Three Major Trends Shaping Biopharma Licensing Deals in 2025: China's Rise, Multispecific Antibodies, and AI-Driven Drug Discovery

GSK China

Pharmaceutical Manufacturer

GSK

Pharmaceutical R&D Manufacturer

AstraZeneca

Pharmaceutical Technology Research and Development Provider

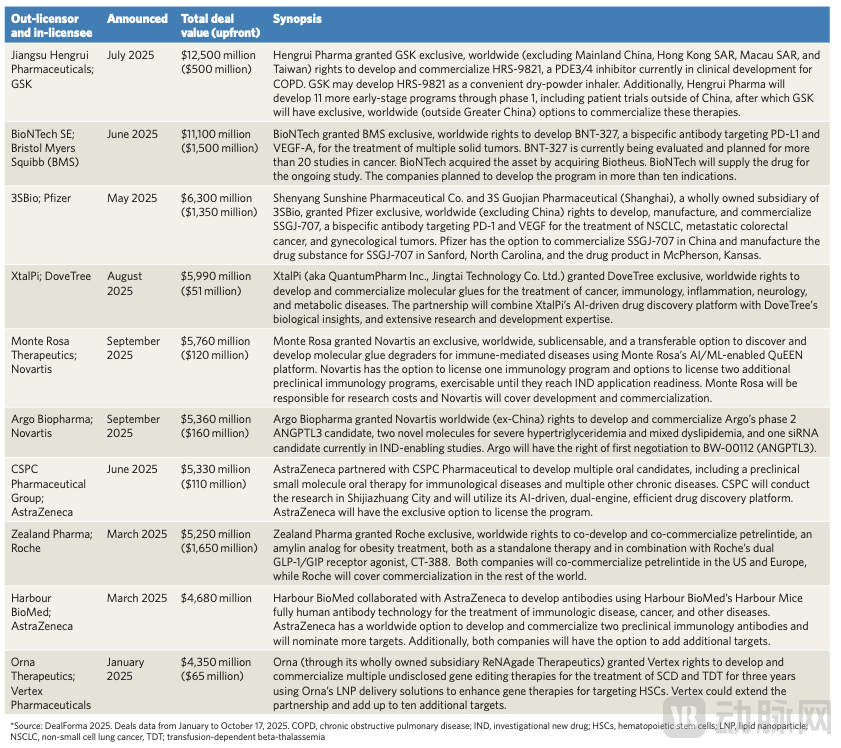

From January to October 2025, the top ten R&D licensing collaboration deals in the global biopharmaceutical field demonstrated three significant trends.

According to an analysis report published by Nature in December 2025, Chinese companies participated in five of these deals, which have a total value exceeding 70 billion US dollars, becoming an important source of early-stage assets.; The number of bispecific and multispecific antibody deals reached 24, showing a significant increase from previous years; collaborations driven by artificial intelligence in drug discovery accounted for 23% of all such deals this year. The largest deal was between GSK and Jiangsu Hengrui Medicine Co., Ltd. of China, with a total value of up to 12.5 billion US dollars.

Figure: Top 10 biopharmaceutical R&D licensing collaboration projects by total disclosed deal value in 2025 (Source: Nature)

These trends not only reflect the profound transformation of the global biopharmaceutical industry chain but also foreshadow a new landscape for future drug development.

Biopharmaceutical Licensing Deals refer to one company granting another company the rights to develop and commercialize its drug candidate molecules or technology platforms. Typically, large pharmaceutical companies pay upfront fees and milestone payments to biotech firms. These deals are a core mechanism of the global pharmaceutical innovation ecosystem, providing financial support to innovative biotech companies while helping large pharmaceutical companies rapidly expand their product pipelines.

The data from 2025 reveals a prominent phenomenon:Five of the top ten deals involved Chinese companies.Chris Dokomajilar, founder and CEO of DealForma, pointed out that there has been a significant increase in deals between large multinational pharmaceutical companies and Chinese biopharmaceutical companies in 2025. Among all large pharmaceutical licensing-in deals with upfront payments of at least $50 million, 38% came from China, accounting for 30% of the global total of licensing upfront payments. This rising proportion marks China's transformation from a technology follower to a key contributor to global innovation.

A representative case of this trend is the agreement reached between GSK and Jiangsu Hengrui Medicine in July 2025. According to the agreement, GSK paid an upfront payment of $500 million to obtain the global (excluding mainland China, Hong Kong, Macao, and Taiwan) exclusive license for Hengrui Medicine's phosphodiesterase (PDE) 3/4 inhibitor, HRS-9821, which is currently in clinical development for chronic obstructive pulmonary disease (COPD). In addition, the agreement also covers another 11 early-stage candidate drugs across respiratory, immunology/inflammation, and oncology fields. Hengrui Medicine will lead Phase I clinical trials for these projects, after which GSK can opt to acquire global commercialization rights. The total potential milestone payments could reach approximately $12 billion, making this deal the highest-value licensing agreement of 2025.

AstraZeneca's layout in China is particularly active.The company occupies two seats in the top ten transactions,Including partnerships with Harbour BioMed and CSPC Pharmaceutical Group. In March 2025, AstraZeneca committed to paying up to $4.68 billion to Harbour BioMed for the global development and commercialization rights of next-generation multispecific antibodies based on Harbour Mice technology. AstraZeneca will also establish a collaborative innovation center within Harbour BioMed and make an equity investment. These moves reflect multinational pharmaceutical giants deeply integrating China's innovative resources, shifting from pure market expansion to strategic cooperation at the technological source.

Dokomajilar emphasized that the appeal of Chinese biopharmaceutical companies in licensing deals mainly comes from their "rapid clinical development capabilities for potentially large-market biologics." Chinese enterprises not only demonstrate advantages in R&D speed but also show increasing strengths in cost control and adaptability to the global regulatory environment, making them one of the preferred partners for global pharmaceutical giants seeking innovative assets.

Bispecific and Multispecific Antibodies(Bispecific and Multispecific Antibodies) are a class of engineered antibodies that can simultaneously target two or more different antigens or epitopes. Compared with traditional monoclonal antibodies, these antibodies can achieve more complex therapeutic mechanisms, such as simultaneously blocking two signaling pathways or guiding immune cells to tumor sites. In the field of cancer treatment, this technology is becoming a key investment focus in the industry.

In the first ten months of 2025, there were 24 licensing and R&D cooperation deals related to bispecific and multispecific antibodies, continuing the high trend set by the record 33 deals in 2024. Three of the top ten deals specifically involved such antibodies, two of which were related to Chinese companies. The most focused combination of targets isProgrammed Cell Death Protein 1 (PD-1) or Programmed Cell Death Ligand 1 (PD-L1) and Vascular Endothelial Growth Factor (VEGF).Dokomajilar pointed out that the total upfront payments for bispecific antibodies targeting the PD-1/VEGF combination in tumor treatment exceeded $2.8 billion in 2025, with a total deal value of $17.4 billion.

The deal reached between Pfizer and 3SBio in May 2025 is a typical case in this field. Pfizer paid $1.25 billion upfront and $100 million in equity investment to obtain global exclusive rights outside of China for 3SBio’s bispecific antibody SSGJ-707, which targets PD-1 and VEGF and is about to enter Phase 3 clinical trials for the treatment of non-small cell lung cancer, metastatic colorectal cancer, and gynecological tumors. Potential milestone payments could reach $4.8 billion, bringing the total value of the deal to $6.3 billion. Similarly, the agreement signed between Bristol Myers Squibb and BioNTech in June 2025 is even more valuable — totaling $11.1 billion — focusing on BioNTech's next-generation bispecific antibody BNT-327, which targets PD-L1 and VEGF-A for the treatment of refractory solid tumors. These massive investments reflect the strong confidence of large pharmaceutical companies in multimodal oncology treatment mechanisms.

AI-Driven Drug Discovery(AI-driven Drug Discovery) is becoming another rapidly growing field. Since 2017, there have been a total of 513 such deals globally, with 120 occurring in the first ten months of 2025 alone, accounting for 23%. The core of these deals lies in utilizing AI algorithms to accelerate target identification, molecular design, and preclinical optimization, thereby reducing the time and cost of traditional drug development, especially for traditionally difficult-to-drug targets (Undruggable Targets).

XtalPi and DoveTree Medicines' Collaboration in August 2025 Showcases AI Platform’s Multimodal Capabilities

Notably, although the total value of AI-related deals as a proportion of all licensed deals has increased from 18% in 2024 to 27% in 2025,The proportion of upfront payments in AI deals is only 3% of the total value, significantly lower than the 10% in biologics deals or 6% in small molecule deals.Dokomajilar analyzed that although large pharmaceutical companies have recognized the downstream potential value of AI, they remain cautious about these latest discovery platforms. This "high expectations, low upfront investment" model reflects the industry's prudent assessment of the maturity of AI technology and its clinical translation capabilities.

Three Major Trends in Biopharmaceutical Licensing Deals in 2025 Mark a Profound Restructuring of the Global Innovation EcosystemThe Rise of Chinese EnterprisesNot only has it changed the geographical distribution of innovative assets, but it has also driven the global pharmaceutical industry towards a more diversified and distributed collaboration model. The advantages of Chinese companies in clinical development speed, cost efficiency, and technological innovation have made them indispensable partners for global pharmaceutical giants. AstraZeneca's establishment of a Global Strategic Research Center in Beijing, along with numerous multinational corporations increasing their equity investments in Chinese biotech companies, both indicate that this trend will continue to deepen in the coming years.

Multi-specific AntibodiesThe widespread application in tumor treatment reflects the evolution of Precision Medicine from single-target to multi-target and multi-mechanism synergy. The combination of PD-1/PD-L1 and VEGF is favored because it can simultaneously enhance immune response and inhibit tumor angiogenesis, achieving a "1+1>2" therapeutic effect. However, this field also faces challenges: the design, production, and safety evaluation of multi-specific antibodies are more complex than traditional antibodies. How to control adverse reactions while ensuring efficacy will be the key to future development. In addition, as more bispecific antibodies enter the late clinical stage, market competition will intensify, and differentiated design and indication selection will become the watershed for corporate success or failure.

Application of AI in Drug DiscoveryCurrently in the transition period from "proof-of-concept" to "large-scale application." AI technology has demonstrated significant advantages in protein structure prediction (e.g., AlphaFold), virtual screening, and molecular generation. However, its actual effectiveness in clinical translation still requires more data validation. At present, AI platforms mainly focus on the early discovery stage, while the majority of drug development costs and risks are concentrated in the clinical trial phase. Therefore, whether AI technology can truly shorten the overall R&D cycle and reduce failure rates remains to be seen through long-term clinical results. The industry generally expects that as the first batch of AI-designed drugs are approved for marketing in the coming years, the commercial value of this technology will be more clearly validated, thereby driving more early-stage investments.

From a broader perspective, the trends in licensing deals for 2025 reveal a core proposition:Innovation is seeking a new balance between globalization and specialization.Large pharmaceutical companies are increasingly relying on external sources of innovation, whether it's China's rapid clinical development capabilities, specialized antibody companies' engineering platforms, or the algorithmic advantages of AI startups. This "Open Innovation" model requires enterprises not only to have the ability to integrate diverse resources but also to establish new governance mechanisms in intellectual property, regulatory pathways, and cross-cultural collaboration. Meanwhile, small and medium-sized biotechnology companies need to adopt more precise positioning in terms of technological differentiation and commercialization strategies to stand out in fierce competition.

The Three Major Trends in Biopharmaceutical Licensing Deals in 2025—The Globalization of Chinese Companies, the Ongoing Popularity of Multi-Specific Antibodies, and the Rapid Penetration of AI Technology—Collectively Paint a Picture of Transformation in the Global Biomedical Industry.

These trends not only reflect the current technological frontier and market demands but also foreshadow that future drug development will rely more heavily on deep cross-regional and interdisciplinary collaboration. As the first batch of AI-designed drugs and a new generation of multi-specific antibodies progressively enter the late clinical stages, the true value of these technological pathways will be validated in the coming years, potentially redefining the entire industry’s innovation paradigm. For patients, this means more and more effective treatment options are accelerating their arrival.