Whale Intelligence | 2018 China Healthcare Venture Capital Market Analysis

Editor’s Note: This article is excerpted from “Jingzhun Research Institute | 2018 White Paper on Venture Capital in China’s New Economy,” republished with authorization by VCBeat.

Looking back at 2018, the establishment of the National Healthcare Security Administration, the National Health Commission, and the National Medical Products Administration marked the beginning of healthcare reforms in China. The listings of Ping An Good Doctor and Innovent Biologics on the Hong Kong Stock Exchange, Mindray Medical’s listing on the A-share market, and Blue Sail Medical’s acquisition of Biosensors International for RMB 1.9 billion pushed total investment and financing in the healthcare industry to new highs. As a typical counter-cyclical sector, the healthcare industry is expected to remain one of the most watched investment areas during the “capital winter” in 2019. Which sub-sectors will continue to be at the forefront of investment trends? What industry development trends deserve attention?

This excerpt is from the “VBInsight | 2018 White Paper on Venture Capital and Private Equity in China’s New Economy,” which provides a detailed analysis of investment and financing activities in the healthcare industry in 2018, with a focus on key subsectors. For further insights, please contact analyst Liu Jiaying (WeChat ID: liujiaying3008).

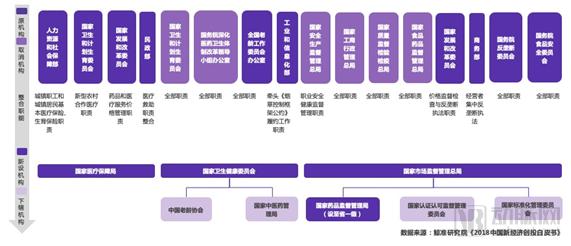

1.1 Major Institutional Reforms by the State Council: Restructuring of Functions for the National Healthcare Security Administration, the National Health Commission, and the National Medical Products Administration

1.2 Multi-party Collaboration Drives Industry Growth, as Healthcare and Pharmaceutical Reforms Continue to Deepen

Policy-Driven Initiatives: Reform of the healthcare regulatory organizational structure, with the successive establishment of the National Healthcare Security Administration (NHSA), the National Health Commission (NHC), and the National Medical Products Administration (NMPA); priority review for innovative drugs and medical devices with significant clinical value; implementation of volume-based procurement policies to further enforce consistency evaluation; encouragement of private healthcare provision and allowance for physicians to practice at multiple institutions.

Capital Empowerment: Capital support facilitates the research and development (R&D) of new products, enhances corporate R&D expenditure capacity, and provides long-term, reliable financial assurance for strengthening a company’s long-term industry competitiveness. Leveraging capital strength, healthcare enterprises achieve upstream and downstream integration through investments and mergers and acquisitions (M&A), enabling rapid expansion and the concentration of resources toward high-end, sophisticated, and cutting-edge development.

Technological Advancements: Rapid progress in precision medicine fields such as genomics and proteomics has led to the development of targeted therapeutic drugs and methods for specific disease subtypes. Meanwhile, high-tech innovations represented by big data, information technology, and artificial intelligence are providing new tools and platforms for the growth of the healthcare industry.

Consumption Upgrade: As residents’ consumption levels rise, demand for consumer-oriented healthcare continues to grow, thereby driving the development of specialized consumer-focused medical disciplines and other high-end, premium medical services. People increasingly desire convenient experiences in seeking medical care and purchasing medications, along with personalized disease prevention and treatment plans, spurring numerous innovative products and service models in the digital health industry.

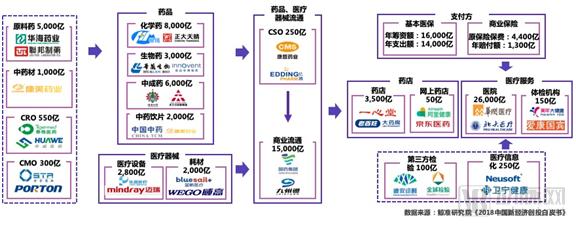

1.4 Coordinated Development Across the Upstream, Midstream, and Downstream Sectors; Large Market Size for Hospitals, Pharmaceuticals, and Commercial Distribution

1.4 Industry Trends: Policy and Technology Jointly Drive the Healthcare Sector Toward High-End Maturity

Pharmaceuticals: With the implementation of volume-based procurement for generic drugs, domestic generic drug prices in China will see significant reductions. Meanwhile, a series of key policies, including expedited new drug approvals and consistency evaluations for pharmaceutical products, are being intensively rolled out. These measures will enhance the quality of Chinese-made drugs over the long term, encourage pharmaceutical innovation, promote industrial upgrading and transformation, and accelerate the integration of China’s domestic pharmaceutical market with international standards.

Medical Devices: Currently, import substitution in China’s medical device industry is limited to a few high-end segments. In recent years, the government has launched multiple special programs to provide financial support for R&D of medical devices, while accelerating the approval process for innovative devices. Furthermore, the government has implemented concrete measures to encourage the procurement of high-quality domestically produced medical devices. The industry is inevitably poised to advance toward the high-end sector.

Medical Services: Currently, medical services are primarily provided by public healthcare institutions. With the introduction of multiple national policies encouraging private investment in healthcare, the proportion of private hospitals is expected to increase significantly in the future. Healthcare institutions with strong medical and consumer-oriented attributes will have substantial growth potential, while specialized clinics and high-end premium services will also enter a golden period of development.

Digital Healthcare: As the level of healthcare informatization continues to improve and policies increasingly favor primary care, the market potential for AI- and big data-driven applications, such as intelligent diagnostics, will gradually be unlocked within primary healthcare institutions. Furthermore, the digital healthcare industry will expand its service scope to include B-end clients such as government agencies and insurance companies.

2. In 2018, the number of industry financing deals decreased, while the average amount per deal rose rapidly

From the perspective of overall investment and financing conditions, the amount of financing in the healthcare industry has continued to rise: the total domestic financing in the healthcare industry was RMB 21.2 billion in 2014, and the total financing reached RMB 78.7 billion in 2018. Pharmaceuticals and medical services were the two fastest-growing sectors, reaching RMB 34.1 billion and RMB 31.4 billion, respectively, in 2018.

Regarding annual financing trends, investment enthusiasm in the healthcare sector gradually increased after 2014, stabilizing in 2016 and 2017 with minimal fluctuations in the number of deals. In 2018, the number of financing events dropped significantly to 824. In terms of average deal size, it remained relatively stable at approximately RMB 40 million from 2014 to 2017. However, in 2018, the average single financing amount surged to RMB 95 million, representing an increase of around 130% compared to previous years.

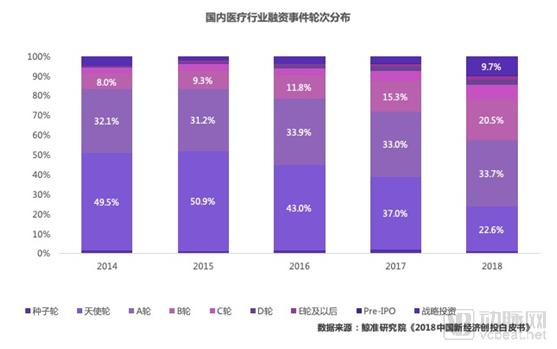

2.2 The proportion of pre-Series A investments has sharply decreased, while the proportions of M&A and strategic investments have risen; the proportion of investments exceeding RMB 100 million has increased significantly

From the perspective of financing rounds, the proportion of angel-round financing events in the industry has sharply decreased, dropping continuously from 49.5% in 2015 to 22.6% in 2018. Meanwhile, the share of strategic investments in the industry rose from 4.6% in 2014 to 9.7% in 2018. This trend reflects the maturation of the healthcare sector, with a gradual decline in early-stage projects and investment increasingly concentrated on leading companies, while the importance of mergers and acquisitions (M&A) and strategic investments continues to grow.

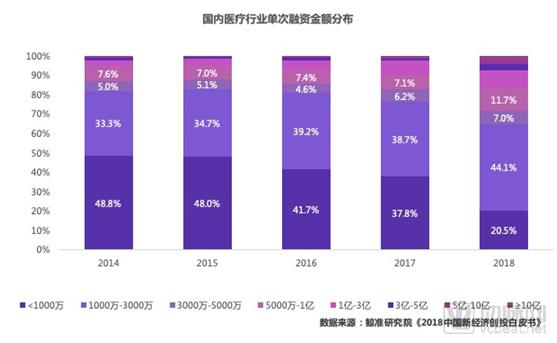

In terms of the amount raised per financing round, the proportion of investments under RMB 10 million has declined significantly. In 2014, 48.8% of financing deals were valued at less than RMB 10 million, whereas this figure dropped to just 20.5% in 2018. Meanwhile, the share of investments exceeding RMB 100 million rose from 5.3% in 2014 to 16.7% in 2018. Investment activities have increasingly concentrated on larger-scale, high-quality targets characterized by industry innovation.

2.3 Provinces and cities such as Beijing, Shanghai, and Guangdong exhibit active investment, with industrial clusters beginning to take shape

From the perspective of geographical distribution, healthcare industry financing events in the first three quarters of 2018 mainly occurred in provinces and municipalities such as Beijing, Shanghai, and Guangdong. Beijing ranked first nationwide with 194 cases; followed by Shanghai with 160 cases; Guangdong, Jiangsu, and Zhejiang had 117, 104, and 103 cases, respectively.

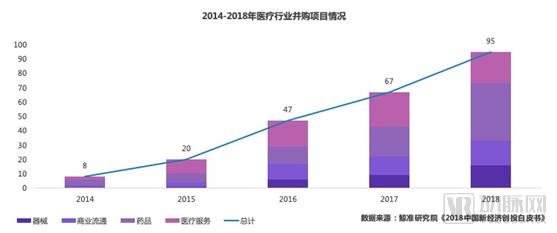

2.4 The Number of M&A Projects Increases Year by Year, Driving the Healthcare Industry Toward High-End Development

There is currently a certain gap in the product and service levels of China’s healthcare industry. Drawing on the development trajectories of developed countries, industrial consolidation through mergers and acquisitions (M&A) has become an inevitable trend for sector growth. In recent years, M&A activity in China’s healthcare industry has grown rapidly; the number of healthcare M&A deals in 2018 was ten times higher than that five years earlier, indicating a significant acceleration in the trend of industrial consolidation. The primary reasons are as follows:

From a policy perspective, the State Council reformed medical regulatory agencies in 2018, establishing a relatively comprehensive policy and regulatory framework. A series of policies were implemented to encourage product innovation, promote industrial upgrading, and accelerate the integration of China’s domestic pharmaceutical and medical device markets with international standards, thereby enhancing the long-term quality of domestically produced services and products.

From a corporate perspective, industry innovation and premiumization have become inevitable trends for development. Companies are leveraging mergers and acquisitions to integrate key segments of the industrial chain, thereby transforming their core businesses toward higher value-added areas. For instance, Blue Sail Medical, a leading manufacturer of low-value consumables, achieved rapid advancement by acquiring Biosensors International, a global giant in cardiac stents, successfully transitioning into China’s leading enterprise in high-end implantable devices.

2.5 Listed Companies in the Healthcare Sector Are Widely Favored by the Market, with a Significant Increase in Average Fundraising Amounts

As a pivotal year for shifts in the style of China’s A-share market, 2018 saw future opportunities increasingly focused on the “new economy.” The healthcare industry, being critical to national welfare and people’s livelihoods, exhibited strong certainty. In 2018, the overall number of initial public offerings (IPOs) in the A-share market declined significantly compared with the previous year, leading to a substantial drop in the number of healthcare IPOs as well. However, in terms of capital raised, the average amount per healthcare company reached RMB 1.324 billion in 2018, up sharply from RMB 427 million in 2017—a surge of 210%—reflecting broad recognition by the A-share market.

Bolstered by strong policy support in recent years, the healthcare industry has witnessed rapid development, with leading companies across various subsectors choosing to list on China’s A-share market, such as CRO giant WuXi AppTec and medical device giant Mindray Medical. Currently, the pharmaceutical industry stands at a critical juncture, with a new round of consolidation already underway. In the future, high-quality enterprises within the sector will attract widespread attention from the A-share market.

2.6 The Healthcare Industry Is Experiencing Rapid Growth, with Innovative Companies Seeking Listings on the HKEX and US Stock Markets

Given the relatively stringent performance requirements for listing on China’s A-share market, innovative healthcare companies—typically in their early stages with few mature products and high R&D expenditure ratios—face significant hurdles. In recent years, the Chinese government has introduced multiple policies to encourage innovation in the pharmaceutical industry, spurring rapid development of the mainland China healthcare sector and a substantial increase in corporate financing needs. Meanwhile, the Hong Kong and U.S. securities markets offer clear, transparent listing frameworks and predictable approval timelines.

Consequently, healthcare companies are increasingly inclined to pursue listings in the United States and Hong Kong. On the other hand, the market-capitalization-weighted P/E ratio for healthcare companies’ initial public offerings (IPOs) in Hong Kong is higher than that in mainland China, indicating that these companies can achieve higher valuations when going public in Hong Kong. Meanwhile, in early 2018, the Hong Kong Stock Exchange introduced new regulations allowing biotechnology companies without revenue or profitability to apply for listing in Hong Kong. As a result, more outstanding domestic innovative biopharmaceutical companies are expected to seek IPO financing in the future.

2.7 High-tech niche sectors, represented by intelligent diagnostics, have attracted widespread attention from the investment market

With the advancement of artificial intelligence (AI) and big data in healthcare, intelligent diagnostic systems trained on large datasets are poised to become the most rapidly deployed AI applications in the medical field. Data indicate that nearly 100 companies in China are developing AI-powered diagnostic products related to medical imaging, with a focus on pulmonary nodule detection and fundus image screening. Currently, most intelligent diagnostic products have not yet been fully implemented in clinical practice, and their potential for application in areas such as neurological disorders remains to be further explored.

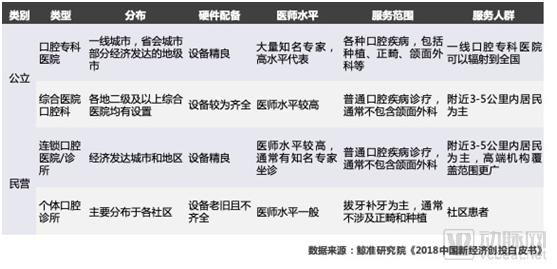

3.1 Heat of the Oral Diagnosis and Treatment Industry

As residents’ health awareness and disposable income continue to rise, the demand for dental diagnosis and treatment services has been steadily increasing. Moreover, due to advantages such as relatively low capital investment, shorter payback periods, and ease of scalable replication, the dental care sector has become one of the most sought-after investment areas in recent years. Dental diagnosis and treatment primarily refer to medical institutions providing consumers with services such as diagnosis and treatment of oral diseases and oral healthcare. By specialty, it can be categorized into endodontics, oral and maxillofacial surgery, prosthodontics, orthodontics, pediatric dentistry, periodontics, and others.

3.2 Market Capacity of the Dental Diagnosis and Treatment Sector

Within the dental industry, there are two primary models for data statistics: one based on outpatient visits at general hospitals, and the other based on the number of first-visit patients, taking into account that certain dental treatments often require multiple sessions over an extended period.

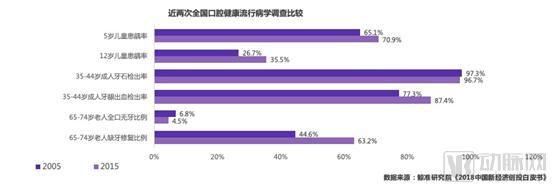

Since the National Health Commission has compiled statistics on the number of outpatient visits to dental clinics but not on first-visit data, the following estimation is based on the total number of outpatient visits: According to this metric, China’s total number of dental outpatient visits reached 250 million in 2016.

In 2016, the total medical revenue of stomatological hospitals in China reached RMB 14.44 billion, with 32 million outpatient and emergency visits and 1.4 million inpatient admissions. Excluding inpatient services, the average revenue per outpatient visit at stomatological hospitals was approximately RMB 450. Due to differences in case complexity and physician expertise compared to specialized stomatological hospitals, the average cost per visit at the dental departments of general hospitals was set at 80% of that at stomatological hospitals, i.e., RMB 360 per visit. Although some high-end clinics had higher average costs per visit, a large number of private clinics offered only low-cost services such as tooth extraction, prosthesis placement, and fillings. Therefore, the average cost per visit at chain or individual private clinics was set at 90% of that at the dental departments of general hospitals, i.e., RMB 324 per visit. Based on these calculations, the size of China’s dental treatment market in 2016 was estimated at RMB 86.4 billion.

3.2 Oral Care Diagnosis and Treatment Industry Chain

In the dental care industry chain, the upstream sector comprises the medical equipment, dental materials, and pharmaceutical industries, while the downstream sector directly serves dental patients. The upstream medical equipment industry primarily provides dental treatment devices, basic diagnostic equipment, and other apparatuses, including dental forceps, dental handpieces, and dental chairs. The dental materials industry mainly supplies materials for dentures, dental implants, and orthodontics. The pharmaceutical segment primarily includes anesthetics and anti-infective agents, accounting for a relatively small proportion.

3.3 Competitive Factors in the Dental Care Market

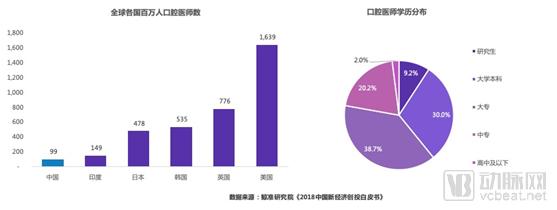

Talent: Significant Shortage of Dentists

Talent is one of the most critical factors in the dental healthcare services sector. Outstanding dentists wield significant market appeal; beyond the individual draw of renowned experts, the strength of an expert team directly reflects the competitiveness of private dental institutions. In recent years, major dental chain organizations have continuously strengthened their talent development mechanisms to secure personnel for sustained growth and future expansion.

In 2016, China had 136,000 licensed dentists, equating to 99 dentists (excluding assistant licensed dentists) per million population, a figure that lags significantly behind other countries. In terms of educational attainment, only 39.2% of licensed dentists held a bachelor’s degree or higher, while 22.2% had a secondary vocational school, high school, or lower level of education. Geographically, approximately 53.6% of dentists (including assistant licensed dentists) were located in the eastern region, with only 22.2% distributed across the western region.

Management: Chain Operations Require Enhanced Management Capabilities

Founders of private dental clinics are mostly dentists. Chain operations still require the following management capabilities: store expansion and financial balance management. For example, opening a new clinic with approximately 10 dental chairs and an area of 800-1,000 square meters requires an initial investment of 5-8 million yuan, and it generally achieves monthly profitability within one year of operation.

As competition within the industry intensifies, some chain enterprises have pursued aggressive expansion, resulting in excessively high asset-liability ratios and necessitating vigilance against the risk of capital chain rupture. Other Management Areas: As enterprises scale up, the importance of management becomes increasingly evident. Professional management teams are required for establishing various rules and regulations, medical quality management, talent acquisition, performance accounting, and the development of promotion models and marketing strategies.

Brand: Dental chains emphasize brand control and predominantly adopt a direct-operated model.

Competitive factors for healthcare institutions include talent strength, service quality, environmental facilities, pricing, and location, with brand serving as a comprehensive reflection of these elements. Brand value gradually emerges only when an institution’s competitive factors are maintained at high levels and accumulated over an extended period.

a. Brand Appeal: Consumers have limited understanding of dental care services and struggle to differentiate among the numerous dental institutions available in the market. Well-known dental brands can attract patients, thereby fostering long-term trust, which facilitates word-of-mouth accumulation and expands the consumer base.

b. Employee Cohesion: A strong brand image helps enhance employees’ sense of responsibility and self-confidence, thereby facilitating talent attraction and recruitment for dental institutions amid the current shortage of high-quality dentists.

c. Business Model: Dental chains predominantly adopt a direct-operation model. While franchising is an important avenue for chain expansion—typically offering shorter payback periods, lower risks, and established brand reputation compared to building new standalone clinics—it presents significant management challenges. Inconsistencies in medical quality, pricing, service, or operational promotion relative to the overall brand strategy can severely damage the group’s brand image. Consequently, most well-known dental chains currently favor the direct-operation model.

3.4 Operational Analysis of Dental Care Providers

Compared with data from listed and NEEQ-quoted companies, the average gross profit margin for dental care services is approximately 40%-50%, while the labor cost ratio stands at around 35%-45%. Topchoice Medical primarily operates dental hospitals, with each single store generating annual revenue exceeding RMB 40 million, whereas other branded chain clinics report annual revenues of approximately RMB 5 million. As Topchoice Medical’s hospitals adopt quasi-public naming conventions in the format of “Location Name + Dental Hospital,” they benefit from strong brand recognition, resulting in a sales expense ratio of only 1.0%, significantly lower than the industry average of 15%-20%.

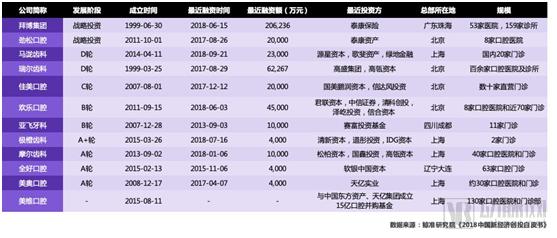

3.5 Investment and Financing Analysis of Oral Diagnosis and Treatment

Listing and Quotation Stage: Currently, Topchoice Medical is the only A-share listed company in the dental care industry. Companies quoted on the National Equities Exchange and Quotations (NEEQ) include Little White Rabbit Dental, Tongbu Dental, Zhengfu Dental, Keen Dental, Bairui Dental, and Huamei Dental, totaling six firms. In addition, Lantian Dental applied for NEEQ quotation on August 30, 2018.

Other Stages: According to the data, Bybo Group, Malo Dental, and Happy Oral Care all secured substantial financing after June of this year, indicating that the industry as a whole is in a phase characterized by strong investor enthusiasm and intensifying competition.

3.6 High-Quality Targets in Dental Diagnosis and Treatment

3.7 Trends and Opportunities in the Dental Care Industry

Industry Trends:

a. Accelerated Expansion of Dental Chains: In recent years, the dental industry has attracted increasing attention. Compared with general hospitals, dental hospitals offer advantages such as lower capital investment, shorter payback periods, higher profit margins, and less impact from medical insurance quotas. Major institutions are accelerating their expansion through self-funded capital or external financing, and competition in economically developed cities is expected to intensify in the future.

b. Industry chain integration: Dental clinics such as Huamei Dental have gradually established dental prosthesis manufacturing plants and medical device trading companies, forming a complete industry chain; meanwhile, upstream dental prosthesis manufacturers like Bairui Dental have also begun opening dental clinics, extending their business scope downstream.

c. Technological Advancements and Service Enhancements: The application of technologies such as intraoral scanning, cone-beam CT, and CAD/CAM has significantly improved diagnostic and treatment precision, thereby enhancing clinical outcomes. Techniques like clear aligner therapy and immediate implant placement have improved patient experience, with their adoption rates expected to continue rising in the future.

Investment Opportunities:

a. Regional Brands: Geographic expansion has always been one of the major challenges in the dental industry. Due to the relatively high customer stickiness, dominant regional brands often hold a competitive advantage when facing external competition.

b. Specialty Advantages: In economically developed cities, competition in the dental industry is extremely intense. Institutions that focus on specific niche areas are more likely to stand out, and a differentiated brand image is more effective in attracting potential patients and converting them into long-term clients. Examples include Jicheng Dental and Qingmiao Children's Dentistry, which specialize in pediatric dentistry; Malo Clinic, which focuses on dental implants; and Side Sunshine, which specializes in orthodontics.