National Pilot Program for Centralized Drug Procurement Unveiled: Deep Dive into Policy Framework and Product Implications

Volume-based procurement continues to keep pharmaceutical professionals on edge, evolving from a hot topic into a subject of ongoing monitoring.

VCBeat has learned that the State Council Information Office held a regular policy briefing at 3:00 p.m. on Thursday, January 17, 2019. Chen Jinfu, Deputy Director of the National Healthcare Security Administration, along with relevant officials from the National Health Commission and the National Medical Products Administration, were invited to introduce the pilot program for the state-organized centralized procurement and use of pharmaceuticals and to answer questions from reporters.

Following the release of the “4+7 Centralized Procurement” documents, this marks another major policy update to volume-based procurement. The State Council has issued an official document and convened a dedicated policy briefing to introduce relevant developments, with detailed implementation guidelines for volume-based procurement now in place.

The main contents of this article are as follows:

1. The top-level design has been perfected, and implementation details are being gradually rolled out;

2. A Review of the History of Drug Centralized Procurement: The General Trend of Price Reductions and Cost Control;

3. The value of generic drug manufacturers is returning to normal, and the key to breaking through lies in innovation;

4. Accelerating the Tri-Medical Linkage Reform, with Each Sector Fulfilling Its Role in Coordinated Advancement.

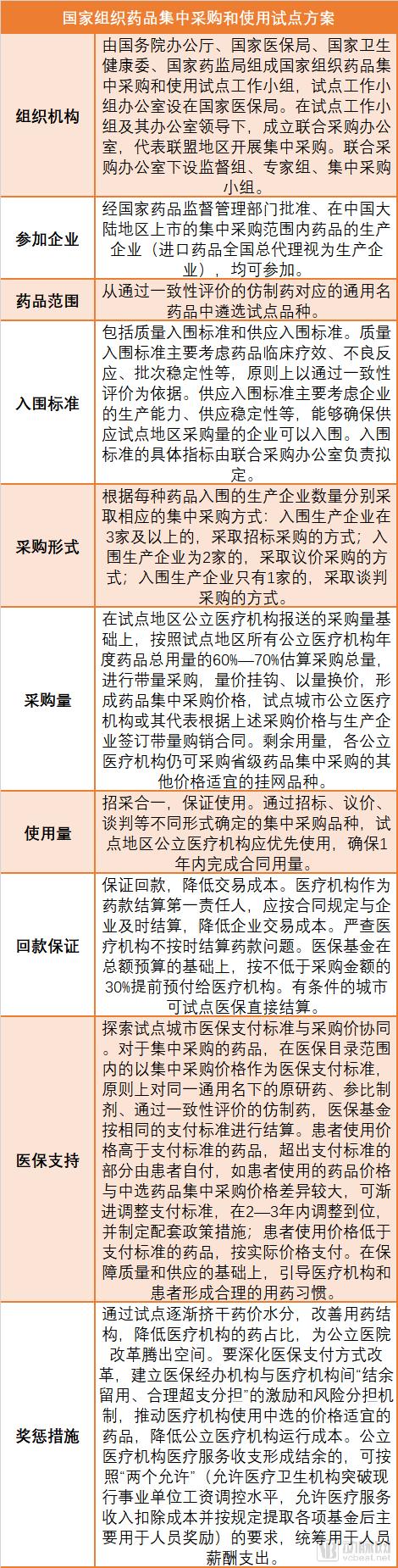

The “Pilot Program for Centralized Procurement and Use of Drugs Organized at the National Level” (hereinafter referred to as the “Program”) has been approved by the State Council, which has deployed pilot work for centralized drug procurement. The pilot program is being implemented in four municipalities directly under the central government—Beijing, Tianjin, Shanghai, and Chongqing—as well as in seven other cities: Shenyang, Dalian, Xiamen, Guangzhou, Shenzhen, Chengdu, and Xi’an, totaling 11 cities.

“The Plan” outlines arrangements for the organization, participating enterprises, drug scope, eligibility criteria, procurement methods, and payment mechanisms involved in the national centralized drug procurement and utilization program. VCBeat has summarized the key points of this national pilot scheme for centralized drug procurement:

At the briefing, Chen Jinfu, Deputy Director of the National Healthcare Security Administration, introduced that the purpose of the "Plan" is to adhere to a problem-oriented approach and focus on addressing prominent issues in the area of drug procurement. The main objectives are: First, to effectively reduce drug prices by eliminating inflated costs through the transformation of reform mechanisms. Second, to link volume with price, improve the procurement mechanism, address irregular practices in the procurement field, remove institutional barriers, purify the industry ecosystem, and, in other words, reduce unnecessary expenses to promote the healthy development of the industry. Third, to support and guide medical institutions in standardizing medication use, optimizing the structure of drug usage, enhancing the level of diagnosis and treatment related to medication, and promoting the reform of public medical institutions. Fourth, to explore and improve the drug procurement mechanism and establish a market-led drug price formation mechanism.

In line with this objective, an overarching reform framework has been established, which can be succinctly summarized as “state-led organization, consortium-based procurement, and platform-based operations.” State-led organization refers to the government’s role in facilitating inter-departmental coordination, removing institutional barriers, and ensuring policy coherence throughout the tendering and procurement process. Consortium-based procurement entails public healthcare institutions, as the primary purchasing entities, forming regional alliances in accordance with laws and regulations, and conducting drug tendering and procurement for public hospitals through a Joint Procurement Office. Considering that multi-platform operations would increase transaction costs and add procedural steps, certain tasks are delegated to the Shanghai Pharmaceutical Affairs Institute, which operates the “Sunshine Platform.” This constitutes the fundamental approach of the reform.

This round of centralized procurement differs from previous rounds in four fundamental aspects. First, it strictly mandates volume-based procurement, exchanging volume for price. By providing enterprises with a committed market share, companies can conduct cost and operational calculations based on this guaranteed volume, thereby facilitating the exchange of volume for price and price for volume. Second, it strictly integrates procurement with usage to ensure actual consumption. Since a commitment regarding market volume has been made to enterprises, it is essential to guarantee that this commitment is fulfilled at the point of use.

Third, ensure quality and guarantee supply. Since the drug consumption in the "4+7" pilot regions accounts for approximately 30% of the national total, it directly impacts the accessibility and quality assurance of medications for the general public; therefore, quality must be strictly ensured. The eligibility criteria for winning bids in this round include: first, passing the consistency evaluation to compete on an equal footing with originator drugs; and second, providing guaranteed production capacity.

Fourth, payment collection must be guaranteed to reduce efficiency costs. In the past, significant arrears and delayed payments from centralized procurement processes unnecessarily increased transaction costs for both distribution and manufacturing enterprises; therefore, ensuring timely payment collection is imperative. Regarding payment assurance, medical institutions serve as the primary entities responsible for settling payments, while the medical insurance fund provides 30% as an advance payment to alleviate the repayment pressure on medical institutions. These are the four strict requirements for centralized procurement.

Source: China.org.cn Live

Work Arrangements for the Pilot Program. The pilot initiative was implemented in three phases. Phase I consisted of the centralized procurement phase. On December 6, 2018, information regarding centralized procurement declarations was made public, price negotiations were conducted and confirmed, and notarized preliminary award results were generated. After a one-week public notice period, the final award results were announced, ensuring that the entire operational procedure was lawful and compliant. Twenty-five products were selected, with an average price reduction of 52% and a maximum reduction exceeding 90%, thereby basically achieving the initial objectives of the reform.

However, this is merely the initial step of the reform, with two subsequent phases to follow: namely, the implementation of bid-winning results and the rollout of supporting measures. Finally, pilot evaluations and summaries will be conducted in accordance with the requirements set forth by the Central Committee of the Communist Party of China and the State Council. If this reform proceeds smoothly, its achievements will be institutionalized to further advance the reform of the drug procurement and bidding system. This will ensure that the benefits of the reform translate into tangible gains for the public, promote high-quality development of the pharmaceutical industry, optimize healthcare institutions, and enhance the performance of the medical insurance fund, thereby fulfilling the requirement to include more life-saving and emergency medications in the medical insurance coverage.

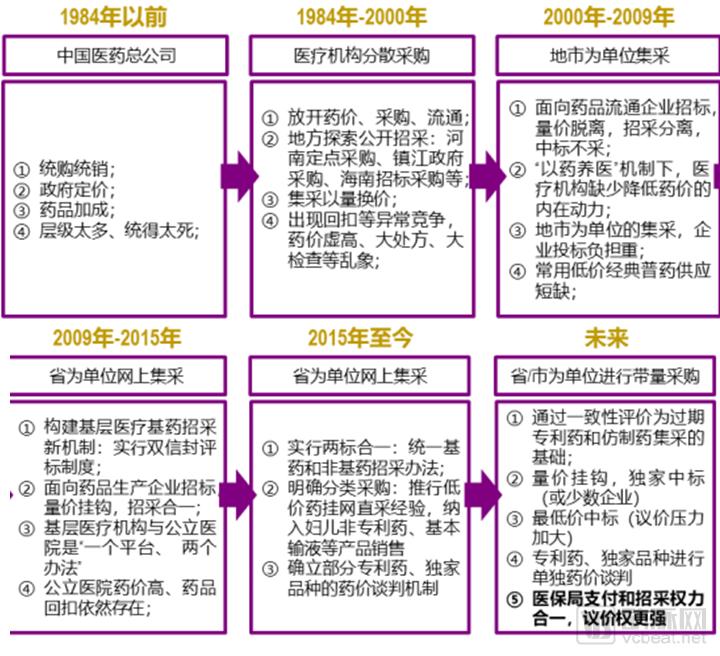

China’s drug procurement and bidding processes have generally evolved through six phases: prior to 1984, centralized purchasing and distribution were managed by the China National Pharmaceutical Corporation; from 1984 to 2000, healthcare institutions conducted decentralized procurement; from 2000 to 2009, centralized procurement was carried out at the prefecture-level city level; from 2009 to 2015, online centralized procurement was implemented at the provincial level; from 2015 to the present, online centralized procurement has continued at the provincial level, while exploring approaches such as classified procurement and price negotiations; in the future, the system is expected to evolve into a multi-department collaborative centralized procurement model led by the National Healthcare Security Administration.

A Retrospective on the History of Drug Procurement and Bidding in China

Source: Official websites of the State Council, National Health Commission, and National Healthcare Security Administration; Everbright Securities Research Institute

The keywords for the changes in drug centralized procurement methods are “price reduction” and “cost containment.” The background includes continuously rising healthcare expenditures, increased pressure on medical insurance payments due to population aging, and long-standing unreasonable drug pricing levels.

According to data from the National Health Commission, China’s total healthcare expenditure in 2017 (excluding expenditures covered by social security funds, commercial health insurance reserves, and private medical institutions) reached RMB 4.20 trillion, a year-on-year increase of 13%, significantly higher than the concurrent growth rates of GDP and fiscal expenditure (6.9% and 8.2%, respectively). A breakdown reveals that fiscal investment is slowing down, with enterprises and residents being the primary drivers of the recent growth in total healthcare spending. From January to November 2018, the growth rate of basic medical insurance revenue showed a slowdown compared to the same period in 2017. Considering factors such as the declining proportion of the working-age population and the new normal in economic growth, pressure on the balance of medical insurance revenues and expenditures will persist in the long term.

Guosen Securities’ research report points out that the aging population in China is becoming increasingly prominent, placing dual pressure on the basic medical insurance fund due to declining revenues and rising expenditures. The state has made multiple attempts at healthcare reform; following the introduction of the new healthcare reform policy in 2009, a “lowest bid wins” policy was implemented in the drug tendering and procurement process, aiming to reduce medical insurance spending by lowering drug costs.

However, due to the inconsistent quality of domestically produced generic drugs in China, they struggle to be classified in the same quality tier as imported originator products in tiered bidding processes. This has trapped Chinese-made generics in vicious low-price competition, while imported originator drugs with expired patents enjoy “supra-national” pricing (prices significantly higher than those in European and American markets) and dominate the majority of the generic drug market share, making it difficult to alleviate the payment pressure on the medical insurance system.

Amid the vicious competition driven by a “lowest-price-wins” mentality in the domestic pharmaceutical market, emerging drug quality issues have compelled tendering policies to become more moderate once again. Through the consistency evaluation, domestically produced generic drugs now compete on an equal footing with imported originator products, enabling rapid import substitution while ensuring quality. Overall, domestic substitution has saved substantial expenditures for the national medical insurance system and created market space to boost the penetration rate of innovative drugs.

Since 2015, a series of new regulatory policies covering the entire lifecycle of pharmaceuticals—“R&D, manufacturing, distribution, tendering/procurement, and payment”—have been successively introduced, virtually reshaping China’s pharmaceutical regulatory framework. In March 2018, following the State Council’s institutional restructuring, the National Healthcare Security Administration (NHSA) was established, consolidating procurement, payment, and pricing authorities. The NHSA began piloting volume-based procurement (VBP) for generic drugs that have passed consistency evaluations. This shift replaced the previous paradigm, in which high-priced generics commanded large market volumes, with a new model where only cost-effective products can achieve substantial sales volumes.

One of the prerequisites for volume-based procurement is that drugs must pass the consistency evaluation. Officials from the National Medical Products Administration (NMPA) have stated that conducting consistency evaluations on already approved generic drugs is a way to address historical gaps. Because there were no mandatory requirements for consistency with originator drugs when these products were previously approved, some generics exhibited certain disparities in efficacy compared to their originator counterparts. Historically, countries such as the United States and Japan have undergone similar processes; Japan, for instance, spent over a decade advancing the consistency evaluation of generic drugs.

According to the Yaozhi Drug Registration and Acceptance Database, as of January 16, a total of 752 acceptance numbers for consistency evaluation were recorded (statistically based on supplemental applications, same below), involving 252 varieties from 272 enterprises. Among these, 374 acceptance numbers (covering 95 varieties) were for drugs listed in the Catalogue of 289 Varieties; 123 acceptance numbers (covering 61 varieties) have been approved.

On December 28, 2018, the National Medical Products Administration (NMPA) issued a document emphasizing that quality takes precedence over timelines. For drugs listed in the National Essential Medicines List that have failed to complete the consistency evaluation within the prescribed period, enterprises may apply for an extension to their provincial-level drug regulatory authorities if, after assessment, the drugs are deemed clinically essential and in short supply in the market. This supplementary guidance on the consistency evaluation, taking into account the progress of implementation, extends the deadline but does not relax the requirements.

Data source: YZData

A research report by Everbright Securities points out that volume-based procurement will reshape the key competitive factors in the industry. Pursuing high product pricing and extended product life cycles is a common objective for pharmaceutical companies. Previously, to maintain high prices, pharmaceutical companies tended to develop proprietary dosage forms and specifications; to extend product life cycles, they invested heavily in product marketing.

However, under the volume-based procurement model, pharmaceutical companies can only maintain overall high pricing for their product portfolios by continuously innovating; only those with cost advantages can extend product life cycles. The competitive dynamics of the industry are set to be reshaped, as specifically manifested below:

1) Standardization of Generic Drug Quality: The quality assessment for volume-based procurement is primarily based on the consistency evaluation. Once generic drugs pass this evaluation, they are considered standard products with equivalent quality. Previously, originator drugs, first-to-market generics, and those supported by major national special projects no longer enjoy preferential treatment under quality-tiering policies.

2) Weakened Marketing of Generic Drugs: Following the implementation of volume-based procurement, the marketing role of generic drugs has diminished due to guaranteed sales volumes.

3) Strengthening R&D Value: Standardization of generic drug quality requires pharmaceutical companies to orient their R&D efforts toward clinical value. Exclusive dosage forms and specifications that lack significant clinical advantages will no longer hold strategic importance. Furthermore, volume-based procurement enables new products to rapidly scale up sales but also accelerates their replacement by superior alternatives, thereby significantly shortening the lifecycle of any single product. This necessitates that enterprises possess the capability for continuous innovation, meaning that both generic and innovative drug development must be conducted with high efficiency.

4) Reinforcement of Cost Advantage Value: Apart from low-priced drugs, the pricing of original drugs was generally not linked to production costs. Under the volume-based procurement (VBP) model, drug prices will decline significantly as they face continuous competition from new market entrants. Therefore, enterprises with cost advantages—driven by factors such as low active pharmaceutical ingredient (API) costs and high operational efficiency—will gain a distinct edge. For instance, companies with integrated “API + formulation” capabilities will possess stronger competitive advantages.

Innovation is the key to the future. Changes in mechanisms have altered the lifecycle curves of pharmaceutical products, thereby influencing the choice of business models for enterprises. The marketing model previously adopted by generic drugs—characterized by “high pricing, high expenses, and high gross margins,” similar to that of innovative drugs—is coming to an end. In the future, China’s pharmaceutical industry will transition toward innovative drugs. With the subsequent implementation of policies such as Diagnosis-Related Groups (DRGs) and medical insurance payment standards, clinical value has become a more core competitive factor; only drugs with genuine cost-effectiveness can achieve rapid volume growth. Going forward, enterprises can survive only by continuously innovating, steadily increasing R&D investment, and consistently developing new products with true clinical value.

As this trend transmits to the capital markets, valuation levels for generic drug manufacturers will normalize, further highlighting the value of innovative drugs.

Chen Jinfu stated that the centralized procurement process should be leveraged to synchronously advance the coordinated reform of medical insurance, pharmaceuticals, and healthcare services (“Three-Medical Linkage”). Specifically, improving the national pilot centralized procurement program should serve as a critical component to drive reforms in related sectors, including medical insurance, pharmaceuticals, and public medical institutions. This involves four specific aspects.

First, explore the synergy between medical insurance payment standards and centralized procurement prices in pilot cities. It has long been recognized that medical insurance payment standards are not synchronized with the procurement prices adopted by medical institutions. Consequently, after negotiating procurement prices, pharmaceutical companies have been more concerned about how payment standards are determined. This initiative aims to bridge this gap. In principle, for originator drugs, reference listed drugs, and generic drugs that have passed consistency evaluation under the same generic name, the medical insurance fund will apply a uniform payment standard, which is determined based on the winning bid price. Of course, the policy document also stipulates a 2–3-year transition period for adjusting the payment standards of certain high-priced medications that may increase the financial burden on patients. This approach not only reduces disparities in public policy but also guides the market toward reasonable price adjustments.

Second, promote the reform of medical institutions through mechanism transformation. The portion of distribution costs eliminated through centralized procurement, after assessment, will be retained by public hospitals to fund internal reforms, such as compensation system restructuring and adjustments to medical service prices, thereby stimulating the initiative of healthcare providers.

Third, regarding utilization issues, the current “Three-Medical” linkage reform explicitly emphasizes consolidating the responsibilities of medical institutions to ensure drug usage volumes. It is mandated that the prescribed procurement volume for winning bid drugs must be achieved within one year. The use of products selected through centralized procurement is encouraged. Relevant authorities are required to issue stipulations concerning clinical guidelines for medication use in medical institutions, generic drug substitution, and compliance with agreements, thereby ensuring that medical institutions utilize the winning bid products. Naturally, if any existing policies conflict or contradict these measures during implementation, appropriate adjustments should be made—such as those related to the drug revenue proportion and the “one product, two specifications” rule—to facilitate the advancement of the reform.

Fourth, regarding the coordinated reform of medical insurance, healthcare services, and pharmaceuticals, all relevant departments—including those overseeing medical insurance, healthcare delivery, pharmaceuticals, as well as industry and information technology—are required to strictly adhere to their respective responsibilities as outlined in the pilot program, perform their duties accordingly, and work in concert to ensure the smooth realization of the pilot reform outcomes.

In the long run, volume-based procurement of pharmaceuticals will impact the entire industry, starting with pharmaceutical manufacturing. The value of innovative drugs will become increasingly prominent, while generic drug manufacturers may face a wave of transformation—either by leveraging their prior market presence to expand into innovative drugs or by gaining cost advantages through the synergy of “active pharmaceutical ingredients (APIs) plus formulations.” Pharmaceutical marketing models are undergoing change, and traditional medical representatives are in urgent need of transformation.

R&D and marketing innovation, previously undervalued, will gradually gain prominence, driving the prosperity of the pharmaceutical big data and artificial intelligence sectors. This is because information technology can reduce costs associated with product development and clinical research, while big data mining and analysis will facilitate support in regulatory approval, market access, and reimbursement—exemplified by real-world studies and pharmacoeconomics.

“Internet + Healthcare” will emerge as a provider of solutions and a driver of value creation, leveraging the “Internet +” model to integrate medical services, pharmaceuticals, and health insurance. It will deliver more comprehensive, end-to-end management services for common and chronic diseases. Shifting from merely supplying medications to offering holistic disease-management solutions will become a central theme in the transformation of pharmaceutical companies and healthcare service providers.

In the distribution segment, the channel value of retail pharmacies will be further strengthened. Products that are abandoned, fail to attract bids, or lose bids will target out-of-hospital channels, deeply exploring opportunities in the grassroots pharmaceutical market and retail pharmacies. Policies such as classified and graded management of retail pharmacies, electronic prescriptions, and the outflow of prescriptions from hospitals will also further promote the development of the retail pharmacy industry.

【References】

Transcript of the State Council’s Regular Policy Briefing on January 17

The General Office of the State Council Issued the "Pilot Program for National Organization of Drug Centralized Procurement and Use"

Everbright Securities: 2019 A+H Strategy Report for the Pharmaceutical and Biotechnology Industry

Guosen Securities: 2019 Investment Strategy for Pharmaceuticals and Biotechnology