Cross-Industry Convergence and Mega M&A Signal a New Era in U.S. Pharmaceutical Retail

There have been many hot topics in the U.S. pharmaceutical retail market recently.

In January 2019, Microsoft announced a partnership with Walgreens Boots Alliance (WBA), the largest pharmacy chain in the United States;

In November 2018, U.S. pharmaceutical retail giant CVS Health announced the completion of its acquisition of Aetna, with a transaction value of $70 billion;

In September 2018, Cigna’s $52 billion acquisition of Express Scripts, the largest independent pharmacy benefit manager (PBM) and pharmaceutical retail company in the United States, was approved;

In June 2018, Amazon announced the acquisition of online pharmacy PillPack for nearly $1 billion, a company that had been in existence for less than five years.

Two Major Trends in the U.S. Pharmaceutical Retail Industry Can Be Summarized from News Reports:

1. Cross-industry collaborations are becoming increasingly frequent, with closer ties between pharmaceutical retail and medical insurance, healthcare services, and even internet giants, giving rise to a continuous emergence of new service models;

2. Entering a period of heightened M&A activity, acquisitions and mergers are occurring frequently with substantial transaction values. These deals have transcended typical intra-industry consolidation, with an increasing number of transactions involving vertical integration along the upstream and downstream segments of the industry chain.

“Using others as a mirror helps one understand gains and losses.” Due to differences in healthcare security systems, the U.S. industry landscape will not be 100% replicated in China; however, the fundamental laws governing industrial evolution remain the same. In other words, understanding why the U.S. pharmaceutical retail market is “turbulent” and the underlying reasons behind it may provide valuable guidance for industry development.

The structure of this article is as follows:

1. Interpretation of Dynamics in the U.S. Pharmaceutical Retail Industry: Giants Rush to Enter the Market;

2. Analysis of the Macro Environment of the U.S. Pharmaceutical Market: The Path to Integration Has Just Begun;

3. New technologies accelerate the transformation of traditional industries: cloud computing, big data, IoT, mobile internet, AI, and blockchain;

4. The Future Landscape of the Pharmaceutical Industry: From Products to Solutions.

Let’s take a detailed look at the recent hot topics in the U.S. pharmaceutical retail industry. First is the partnership between Microsoft and Walgreens Boots Alliance (WBA) announced in January. One of the key players, Microsoft, the world’s largest operating system and software company, recently surpassed Apple to become the most valuable company globally by market capitalization. Its secret weapon for growth has been cloud services and artificial intelligence (AI). Walgreens Boots Alliance is the parent company of Walgreens, formed in 2014 through the merger of U.S. pharmacy chain giant Walgreens and UK-based pharmaceutical distributor Alliance Boots. Following the merger, it became the world’s largest publicly traded company primarily engaged in pharmaceutical retail and distribution, with a market capitalization of nearly $70 billion.

Walgreens Boots Alliance (WBA) currently operates in 25 countries and regions worldwide, primarily in the United States and the United Kingdom. It owns 18,500 pharmacies, including nearly 10,000 in the United States, over 2,000 in the United Kingdom, and more than 1,000 in Mexico. The company maintains over 390 pharmaceutical distribution centers and employs 415,000 people. Its revenue in 2017 amounted to $131.54 billion. Walgreens Boots Alliance is also a shareholder of AmerisourceBergen, the largest pharmaceutical distributor in the United States, and Guoda Drugstore, the largest pharmacy chain in China.

The collaboration between Microsoft and Walgreens Boots Alliance primarily includes the following: Walgreens Boots Alliance will migrate its IT systems to the Microsoft Azure cloud platform, with all employees granted access to the Microsoft Office suite; Microsoft and Walgreens Boots Alliance will jointly seek new partners in the pharmaceutical industry to build a healthcare service network; and they will co-develop chronic disease management solutions, supported by Microsoft’s cloud services and AI technologies. Additionally, Walgreens Boots Alliance will launch “Digital Health Corners” in 12 pharmacy locations to sell digital health hardware.

The “marriage” between Microsoft and Walgreens Boots Alliance is a long-term plan that will last for seven years. Both companies attach great importance to this partnership, with Microsoft CEO Satya Nadella and Walgreens Boots Alliance Executive Vice Chairman and CEO Stefano Pessina jointly endorsing the collaboration. Outside observers believe the primary aim of this alliance is to confront their common “enemy,” Amazon, which competes with both companies in cloud services and pharmaceutical retail, respectively. The cooperation represents a new direction for both firms: Microsoft can leverage the opportunity to deepen its presence in the healthcare industry, while Walgreens Boots Alliance will be able to provide more services to its customers.

Walgreens Boots Alliance CEO Stefano Pessina (left) and Microsoft CEO Satya Nadella (right). Image source: Microsoft official website

Furthermore, we must address the transformations in the U.S. pharmaceutical retail and PBM sectors. Whether it is CVS’s acquisition of Aetna or Cigna’s merger with Express Scripts, these developments are clear evidence of the changes reshaping this landscape. Positioned between payers (including public health insurance and commercial insurers) and pharmacies is a key intermediary: the Pharmacy Benefit Manager (PBM). PBMs are responsible for reviewing and adjudicating patient prescriptions and channeling medication demand to retail pharmacies (sometimes fulfilling orders directly via mail-order delivery). As a product of the U.S. healthcare system, PBMs were established primarily to control costs, with their core operational logic centered on centralized drug distribution.

CVS is the largest pharmacy benefit manager (PBM) in the United States, managing over 90 million members and processing more than 4 billion prescriptions annually. Express Scripts (ESI) was previously the largest independent PBM. The acquisition of Aetna by CVS, as well as the merger between Cigna and ESI, were driven by multiple factors, including further declines in pharmaceutical profits (as discussed below, outpatient channel prescriptions are dominated by generic drugs, whose profit margins continue to shrink) and the natural synergies among insurance, PBM, and pharmaceutical retail businesses.

The tech giants’ entry into the pharmaceutical retail sector is another significant factor—particularly Amazon. Aspiring to dominate more than just online retail, the e-commerce giant has been striving to reshape the healthcare ecosystem by leveraging its strengths and expertise to disrupt every link in the medical chain, from pharmaceutical supply chains to health insurance management. By introducing unconventional business models, logistics, and information technology infrastructure, it aims to enhance customer satisfaction within the industry.

Amazon’s moves in the healthcare sector include: In early 2018, Amazon announced a partnership with JPMorgan Chase and Berkshire Hathaway to establish a joint venture focused on healthcare; prior to this, Amazon acquired the online pharmacy PillPack for nearly $1 billion. Looking ahead, Amazon’s healthcare strategy may extend deeply into pharmacies, laboratory testing centers, urgent care, and health benefits, posing a significant threat to the relatively “traditional” retail pharmacy and health insurance industries.

Speculation on Amazon's Healthcare Strategy

Source: CB Insights

Insurance, PBM, and pharmaceutical retail are beginning to consolidate, while tech companies are showing interest in the pharmaceutical industry. The landscape of industry consolidation is emerging, and the following analysis will explore the reasons behind these changes.

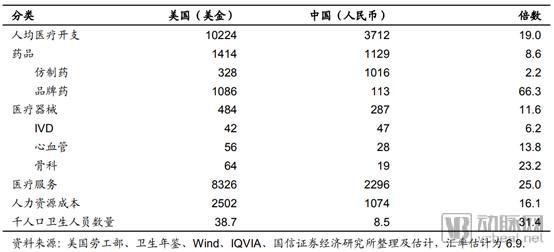

Integration has been the dominant theme in the U.S. pharmaceutical market recently, primarily driven by a mature macroeconomic environment. First, let us examine the U.S. pharmaceutical market from the perspective of healthcare expenditures. According to comprehensive data compiled by Guosen Securities Economic Research Institute, per capita healthcare spending in the United States amounted to USD 10,224 in 2017, compared with RMB 3,712 in China.

Per capita healthcare spending in the United States is 19 times that of China. However, for generic drugs, the ratio is only 2.2 times. Meanwhile, spending on medical services (excluding medical devices and pharmaceuticals, but including insurance and other service-related categories) reaches 25 times that of China.

Per Capita Healthcare Expenditure in the United States and China: A Rough Breakdown

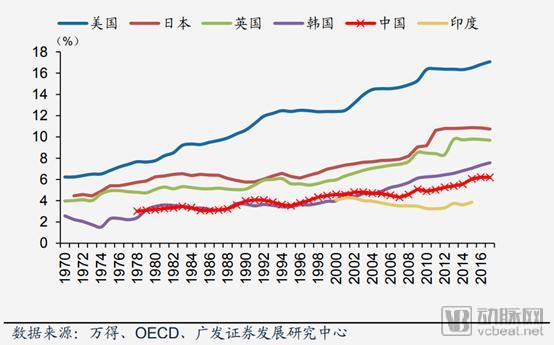

Healthcare Expenditure as a Percentage of GDP in Selected Countries

From a growth perspective, U.S. healthcare expenditure has already accounted for approximately 18% of GDP, leaving limited room for future expansion and primarily offering opportunities for structural adjustment. In contrast, China’s figure stands at below 5%, indicating substantial growth potential.

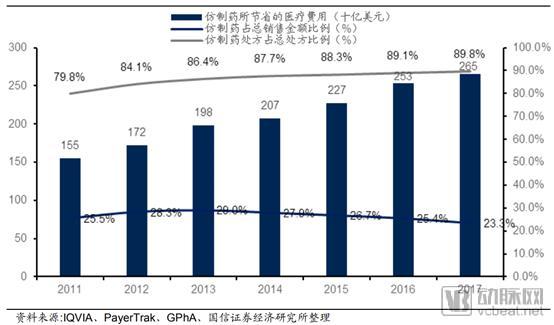

As the country with the highest global pharmaceutical expenditure, the United States has seen a continuous increase in the volume of generic drugs used, while consumer spending on them has steadily declined. In 2017, generics accounted for 90% of prescription volume but only 23% of sales revenue.

In the United States, nearly half of generic drugs achieve cost savings rates of 76%–100%, meaning their prices are reduced by approximately three-quarters compared to those of originator drugs. In contrast, half of the generic drugs in China yield cost savings rates of only 1%–25%, reflecting a situation characterized by “high prices, high gross margins, and high marketing expenditures.” To address quality and pricing issues associated with generic drugs, relevant authorities have successively introduced the Generic Drug Consistency Evaluation policy and the Volume-Based Procurement policy.

Proportion of Generic Drug Prescription Volume and Sales in the United States, 2011–2017

The rapid launch of new products is a key reason why it is difficult for generic drugs in the United States to achieve excess profits. From 2000 to 2010, the U.S. FDA approved an average of 23 new drugs per year; since 2010, this figure has risen to nearly 36 approvals annually. The rise of biologics and small-molecule targeted therapies has led to the development of more new drugs than in the past.

From the perspective of pharmaceutical distribution channels, the United States exhibits a high degree of separation between prescribing and dispensing, coupled with a robust prescription management system, resulting in a terminal distribution structure that differs significantly from that of China. Based on sales volume, the ratio of in-hospital to out-of-hospital channel sizes in the U.S. pharmaceutical market is approximately 3:7. Major out-of-hospital channels include retail chain pharmacies, independent pharmacies, PBM mail-order services, and mass merchant/supermarket pharmacies.

In terms of market share, chain pharmacies account for over 40%, while the share of independent pharmacies is gradually declining to around 15%. PBM mail-order services hold a 25% share, and supermarkets and specialty pharmacies account for 20%.

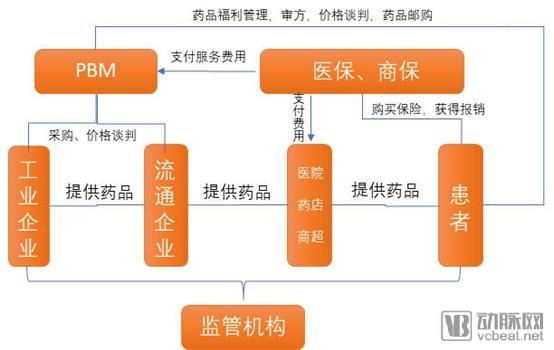

From the perspective of roles within the industry chain, the healthcare supply chains in the United States and China inevitably involve similar stakeholders, including the government, health insurance agencies, pharmaceutical and medical device manufacturers, distributors, and healthcare service providers. The key difference lies in the fact that commercial insurance is highly developed in the U.S., accounting for a significant proportion of total healthcare expenditure. Consequently, there is a direct demand for cost containment, which has led to the development of sophisticated cost-control mechanisms, such as Pharmacy Benefit Managers (PBMs) and Diagnosis-Related Groups (DRGs).

Roles in the Pharmaceutical Industry Chain

Taking DRGs as an example, the version currently implemented in the United States is Medicare DRGs, which includes 26 Major Diagnostic Categories (MDCs) and 989 diagnosis-related groups. In the U.S., the DRG system is highly suitable for treating patients with short-term hospital stays, as the average length of stay for non-chronic maintenance conditions is very short, and the variation in medical costs among different patients is relatively small. Conversely, conditions treated in psychiatric and rehabilitation hospitals, which typically involve longer average lengths of stay, are excluded from the scope of this payment model.

In summary, the primary drivers behind the consolidation of the U.S. pharmaceutical market.

First, U.S. healthcare expenditures have already accounted for a very high proportion of GDP; steady growth will replace rapid expansion.

The industry model has become highly mature, as seen in sectors such as generic drugs, health insurance, and pharmaceutical retail; scale adjustment has replaced innovation in technology, products, and service models.

Mature capital operation models, industrial accumulation, and convenient financing channels provide ample funds for mergers and acquisitions.

The synergies generated by the integration of upstream and downstream segments in the industrial chain will create new profit margins. This is particularly evident in closely linked business areas such as active pharmaceutical ingredients (APIs) and generic drugs, medical insurance and cost containment, and pharmaceutical retail and insurance, where scale effects are significant and integration challenges are relatively low.

New technologies have reduced management complexity; information technologies such as cloud services and collaborative office platforms have facilitated cross-industry and cross-regional management, thereby lowering the difficulty of integration post-consolidation.

At its core, the pharmaceutical and medical device industry is strongly technology-driven. Whether for drugs or devices, the foundation of innovative companies lies in the discovery and successful commercialization of specific technologies or technological categories, such as large-scale medical equipment and novel therapies. However, the healthcare industry is also “traditional” in nature, with technological iterations often measured in decades rather than years, and requiring extensive clinical trials and data support to secure regulatory approval.

As emerging technologies such as cloud computing, big data, the Internet of Things, mobile internet, and artificial intelligence mature and are increasingly deployed within vertical industries, they will accelerate the transformation of the traditional pharmaceutical sector. Taking the U.S. market as an example, cloud service providers in the life sciences space include established players like Oracle as well as newer entrants such as Veeva.

Since its founding in 2007, Veeva’s clientele has encompassed nearly all of the Top 20 pharmaceutical companies, with revenues reaching $685.6 million in 2017. The company’s business truly took off after the iPad was launched in 2010. Suddenly, 95% of pharmaceutical sales representatives were using iPads, and Veeva’s cloud-based CRM software, tailored specifically for the pharmaceutical industry, proved highly suitable for both the devices and the representatives.

The same holds true for big data. During the 2018 Spring Festival, Roche announced its plan to acquire Flatiron Health, a cancer big data company, for $1.9 billion. Founded in 2012, Flatiron Health has been dedicated from its inception to leveraging big data analytics to support cancer treatment. It is a market leader in both electronic health record (EHR) software and real-world evidence (RWE) management within the oncology field.

Not to mention the Medical Internet of Things (IoMT), which enables the convenient collection of data from both patients and healthy individuals through ubiquitous sensors. This data can be used to optimize and adjust existing products or services, while also creating new demands—such as continuous data monitoring or interpretation, and personal care.

Mobile internet has primarily transformed the marketing approaches of pharmaceutical companies. Abroad, pharmaceutical firms began experimenting with digital marketing at an early stage, with many establishing dedicated digital marketing departments. According to a survey previously released by PwC Strategy& involving more than 150 executives from European and American pharmaceutical companies, 90% of these enterprises have extensively promoted or piloted the use of digital tools as one of their marketing channels to deliver information and services related to diseases, products, cutting-edge academic technologies, and medical education.

The potential of artificial intelligence in the healthcare industry has been fully demonstrated: from the perspective of pharmaceutical R&D, it can be applied to target discovery, molecular design, and clinical research; from the perspective of diagnosis and treatment services, it can be utilized in intelligent triage, medical imaging, assisted diagnosis, and post-discharge follow-up; as well as in public health decision-making and medical cost control.

While blockchain technology is still in its early stages, it has demonstrated significant potential in clinical research and data sharing, pharmaceutical supply chains, prescription management, and healthcare payments. Major pharmaceutical companies such as Pfizer, Novartis, Roche, Merck & Co., and Sanofi are already integrating blockchain into their pharmaceutical operations. In China, Alibaba Health is applying blockchain in the construction of medical consortiums, while Yilian is leveraging it for supply chain finance. The decentralized, traceable, and tamper-resistant nature of blockchain aligns closely with the security and regulatory requirements of the pharmaceutical industry.

In *The Innovator’s Prescription*, Chris Stimson puts forward the view that, in the future, pharmaceutical companies will provide not just products but comprehensive solutions centered on diseases. This is particularly true in the era of precision medicine and wearable devices, where molecular- and gene-level diagnostics can clearly identify the causes of diseases, while wearable devices can continuously track behavioral data and enable timely interventions in lifestyle habits. This constitutes a truly “patient-centered” value-based healthcare system, with solutions that are highly personalized for each individual.

Although this scenario is still some distance away, the pharmaceutical industry is moving in the right direction: for example, GlaxoSmithKline’s partnership with the genetic testing company 23andMe, and Roche’s strategic investments in genetic testing and diagnostic equipment. Moreover, pharmaceutical companies are extensively collaborating with various technology firms across areas such as R&D, payment solutions, and patient education and science popularization.

Concurrently in China and the United States, tech giants are increasingly penetrating the healthcare industry. Google has three subsidiaries in the healthcare sector: Verily, DeepMind, and Calico. Verily focuses on improving healthcare through data analytics tools, interventions, and research; DeepMind has become synonymous with artificial intelligence in healthcare; and Calico is dedicated to researching and combating aging and age-related diseases. Meanwhile, Google has also strategically invested in multiple projects, including Oscar Health, Fossil Group, and XtalPi.

Apple has also adopted a “first-party + third-party” approach in the healthcare sector. It offers data platforms such as HealthKit, ResearchKit, and CareKit, providing data interfaces for medical software developers. The Apple Watch, synonymous with smart devices, is highly anticipated for its prospects in electrocardiogram (ECG) monitoring. Meanwhile, Apple has invested in Beddit, a smart sleep-monitoring hardware company, and Gliimpse, a patient data platform.

In China, Alibaba and Tencent are the two companies most worthy of attention. Alibaba operates its flagship platform, Ali Health, which encompasses pharmaceutical retail, smart healthcare, health management, and product traceability, along with Alipay’s “Future Hospital” initiative and Alibaba Cloud’s medical cloud services and AI capabilities. Tencent, meanwhile, runs businesses such as its AI Laboratory’s Miying (Shadow) project and Tencent Yidian. The two companies have invested more than RMB 3 billion in the healthcare sector, funding hundreds of projects.

The recent collaboration between Microsoft and Walgreens Boots Alliance (WBA) can be interpreted from two perspectives. First, the market for information technology services in the healthcare sector is enormous, attracting strong interest from tech giants such as Microsoft, Amazon, and Google. Second, for offline retail chains like WBA, the key challenge lies in driving foot traffic to stores and enhancing the range of services offered to customers. This explains why WBA had previously partnered with Google’s Verily. For these two parties from different industries, the relative strategic importance of this partnership may be immediately apparent.

What defines an excellent enterprise is its ability to hit the right beats amidst the changing times. Recent developments in the U.S. pharmaceutical retail sector indicate that the industry has reached a critical juncture for business model adjustment. Cross-industry integrations aimed at service upgrades are beginning to emerge, with product or service providers increasingly inclined to deliver services (or solutions) to end-users through centralized approaches. This trend not only offers greater convenience to end-users but also provides cost and scale advantages to service providers.

For pharmaceutical companies engaged in large-scale investment and M&A within China, is it possible to look beyond single-industry consolidation and explore cross-industry, solution-driven integration opportunities?