), and TCM decoction pieces. As a result, industry consolidation among retail pharmacies is expected to accelerate, benefiting large-scale enterprises.

Secondly, the outflow of prescriptions is gradually materializing, with the prescription-sharing platform model emerging as the mainstream approach in regional pilots, supported by cities such as Xi’an, Chengdu, and Chongqing. The source of prescriptions, drug supply assurance capabilities, and pharmaceutical care service capabilities are the most critical factors driving prescription outflow. Some pharmacies are transitioning toward specialized models, with Direct-to-Patient (DTP) and pan-DTP models becoming the primary formats in pharmaceutical retail for accommodating prescription outflow. However, this sector is predominantly occupied by established players with substantial resources and mature operational models, making it challenging for new entrants from outside the industry to gain a competitive advantage.

In the realm of innovative medical products, medical artificial intelligence (AI) has garnered the most attention. After nearly three years of development, a cohort of leading enterprises has emerged, with relatively mature products. The primary tasks ahead are obtaining regulatory approval and achieving commercial implementation. Regulatory authorities have been actively following suit; on December 25, a public-interest training session on the registration and application of AI-based medical devices was held in Beijing, focusing on key points for product registration submissions.

Based on meeting minutes, VCBeat has compiled the key points for the application and approval of medical AI products. (See: “AI Milestone! NMPA Class III AI Medical Device Application Process Leaked! Comprehensive Interpretation of Approval Key Points!”) Industry insiders stated that due to the numerous approval requirements, some provisions may be relatively stringent for many current artificial intelligence companies. These enterprises are still preparing relevant materials. According to several leading AI companies, the current application process is characterized by intricate details and high standards. They are submitting documentation for filing and approval; however, due to the lack of precedents, they are unable to make further judgments regarding subsequent outcomes.

The medical artificial intelligence (AI) industry is an emerging sector in China, with registration standards and approval processes still under exploration. Collaborative efforts between enterprises and regulatory authorities are required to gradually refine the relevant rules. In this regard, the practices of the U.S. Food and Drug Administration (FDA) may offer valuable lessons. Among the 121 digital health products approved by the FDA over the past three years, approximately 10 were AI-based, demonstrating a significant effect of policy innovation. Key approaches include implementing the “Digital Health Innovation Action Plan” for innovative medical devices, establishing a dedicated review division for medical AI and digital health, and accelerating the approval of medical AI products by lowering entry barriers.

Regulation and favorable policies go hand in hand, while innovation and integration advance together. In this era of significant policy shifts, the industry stands at a crossroads on its new journey.