Imported, Premium, and Branded: Key Trends Reshaping China's Maternal & Baby FMCG Market

This article is reprinted from Maternal and Infant Industry Observer, with authorization granted to VCBeat for republication.

Amid the broader context of consumption upgrades and the downward shift in traffic, new consumer mindsets are creating fresh market opportunities, prompting companies to continuously adjust their channel strategies. Furthermore, with the rising proportion of two-child families and shifting consumption preferences among new parents, the maternal and infant market is witnessing numerous emerging trends and opportunities. How can maternal and infant enterprises gain insights into these changes and seize the opportunities? Ni Yi, Vice President of Nielsen China, delivered a keynote presentation titled “New Trends in China’s Infant and Toddler FMCG Sector.” The presentation analyzed the latest dynamics in the current maternal and infant market from perspectives including China’s macroeconomic environment, consumer insights across maternal and infant channels and categories, and future development trends in maternal and infant fast-moving consumer goods (FMCG), providing a reference for the future growth of businesses in this sector.

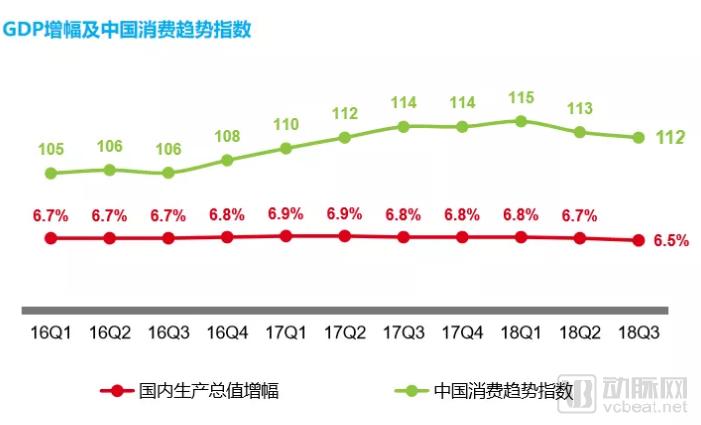

According to the macro consumption trends compiled by Nielsen, China’s Consumer Confidence Index remains relatively high globally, reaching 112 in the previous third quarter, although it has declined compared with the first quarter of 2018. China’s GDP growth rate has remained stable at 6.5%–6.9%, indicating that the overall macro consumer market is still relatively stable.

In addition, the state has also introduced the "Six Stability" policy, which includes:

1. Employment: Keep the urban unemployment rate below 4%;

2. Further standardize the financial regulatory system;

3. Further promote investment and the introduction of foreign capital;

4. Notably, foreign trade showed strong performance, with the total value of imports and exports increasing by 13.8% year-on-year in the third quarter of 2018, which stands out as a highlight from a macroeconomic perspective;

5. Finally, expectations are that continuing to strengthen supply-side structural reforms will still play a certain role in expanding domestic demand.

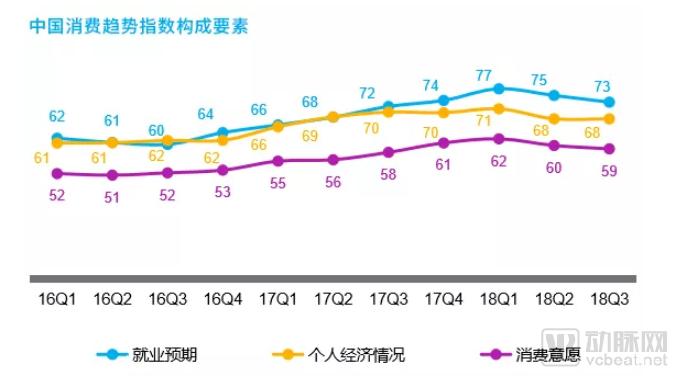

Consumer Trend Index, which mainly consists of three components: first is employment expectations (job security and long-term career prospects); second is personal financial situation (personal employment income and investment returns); lastly, consumer willingness. As can be seen from the chart, in the first quarter of 2018 when the Consumer Trend Index was relatively high, almost all three main indicators were at elevated levels; however, in the past second and third quarters, employment expectations and consumer willingness have declined somewhat, while personal financial conditions have remained stable.

Personal financial conditions have actually benefited from the individual income tax reform, remaining basically stable. Since the implementation of the new individual income tax reform in January 2019, the increase in the tax exemption threshold and the expansion of lower tax brackets have had a very positive impact on personal income. The six special additional deductions have played a positive role in supporting the growth of personal and household expenditures.

Amid the current complex market conditions, Nielsen has conducted quarterly consumer surveys to gain a more objective understanding of consumers. The research results indicate that the proportion of households reporting increased or unchanged consumption expenditures remains relatively high, with no significant trend toward reduced spending observed. Similarly, in terms of the ratio between households increasing and decreasing their expenditures, the proportion of those increasing spending exceeded those decreasing it during the first, second, and third quarters. This continues to send positive signals at the macroeconomic level.

1. Dynamic Tracking of the Maternal and Infant Channels

1) Double-digit growth in the maternal and infant channel, with a significant acceleration in the maternal and infant market

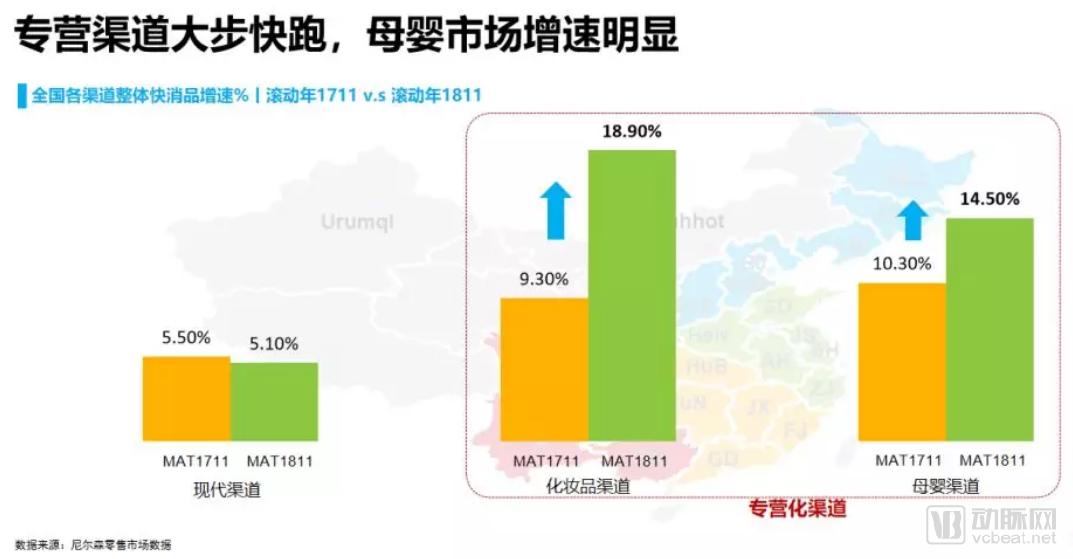

From the perspective of maternal and infant channels, Nielsen collaborates with many such channels, including online and offline retailers, on market data, primarily reflecting point-of-sale data. China’s traditional retail channels mainly include offline formats such as hypermarkets, supermarkets (large and small), and convenience stores, as well as channels unique to China, such as maternal and infant product channels and cosmetics channels.

As shown in the figure, while growth in traditional supermarket and hypermarket channels remained sluggish over the past two years, cosmetics specialty stores and maternal-and-infant product channels continued to sustain robust double-digit growth. This has been a key driver of omnichannel (online and offline) growth in the fast-moving consumer goods (FMCG) sector. Notably, for the maternal-and-infant channel, the year-on-year growth rate continued to expand compared with 2017, reaching 15% as of November 2018.

2) Offline maternal and infant channels remain the primary battleground, with their market share continuing to expand

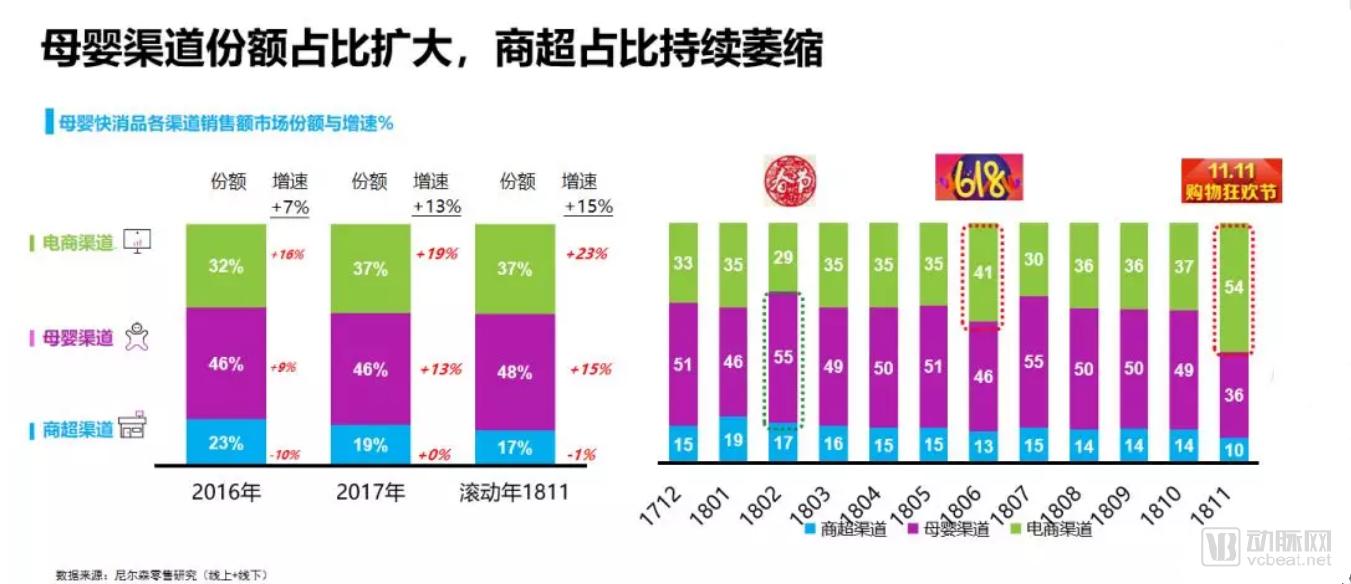

Turning to the omni-channel landscape for maternal and infant products, the three colors represent e-commerce, specialized maternal and infant channels, and supermarket/hypermarket channels, respectively. The chart reveals that, compared to the past two years, offline specialized maternal and infant channels remain the most critical battleground for overall sales of fast-moving consumer goods (FMCG) in this category, accounting for approximately 50% of the market share. This share continues to expand, having grown by 15% over the past year. Meanwhile, online e-commerce has continued its robust growth, with the broader maternal and infant product category increasing by 23% in the past year. These two major channels have essentially driven the growth of the overall retail market for maternal and infant FMCG. Nielsen breaks down the full year into 12 months; monthly data indicates that offline specialized maternal and infant channels constitute the majority of the overall distribution channels for maternal and infant FMCG. However, e-commerce promotional events, such as the Double 11 Shopping Festival, exert certain pressure on offline specialized maternal and infant channels as well as supermarket/hypermarket channels. Nevertheless, during traditional festivals like the Spring Festival, offline specialized maternal and infant channels remain the primary sales driver.

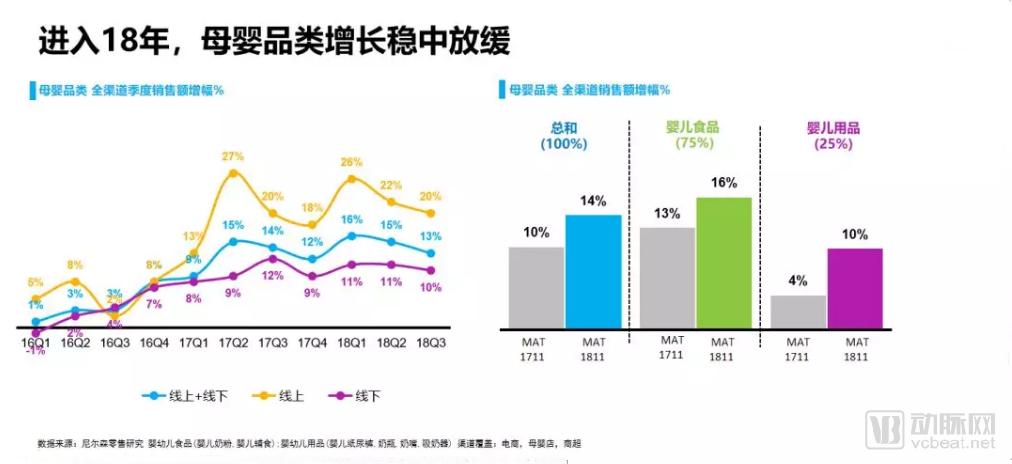

3) Growth in the maternal and infant product category slowed down in 2018

Among omni-channel data, the overall fast-moving consumer goods (FMCG) sector experienced minimal growth in the first, second, and third quarters of 2016. However, by 2018, the FMCG sector achieved robust growth, with an omni-channel increase of approximately 14%. In the maternal and infant products category, a surge was observed from the third quarter of 2016 through the first quarter of 2018, with both online and offline channels largely returning to high double-digit growth rates; online growth exceeded 20%.

However, in recent quarters, particularly the third and fourth quarters, growth is estimated to have slowed. Among various categories of maternal and infant products, baby food remains the leading segment, with a 16% growth over the past year, serving as the primary driver for the growth of fast-moving consumer goods (FMCG) in the maternal and infant sector.

2. Development of Key Maternal and Infant Product Categories

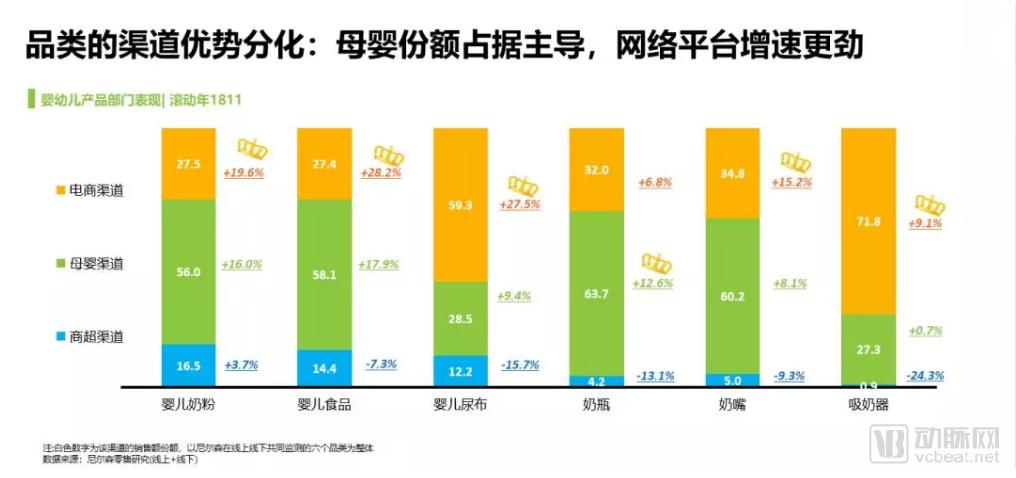

1) Channel Diversification by Category: Maternal and Infant Channels Dominate, While E-Commerce Shows Strong Growth

Breaking down key categories further, there are six major maternal and infant product categories: infant formula, baby food, diapers, feeding bottles, nipples, and breast pumps. The share of these six categories across three major channels varies. For infant formula, baby food, and nipples, the maternal and infant specialty channel accounts for a relatively high proportion, basically reaching around 50%–60%, making it the primary sales channel. Online channels are also accelerating; the growth rates for infant formula, diapers, and nipples online exceed those of the overall maternal and infant specialty channel. However, traditional supermarket and hypermarket channels are essentially in a state of contraction.

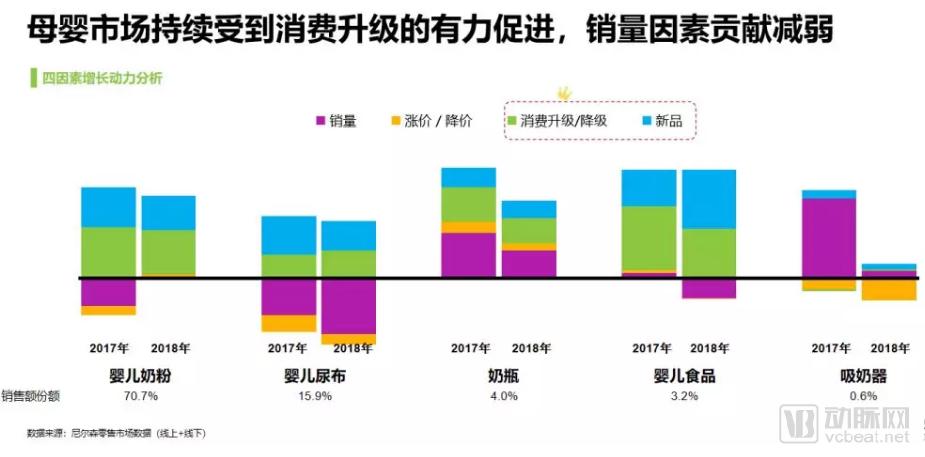

Regarding growth, it is essential to analyze the underlying drivers. From a relatively scientific and quantitative perspective, there are four primary drivers of growth: First, volume—whether more products have been distributed to the market and ultimately purchased by consumers. Second, price—whether overall sales revenue can be boosted through price increases. Third, consumption upgrading, which is the most critical factor. Fourth, new products—whether a significant number of new products are launched into the market with premium pricing, thereby driving growth across the entire category.

2) Consumption Upgrading and New Product Launches Become the Main Drivers of Growth in the Maternal and Infant Market

Compared with the past two years, volume growth has contributed little to the expansion of the five major categories; sales volume has basically made no contribution and has even dragged down overall sales revenue. For instance, the sales volume of leading infant formula brands saw virtually no increase in 2018, with growth driven primarily by consumption upgrades and new product launches. This trend is similarly evident in categories such as diapers, baby bottles, and baby food.

3) Subcategory Trends: Organic Infant Formula Growth Rate Reaches 50%

Notably, consumption upgrades and new product launches are driving growth across the entire maternal and infant care category. A simple example illustrates this: statistical data shows that the growth rate of organic infant formula is significantly higher than that of other categories, reaching nearly 50%. It has become a key sub-segment contributing to the overall infant formula market. In recent years, organic baby food products have also propelled the expansion of the maternal and infant care market.

4) Consumers are increasingly prioritizing quality and international standards

Regarding consumption upgrading, Nielsen primarily analyzes mainstream brands. The top five diaper brands represent a relatively concentrated category, consisting entirely of foreign brands, with a contribution rate approaching 40%, indicating a highly concentrated market. In terms of baby bottles, beyond traditional glass materials, consumers are currently placing greater emphasis on safety, health, and high-quality products. Over the past year, PPSU bottles and silicone bottles have seen growth rates exceeding 30%, driving sales growth in the baby bottle category. PPSU is drop-resistant and heat-resistant, and it does not easily release chemical toxins during heating and sterilization processes, which has significantly boosted consumer demand for such products.

3. Shopper Insights on Maternal and Infant FMCGs

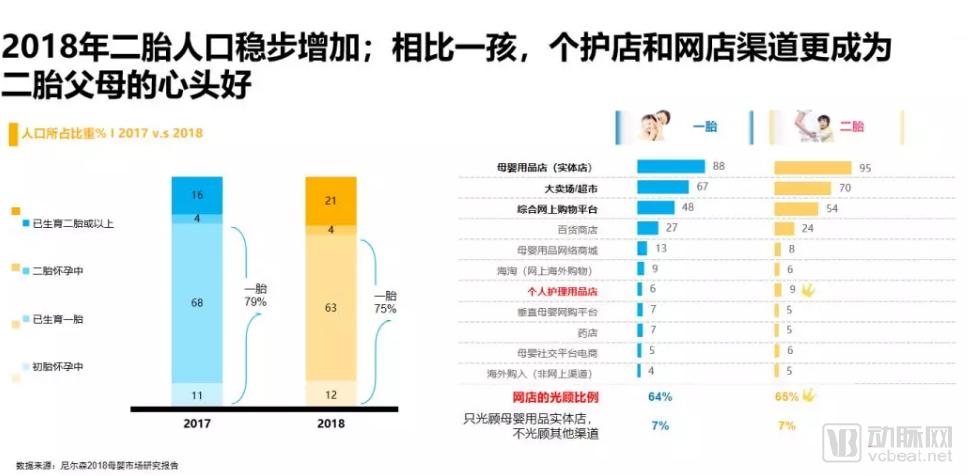

1) Personal care stores become the preferred choice for two-child families, with channels accelerating integration

Regardless of market fluctuations, research on consumers, users, and members remains the core focus. A comparison of maternal and infant consumer data from the past two years shows an increase in the number of second births and a rising proportion of families with two children. When comparing families with one child to those with two, where do they prefer to shop, and why? Through insights gathered over the past year, Nielsen has found that, in addition to traditional maternal and infant channels, supermarkets, and online platforms, families with two children show a stronger preference for purchasing maternal and infant products through personal care product channels. Channel integration is accelerating, encompassing not only the convergence of online and offline channels but also the blending of different types of offline channels.

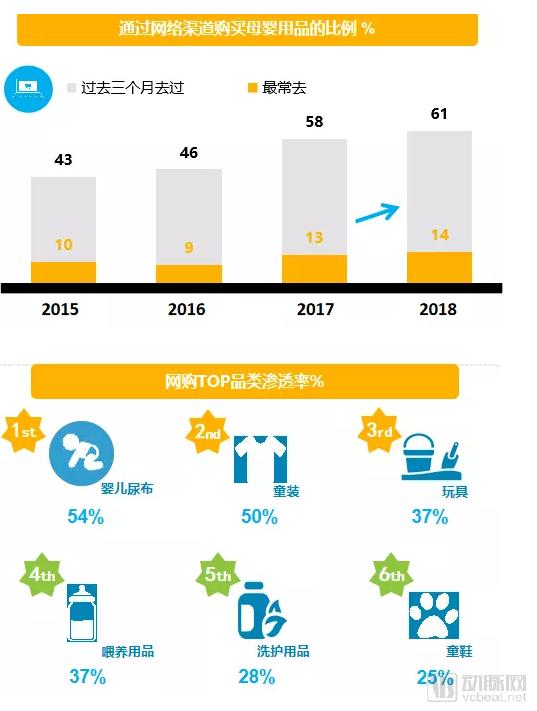

2) Accelerating Increase in Online Channel Penetration Rate

It is worth noting that the impact of online channels on offline retail persists. In recent years, online penetration has accelerated, including both the proportion of consumers who have ever shopped on e-commerce platforms and the share of those making frequent purchases within a month. The top three product categories by online sales are diapers, children’s clothing, and toys, while feeding supplies also represent a significant category in online channels.

3) One-stop services and experiential offerings are becoming increasingly important for offline channels

Although the integration of online and offline channels has been widely discussed, numerous challenges have emerged during this process. From the consumer’s perspective, what factors drive the choice between online and offline purchases, and what are the key differences?

By comparing two years of research data, Nielsen found that consumers’ reasons for purchasing maternal and infant products through online and offline channels are varied. The comparative advantages of online channels lie in instant ordering, time savings, convenience, urban short-haul logistics, timely home delivery, and product comparison. In contrast, offline channels primarily offer comprehensive product categories, authentic goods at fair prices, and a wider selection of brands. Additionally, over the past year, two further factors have become prominent for offline channels: first, whether physical maternal and infant stores can meet consumers’ demand for one-stop services; and second, the experiential aspect, such as designated play areas for babies. Consumers’ preference for offline channels is largely driven by the desire for in-store experiences and by strategies that engage them emotionally to build brand loyalty.

The future development trends of fast-moving consumer goods (FMCG) for mothers and infants will continue to be characterized by importization, premiumization, and branding.

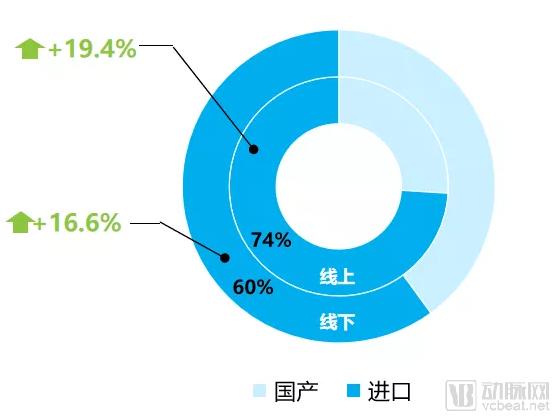

From the perspective of import penetration, we primarily analyze several key weighted categories. Infant formula and diapers are the most significant weighted categories within the maternal and infant FMCG sector. In the infant formula category, imported products still accounted for 60% of offline channel sales over the past year, with a growth rate as high as 16%, continuing to erode the market share of domestic brands. Regarding baby diapers, imported brands have seen further growth, while domestic brands have experienced a slight decline. For other categories with slightly lower weightings, such as baby bottles, nipples, and breast pumps, the market is predominantly dominated by domestic products, which have also achieved solid growth. In terms of channel distribution across the entire infant formula category, imported products hold a 74% share in online channels and a 60% share in offline channels, with growth rates reaching 19% and 16%, respectively, indicating rapid expansion of imported products.

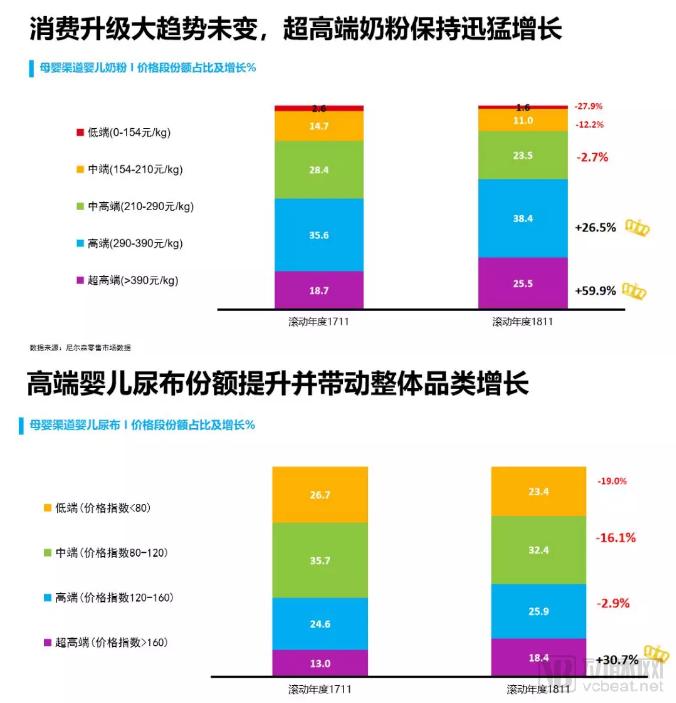

From the perspective of premiumization, an analysis of infant formula price segments reveals that the ultra-premium segment has achieved a 60% growth rate, which will further intensify competition and reshape the landscape of the entire infant formula category. This trend is also evident in the diaper category, where high-end baby diapers priced above RMB 160—equivalent to 1.6 times the market average—have seen a 30% growth rate.

From a branding perspective, both the infant formula and diaper categories exhibit high market concentration. Nearly 80% of the top five leading brands in these sectors are foreign-owned, accounting for approximately 40% of the infant formula market share and nearly 50% of the diaper market. Branding trends are also evident in so-called niche categories, including children’s clothing, infant nutritional supplements, and baby bottles. Notably, the children’s clothing market in China is highly fragmented, with top brands holding only about 10% of the market share, compared to 30%–50% in developed countries in Europe and the United States. This suggests that leading children’s clothing brands may emerge in the future.

China’s overall economy remains relatively stable, while the Chinese fast-moving consumer goods (FMCG) sector continues to lead global growth rates and is on a positive development trajectory. In the maternal and infant market, alongside consumption upgrades, e-commerce will continue its robust expansion. Leading brands will increasingly exhibit trends toward organic positioning, internationalization, and premium quality. For infant-related products, stakeholders should pay closer attention to the trends of importation, higher price points, and premiumization. Over the next three to five years, it is advisable to focus on currently fragmented, highly segmented subcategories within the infant and toddler market, where more leading brands are expected to emerge and consolidate market control.