Top 10 Predictions for China's Pharmaceutical Industry in 2019: Accelerating and Irreversible Changes

Editor’s Note: This article is reprinted from E-Pharma Manager, authored by Guo Zizhen. VCBeat has been authorized to republish it.

In 2018, numerous events unfolded. While these events appeared superficially to be mere beginnings, they were in fact the crux of major developments that had occurred previously and served as the catalysts for future upheavals.

In the first half of 2018, the pharmaceutical industry achieved significant excess returns, driven by a rebound in growth and the implementation of numerous favorable policies amid the deepening of the new healthcare reforms.

However, the winter of that year was exceptionally long, seemingly beginning in summer: The US-China trade war erupted, impacting China’s active pharmaceutical ingredient (API), formulation, and biopharmaceutical sectors, which had traditionally been characterized by their defensive resilience. The “Guiding Opinions on Regulating the Asset Management Business of Financial Institutions” (commonly known as the New Asset Management Regulations) were officially released and implemented, leading to deleveraging and a comprehensive tightening of source capital after years of liquidity ease. Pharmaceutical quality and safety issues, such as the Changsheng Vaccine incident, triggered market panic and coincided with personnel upheavals among the top designers of the new round of drug review and approval reforms. The volume-based procurement rules emerged unexpectedly, working in tandem with the consistency evaluation process, ushering in major changes to the generic drug landscape and causing fundamental shifts in established business models...

Facing 2019, we believe that all days originate from the night, just as all springs begin in winter.

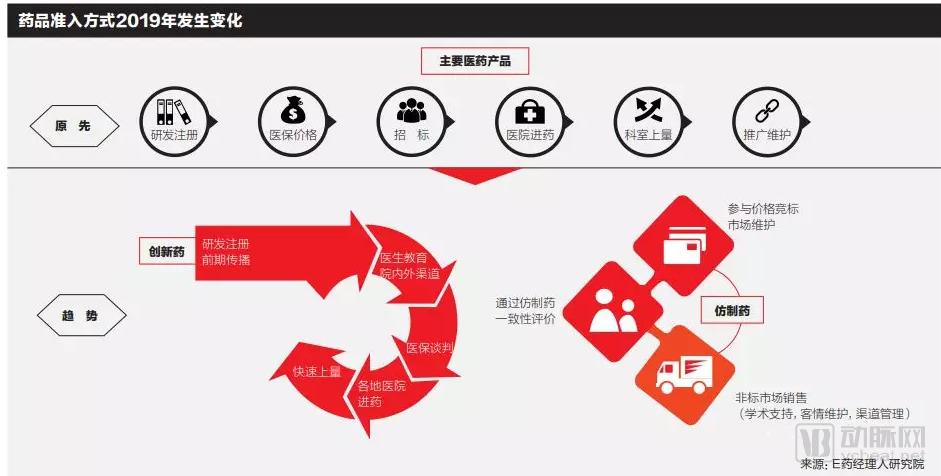

It is certain that volume-based procurement was the defining event for the pharmaceutical industry in 2018, representing a new round of nationwide quantity-price negotiations aimed at ensuring drug quality and controlling costs.

The “government-led, province (autonomous region, municipality directly under the Central Government)-based online centralized drug procurement” system, implemented for many years, has given rise to various models such as “listed procurement,” secondary price negotiations, and Group Purchasing Organizations (GPOs) as reforms have advanced. With the transfer of drug procurement responsibilities to the National Healthcare Security Administration in 2018 and the introduction of the “4+7” policy, China’s centralized drug procurement and drug pricing mechanisms have entered a new phase.

The volume-based procurement pilot launched in late 2018, covering 31 drug varieties across 11 cities, exhibited the characteristics of “moderate volume commitments and aggressive price reductions.” By leveraging consistency evaluation as the quality benchmark, production costs as the price floor, and procurement volumes as bargaining chips, this approach ensured targeted and effective price cuts. Under the current volume-based procurement framework, the pharmaceutical market is undergoing a redistribution of market share, thereby making room for high-quality innovative drugs. As these policies are rolled out nationwide in the future, supply security and quality assurance will emerge as new focal points.

The propositions awaiting resolution in 2019 are: How will the drug utilization structure in public hospitals across the 11 pilot cities change following the “4+7” volume-based procurement? What impact will the “4+7” volume-based procurement have on drug prices in other cities? When will the next round of similar “4+7” volume-based procurement take place? Which companies will emerge as dark horses in the post-“4+7” era?

The policy evolution of centralized drug procurement is marked by three key documents: The 2001 document, "Notice on Issuing the Specifications for Centralized Bidding and Procurement of Drugs by Medical Institutions (Trial)," signaled China’s entry into the phase of centralized procurement. By 2009, the new healthcare reform introduced a new stage characterized by "government-led, province-based, online centralized procurement." In 2015, the "Guiding Opinions of the General Office of the State Council on Improving Centralized Drug Procurement in Public Hospitals" proposed adhering to the direction of province (autonomous region, municipality)-based online centralized drug procurement, implementing a single platform with vertical coordination, transparency, and classified procurement, thereby entering the stage of classified procurement. In 2017, the "Several Opinions of the General Office of the State Council on Further Reforming and Improving Policies for Drug Production, Circulation, and Use" provided top-level design for the entire chain of drug production and circulation and further implemented the classified drug procurement model.

What distinguishes this round of centralized drug procurement from previous ones is as follows: First, it has received a high level of attention at the national level. National leaders have emphasized the importance of deepening reforms in the drug supply and guarantee system and put forward clear requirements for centralized drug procurement at the National Health and Wellness Conference. Second, a multi-tiered medical security system centered on the basic medical insurance scheme has been basically established. The integration of urban and rural basic medical insurance has been achieved, with annual fund revenues and expenditures exceeding RMB 3 trillion, thereby creating greater group purchasing power.

Most importantly, the establishment of the National Healthcare Security Administration in 2018 optimized the governance structure of medical insurance and enhanced governance capabilities, creating conditions for medical insurance to participate in price setting and centralized procurement.

Since the theme of China’s pharmaceutical industry development shifted from generics to innovation, drug innovation has become the core driver supporting enterprises’ future growth, prompting a surge in new drug R&D projects.

Over the past five years, China’s pipeline of Class I new drug development has continued to expand. Innovation experienced explosive growth in 2018, with both the number of clinical trial applications for new drugs and the number of approved investigational new drug trials growing at a rate of 20%–30%. The growth rate of newly approved marketed drugs also reached a breakthrough level of 40%.

Accelerated drug approval policies serve as the primary policy safeguard for boosting domestic R&D capabilities. According to statistics from the National Medical Products Administration (NMPA), the number of pending drug registration applications has dropped from a peak of 22,000 in 2015 to fewer than 3,200. The review and approval processes for innovative drugs and medical devices have been further expedited. Jiao Hong, Commissioner of the NMPA, stated that new drugs under review are categorized to prioritize those treating rare diseases and preventing or treating life-threatening conditions, such as anti-HIV and anticancer medications. The NMPA will concentrate its review resources to accelerate these assessments, aiming to complete reviews for rare disease drugs within three months and for other clinically urgent drugs within six months, thereby shortening the time to market by an estimated one to two years.

However, it is undeniable that there is currently a phenomenon of clustering of innovative drugs in certain hot fields. Drug research and development in China still mainly focuses on fast-following, with most drugs being Me-too or Me-better, and very few first-in-class.

The proportion of oncology drugs in R&D pipelines is particularly significant for Chinese pharmaceutical companies, accounting for nearly half of their portfolios. Chinese pharmaceutical firms have devoted substantial resources to popular therapeutic areas and high-profile targets. Statistics show that the top 20 pharmaceutical companies in China have 22 VEGF projects, 15 HER2 projects, and 10 PD-1/PD-L1 projects under development. When considering all pharmaceutical companies across China, the number of PD-1/PD-L1 projects in development approaches 100.

Amid the Fierce Competition in PD-1, CAR-T, and DPP4 Inhibitors, What Are the Strategies of Domestic Enterprises? Represented by Ascletis, BeiGene, Innovent, Junshi Biosciences, Henlius, and Zai Lab, China’s emerging innovative pharmaceutical companies have navigated the stages of startup formation, R&D, financing, clinical trials, and IPOs in recent years, with their product launches now at the final critical stage.

In 2019, the launch of these new products will serve as a stage for domestic innovative pharmaceutical companies to showcase their capabilities. Beyond assembling core commercialization teams, the subsequent challenges will lie in managing and incentivizing these teams. Thereafter, numerous aspects—including new product planning, market positioning, sales strategies, government affairs, decisions on self-operation versus agency models, academic promotion, and compliance—will test these biotech upstarts founded by scientists.

In November 2018, the National Essential Medicines List (2018 Edition) was officially implemented across China, marking its first revision in six years since the previous update. The 2018 edition added 187 medicines and removed 22 (including 17 chemical drugs), increasing the total number from 520 to 685. A certain number of oncology drugs and innovative medicines were included in the list.

It is worth noting that the National Essential Medicines List (NEML) and the National Reimbursement Drug List (NRDL) do not fully overlap, with many essential medicines not yet included in the NRDL. Whether essential medicines will be incorporated into the NRDL in the future depends on whether they are proven effective and urgently needed by patients. For non-innovative drugs, passing the consistency evaluation is mandatory; otherwise, sustainable procurement across various regional markets would be difficult. With the implementation of volume-based procurement (VBP) under the medical insurance scheme, essential medicines must also undergo competitive bidding on price to gain entry into the NRDL.

For a long time, there have been strong calls from various stakeholders for reform of the National Essential Medicines List (NEML). Key market concerns include cost factors and the establishment of mechanisms for drug iteration and phase-out. With the implementation of volume-based procurement under medical insurance and the potential future introduction of medical insurance payment standards, dynamic adjustments to drug prices and market utilization are imperative. A more flexible and market-oriented mechanism for the NEML will be the direction of future reforms.

The characteristics of China’s National Essential Medicines List (NEML) are its relatively limited product categories, slow update cycles, and the absence of a rolling admission mechanism; new drugs must wait for the next round of list review to be included. The dilemmas facing the current system stem from two main aspects. First, there is inherent pressure on the medical insurance fund pool. Due to rapid population aging, legacy issues related to employee contributions, and disparities in contribution capacity between urban and rural areas, medical insurance reimbursement has long faced the dilemma of whether to prioritize breadth before depth or depth before breadth. Second, there is the challenge of cost containment. As long as hospitals’ economic interests remain tied to pharmaceutical sales, expanding medical insurance coverage will inevitably raise concerns about potential abuse.

What impact will the new edition of the National Essential Medicines List have on the pharmaceutical market in 2019? Can the national essential medicines system be effectively implemented? What measures will healthcare institutions take?

In 2019, the pharmaceutical industry will once again be hit by an anti-commercial bribery storm. The medical representative registration system, which has been stalled for a year, will be restarted. Efforts to improve professional conduct in medical institutions will be intensified.

On May 17, 2018, the State Administration for Market Regulation issued the “Announcement on Launching Key Enforcement Actions Against Unfair Competition,” initiating a nationwide campaign from May to October 2018. The outcomes of this campaign once again exposed numerous issues in the pharmaceutical sector, spanning various business lines, and demonstrated that commercial bribery is no longer confined to the purchase and sale of pharmaceutical products.

Meanwhile, the issue of commercial bribery during the IPO review process for multiple pharmaceutical companies has again been raised by the Issuance Examination Committee, including the specific breakdown of promotional expenses and academic promotion fees in each period of the reporting period. Involving customer kickbacks, off-book rebates, gifts, and other disguised forms of commercial bribery, commercial bribery by pharmaceutical companies has once again become a key focus of attention.

Hospital presidents, Pharmacy and Therapeutics Committees, and pharmacy departments hold the authority to determine hospital drug procurement catalogs, making them key targets for pharmaceutical companies’ public relations efforts. Due to the small number of individuals in these roles and the substantial amounts involved in bribery, recent enforcement cases have typically involved sums exceeding RMB 1 million, with some surpassing RMB 100 million, thereby generating significant public outcry and media pressure.

The Changsheng Vaccine Incident became the biggest black swan event in the pharmaceutical industry in 2018, but what lay hidden behind this incident was the “ticking time bomb” planted by changes in manufacturing processes within the pharmaceutical sector.

In August 2016, the former China Food and Drug Administration (CFDA) issued the “Announcement on Launching the Verification of Drug Manufacturing Processes (Draft for Comments),” ushering in a new round of stringent inspections into manufacturing processes. The document stated: “In recent years, food and drug regulatory authorities have discovered during supervisory inspections that certain drug products approved for marketing before 2007 were not manufactured in accordance with their approved manufacturing processes, and that changes to manufacturing processes were not researched and submitted for approval as required.”

During the production phase, companies often encounter situations where the "registered manufacturing process" fails to yield qualified pharmaceutical products. To produce compliant drugs, pharmaceutical enterprises begin to explore and optimize their manufacturing processes, which inevitably entails process changes. Additionally, to protect trade secrets, some companies may provide false descriptions of their manufacturing processes or deliberately submit incomplete registration dossiers with ambiguous parameters.

Reasons for enterprises’ non-compliant process changes without filing applications include: major changes require validation, and even clinical trial validation, which companies are reluctant to undertake due to the associated time and financial costs. Furthermore, the review and approval queue for all change applications is lengthy.

In another scenario, pharmaceutical companies deliberately and maliciously substitute high-cost excipients with cheap, substandard ones. For instance, the exposure of Changchun Changsheng’s fraud stemmed from a real-name whistleblower report by a former employee. The specific fraudulent practice involved an unauthorized change to a critical manufacturing process, which the manufacturer failed to report and obtain approval for in a timely manner.

In the pharmaceutical industry, an inadvertent change in a manufacturing process can lead to vastly divergent outcomes. In this regard, what are the respective responsibilities of governments, industry associations, enterprises, and third-party organizations? How can management practices be strengthened to prevent fraudulent activities similar to those committed by Changchun Changsheng?

As one of the world’s leading producers of active pharmaceutical ingredients (APIs), China is home to more than 2,000 API manufacturers capable of producing approximately 1,600 different APIs, with an annual output exceeding 1 million metric tons. In recent years, however, soaring API prices have remained persistently high, affecting multiple API varieties.

According to a notice issued by the State Administration for Market Regulation, since February 2018, under the leadership of Hunan Er-Kang Pharmaceutical Co., Ltd., Hunan Er-Kang and Henan Jiushi Pharmaceutical Co., Ltd. maintained close contact and coordinated their actions to abuse their dominant market position. They sold chlorpheniramine maleate active pharmaceutical ingredients (API) to downstream operators at unfairly high prices or refused to supply the API to downstream operators on the grounds of “unavailability.”

Not only chlorpheniramine, but according to incomplete statistics, since 2018, nearly ten types of active pharmaceutical ingredients (APIs), including phenol, inosine, isoniazid, allopurinol tablets, amino acids, vitamins, uric acid, camphor, and meglumine, have experienced varying degrees of price increases within a short period.

In recent years, increasingly stringent national environmental protection requirements have led some active pharmaceutical ingredient (API) manufacturers to scale back or even halt production, resulting in insufficient production and supply of certain APIs. Beyond this, the primary cause lies in the lack of adequate competition in China’s current API market, where frequent instances of unfair competition and monopoly have driven price hikes and even supply disruptions.

“Rising prices of active pharmaceutical ingredients (APIs) have long been a recurring topic. The primary reason is the insufficient marketization of China’s domestic API market, which has led to persistent cutthroat competition,” said Guo Yunpei, President of the China Pharmaceutical Enterprise Management Association. In 2018, Guo Yunpei conducted field research in multiple regions to investigate the issue of rising API prices. His findings revealed that many pharmaceutical companies are more concerned about their predicament under the national “4+7” volume-based procurement pilot program: after state-led price negotiations force drug prices down to their lowest levels, how should companies cope with potentially rising costs of raw materials and excipients? Will this pressure compromise the baseline standards for drug quality?

Over the past two years, drug procurement policies and various forms of secondary price negotiations have tightened control over drug prices, shrinking profit margins and causing many drugs to lose bids or even be withdrawn from hospital tendering processes. As the zero-markup policy for hospitals is further implemented, hospitals’ operational incentives have diminished. Consequently, pharmaceutical manufacturers, distributors, and retail outlets all anticipate the outflow of hospital prescriptions, triggering the so-called “explosive surge in the outflow of RMB 300 billion worth of prescription drugs.”

The share of the domestic prescription drug market accounted for by retail pharmacy outlets has risen to 9.8%. However, the primary beneficiaries of prescription outflow are currently pharmacies affiliated with Sinopharm, Shanghai Pharmaceuticals, and China Resources Pharmaceutical, which maintain close collaborations with hospitals. These pharmacies are predominantly concentrated in first-tier cities, such as Renhe Pharmacy Online (formerly Jingwei Pharmacy), Cardinal Health Pharmacy (formerly Baiji Xinte Pharmacy), Shanghai Zhongxie Pharmaceutical (now part of Shanghai Pharmaceuticals), and Beijing Yibao Quanxin Grand Pharmacy.

Meanwhile, driven by a surge in capital, the retail pharmacy terminal is undergoing rapid consolidation and becoming highly concentrated, gearing up for the “outflow of prescriptions.”

Since their listings on the A-share market, the four major listed pharmacy chains—Yixintang, Yifeng Pharmacy, Laobaixing, and Dashenlin—have advanced rapidly, launching an aggressive “land-grab” campaign and emerging as the primary drivers of mergers and acquisitions and consolidation in the pharmacy industry in recent years.

However, the major players are not industrial capital, but private equity consortia from the primary market. PE-backed capital, represented by Hillhouse Capital, CDH Investments, Hony Capital, the Huatai Group, and Morgan Stanley-affiliated firms, is rapidly expanding its footprint and competing fiercely in the pharmacy merger and acquisition market.

The “U.S. Section 301 Investigation Report on China,” released on November 20, 2018, consistently emphasized that the Chinese government’s strategic priorities in the biopharmaceutical sector are directly linked to the interest of Chinese venture capital firms in overseas biotechnology companies, and it unusually named three Chinese VC firms. Since the listing of Ascletis Pharma, the first biotech company on the Hong Kong Stock Exchange’s new listing board, in August this year, four innovative companies—Ascletis Pharma, BeiGene, Hua Medicine, and Innovent Biologics—have gone public on the HKEX. In November, news emerged that the Chinese government will establish the Science and Technology Innovation Board (STAR Market) on the Shanghai Stock Exchange and pilot a registration-based IPO system.

Will capital support for biopharmaceutical innovation in China be affected by the US-China trade war? Will the capital market welcome biopharmaceutical innovation with a winter chill or a spring warmth? What impact will the HKEX’s Innovation Board and the SSE’s STAR Market have on biopharmaceutical innovation in China? How should companies driven by innovative drug R&D that went public in 2019 be rationally valued?

The listing of innovative pharmaceutical companies in Hong Kong and the United States is not driven by capital, but rather represents a “baton pass” of capital. From venture capital (VC) and private equity (PE) to the capital markets, the financial support for innovative drugs has become more robust, turning investment in innovative drugs into a “business” rather than a “gamble.” This is undoubtedly good news for the advancement of innovative drugs and therapeutic methods, as only an institutionalized and industrialized investment model can ensure stable output.

On December 12, the National Health Commission issued the Notice on Strengthening the Clinical Application Management of Adjuvant Drugs (hereinafter referred to as the “Notice”), explicitly stating that clinical application management of adjuvant drugs in medical institutions will be strengthened to improve the rational use of medications.

The “Notice” specifies that medical institutions at the secondary level and above in each province shall compile a catalog of adjuvant drugs by listing them under their generic names, ranked in descending order by annual expenditure, with no fewer than 20 varieties, and submit this catalog to the provincial health administrative departments. After consolidating the submissions, each provincial health administrative department shall report information on the top 20 varieties, listed by generic name and ranked in descending order by total expenditure, to the National Health Commission. The National Health Commission will formulate and publish a national catalog of adjuvant drugs. Sound management systems and working mechanisms shall be established and improved to strengthen whole-process management of adjuvant drugs across all stages, including selection, procurement, prescription, dispensing, clinical application, monitoring, and evaluation.

It is evident that the regulation of adjuvant drugs has become a major nationwide initiative extending from the national to regional levels. Coupled with intensified cost-containment efforts in medical insurance from the central government to local authorities, regulatory oversight of adjuvant drugs will continue to tighten.

But how exactly should adjuvant medications be defined? How can we avoid the unjustified exclusion of such drugs?

According to relevant statistics, as of now, a total of 14 provinces and regions, including Beijing, Hebei, Shanxi, Inner Mongolia, Liaoning, Jiangsu, Anhui, Hubei, Yunnan, Fujian, Sichuan, Guangxi, Qinghai, and Gansu, have issued relevant policies explicitly stating that adjuvant drugs will be subject to key supervision or restricted use, among which 9 provinces and municipalities have published specific lists.

From the National Healthcare Security Administration’s launch of pilot programs for Diagnosis-Related Group (DRG)-based payment, to the National Health Commission’s implementation of numerous policies on the management of adjuvant drugs and clinical pathways for diseases, the successive rollout of various regulatory measures means that the release of the 2019 national list of adjuvant drugs will trigger a major reshuffle in the relevant sectors.

China is a major producer of generic drugs, with over 95% of its nearly 170,000 drug approval numbers belonging to generics. However, on the supply side, the industry is large but not strong; low quality standards, a fragmented manufacturer base, widespread cutthroat competition, and pervasive kickback-driven sales practices have even allowed so-called “miracle cures” to flourish. On the demand side, many patients cannot afford high-priced originator drugs, leading to not uncommon instances of purchasing counterfeit foreign medicines or self-compounded drugs online. This underscores an urgent need for reform to break the deadlock. With the introduction of the “4+7” policy, many have begun to see the future direction of China’s generic drug industry. But will this future be one filled with opportunities, or will it be fraught with thorns?

The United States is the world’s largest generic drug market, with a market size of $70 billion. Meanwhile, it also boasts the highest generic substitution rate and the fastest substitution speed globally. Generic drugs account for over 90% of prescription volumes in the U.S., but less than 20% of sales revenue. Among developed countries, the United Kingdom has the highest share of generic drug sales, exceeding 25%, followed by Canada, where the share of generic drug sales has long remained at around 24%.

A review of both international and domestic markets reveals that declining generic drug prices are a major trend, yet the development of generics remains highly promising. Varieties that have passed the Consistency Evaluation of Quality and Efficacy for Generic Drugs face only price reductions; however, inclusion in national centralized procurement can significantly reduce sales costs, enabling profitability through high-volume, low-margin sales.

In 2019, the Year of the Pig, there may have been another Year of the Pig in history that resembled this one. Scholar Ray Huang wrote a short book about it titled 1587, A Year of No Significance. People might easily dismiss this year as “insignificant,” as it saw no major battles, no collapse of empires, and no natural disasters; yet there were more subtle developments worth noting, as well as more concentrated internal conflicts. The book was later republished under the title Wanli Shiwu Nian (The 15th Year of the Wanli Reign) and became a bestseller.

In 2019, a series of events unfolded, including volume-based procurement, medical insurance cost containment, national drug price negotiations, consistency evaluation, tiered diagnosis and treatment, the National Key Monitoring Drug List, and the market launch of innovative drugs.