DRG Payment System Construction: International Experience in Cost Data

Globally, the development of Diagnosis-Related Group (DRG) systems, along with accurate case grouping and weight determination, relies on two foundational types of data: first, clinical information contained in medical record face sheets, including diagnosis codes and procedure codes; and second, cost information derived from medical records. Based on clinical information, each case is assigned to a specific DRG group. Using DRG cost data, the homogeneity of different DRG groups is assessed; if homogeneity is insufficient, consideration is given to splitting them into separate groups. The previous column introduced clinical data related to medical record face sheets. This issue focuses on international experiences in the collection and analysis of cost data.

Columnist: Dr. Liu Zhichen, a senior DRG expert and postdoctoral fellow in Public Administration at Fudan University

Professional Profile: Postdoctoral Fellow at the Postdoctoral Mobile Station in Public Administration, Fudan University, and at the Postdoctoral Workstation of the Statistical Information Center, National Health and Family Planning Commission. Previously served as Director of Scientific Research Business Development at a listed domestic IT solutions and services provider. As the overall project lead, participated in a pilot project for DRG-based health insurance payment reform at the prefectural level in China. Assisted the city’s Healthcare Security Administration in designing the top-level framework for the citywide DRG payment system reform and implemented the supporting information technology systems.

I. The Relationship Between DRG Implementation and Cost Data

Under the traditional fee-for-service and global budget payment models, cost accounting was not a primary priority for hospitals. However, with the implementation of Diagnosis-Related Group (DRG)-based payment, all hospital services have shifted from generating incremental revenue to incurring incremental costs, making effective cost control increasingly critical. Without a robust accounting system, hospitals cannot determine whether they are operating at a profit or a loss under the DRG model. More importantly, a high-quality and accurate cost accounting system is the foundation for calculating precise relative weights. The accuracy of DRG relative weights significantly influences the effectiveness and fairness of the DRG payment system.

If the relative weight values are too high, it becomes difficult to incentivize hospitals to improve efficiency by enhancing treatment methods. Conversely, if the relative weight values are too low, hospitals may compromise medical quality to reduce healthcare costs. In light of these considerations, countries around the world have begun regularly collecting hospital cost accounting data following the implementation of Diagnosis-Related Groups (DRGs) to calculate and continuously update DRG weights.

At the 2017 China DRG Payment and Reimbursement Conference, Poul Erik Hansen, Deputy Director of the Danish National Institute for Public Health, explicitly stated in his speech, “The introduction of DRG Data and Cost Management in Denmark,” that when Denmark developed its Dk-DRG system in 1997 to reflect national characteristics, it primarily drew on the DRG systems of the U.S.-based 3M Company, Australia, the Nordic countries, and later Germany.

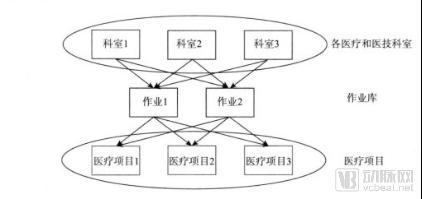

In summary, the Dk-DRG system primarily consists of “DRG grouping logic plus cost accounting.” This DRG system reflects both the clinical realities in Denmark and the cost structure of Danish hospitals (as shown in Figure 1). Similar to Denmark, the introduction of DRGs has led regulatory authorities in many European countries to gradually recognize the importance of cost accounting. Studies by Nathanson et al. (2009) indicate that high-quality cost accounting systems facilitate the development of DRG-based payment mechanisms. This underscores the critical role of cost accounting data within the DRG system.

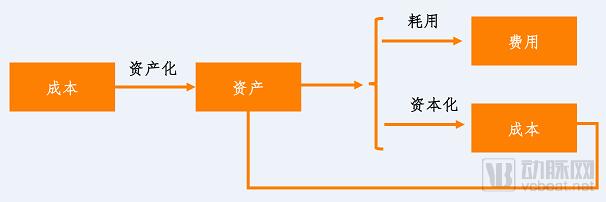

Figure 1: DRG Grouping Logic and Cost Accounting Constitute the DRG System

II. Origin and Definition of Hospital Cost Accounting

Research on hospital cost accounting in developed countries truly began in the 1950s. Initially, hospital cost accounting drew upon corporate cost accounting methods, establishing a volume-based cost accounting system in which indirect costs were allocated using the step-down allocation method.

However, in practical applications, it has been observed that cost accounting for medical services differs significantly from that in other industries. Relying solely on volume-based metrics distorts cost accounting information. Factors such as individual patient differences, disease categories, length of hospital stay, and disease severity all influence the amount of costs incurred. Consequently, a series of studies on hospital cost accounting have rapidly emerged.

Based on the theory of enterprise costs, the definition of hospital costs can be summarized as: the monetary expression of the value transferred from means of production consumed during medical activities and the value created by medical personnel for themselves. In other words, it is the total amount of funds expended by the hospital in its medical activities. The transferred value of means of production includes the consumption of pharmaceuticals, sanitary materials, low-value consumables, and other materials; the depreciation of fixed assets; the amortization of intangible assets; the provision for medical risk funds; and other values of embodied labor. The value created by medical personnel for themselves includes basic salaries, performance-based pay, social security contributions, welfare benefits, and other related expenses.

Hospital cost accounting refers to the process by which a hospital aggregates and allocates various expenditures incurred in its operational activities according to specific cost objects, thereby calculating total costs and unit costs. While hospital cost accounting possesses its own unique characteristics, it must also adhere to the general principles of cost accounting. The new "Hospital Financial System" explicitly stipulates that "cost accounting shall follow the principles of legality, reliability, relevance, periodic accounting, accrual basis, actual cost valuation, matching of revenues and expenses, consistency, and materiality."

Cost accounting objects in hospitals refer to the content reflected and monitored by cost accounting. Clearly defining these objects is of significant importance for determining cost accounting tasks, as well as for studying and applying cost accounting methods. In accordance with hospital operational management requirements, the cost accounting objects are total hospital costs and departmental costs. To meet the requirements for determining medical service prices, the cost accounting objects are item-level costs and disease-specific costs. To fulfill the requirement of controlling average charging levels, the cost accounting objects are cost per outpatient visit and cost per bed-day.

III. Differences Between Hospital Costs and Expenses

Costs and expenses are two accounting concepts that differ fundamentally in nature. On one hand, costs cannot be directly converted into expenses; they must first undergo "capitalization" as assets and then be recognized as expenses through the process of consumption (i.e., Cost → Asset → Expense). For instance, when an enterprise incurs expenditures to acquire equipment for its production and operational activities, these expenditures constitute the procurement cost of fixed assets. Once the equipment is installed, commissioned, and put into use, it is recognized as a fixed asset of the enterprise (Cost → Asset). If the equipment is used for product manufacturing, the depreciation charged on the fixed asset using an appropriate method each period is included in the production cost of the products (Asset → Cost). If the equipment is used for administrative purposes, the depreciation expense accrued in each period is recorded as administrative expenses for that period (Asset → Expense).

On the other hand, expenses cannot be converted into costs; expenses represent consumption and lack object specificity. We must no longer be influenced by the erroneous notion that "expenses are included in costs," nor should we continue to assert that "the objectification of expenses constitutes cost."

For a long time, certain individuals have exploited the public’s misunderstanding of the relationship between costs and expenses, deliberately blurring the distinction between asset costs and expenses to manipulate profits at will and engage in financial fraud. Expenses are expenses, and costs are costs; costs can only be indirectly converted into expenses through “capitalization,” whereas expenses can never be converted into costs, whether directly or indirectly.

The relationship between the two is illustrated in Figure 2:

Figure 2. Relationship between Costs and Expenses

For hospitals, costs refer to the expenditures required to achieve objectives. The total cost of any objective, service, or plan encompasses financial resources, assets, and human resources. These expenditures or consumptions are premised on their ability to generate benefits. Among the necessary expenditures, those that yield relatively immediate benefits within the current period, such as salaries and rent, are termed expenses, also known as consumed costs. Other expenditures, from which benefits are recovered gradually over subsequent years, such as raw materials and machinery, are referred to as depreciable costs.

Hospital costs not only share characteristics with corporate costs but also possess unique features inherent to medical services, resulting in greater complexity. Furthermore, hospital accounting systems are less developed than those of enterprises, and the competence and diligence of hospital accounting personnel vary significantly. Consequently, the collection of cost data is still being refined. As a result, inpatient costs in the healthcare sector are predominantly reflected in the form of charges.

IV. Research History of Hospital Cost Accounting Methods

Larry K. Macdonald (1973) studied the Patient-specific Approach for calculating healthcare costs. By integrating actual cost information of medical services and using patients as the unit of cost accounting, this method calculates hospital costs in a “bottom-up” manner, with “production capacity” serving as the basis for cost allocation. This approach fully considers the characteristics of the healthcare industry by focusing primarily on major costs (institutional and labor costs) to simplify the calculation process. However, its drawback is that it fails to encompass all institutional resource expenses. Consequently, this method is difficult to widely promote as a standard approach across all departments in all hospitals; rather, it offers a conceptual framework for cost estimation rather than representing a novel methodology.

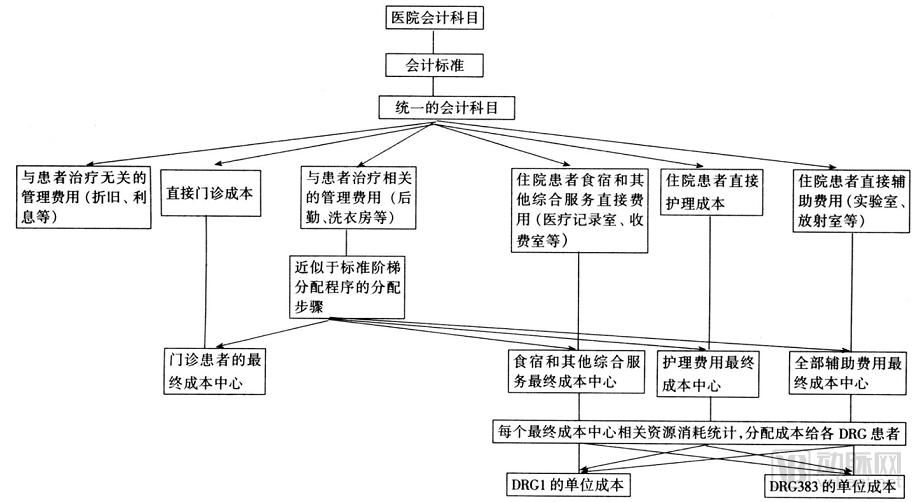

In 1976, the Health Services Research Center at Yale University developed a patient classification system for inpatients (Fetter et al., 1979), using patient case mix as the classification unit and naming it Diagnosis-Related Groups (DRGs). The original purpose of the developers was to monitor internal resource utilization within hospitals. They believed that DRGs could control for different types of patients within healthcare institutions, distinguishing cost variations across different treatment patterns and patient classifications; externally, DRGs could facilitate comparisons of per-unit resource consumption and treatment costs among different hospitals.

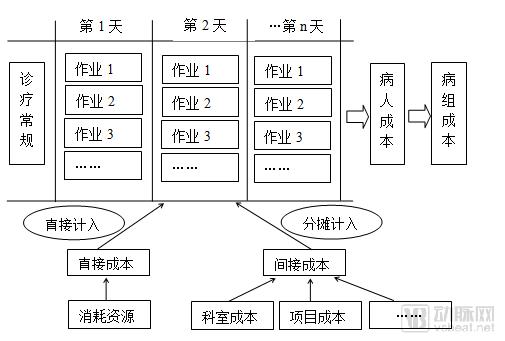

The detailed accounting process is shown in Figure 3, and the allocation of administrative expenses and DRG costs is presented in Figure 4. As illustrated in Figures 3 and 4, the hospital’s final cost centers are categorized into three: comprehensive services, nursing services, and auxiliary services. These cost centers align with the hospital’s responsibility centers, thereby facilitating accounting, management, and planning. The cost calculation process is completed in two stages based on different allocation criteria, which fully reflect the causal relationships in cost allocation. The standardized design of accounting subjects across hospitals ensures the integration between cost accounting and financial accounting, as well as the comparability of unit costs among different hospitals. This approach essentially encompasses all costs associated with inpatients, yielding more authentic cost accounting results. Calculating hospital service costs on a per-disease basis provides a bargaining tool for payers.

In the late 1970s, the aforementioned research findings were first piloted on a large scale in New Jersey, USA, serving as the foundation for the Prospective Payment System (PPS). In 1983, the U.S. Congress mandated the implementation of the DRG-based prospective payment system for all Medicare beneficiaries, after which many states attempted to extend its application to non-Medicare patients. Currently, DRGs have become the basis for global budgeting in some Western countries, Eastern Europe, and Australia.

Figure 3 Method for Determining Patient DRG Treatment Costs

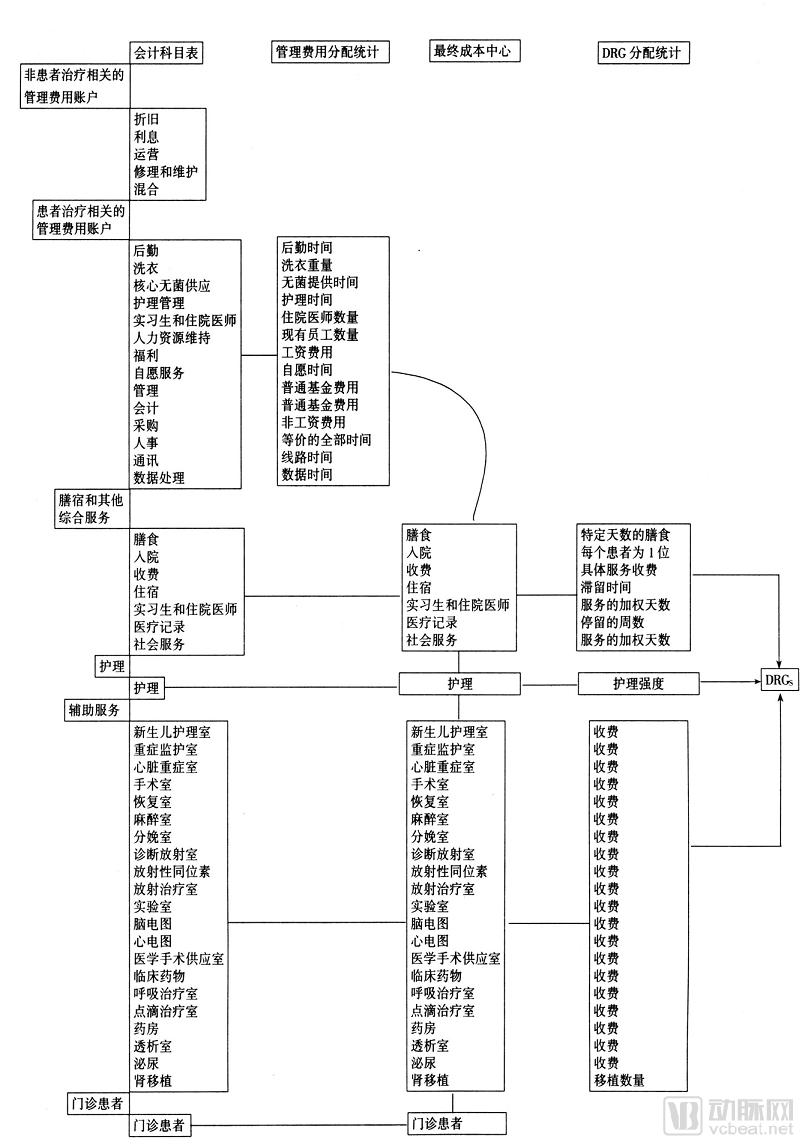

Figure 4 Hospital Chart of Accounts and Its Management Utilization and DRG Allocation Status

The United States uses Diagnosis-Related Groups (DRGs) to determine payment for Medicare acute inpatient cases. The payment standard is calculated using the following formula: DRG Case Payment Standard = Regional Rate × Relative Weight of the DRG to which the case belongs, where the relative weight is calculated using the cost-to-charge ratio method.

Cost-to-Charge Ratio Method. This method assumes that the ratio of costs to charges for each hospital cost center is fixed, and obtains the cost-to-charge ratio (CCR) for each cost center from the annual cost reports submitted by hospitals. In conducting cost accounting, this method adopts a standard rate approach (the standard rate for general hospitals consists of labor and non-labor components, which are derived after adjusting for the overall operational costs of hospitals in each city). It comprehensively considers factors such as regional wage differences, indirect medical education costs, disproportionate share payments, and outlier costs (the average cost of cases falling beyond three standard deviations from the mean charge for each DRG). By eliminating the impact of these differential factors, the method calculates the average charge per DRG, which is then divided by the national average charge standard per case to derive the weight factor.

The advantage of this calculation method is its relative simplicity and the ease of data acquisition (Data sources for Medicare’s CCR calculations: Cost data are primarily derived from the annual cost reports that Medicare requires each healthcare institution to submit. Costs can be allocated to each cost center but not to individual service items. Charge data are mainly sourced from the billing records of each cost center within each healthcare institution.). The limitation is that the CCR assumes a uniform markup ratio across all hospitals; it only accounts for variations between cost centers during measurement, ignoring patient-level differences, which results in lower accuracy.

Activity-Based Costing (ABC) is an advanced cost management philosophy and methodology that emerged in the United States during the 1970s and 1980s. The concept of activity accounting was first proposed by theoretical scholars in 1952. In the late 1980s, Professor Cooper from the University of Chicago and Professor Kaplan from Harvard University observed the widespread phenomenon of cost distortion in American industry. They proposed activity-based costing, which uses activities as the basis for cost calculation, thereby inheriting and further developing the theory and practice of Activity-Based Costing. Due to its significant advantages in disease-level cost accounting and in-depth analysis of cost drivers, ABC has been introduced into hospital management.

Activity-Based Costing (ABC) is a cost calculation and management method that dynamically tracks and reflects all activity processes involved in cost objects, in order to measure the costs of activities and cost objects, and to evaluate operational performance and resource utilization efficiency. The cost accounting of medical service items generally adopts the Activity-Based Costing model. Under ABC, "activities" specifically refer to medical and nursing services performed with patients as the primary focus, consuming certain resources to achieve the goal of disease diagnosis and treatment, such as surgery, ward rounds, consultations, intravenous infusion, and dressing changes.

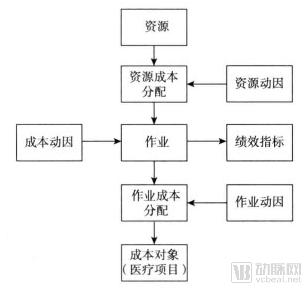

Unlike traditional cost management philosophies, the logical basis of Activity-Based Costing (ABC) is that production triggers activities, products consume activities, activities consume resources, and resource consumption generates costs. From the perspective of ABC, the provision of medical services is a dynamic process composed of a series of activities. Therefore, the primary step in cost calculation is to conduct an activity chain analysis. Medical services “consume” resources through “activities,” thereby shifting the focus of hospital cost management down to the activity level. By controlling and improving the activity chain, workflows are continuously optimized, costs are reduced, and ultimately, the effectiveness of hospital cost management is enhanced. Centered on activities, ABC allocates resource costs to activities based on resource consumption patterns, and then finally assigns costs to specific medical services according to the volume of activities consumed by these services (see Figures 5 and 6 for details).

Figure 5 Calculation Model of Activity-Based Costing in Hospitals

Figure 6. Project Cost Calculation Model Based on Activity-Based Costing

Accounting Process of Activity-Based Costing in Hospitals:

First, identify the activity centers. Initially, after analyzing the hospital’s daily operational processes, these processes are divided into several homogeneous activities. The classification of activities should encompass the hospital’s entire range of operational activities; however, the number of categories must be determined pragmatically. Blindly dividing activities without considering the hospital’s specific circumstances will increase the workload required for cost accounting, thereby demanding more human resources and effort. This increased workload will inevitably lead to a higher error rate, potentially resulting in costs that outweigh the benefits. Therefore, based on the hospital’s actual conditions—such as its current human and material resources—and adhering to the principles of cost-benefit analysis and materiality, homogeneous activities may be appropriately subdivided or consolidated. This approach ensures comprehensive cost information and avoids distorting the hospital’s operational processes, while balancing the costs of implementing Activity-Based Costing (ABC) against the economic benefits derived from its application.

Second, establish a hospital resource pool and identify resource drivers. After delineating hospital activities, it is necessary to analyze the composition of medical costs and create a resource cost pool. Subsequently, determine the resource drivers that link resource consumption to activities based on their intrinsic relationship, and finally allocate and accumulate costs to each activity according to the relevant cost causes.

Third, establish activity cost pools and determine activity drivers. The determination of hospital activity cost pools and allocation drivers is primarily conducted by analyzing the cost structure of the final cost objects and the intrinsic relationships between various activities and these cost objects. Once the drivers are determined, costs are allocated following the same principle as the initial allocation to calculate the costs of the final cost objects.

Currently, numerous hospitals in countries such as the United States, the United Kingdom, France, and Japan have adopted activity-based costing for cost management, demonstrating significant effectiveness in controlling hospital operational costs and enhancing managerial efficiency.

Activity-Based Costing (ABC) applied to cost accounting for DRG groups (see Figure 7) offers numerous advantages:

First, the accounting methodology is more scientific and rational. In Activity-Based Costing (ABC), cost allocation is based on the drivers of cost incurrence. Costs are assigned to cost objects through tracing, driver-based allocation, and apportionment, thereby avoiding the use of a single allocation base characteristic of traditional costing methods. This approach enhances the rationality of cost allocation, yielding cost information that more closely reflects actual resource consumption.

Second, it enables more accurate and timely cost control. Activity-Based Costing (ABC) places greater emphasis on cost traceability. In ABC accounting, directly consumed resources are charged directly, while indirect costs are allocated using multiple criteria based on resource drivers. This approach allows costs to be traced back to the product design phase, identifies the activities constituting the costs, facilitates reasonable forecasting of resource consumption, and thereby assesses the value contributed to customers by the product. Through driver analysis, historical data can be referenced when establishing standard activity-based costs for specific disease types, determining allocation standards for expenses, and thus enabling real-time control during the cost incurrence process. This method facilitates hospital monitoring of the cost generation process. Studies have shown that ABC can provide more detailed cost information on hospital medical activities, thereby improving cost management and, to some extent, reducing costs.

Third, the application of Activity-Based Costing (ABC) can enhance the reliability and accuracy of pricing for medical services. By adopting ABC, a scientific cost accounting methodology, hospitals can proactively refine their cost accounting systems, improve the veracity of cost information, and provide data-driven support for decision-making by both hospital administrators and government authorities.

Figure 7. Activity-Based Costing Method for DRG Group Cost Accounting

Despite the numerous advantages of activity-based costing (ABC), a comparison between theoretical research findings on ABC in previous literature and its practical application outcomes reveals a certain gap. This discrepancy may prevent users of activity-based costing from achieving their expected results. Specifically, the main reasons are as follows:

One major challenge lies in the high computational costs. In the specialized healthcare industry, medical services are diverse and complex; treatment plans often vary significantly among patients depending on their specific conditions. Given the substantial volume of operations in hospitals, implementing activity-based costing (ABC) for accounting purposes is extremely cumbersome. Even with the support of modern computers and databases, hospitals continuously update medical processes and technologies to maintain a competitive edge, while also subdividing or integrating departments based on evolving needs. If ABC is adopted, corresponding activities must likewise be subdivided or integrated, which undoubtedly increases the workload and cost of cost accounting. If hospitals fail to properly balance the economic benefits gained from applying ABC against the additional costs incurred by its implementation, the effort may ultimately prove counterproductive.

Another aspect lies in the errors and biases caused by subjectivity. In Activity-Based Costing (ABC), cost allocation is performed based on specific cost drivers; if the method designers and implementers lack objectivity during application, the effectiveness of ABC implementation will be significantly constrained.

Overall, because Activity-Based Costing (ABC) imposes extremely high requirements on the quality of hospital cost data collected and involves complex calculation methods, its promotion and application for DRG cost accounting require significant time and resources. However, since cost data derived from ABC more closely reflect actual resource consumption, employing this method can effectively improve the DRG grouping system and DRG weights, while also providing guidance for pricing. Countries typically decide whether to adopt this method for DRG cost accounting based flexibly on the sophistication of their hospital information systems and the quality of their data.

If this method is adopted, after collecting the necessary data and information, several key points regarding the implementation of Activity-Based Costing (ABC) must be clarified, as follows: First, define the activity structure, simplifying it as much as possible by minimizing the number of activities. Second, collect and register cost information within the accounting system, along with other additional bases for defining activities, utilizing various forms of cost driver sources. Third, calculate the rate for each given activity using the defined cost drivers and measures of activity output. Fourth, calculate the costs for patients corresponding to specific Diagnosis-Related Group (DRG) categories. Fifth, compare the DRG or patient costs with the payment reimbursements obtained from the Healthcare Security Administration.

V. Selection and Comparison of Healthcare Cost-Sharing Methods Across Different Countries

Theoretically, allocating hospital costs to patients or diagnosis-related groups (DRGs) based on clinical similarity and resource consumption involves the following three components: 1) Allocation of medical-related overhead costs: assigning medical-related overhead costs to clinical departments; 2) Allocation of indirect costs: apportioning departmental indirect costs to individuals; 3) Allocation of direct costs: apportioning departmental direct costs to individuals.

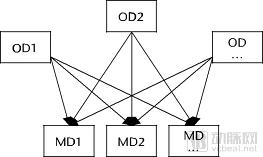

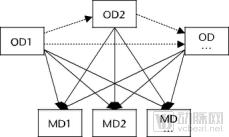

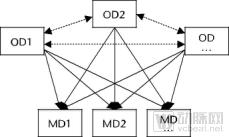

Allocation of healthcare-related costs can be based on inpatient bed-days or direct cost volumes of each cost center, or alternatively, on the principles of activity-based costing. Regardless of whether the allocation is based on cost centers or activity-based costing, healthcare-related costs can be allocated to clinical departments using the following three models: 1) Direct Allocation: Healthcare-related costs are directly allocated to clinical departments, with no cross-allocation among healthcare support departments (Figure 8.1); 2) Step-Down Allocation: Healthcare-related costs are allocated not only to clinical departments but also sequentially to other healthcare support departments, requiring a specific order for allocations among clinically related departments (Figure 8.2); 3) Reciprocal Allocation: Costs from healthcare support departments are allocated to clinical departments and all other healthcare support departments, allowing for bidirectional allocation and requiring multiple iterations to eliminate unallocated costs (Figure 8.3).

Figure 8.1: Direct Allocation

Figure 8.2: Segmented Allocation

Figure 8.3: Interactive Allocation

Note: OD: Overhead Department (medical-related departments); MD: Medical Department (clinical departments)

Indirect Costs: Indirect costs refer to various expenditures incurred in the provision of medical services that cannot be directly attributed and must be allocated according to specific principles and standards.

There are three primary methods for cost accounting: 1) Marginal Mark-up Method: This method allocates indirect costs to direct costs by calculating marginal mark-up percentages and applying them to increase direct costs; 2) Weighted Statistical Method: This method determines different indirect costs through weighted calculations based on statistical weights; 3) Relative Value Units (RVU) Method: This method establishes base values according to the baseline resources consumed by hospital services, adds value based on the resources consumed by individual patients to derive patient-specific relative values, and then calculates costs. While this method most accurately reflects patient-level costs, it demands more granular data.

Direct costs refer to various expenditures incurred by a department in carrying out medical service activities that can be directly charged or calculated using specific methods and then directly charged. Direct cost accounting can be divided into bottom-up costing and top-down costing allocation methods.

Countries such as Denmark and the Netherlands adopt a bottom-up cost allocation method for cost accounting to calculate DRG relative weights. Indirect costs are first allocated to direct cost centers, and then allocated in a bottom-up manner based on the actual volume of services provided during patient treatment. This process determines the actual cost of each type of medical service per patient. The costs of various medical services are then aggregated to obtain the total patient cost, which is subsequently used to derive DRG relative weights. This approach is considered the most accurate method for calculating DRG relative weights because it precisely measures the cost of each service for every patient. It also helps hospital administrators understand the distribution of cost data and track the drivers of cost changes. However, this method requires a precise accounting system and highly skilled personnel. Most countries struggle to obtain resource utilization data at the patient level, or the available data quality is insufficient to meet the requirements.

Tan et al. (2009), after comparing cost allocation methods, pointed out that the top-down allocation method can also serve as a robust alternative to the bottom-up approach. The top-down allocation method allocates costs based on standard service volumes from the top down, ultimately yielding the average cost per patient for each type of medical service. This method does not require patient-level data, offering certain feasibility in terms of data availability. Generally speaking, countries capable of obtaining detailed patient-level data tend to adopt the bottom-up approach, whereas countries lacking such data, such as the United Kingdom and France, employ the top-down approach.

The book *DRGs in Europe* investigates and compares DRG cost accounting in eight European countries, with the comparison results shown in Table 1:

Table 1 Summary of Different Characteristics of DRG Cost Accounting in Eight European Countries

Country | Healthcare-Related Costs | Indirect Costs Allocated to Patients | Direct Costs Allocated to Patients | Number of Hospital Cost Items Collected | Data Validation (Patterns) |

Austria | Hospitals Vary | Hospitals Vary | Total Cost | 20 Reference Hospitals (8% of Hospitals) | Area (Irregular) |

England | Direct Allocation | Weighted Statistics | Top-Down | All Hospitals | National (Annual) |

Estonia | Direct Allocation | Cost-plus rate | Top-down | Hospitals Partnering with EHIF | Country (Annually) |

Finland | Direct Allocation | Weighted Statistics | Bottom-up | 5 reference hospitals meeting specific cost accounting standards (30% specialized nursing) | No, relying on the hospital's liability |

France | Segmented Allocation | Weighted Statistics | Top-Down | 99 volunteer hospitals participating in ENCC (13% hospitalization rate) | Region (Annually) |

Germany | Segmented Allocation | Weighted Statistics | Bottom-up | 125 voluntary hospitals (6% of hospitals) participating in InEK that meet cost accounting standards | National (Annual) |

Netherlands | Direct Allocation | Weighted Statistics | Bottom-up | Unit cost: 15–25 voluntary general hospitals (24% of hospitals) | National (Annual) |

Sweden | Direct Allocation | Weighted Statistics | Bottom-up | Hospital Cost Accounting System (62% of patients participated) | National and Regional (Annual) |

VI. Scope of Costs Covered by DRG Payment

To prevent hospitals from refusing admission or deliberately shortening the length of stay for patients in certain specialties, and given that some diseases lack sufficient data support for grouping due to their low incidence rates, while cost prediction for certain specialties (such as psychiatry) has proven ineffective, various European countries have excluded certain costs from the scope of DRG-based payment. Instead, they have adopted alternative reimbursement methods, such as fee-for-service or supplementary payments.

High-cost pharmaceuticals (France, Germany, the Netherlands, Poland, Sweden) and medical consumables (France, Spain, Sweden) are generally excluded from DRG-based payment. Teaching and research costs are not covered under DRG payment. In Austria, Finland, Germany, and Ireland, hospitals’ capital costs and interest expenses are excluded from DRG payment. Debt subsidies for hospitals in Germany and Ireland are also excluded from DRG payment.

As shown in the following table:

Table 2 Scope of DRG Relative Weight Cost Reimbursement by Country in 2012

Country | Physician Costs | Teaching, Training, and Research Costs | Cost of Capital | High-Cost Medications |

Austria | √ | × | × | √ |

England | √ | × | √ | √ |

Estonia | √ | × | √ | √ |

Finland | √ | × | × | √ |

France | √ | × | √ | × |

Germany | √ | × | √ | × |

Netherlands | √ | × | × | √ |

Sweden | √ | √ | × | √ |

United States | × | Varies by state | × | × |

VII. Requirements for Cost Accounting Systems under DRG Payment Implementation in Various Countries

In summary, granular cost information is critical for DRG grouping and pricing. If cost data are not refined to the level of per-patient treatment costs, it will be difficult to achieve accurate homogeneity in DRG disease groups, and rate calculations will lack precision. Overpricing fails to incentivize hospitals to optimize more efficient clinical pathways, while underpricing may compel some hospitals to compromise medical quality to offset losses.

At the “1st National Diagnosis-Related Groups (DRG) Forum” held on December 9, 2016, Thomas Mansky from the Technical University of Berlin and Berlin Institute of Technology stated in his speech titled “The German Health Insurance System and the Application of DRGs” that inappropriate cost data can lead to a “compression effect,” preventing the achievement of the most granular grouping. He provided the following examples:

Figure 9. The accuracy of cost accounting directly affects DRG grouping results

In countries with a certain cost accounting foundation, the introduction of Diagnosis-Related Groups (DRGs) has simultaneously promoted reforms in hospital cost accounting. These countries selected individual hospitals as pilot sites to develop a standardized cost accounting system. Based on this, the national authorities issued a guideline manual for hospital cost accounting, which clearly specifies cost categories and allocation methods, ultimately enabling the full attribution of hospital costs to cost centers and individual patients.

In other countries, high-quality cost data are virtually nonexistent. For instance, Ireland, Portugal, and Spain lack standardized and comparable high-quality cost information. When introducing DRG-based payment systems, these countries adopted DRG frameworks from other nations—including the associated relative weights—in a package deal, making only minor adjustments to the DRG weights based on locally available department-level aggregated cost accounting data. As a result, it is difficult to ensure homogeneity in resource consumption within each DRG group.

In Estonia and Poland, hospitals transitioned directly from fee-for-service to the DRG system, using length of stay as the cost benchmark for calculating DRG weights. However, this approach fails to account for treatment complexity and patient characteristics, making it difficult to achieve true consistency in resource consumption within the same disease group.

Overall, when introducing the DRG payment system, countries have initiated the construction of national-level cost accounting systems, as shown in Table 3:

Table 3 Cost Accounting Systems in Typical Countries and the Use of Cost Accounting for DRG Pricing

Country | Mandatory Cost Accounting System | National Cost Accounting Guidelines | Cost Accounting System Used in DRG Pricing |

Austria | - | - | √ |

England | √ | √ | √ |

Estonia | - | - | √ |

Finland | - | - | √ |

France | - | √ | √ |

Germany | - | √ | √ |

Ireland | - | √ | - |

Poland | - | - | - |

Portugal | √ | √ | - |

Netherlands | √ | √ | √ |

Spain | - | - | - |

Sweden | - | √ | √ |

References:

1. Reinhard Busse,Alexander Geissler,Wilm Quentin,Miriam Wiley. Diagnosis-Related Groups in Europe : Moving towards transparency, efficiency and quality in hospitals[M]. New York,2011: 27-29

2. Nathanson M.Comprehensive cost accounting systems give chains an edge[J].Modem healtheare,1984,14(3): 122—128

3. Li Yong, Li Weiping. Progress in Hospital Cost Accounting in Developed Countries and Its Implications for China. [J]. Health Economics Research, 2017(5): 3-8

4. Wang Danan, Han Minghui. Cost Accounting and Management in Public Hospitals [M]. Shenyang: Liaoning Science and Technology Press, 2013: 2-3

5. Han Binbin, Zhang Junhua. Research on Hospital Cost Management [M]. Beijing: Economic & Management Publishing House, 2013: 99-102

6. Larry K. Macdonald and Louis F. Reuter IV. A Patient- Specific Approach Hospital Cost Accounting. [J].health services research,1973, Summer:102-120

7. Barbara O. Wynn & Molly Scott. Evaluation of Alternative Methods to Establish DRG Relative Weights. WR 560-CMS, 2008(4), RAND Health working paper series

8. Chen Jianwei. Research on the Cost Accounting Methods for Single Diseases in Hospitals and the Application of Results [D]. Chengdu: Southwestern University of Finance and Economics, 2009:25-26

9. Wang Pingxin. Research on the Theory and Application of Activity-Based Costing [M]. Dalian: Dongbei University of Finance and Economics Press, 2001: 17-25.

10. Zhao Weihua, Zhao Min. Application of Activity-Based Costing in Disease-Specific Cost Accounting [J]. Chinese Journal of Social Medicine, 2014(10):304-306

11. Xu Yuanyuan, Tian Liqi, Hou Changmin, Cao Liqing. Refined Management of Hospital Economic Operations [M]. Beijing: Enterprise Management Publishing House, 2014: 313.

12. Schreyogg J,Stargardt T,Tiemann O,et al.Methods to determine reimbursement rates for diagnosis related groups(DRG):a comparison of nine European countries[J].Health Care Manag Sci 2006,9(2): 15-23

13. Nathanson M. Comprehensive cost accounting systems give chains an edge[J]. Modern healthcare, 1984,14(3): 122-128

14. Tan S S, Rutten F F H, Vanineveld B M, et al. Comparing methodologies for the cost estimation of hospital services[J]. European journal of health economics, 2009,10(4):39– 45

15. Reinhard Busse, Alexander Geissler, Wilm Quentin etc. Diagnosis-related groups in Europe[M],2011

16. Tan S S, Rutten F F H, Vanineveld B M, et al. Comparing methodologies for the cost estimation of hospital services[J]. European journal of health economics, 2009,10(4):39– 45

17. Reinhard Busse, Alexander Geissler, Wilm Quentin etc. Diagnosis-related groups in Europe[M],2011

18. Zhou Yunyan, Jiang Qin, Zhang Zhenzhong. Analysis of DRG Relative Weight Calculation Methods in European and American Countries [J]. Chinese Health Economics, 2016(5): 94-96

Copyright Statement:

Most of the views presented in this article are based on Dr. Liu Zhichen’s personal postdoctoral research findings. The cited articles and viewpoints reflect those of their respective authors, obtained from publicly available sources. Unauthorized reproduction, excerpting, copying, mirroring, or any other form of use is strictly prohibited.