2019 Outlook: Embracing a New Competitive Order of 'Must-Have, Also-Need, As-Well-As, and Even-More'

This article is reposted from Guotai Junan Securities Research, authored by the Guotai Junan Healthcare Team. Republished with permission by VCBeat.

On the afternoon of January 17, the General Office of the State Council officially issued the formal implementation plan for volume-based procurement. This policy development has continued to captivate the attention of investors in the pharmaceutical industry over the past few months.

The pharmaceutical industry, which had been heavily expected to “cure” sluggish market sentiment, instead encountered its own policy “black swan” at the end of last year.

However, in the author’s view, China’s healthcare payment system determines the national consumer goods nature of the pharmaceutical industry. The National Healthcare Security Administration is a new variable, but as long as the total volume continues to grow, the changes are structural.

Navigating Policy Cycles: Demand Expansion, Industrial Upgrading, and Domestic Substitution—These Enduring Themes Will Continue to Fuel High-Prosperity Sectors.

Let us begin our annual outlook to identify the high-growth sectors.

In early 2018, cost containment measures under the medical insurance system fired the “first shot” of healthcare reform, as multiple provinces—including Guangxi, Zhejiang, Sichuan, and Henan—intensively issued notices to expand the scope of diagnosis-related group (DRG)-based payment and fee collection.

On May 31, 2018, the newly established National Healthcare Security Administration was officially inaugurated, consolidating multiple functions including the unified management of medical insurance funds, centralized drug procurement and bidding, and pricing. Its core leadership team was drawn from relevant ministries and commissions such as the Ministry of Finance, the Ministry of Human Resources and Social Security, the National Development and Reform Commission, and the National Health and Family Planning Commission, thereby centralizing previously fragmented responsibilities.

Source: Guotai Junan Securities Research

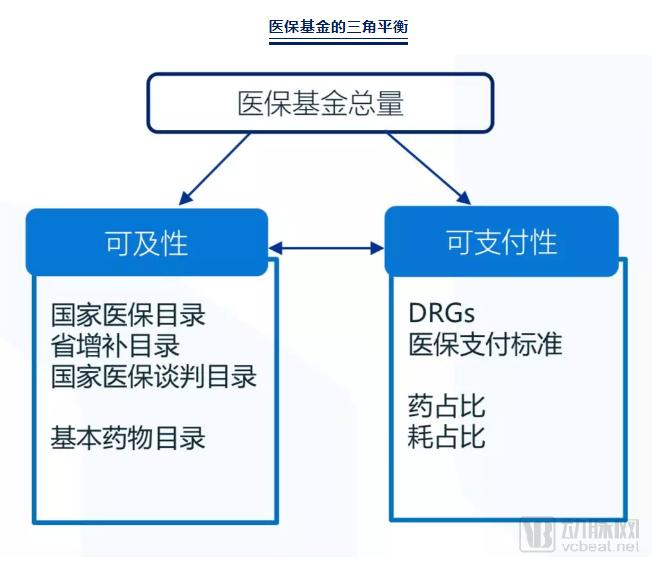

From the perspective of Guotai Junan’s healthcare team, the mandate for the national medical insurance fund is to seek a triangular balance among economics, sociology, and ethics, thereby resolving the contradiction between limited medical resources and unlimited medical demand.

“The most valuable tragedy lies not between good and evil, but between two dilemmas—Hegel”

Data source: Guotai Junan Securities Research

In 2019, we will also witness a “major year” for policy developments in the pharmaceutical industry, encompassing at least the following aspects:

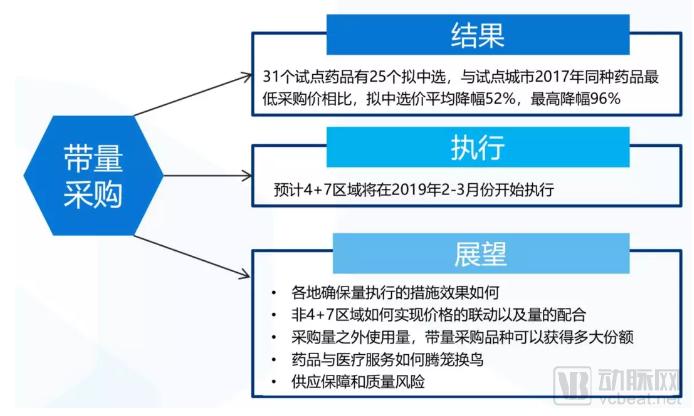

1. Implementation and Diffusion of the “4+7” Volume-Based Procurement

Data source: Shanghai Sunshine Pharmaceutical Procurement Network, Guotai Junan Securities Research

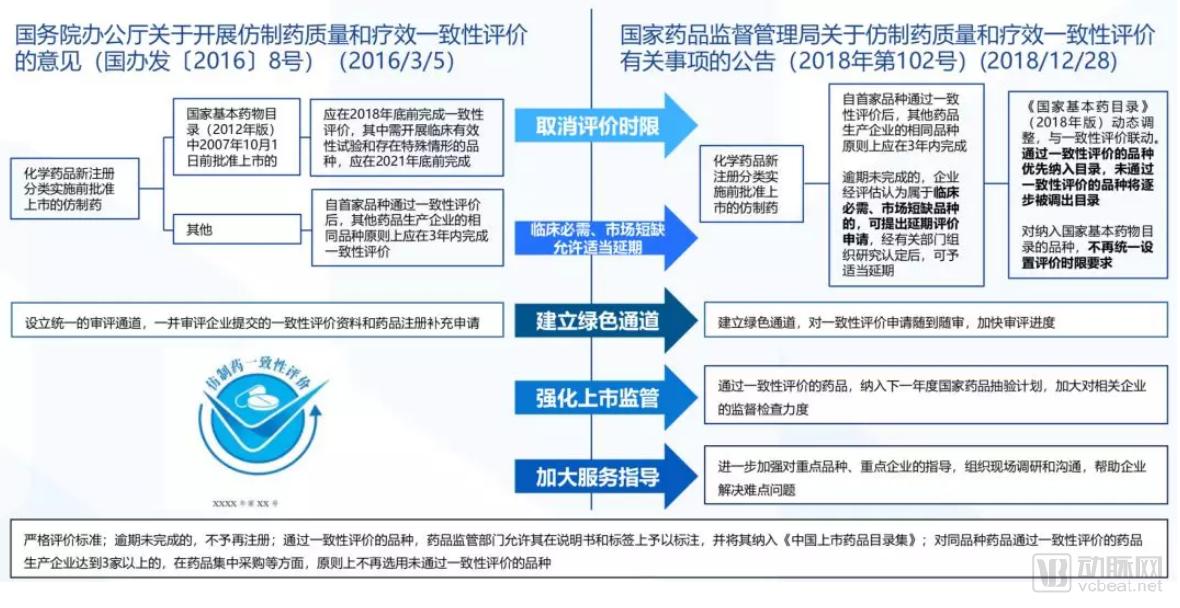

Second, the consistency evaluation will uphold standards while adjusting the roadmap

Data Source: NMPA, Guotai Junan Securities Research

Third, policies encouraging the procurement and use of generic drugs that have passed the consistency evaluation will continue to be introduced.

Approximately 23 provinces and municipalities have issued policies related to centralized procurement for drug varieties deemed to have passed the consistency evaluation. Meanwhile, around eight provinces have implemented policies stipulating that procurement of non-evaluated varieties will be suspended if more than three manufacturers of the same generic drug have passed the evaluation.

Fourth, the advancement of reforms in health insurance payment methods

Data Sources: Ministry of Human Resources and Social Security, National Healthcare Security Administration, Guotai Junan Securities Research

The current state of China’s pharmaceutical and healthcare market is the cumulative result of historical developments, reflecting the alignment of past supply structures with payment systems and their institutional designs. In the future, the Chinese market will more closely align with genuine clinical needs dictated by the disease spectrum.

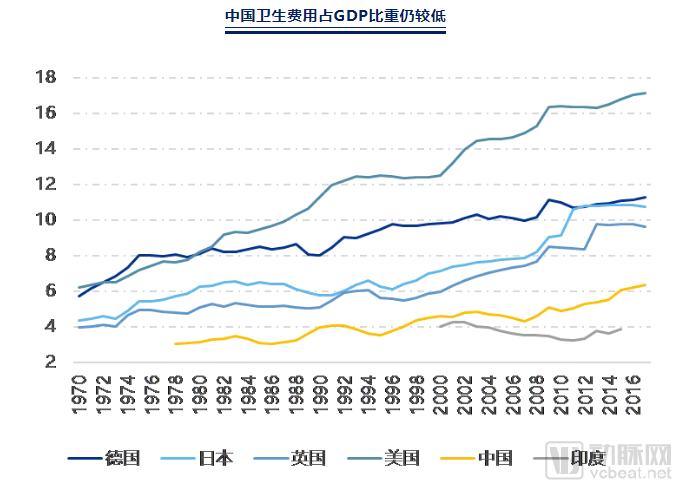

Although the share of health expenditure in GDP is rising globally, China’s health expenditure as a percentage of GDP remains relatively low.

Data sources: OECD, National Bureau of Statistics, National Health Commission, Guotai Junan Securities Research

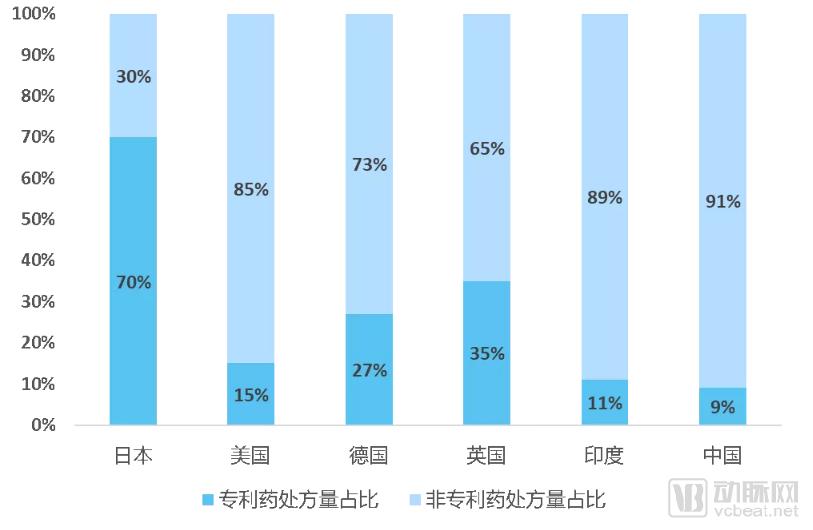

We often say, “With 7% of the world’s arable land, we feed 22% of the global population.” In regard to China’s healthcare sector, it can be stated that, with health expenditures accounting for 6.4% of GDP, China has achieved universal health insurance coverage for a population exceeding 1.3 billion, established a drug supply system centered on generic medications as the mainstay of diagnosis and treatment, and realized import substitution for more than half of the total volume across most drug categories.

Therefore, the first endogenous driver is the steady growth of future medical demand.

Data Source: CDE, OECE, Guotai Junan Securities Research

The second endogenous driver is that, from the perspective of pharmaceutical product utilization patterns, China’s non-mainstream drug usage structure urgently needs to be transformed.

Globally, the proportion of biologics continues to rise, and they are exclusively therapeutic agents; in China, off-patent drugs, traditional Chinese medicine injections, adjuvant therapies, and antibiotics account for an excessively high share.

Data sources: PDB, company annual reports, IMS, Guotai Junan Securities Research

Differences in product structure stem not only from the varying needs of disease diagnosis and treatment at different stages; such pronounced generational disparities are more likely the result of the co-evolution of interests between the healthcare supply side and the pharmaceutical supply side under the existing medical system, aligned with the payment framework.

This will loosen as policy orientations shift.

Data Sources: OECD, IQVIA, Guotai Junan Securities Research

The third endogenous driver is that drug review is optimizing its structure from the source.

As the drug review and approval system reform advances, the historical backlog has been largely cleared, review timelines have significantly decreased, and review standards have substantially improved.

In November 2018, the National Medical Products Administration (NMPA) approved 541 new drug registrations, including 455 for domestically produced drugs, far exceeding the levels of the previous year. The quality of small-molecule drug R&D has been upgraded, biologics R&D has experienced explosive growth, while traditional Chinese medicine (TCM) R&D continues to shrink. Innovative drugs have truly entered an acceleration phase.

Data sources: CDE, Pharmadule, Guotai Junan Securities Research

In this new era of super medical insurance, health insurance reimbursement has become the most significant variable determining the overall growth rate of the industry. A new competitive order is beginning to take shape, extending from review and approval to inclusion in the national reimbursement drug list (NRDL), and further to end-user sales.

Driven by policies such as priority review and national reimbursement drug price negotiations, the market is opening up at an accelerated pace: new drugs are reaching the market and gaining reimbursement coverage more rapidly. Consequently, legacy products are facing competitive pressure from newer agents prematurely, forcing domestic pharmaceutical companies and multinational corporations into head-to-head competition earlier than expected. This implies that the window of opportunity for domestic enterprises to undergo transformation is narrowing.

Taking EGFR small-molecule anticancer drugs as an example, domestic pharmaceutical companies have begun to engage in direct competition with multinational giants.

Data Source: CDE, PharmCube, Guotai Junan Securities Research

However, in the context of tender-based centralized procurement, companies with a single-product portfolio are prone to being trapped in a vortex of cost competition, whereas enterprises with a deep and diversified product portfolio are better equipped to respond effectively.

In volume-based procurement, AstraZeneca, holding Osimertinib in its portfolio, accepted a 75% price cut for Gefitinib to win the bid, which is a clear demonstration of the strength of its robust product pipeline. The shift from single-product competition to portfolio-based competition will be the second hallmark of the new competitive order.

However, for multinational corporations, the long-standing “super-national treatment” (referring to the pricing of off-patent drugs) has been significantly eroded, and like domestic enterprises, they now face a more powerful and centralized payer.

Therefore, under the third rule of the new competitive order, past industrial structures and business models will be forced to change more rapidly.

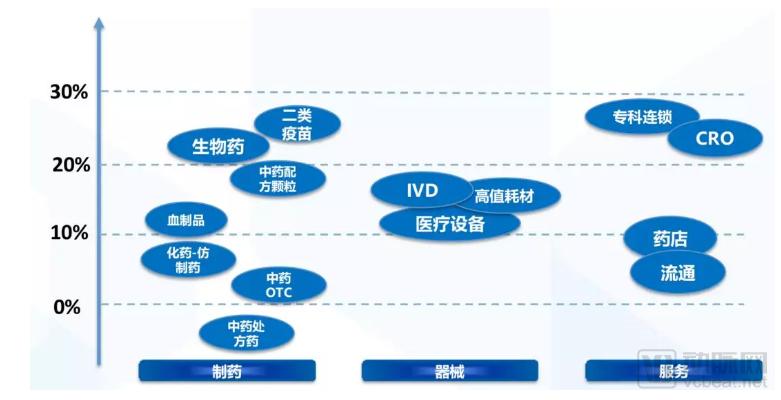

Let’s first use a chart to clarify the current prosperity landscape of sub-sectors within the pharmaceutical sector, as viewed by the Guotai Junan Pharmaceutical Team.

Data source: Wind, Guotai Junan Securities Research

Note: Based on the projected revenue growth rate for 2019.

Neither the Manufacturing Industry nor Pharmaceuticals Is the “Dying to Survive” Miracle Drug

The incumbent market, reshuffled by the “consistency evaluation + volume-based procurement” policy for chemical generic drugs, will coexist with the incremental market opened up by high-end generics in both chemical and biological sectors; meanwhile, intellectual curiosity and the drive for survival jointly serve as the subjective initiative propelling this round of industrial upgrading.

The aforementioned drastic changes in the “game rules” may compel domestic pharmaceutical companies to transform their former advantage in low-cost production factors into an advantage in cost innovation. However, the traditional cash-cow businesses of most domestic enterprises—generic drugs and adjuvant medications—are all facing long-term pressure.

We have entered a new competitive order defined by the imperative to “have it all”—excelling simultaneously in R&D strength, regulatory submission capabilities, market access, and sales and promotion. This represents a comprehensive competition of integrated corporate capabilities, as well as an all-out race in product launch speed, indication expansion, and pricing strategy.

A Game for the Few Amidst Concentrated Payer Purchasing Power Determines That We Will Also Welcome a New Era of Blockbuster Products—If You Bloom, the Breeze Will Come.

Generic Drugs

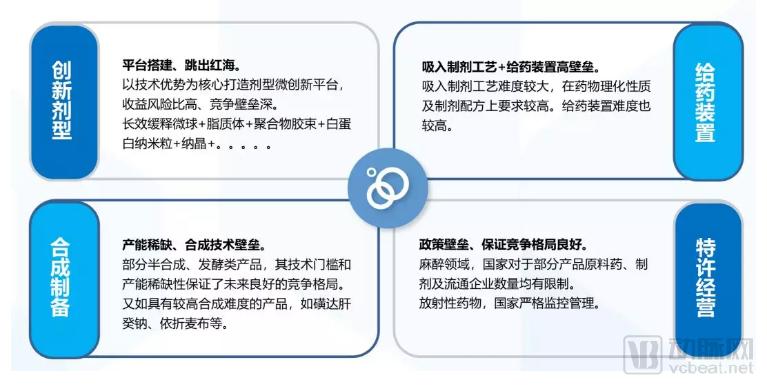

Even after the patent cliff, generic drugs may still yield excess returns, but this is primarily concentrated in high-end generics.

The core barriers to entry for high-end generic drugs are manifested in three aspects: first, technology, such as dosage form innovation centered on clinical needs and underpinned by technical barriers; second, policy, such as state controls over psychotropic and narcotic drugs; and third, production capacity, where existing capacity gains greater bargaining power amid rising environmental pressures and industry consolidation.

Data source: Guotai Junan Securities Research

Innovative Drugs

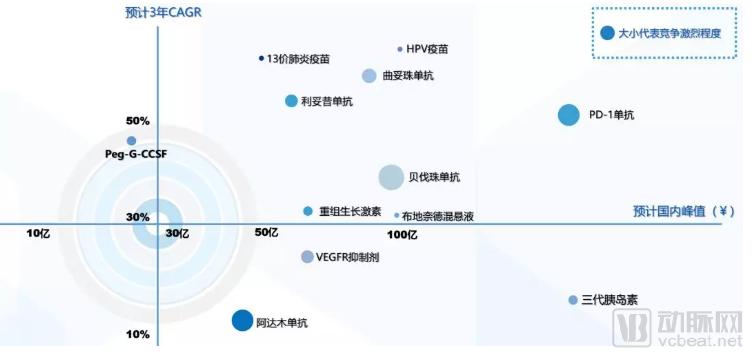

Under the policy support of “Priority Review” and “National Reimbursement Drug List (NRDL) Negotiations,” innovative drugs will reach the market and be included in the NRDL at a faster pace.

The gap in the initial launch time between domestic and foreign similar products has narrowed from 10–15 years in the era of small-molecule drugs to four years in the era of immunotherapy.

Data Source: Yaozhi, Guotai Junan Securities Research

The sales share of targeted oncology drugs (including biologics and small-molecule chemicals) in domestic sample hospitals has been rising year by year, with major domestically produced products poised for rapid growth.

Data Sources: Frost & Sullivan, Company Announcements, Guotai Junan Securities Research

However, the innovative drug sector is a brutal battlefield. The healthcare team at Guotai Junan Securities judges that the future test for innovative pharmaceutical companies will be their “four-in-one” comprehensive competitive capabilities: R&D capability, clinical and regulatory affairs capability, academic promotion and sales capability, and market access capability.

Source: Guotai Junan Securities Research

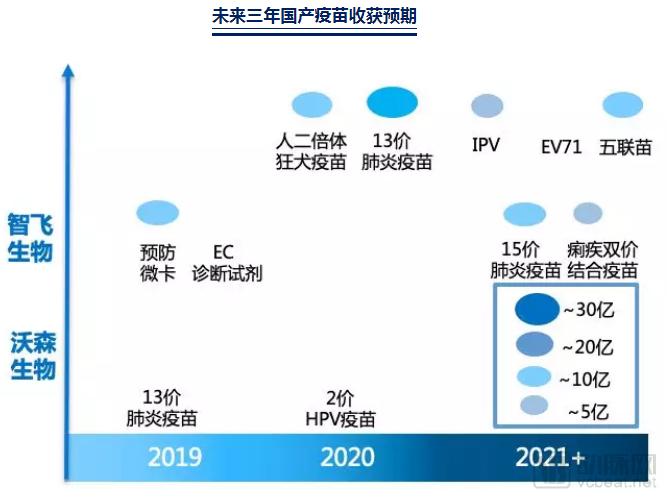

Vaccine

Beyond the two heavyweight segments of innovative drugs and generic drugs, the Guotai Junan pharmaceutical team also provided a detailed analysis in its outlook on areas such as vaccines, traditional Chinese medicine (TCM), blood products, and active pharmaceutical ingredients (APIs) within pharmaceutical manufacturing. Here, we will elaborate on vaccines, which have attracted considerable public attention.

Currently, the global vaccine market is experiencing steady growth, driven by increasing demand for vaccination, support from governments and international organizations, and the development and launch of new vaccines, all of which continue to propel the expansion of the global vaccine industry.

Compared with developed countries, most commonly used vaccines in China are previous-generation products, and the pace of introducing and launching new vaccines lags behind the international market.

However, driven by the accelerated approval of novel vaccines and the maturation of R&D efforts among domestic enterprises leading to increased market uptake of major new vaccine products, along with the development of the adult vaccine market, growing public awareness of vaccination, and improved affordability, China’s Class II vaccine market is expected to sustain rapid growth.

Data Sources: CIC, Frost & Sullivan, Guotai Junan Securities Research

Amid healthcare reforms, the National Medical Products Administration (NMPA) has accelerated the vaccine approval process, leading to the successive market launch of multiple imported and domestically developed new products, with EV71 and HPV vaccines seeing rapid volume growth. Currently, several promising novel vaccines in China have completed R&D and entered late-stage clinical trials, signaling that domestic vaccine manufacturers will enter a period of significant product launches in the coming years.

For Class II vaccines, which are widely recognized by parents, their preventive nature is nearly a rigid demand. They continuously benefit from the market trend of consumption upgrading. With short and flexible bidding cycles, they are not subject to medical insurance cost controls, face minimal pressure for price reductions, achieve rapid volume growth, and demonstrate significant earnings elasticity.

Data sources: Company financial reports, National Institutes for Food and Drug Control (NIFDC), Guotai Junan Securities Research

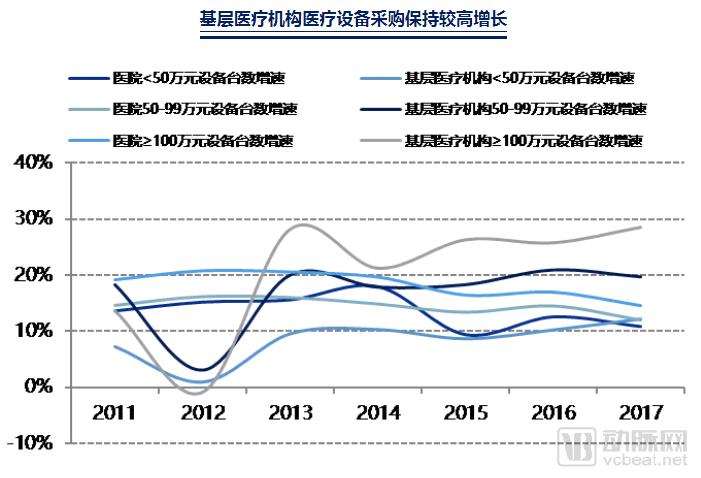

Medical Devices Maintain Rapid Growth

Having discussed pharmaceuticals, let us now turn our attention to the medical device industry.

The medical device industry is highly heterogeneous and can be subdivided into medical equipment, high-value consumables, and in vitro diagnostics (IVD). The hospital equipment market exhibits strong performance, primarily driven by increased demand for primary-care facilities under the tiered diagnosis and treatment system, coupled with accelerated import substitution as leading domestic manufacturers penetrate the high-end segment.

As the tiered diagnosis and treatment system continues to advance, primary healthcare institutions—particularly county-level hospitals—are entering a period of rapid development, which is expected to drive market expansion for the medical device industry serving these facilities.

Data source: Health Statistics Yearbook, Guotai Junan Securities Research

Valuation Repair Scenario 1: Innovative Drugs Transition from Event-Driven to Performance Realization

Investment in innovative drug stocks follows three stages: value discovery, event-driven catalysts, and earnings realization. After the value discovery phase driven by top-level policies from the General Office of the CPC Central Committee and the General Office of the State Council in October 2017, the sector entered an event-driven phase in 2018 with progress in regulatory submissions and approvals. It is expected to enter the earnings realization phase in 2019 as newly approved drugs undergo intensive commercialization. Companies with genuine R&D progress are likely to see their valuations recover. Hengrui Medicine is our top pick.

Valuation Repair Scenario 2: Validated Enhancement of Clear Growth Trajectories for Transforming Companies

The companies undergoing transformation are all former leaders in their respective niche segments. They have already laid out their subsequent product pipelines and possess the material foundation and most of the capabilities required for transformation, but require a 1–2 year validation period. Examples include Huadong Medicine, Livzon Group, Lepu Medical, and Shanghai Pharmaceuticals.

Data Source: Guotai Junan Securities Research

Valuation Recovery Scenario 3: “Certainty” Companies Regain Premium Valuations

Manufacturing and service sectors with consumer attributes, being less correlated with policy, are expected to see their “certainty” premium further reinforced as long as their performance meets or exceeds expectations. Examples include Wolwo Bio-Pharmaceutical, Changchun High-Tech, Aier Eye Hospital Group, Topchoice Medical, and Yuwell Medical.

The above content is excerpted from the following securities research reports already published by Guotai Junan Securities: “Ten Questions and Answers on the ‘4+7’ Volume-Based Procurement,” “Special Report on the Progress of Generic Drug Consistency Evaluation: Imminent Changes and Order Reshaping,” “The New Era of Super Medical Insurance,” and “2019 Pharmaceutical Industry Investment Strategy: Seizing Opportunities in High-Prosperity Segments.” For detailed analysis, including risk disclosures, please refer to the full reports. In case of any ambiguity arising from the excerpts, the content of the full reports shall prevail.