Automated Testing Platforms and iPOCT Applications Rapidly Gaining Traction, with Glucose Testing Leading a RMB 12.9 Billion Market

Editor's Note: This article is reposted from a WeChat official account.Author, Built to Last Economic Research InstituteLi Yong. Reposted with authorization from VCBeat.

As the market penetration of POCT products continues to increase, we estimate that the market size in China will exceed RMB 12.9 billion in 2020, with high-growth segments such as blood gas/electrolytes, diabetes, and cardiac markers warranting particular attention.

National-level requirements for point-of-care testing (POCT) are driving the volume growth of cardiovascular POCT products in hospitals. Based on a neutral estimate, the market size of POCT products for heart disease is expected to increase proportionally with the number of patients, reaching RMB 2.1 billion in 2020. POCT blood glucose meters can be used for initial screening or self-monitoring of blood glucose control by patients during treatment. According to the clinical application guidelines for continuous glucose monitoring (CGM), the market size for blood glucose meters is projected to reach RMB 6.7 billion in 2020. With the implementation of national policies in emergency centers, the market for blood gas and electrolyte analyzers is expected to maintain a compound annual growth rate (CAGR) of approximately 25%, with the market size reaching around RMB 2 billion by 2020.

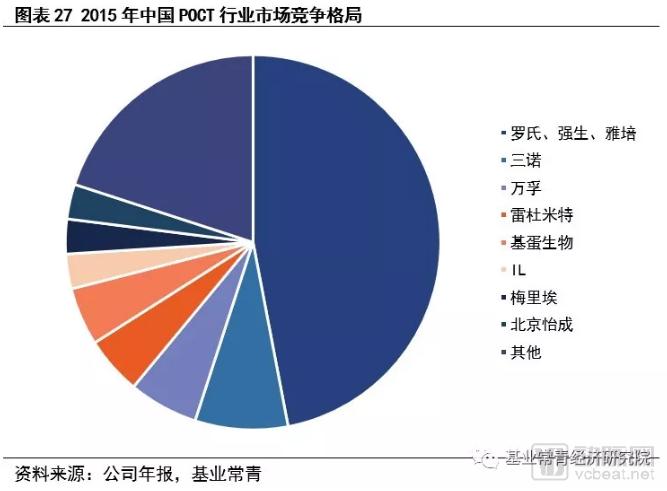

Competitive Landscape: The three major international players hold approximately 45% market share; policy support is driving the growth of domestic enterprises, with leading companies poised to accelerate their market share expansion.

Foreign enterprises account for half of the Chinese market, while domestic companies are expected to benefit from incremental market growth, gradually stabilizing and expanding their market share. The three international diagnostic giants—Roche, Johnson & Johnson, and Abbott—hold a combined market share of approximately 45%. A-share listed companies Sinocare, Wondfo, and Getein have achieved a market share of around 20% by establishing competitive advantages in specific segments. Well-known non-listed companies deeply entrenched in the industry, such as Beijing Yicheng and Rayleigh Biotech, account for approximately 10% of the market.

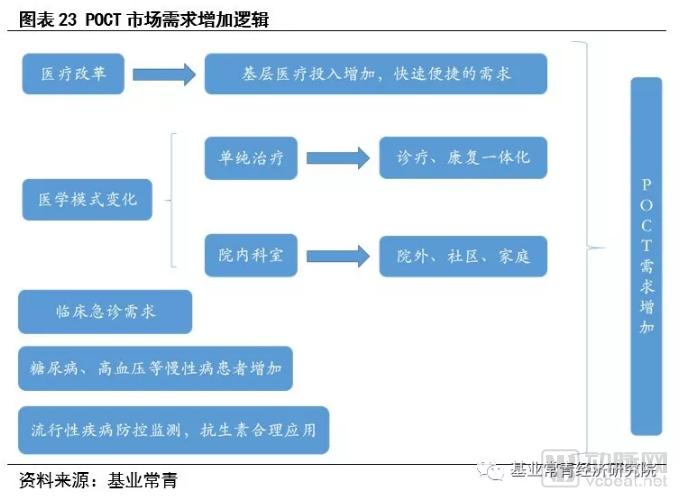

First, there is a rigid demand for point-of-care testing (POCT) in hospital emergency departments and operating rooms. Second, the large population of patients with chronic diseases such as diabetes has generated a need for POCT to support daily monitoring. Furthermore, healthcare reform policies continue to promote the development of primary care. Given that primary healthcare institutions still need to improve their basic infrastructure and the professional competency of their staff, there is a practical demand for these facilities to equip themselves with appropriate diagnostic devices and adopt new diagnosis and treatment models.

Domestic POCT manufacturers are strategically positioning themselves in high-growth niche segments, including cardiac markers, blood glucose monitoring, and blood gas/electrolyte analysis. The high patient volume in healthcare institutions has generated substantial demand for fully automated POCT devices capable of rapid, efficient, high-throughput testing. Furthermore, the need for real-time data monitoring in personalized chronic disease management is inevitably driving the development of cloud-based iPOCT architectures.

With the implementation of supportive policies, domestically produced POCT products will accelerate their market penetration. Therefore, we recommend investing in leading enterprises that have established a presence in high-growth niche segments such as cardiac marker testing, blood glucose monitoring for diabetes, and blood gas/electrolyte analysis:

1. AllTest Diagnostics: Globally Renowned Healthcare Capital Enters the Market, Pioneering the iPOCT Model

2. Ruilai Bio: Led by a Member of the U.S. National Academy of Sciences, China’s First Molecular Diagnostic Reagent Exporter

3. Guosai Biotech: Proprietary specific protein detection technology; holds over 30% market share in the domestic specific protein testing segment

4. Beijing Yicheng: An Enterprise Supported by the “863” Program, Building a Web-Based Chronic Disease Management Platform

*Risk Warning: Policy risks; industry development falling short of expectations; company operational risks.

1.1 POCT Testing: Simplifying Complexity, Meeting Diverse Needs Through Point-of-Care Testing

The 2014 Edition of the “Expert Consensus on Point-of-Care Testing (POCT)” defines POCT (Point-of-Care Testing) as immediate testing or rapid on-site testing, referring to a testing method conducted at the sample collection site that utilizes portable analytical instruments and supporting reagents to rapidly obtain test results.

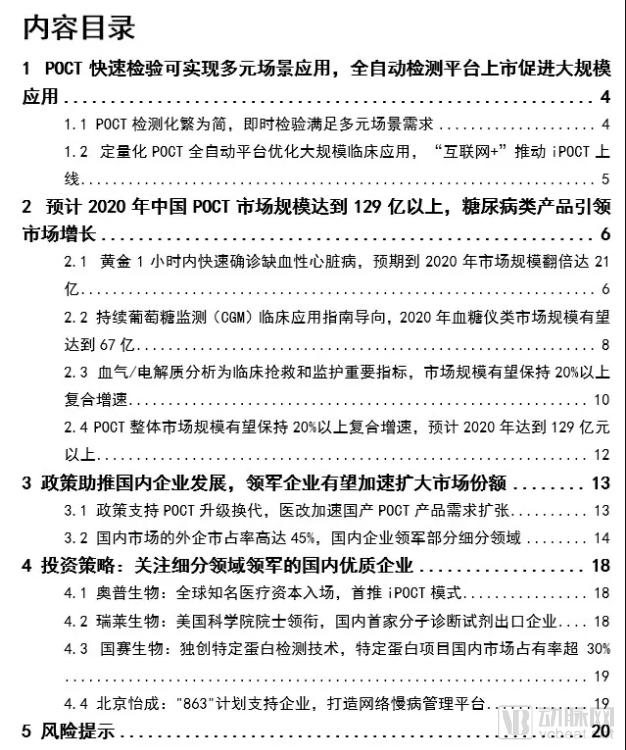

In hospital clinical laboratories, the patient testing process is divided into 11 detailed steps, whereas POCT (Point-of-Care Testing) requires only four steps: sample collection, sample analysis, quality control, and result interpretation. This simplifies the workflow and saves time. Compared with large-scale laboratory analyzers, POCT offers the advantages of speed and convenience. POCT utilizes simple specimens that require no preprocessing, features straightforward product calibration, employs portable instruments, and enables immediate testing with lower demands on operator expertise. However, it has relatively lower accuracy and higher testing costs.

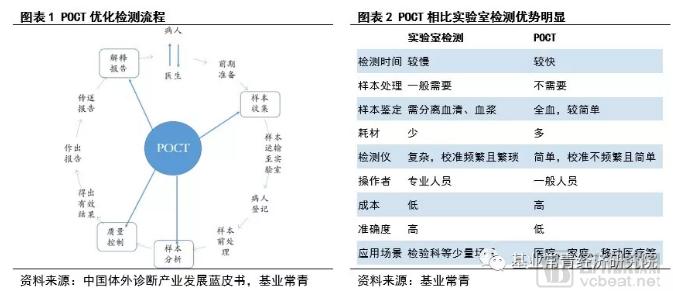

Due to its rapid testing and ease of use, Point-of-Care Testing (POCT) is widely applied across various settings, primarily in hospital clinical departments, Centers for Disease Control and Prevention, food safety inspections, customs inspections, and home-based personal testing. Furthermore, POCT products encompass a range of tests, including cardiac marker detection, blood glucose monitoring, blood gas/electrolyte analysis, and pregnancy testing.

1.2 Optimization of Quantitative POCT Fully Automated Platforms for Large-Scale Clinical Application; “Internet+” Drives the Launch of iPOCT

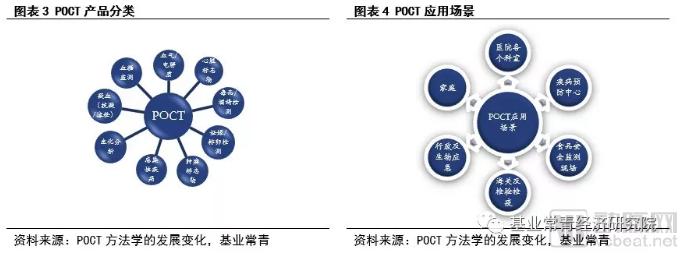

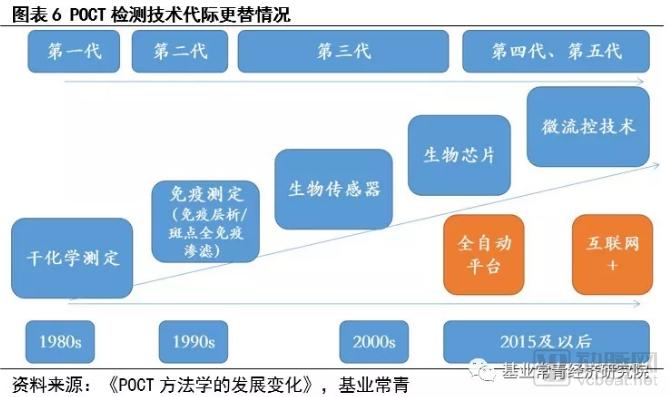

In 1993, China’s first electronic blood glucose meter was developed and launched by Yicheng Biology. After 2000, the domestic POCT market gradually developed; since 2012, Chinese companies have reached a certain scale and have gone public one after another. In 2015, the first fully automated POCT workstation in China was launched. By 2017, fully automated POCT platforms had become popular products, marking the development of China’s POCT platforms toward large-scale application.

Since the 1990s, POCT products have undergone continuous updates and iterations, progressing through four developmental eras: from qualitative to semi-automated quantitative, then to semi-quantitative, and finally to fully automated quantitative products. Currently, by integrating fourth-generation automated quantitative technology with internet technologies, a fifth-generation iPOCT has been developed, characterized by “precision, automation, cloud connectivity, and sharing.” Technologically, this has achieved upgrades in dry chemistry assays, immunoassays, biosensors, biochips, and microfluidics.

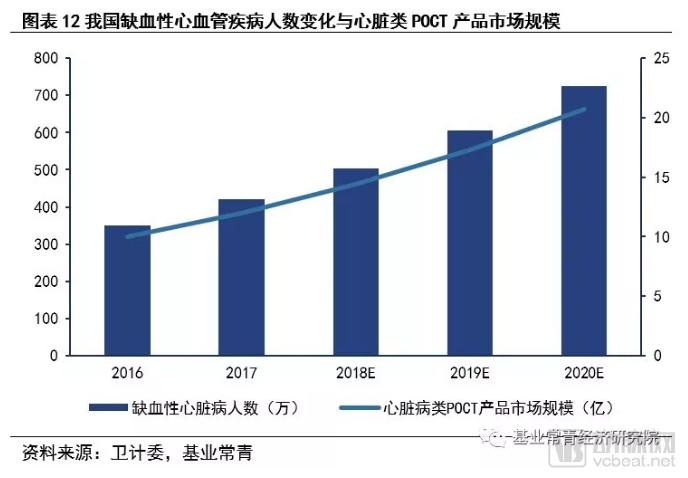

2.1 Rapid Diagnosis of Ischemic Heart Disease Within the Golden Hour, with Market Size Expected to Double to RMB 2.1 Billion by 2020

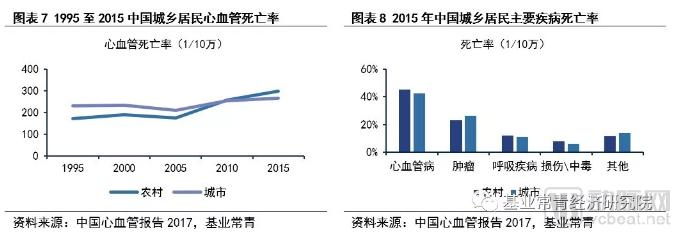

According to the Report on Cardiovascular Diseases in China 2017, there are 290 million patients with cardiovascular diseases in China. In 2015, cardiovascular disease remained the leading cause of death among both urban and rural residents, accounting for more than 40% of all disease-related deaths: 45.01% in rural areas and 42.61% in urban areas. Moreover, the mortality rate from cardiovascular diseases has shown a year-on-year increase. Taking myocardial infarction as an example, it causes approximately 520,000 deaths annually, with the mortality rate in rural areas reaching as high as 70.09%.

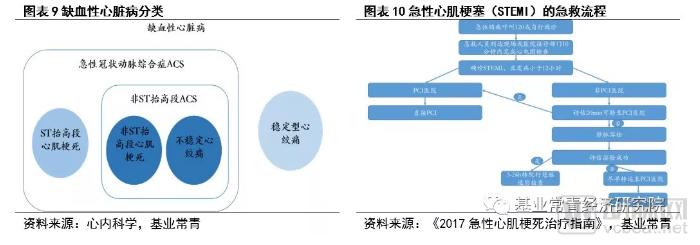

Heart disease is categorized into ischemic and non-ischemic types. Ischemic heart disease typically causes myocardial injury; therefore, diagnosis through the detection of cardiac biomarkers is essential to achieve favorable prognostic outcomes. Myocardial infarction, in particular, presents with a severe and rapid onset, with the golden window for treatment being within one hour of symptom onset. Point-of-care testing (POCT) products for cardiac biomarkers enable rapid diagnosis. Furthermore, by detecting relevant biomarkers in the blood prior to disease onset, POCT products can facilitate preliminary assessment of the patient's condition and provide early warning signals.

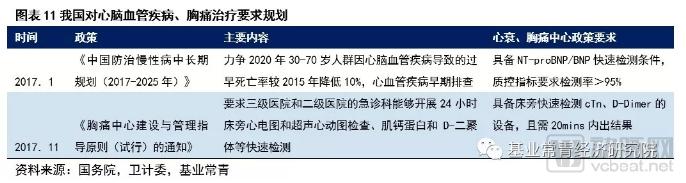

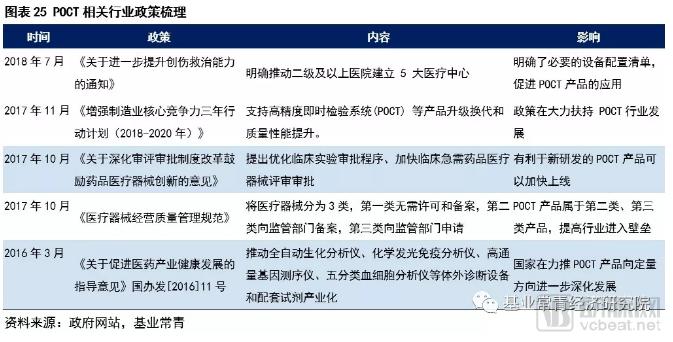

In 2017, the Chinese government separately issued the "Medium- and Long-Term Plan for the Prevention and Control of Chronic Diseases in China (2017–2025)" and the "Notice on Guidelines for the Construction and Management of Chest Pain Centers (Trial)," establishing specific requirements for Chest Pain Centers and Heart Failure Centers: Chest Pain Centers must be equipped with point-of-care testing devices for cardiac troponin (cTn) and D-dimer, capable of delivering results within 20 minutes; Heart Failure Centers must have the capacity for rapid testing of NT-proBNP/BNP, with a quality control indicator requiring a detection rate of >95%.

The Plan aims to reduce the premature mortality rate from cardiovascular and cerebrovascular diseases among individuals aged 30–70 by 10% in 2020 compared with 2015, and emphasizes early screening for cardiovascular diseases. It requires emergency departments in tertiary and secondary hospitals to provide 24-hour bedside electrocardiography (ECG) and echocardiography, as well as rapid testing for troponin and D-dimer. National-level requirements for point-of-care testing (POCT) will drive continuous growth in the adoption of cardiovascular POCT products in hospitals.

According to data released by the National Health and Family Planning Commission, the number of hospital discharges for ischemic heart disease was approximately 3.5 million in 2016. Based on statistical analysis, we project that the number of discharges for ischemic heart disease will maintain an annual growth rate of approximately 20% through 2020, reaching an estimated 7.26 million by that year. In 2016, the market size for POCT (Point-of-Care Testing) cardiac products was approximately RMB 1 billion. Under a neutral scenario, assuming the market size grows in proportion to the number of patients, the market for POCT cardiac products is expected to reach RMB 2.1 billion by 2020.

2.2 Guided by Clinical Application Guidelines for Continuous Glucose Monitoring (CGM), the Market Size of Blood Glucose Meters Is Expected to Reach RMB 6.7 Billion in 2020

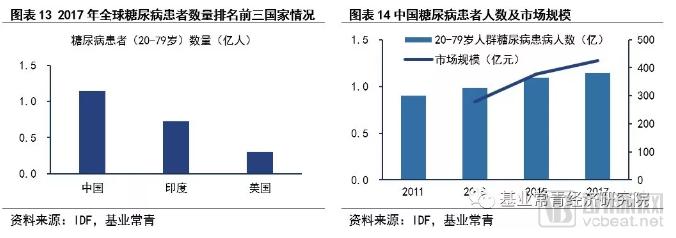

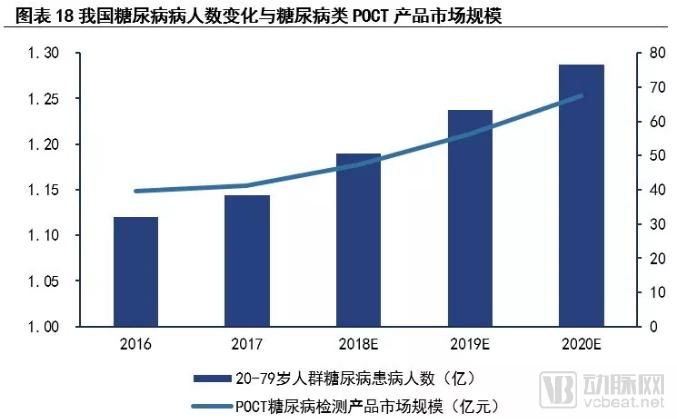

According to the 2017 IDF Diabetes Atlas (8th edition) released by the International Diabetes Federation (IDF), the top three countries with the highest number of diabetic patients aged 20–79 in 2017 were China, India, and the United States, with patient counts of 114.4 million, 72.9 million, and 30.2 million, respectively. From 2011 to 2017, the number of diabetic patients in China increased from 90 million to 114.4 million, representing a compound annual growth rate (CAGR) of 4.08%. From 2013 to 2017, the market size for diabetes diagnosis and treatment grew from RMB 27.8 billion to RMB 42.5 billion, with a CAGR of 11.20%.

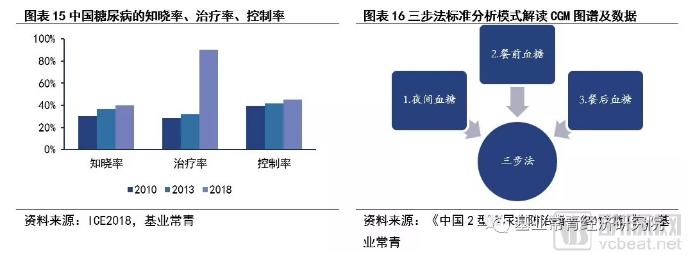

Although China has a large number of diabetes patients and a relatively stable incidence rate, the awareness and control rates for diabetes in China are only about 40%. Therefore, the primary tasks for the future will be to raise awareness among the remaining approximately 60% of undiagnosed individuals and to improve glycemic control in those already undergoing treatment. Only through early detection and early intervention can blood glucose levels be timely controlled, thereby reducing the occurrence of complications.

The Chinese Guidelines for the Prevention and Treatment of Type 2 Diabetes (2017 Edition) specifically highlights “blood glucose monitoring,” emphasizing its critical role in diabetes management, and recommends adopting the “three-step” standard analysis model to interpret continuous glucose monitoring (CGM) profiles and data. According to the Chinese Clinical Application Guidelines for Continuous Glucose Monitoring (2017 Edition), the level of blood glucose control is directly related to the patient’s disease status; blood glucose monitoring can assess glycemic metabolism in patients with diabetes, thereby facilitating the formulation of reasonable treatment plans. However, due to significant intraday blood glucose fluctuations, testing at least 1–4 times per day is required to ensure the validity of this transient indicator, thus necessitating patient cooperation through self-monitoring.

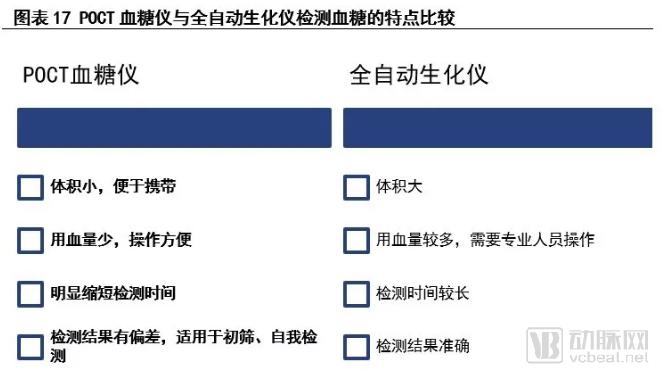

A comparison of blood glucose measurements using POCT glucometers and fully automated biochemical analyzers reveals that POCT glucometers offer distinct advantages, including compact size, portability, ease of operation, minimal blood sample requirements, and significantly reduced testing time. Therefore, they are suitable for initial screening and for self-monitoring of glycemic control by patients during treatment.

According to data released by the International Diabetes Federation (IDF), the number of people aged 20–79 with diabetes in China was approximately 114 million in 2017. Based on statistical analysis, we project that the number of diabetic patients in this age group will maintain a compound annual growth rate (CAGR) of approximately 4% through 2020, reaching an estimated 129 million by 2020. In 2016, the market size for point-of-care testing (POCT) diabetes products was approximately RMB 4 billion. Under a neutral scenario, assuming the market size grows proportionally with the number of patients, the market for POCT diabetes products is expected to reach RMB 6.7 billion by 2020.

2.3 Blood Gas/Electrolyte Analysis: A Critical Indicator for Clinical Emergency Care and Monitoring, with Market Size Expected to Maintain a CAGR of Over 20%

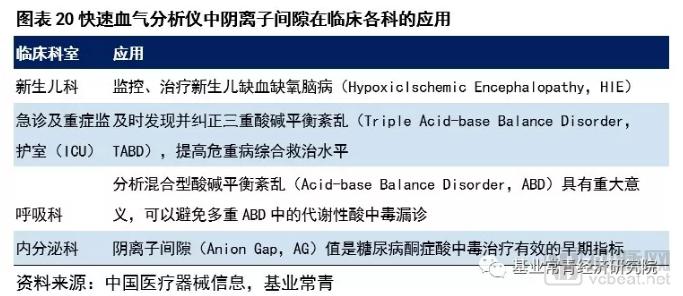

Blood gas analysis evaluates a patient’s respiratory, oxygenation, and acid-base balance status by analyzing the levels of O2 and CO2 in the blood. Electrolyte analysis assesses acute and potential changes in the internal environment related to acid-base balance and gas exchange by measuring ions such as K+, Na+, and Cl-.

Critically ill patients across various departments may develop acid-base balance disorders (ABD) due to individual factors. Severe ABD can damage vital organs and may even be fatal. Therefore, blood gas and electrolyte analysis serves as a critical indicator for the emergency treatment and monitoring of patients, making it indispensable in settings such as emergency rooms, operating rooms, intensive care units, and respiratory departments.

In July 2018, the Bureau of Medical Administration and Hospital Management under the National Health Commission issued the "Notice on Further Enhancing Trauma Care Capabilities," requiring hospitals at Level II and above to establish "Five Major Medical Centers." The notice also specified a mandatory list of equipment configurations for these medical centers, explicitly highlighting the requirement for blood gas analyzers. It mandated that each center department be equipped with at least one unit. Consequently, the market for point-of-care testing (POCT) blood gas analyzers is expected to sustain rapid growth.

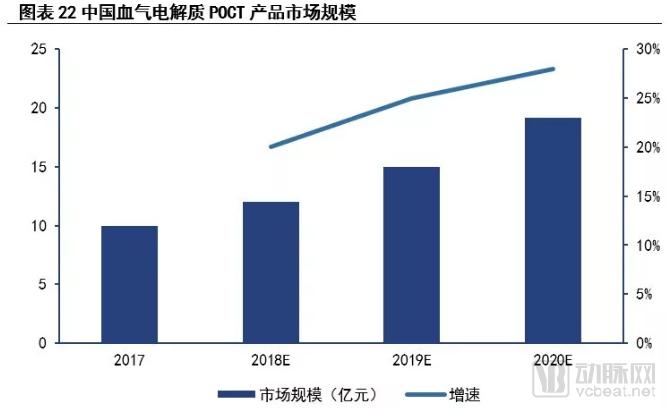

In 2017, the market size of blood gas/electrolyte analyzers in China was approximately RMB 1 billion. With the implementation of national policies in emergency centers, and according to the "China Medical Device Industry Development Report (2017)," it is expected that the market growth rate will maintain a compound annual growth rate of around 25%. It is projected that by 2020, the market size could reach approximately RMB 2 billion.

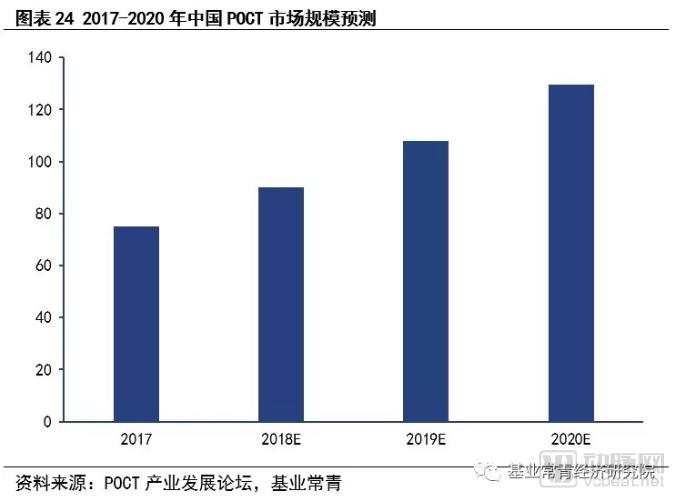

2.4 The overall market size of POCT is expected to maintain a compound annual growth rate (CAGR) of over 20%, and is projected to exceed RMB 12.9 billion by 2020

First, there is a rigid demand for point-of-care testing (POCT) in hospital emergency departments, operating rooms, and other critical settings. Second, the large population of patients with chronic diseases such as diabetes has generated a need for POCT to support daily monitoring. Furthermore, healthcare reform policies continue to promote the development of primary care. Given that primary healthcare institutions still need to improve their basic infrastructure and the professional competence of their staff, there is a practical demand for diagnostic equipment and clinical care models in these settings.

Based on incomplete statistics, we have conducted market size estimation and calculation with a focus on blood gas/electrolyte analysis, diabetes testing, and cardiac marker testing. According to the statistics and forecasts of the domestic POCT market size, the industry has entered a fast-track development phase, and the market size is expected to exceed RMB 12.9 billion by 2020, with a compound annual growth rate of approximately 20%.

3.1 Policy Support for POCT Upgrades: Healthcare Reform Accelerates Demand Expansion for Domestically Produced POCT Products

In 2016, the Chinese government issued the Guiding Opinions on Promoting the Healthy Development of the Pharmaceutical Industry, vigorously promoting the further development of POCT products toward quantitative analysis. In 2017, the state introduced the Three-Year Action Plan for Enhancing the Core Competitiveness of the Manufacturing Industry (2018–2020), which specifically mentioned support for the upgrading and quality improvement of high-precision point-of-care testing systems.

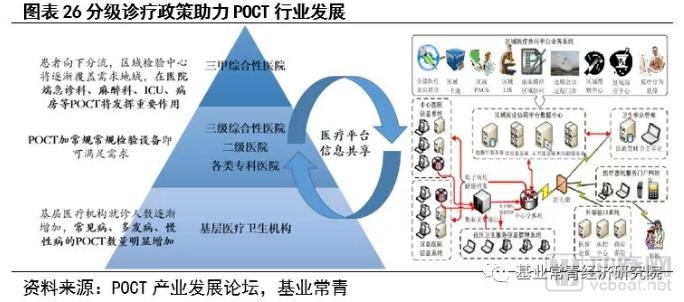

With the implementation of the tiered diagnosis and treatment policy, domestically produced point-of-care testing (POCT) devices will gradually see increased adoption in emergency departments, anesthesiology, intensive care units (ICUs), and general wards of tertiary hospitals, as well as in the markets for common and chronic diseases at primary healthcare institutions (secondary hospitals and below). Under the tiered diagnosis and treatment framework, regional laboratory centers will play an increasingly significant role as patient flow is redistributed. Large-scale laboratory platforms in tertiary hospitals will progressively shift toward clinical POCT-oriented models. Meanwhile, primary healthcare institutions (secondary hospitals and below) will experience a surge in patient visits, driving sustained growth in the volume of POCT products used for diagnosing common and frequently occurring conditions. Furthermore, the integration of POCT with internet technologies will enable cloud-based data management, accelerate the upgrading of healthcare service models, and facilitate the gradual establishment of big data platforms in healthcare.

3.2 Foreign enterprises hold a 45% market share in the domestic market, while Chinese companies lead in certain niche segments

According to incomplete statistics from various companies in the POCT industry in 2015, foreign enterprises accounted for half of the Chinese market. Domestic companies are expected to benefit from the trend of market growth, gradually stabilizing and expanding their market share. The three international diagnostic giants—Roche, Johnson & Johnson, and Abbott—held a combined market share of approximately 45%. A-share listed companies Sinocare, Wondfo, and Getein Biotech achieved a market share of about 20% by leveraging competitive advantages in specific fields. Well-known non-listed companies with deep industry roots, such as Beijing Yicheng and Realy Bio-Tech, accounted for approximately 10% of the market.

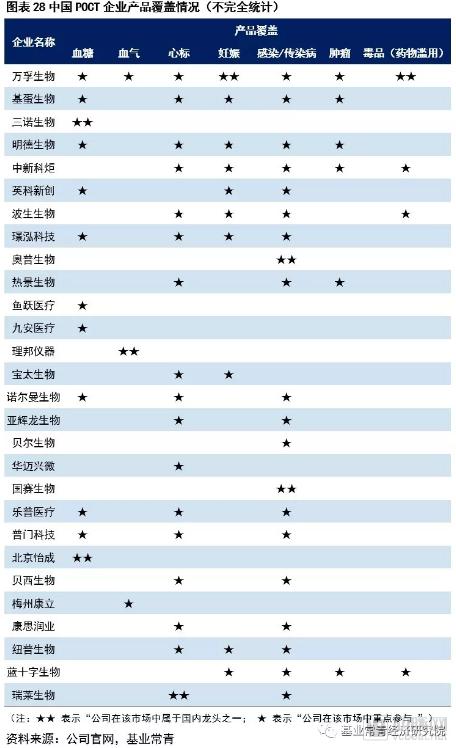

According to incomplete statistics on companies in China’s POCT industry, more than 65 domestic companies are engaged in the production of POCT products. Domestic POCT manufacturers have established a presence in high-growth segments such as cardiac markers, blood glucose monitoring, and blood gas and electrolyte analysis, while also actively entering frontier areas such as tumor detection.

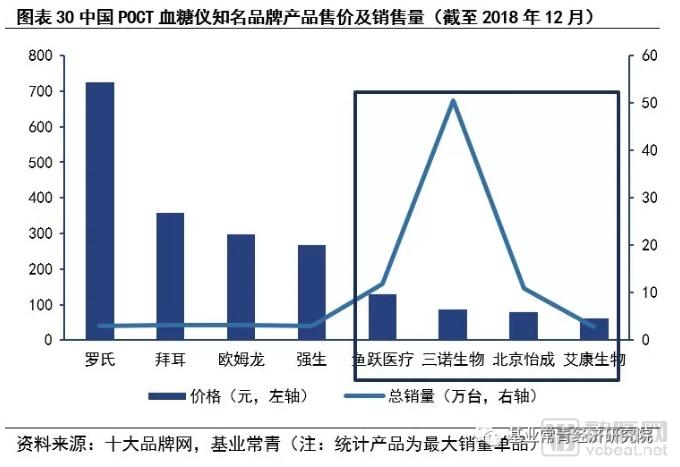

Taking the field of diabetes as an example, the "Guidelines for the Prevention and Treatment of Type 2 Diabetes in China (2017 Edition)" specifically highlights "blood glucose monitoring," emphasizing its critical role in diabetes management. Therefore, efficient and rapid confirmation of intraday blood glucose fluctuations is necessary to ensure effective control rates among patients with diabetes. Statistics on well-known domestic and international blood glucose meter brands indicate that Chinese-made products generally meet the testing needs of diabetic patients in terms of performance, and Chinese-made POCT blood glucose meters offer significant price advantages.

POCT glucose meters designed for home and individual use exhibit significant price sensitivity, with low-price strategies driving continuous market share expansion. Statistics on the listed prices and sales volumes of POCT glucose meters from eight major domestic and international brands show that the lowest unit price for foreign-brand glucose meters was RMB 268, while the highest was RMB 724. As of December 2018, the average sales volume per product across four major foreign brands stood at 30,600 units. In contrast, the lowest unit price for domestically produced glucose meters was RMB 62, and the highest was RMB 129. Among these, Sinocare, Yuwell Medical, Beijing Yicheng, and ACON Biosciences reported sales volumes of 505,000 units, 118,000 units, 108,000 units, and 27,000 units, respectively.

With the implementation of supportive policies, domestically produced POCT products will accelerate their market penetration. Sub-segments such as cardiac marker testing, blood glucose monitoring for diabetes, and blood gas/electrolyte testing exhibit high growth potential; therefore, leading enterprises with strategic layouts in these areas are recommended.

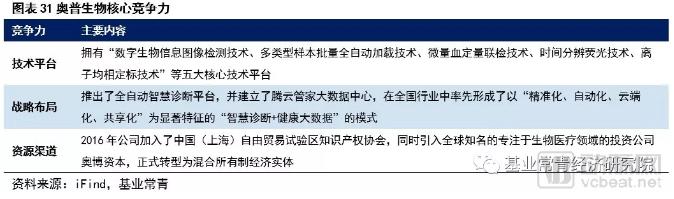

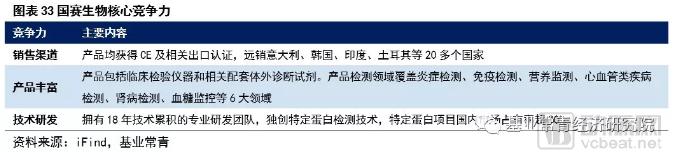

4.1 Aupubio: Entry of Globally Renowned Healthcare Capital, Pioneering the iPOCT Model

Shanghai Aupu Biopharmaceutical Co., Ltd. is located in the Modern Medical Device Park, East Zone of Zhangjiang Hi-Tech Park. It is a national high-tech enterprise specializing in intelligent medical diagnostics and health big data information. Led by its founder, Xu Jianxin, the Aupu innovation team officially entered the Zhangjiang Torch Pioneer Park for incubation in 2001. The company has undergone a transformation from distribution to R&D, and further to independent innovation, with cumulative tax contributions exceeding RMB 100 million.

1) Possesses five core technology platforms: “Digital Bioinformatics Image Detection Technology,” “Fully Automated Batch Loading Technology for Multi-Type Samples,” “Quantitative Combined Testing Technology for Micro-Volume Blood,” “Time-Resolved Fluorescence Technology,” and “Ion Homogeneous Calibration Technology.” 2) Pioneered in China’s industry the “Smart Diagnostics + Health Big Data” model, characterized by “precision, automation, cloud integration, and sharing.” 3) Introduced OrbiMed, a globally renowned investment firm specializing in the biomedical sector, and officially transitioned to a mixed-ownership structure.

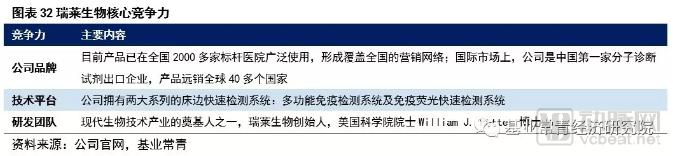

4.2 Rayleigh Biotech: Led by a Member of the U.S. National Academy of Sciences, China’s First Exporter of Molecular Diagnostic Reagents

Ruilai Bioengineering (Shenzhen) Co., Ltd. was established in 2001, with its basic R&D center located in Silicon Valley, California, USA, and its Asia-Pacific headquarters in Shenzhen. The company is primarily engaged in the research and development, production, and sales of POCT rapid diagnostic reagents and supporting diagnostic instruments. Its testing portfolio includes series for rapid detection of cardiovascular diseases, acute kidney injury, and inflammatory responses.

1) The company’s core team includes Dr. William J. Rutter, founder of Reilai Biology, a member of the U.S. National Academy of Sciences and one of the pioneers of the modern biotechnology industry. 2) The company offers two major series of point-of-care rapid testing systems: a multiplex immunoassay system and an immunofluorescence rapid testing system.

4.3 Guosai Biology: Proprietary Specific Protein Detection Technology, with Over 30% Market Share in the Domestic Specific Protein Testing Segment

Shenzhen Guosai Biotechnology Co., Ltd. was founded in 1999. Since its inception, Guosai has been dedicated to the research and development, manufacturing, and sales of products in the biotechnology field, including clinical laboratory instruments and related supporting in vitro diagnostic reagents.

1) As a national and Shenzhen-based high-tech enterprise, Guosai has consistently maintained first-class R&D capabilities and technical expertise in the field of specific protein testing. Guosai pioneered the establishment of stringent testing standards for specific proteins in China and has continuously advanced its technological proficiency in this domain. 2) As a leading enterprise in China’s specific protein testing sector, Guosai Biotech has conducted pioneering research on “whole blood testing,” “capillary blood testing,” and “one-step methods” for specific proteins. Furthermore, it has implemented comprehensive strategic deployments across the IVD industry, achieving multi-sector coverage of its product portfolio.

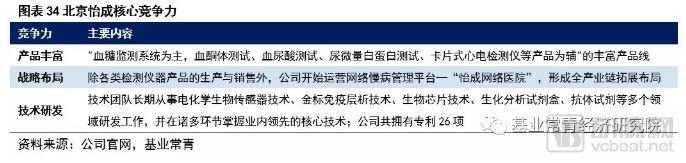

4.4 Beijing Yicheng: An Enterprise Supported by the "863" Program, Building a Network-Based Chronic Disease Management Platform

Beijing Yicheng Bioelectronics Technology Co., Ltd. was established in 1993. The company’s core business involves the research and development, manufacturing, and sales of rapid in vitro diagnostic products for diabetes and its complications (including instruments and in vitro diagnostic reagents), as well as the provision of related comprehensive personal health management services.

1) The Company is a renowned Chinese manufacturer of blood glucose meters, a National High-Tech Enterprise, a Zhongguancun High-Tech Enterprise, an enterprise supported by the National High-Tech Research and Development Program (“863” Program), and a specialized manufacturer in the field of medical rapid diagnostics in China. 2) It has built a diversified product portfolio centered on blood glucose monitoring systems, complemented by products such as blood ketone tests, blood uric acid tests, urinary microalbumin tests, and card-style ECG monitors. 3) With many years of deep industry engagement, the Company’s team possesses extensive R&D experience and has obtained 26 invention patents.

(1) Policy Risk: The industry is significantly influenced by policy, and the molecular diagnostics sector, as an emerging diagnostic technology, faces uncertainties in the regulatory landscape. Although the promotion of precision medicine policies has bolstered industry development and accelerated the domestic substitution of high-end medical instruments, the implementation of these policies in top-tier (Grade A tertiary) hospitals may encounter certain challenges due to their stringent quality requirements for medical equipment.

(2) Industry development falling short of expectations: The production technology barriers for upstream raw materials are relatively high, with domestic companies primarily relying on imports. It is difficult to break through patent barriers through independent innovation, and the process of domestic substitution may fall short of expectations. Market penetration still needs to be improved, posing a risk that future market performance may not meet expectations.

(3) Operational Risks: Although companies in the industry are high-tech enterprises, the technical barriers for POCT instruments and reagents are relatively low. Except for high-end novel POCT instruments, domestic production has been basically achieved. The company faces significant competitive risks and needs to proactively align with future market development trends, which entails considerable uncertainty.