Riding the Surge: 2018 Global Healthcare Investment Report Amid Market Winter – 1,410 Deals and $38.8 Billion in Funding

Key Points of the Report

1. Investment and financing activity in the healthcare sector continues to heat up, while the growth rate of average deal size slows down;

2. Major investment and financing rounds remain at Series A or earlier, indicating substantial growth potential for startups;

3. Overseas biotechnology continues to lead the entire industry, driving rapid development in the healthcare sector; however, China’s pharmaceutical industry has overtaken biotechnology to become the most attractive sector for investment.

4. Although China has surpassed the United States in the number of investment and financing events, the U.S. remains the global center for development in the healthcare sector; India has emerged as a strong contender, overtaking the United Kingdom to rank third in the number of investment and financing events;

5. There remains a significant gap in the average investment and financing amounts between China and the United States; in the U.S. healthcare sector, financing deals involve higher amounts and occur at later stages, indicating a markedly more mature development landscape compared to China’s healthcare sector.

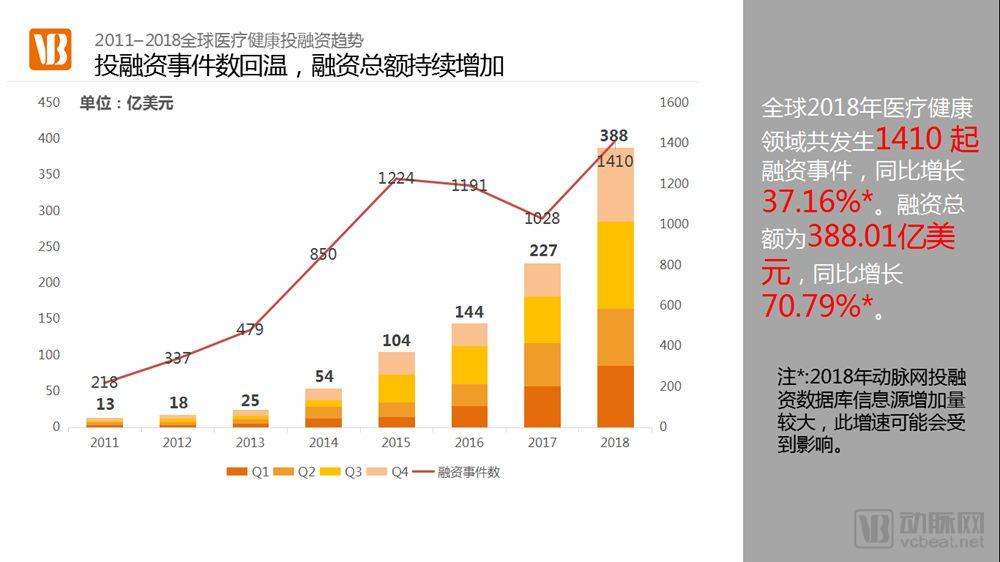

In 2018, there were a total of 1,410 global investment and financing events, marking a rebound from the consecutive declines observed in 2016–2017 and surpassing previous historical highs. The total amount of investment and financing reached $38.801 billion, representing a year-on-year increase of 70.79% and sustaining the rapid growth trend seen in recent years.

Despite simultaneous growth in both the number of financing events and the total amount invested, the average financing size continued to grow by 24.52%, reaching a new high of $27.52 million. Although this growth rate represents a significant decline from the 82.31% recorded in 2016–2017, it is still commendable for the healthcare sector, where early-stage financing continues to account for the majority of transactions.

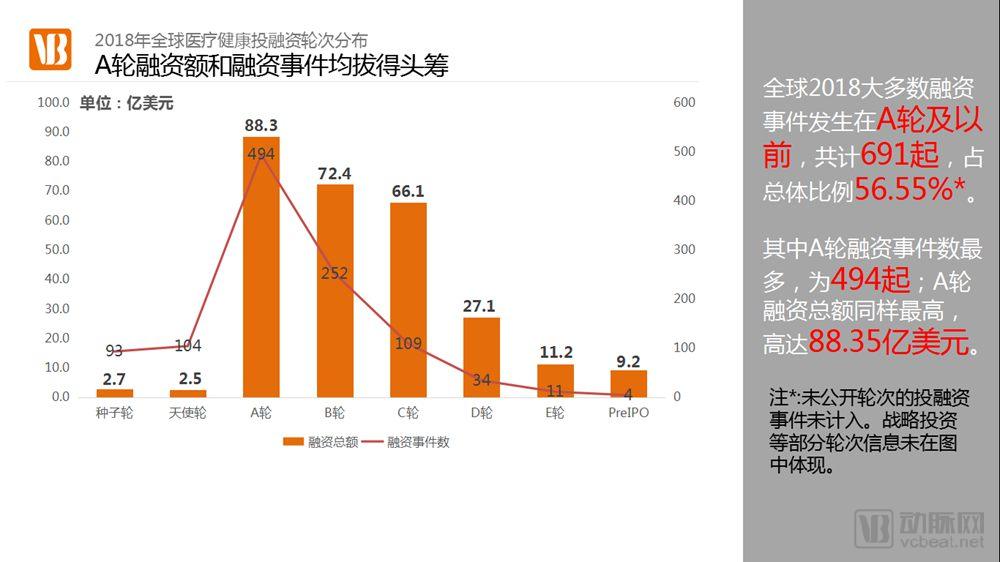

In 2018, global investment and financing activities were still dominated by Series A and earlier rounds, accounting for 56.55% of the total (unannounced rounds were excluded).

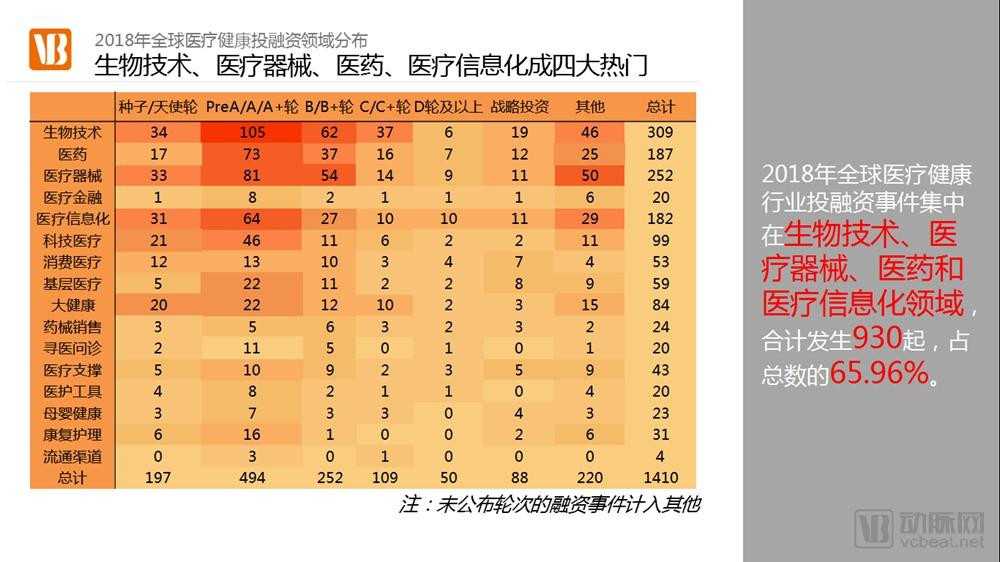

Biotechnology continues to lead the industry with 309 investment and financing events and a total funding amount of $13.8 billion, twice that of the second-ranked pharmaceutical sector. The average financing amount in medical finance reached $150 million, making it the sub-sector with the highest single transaction value. Most sub-sectors showed growth trends, and the overall distribution of investment and financing remained basically the same as in 2017.

The top 10 investment institutions with the highest number of investment deals globally in 2018 each participated in more than 15 transactions. Meanwhile, these firms focused their attention on two specific sectors: biotechnology and pharmaceuticals.

Investment and financing enthusiasm in the biotechnology industry has continued to rise in recent years, reflecting capital’s recognition of technological value. Companies in the pharmaceutical sector that have attracted investor interest are predominantly those with biopharmaceuticals and immunotherapies as their core offerings. The biopharmaceutical industry demonstrated strong fundraising competitiveness in 2018, and this trend is expected to intensify in the future.

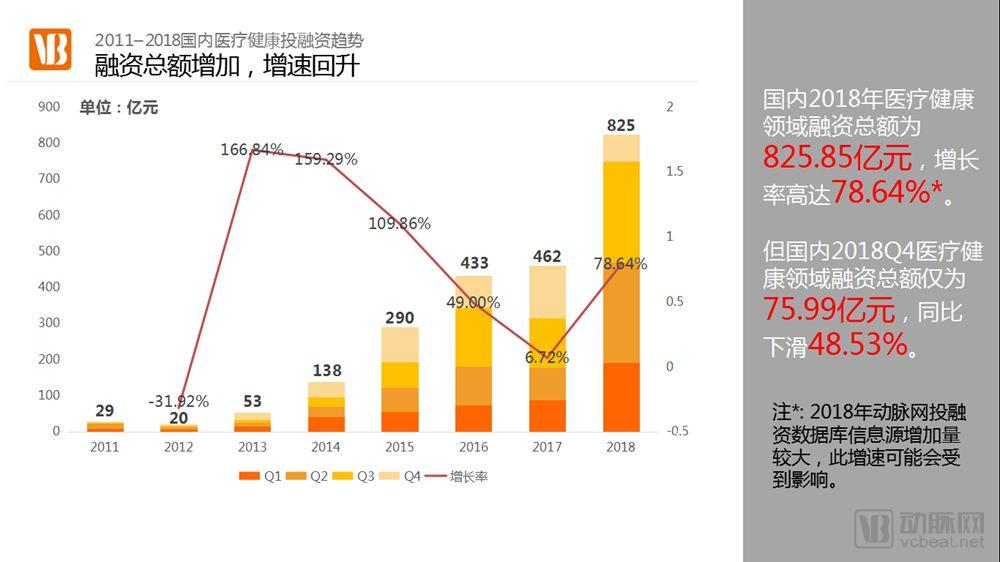

In 2018, the total financing amount in China’s healthcare and medical sector surged again, reaching RMB 82.585 billion, with a growth rate of 78.64%. However, in Q4 2018, the total financing in the healthcare and medical sector amounted to only RMB 7.599 billion, representing a year-on-year decline of 48.53%.

The pharmaceutical industry was a major driver of the significant surge in total investment and financing in 2018; additionally, the medical finance sector emerged as another key growth point that year.

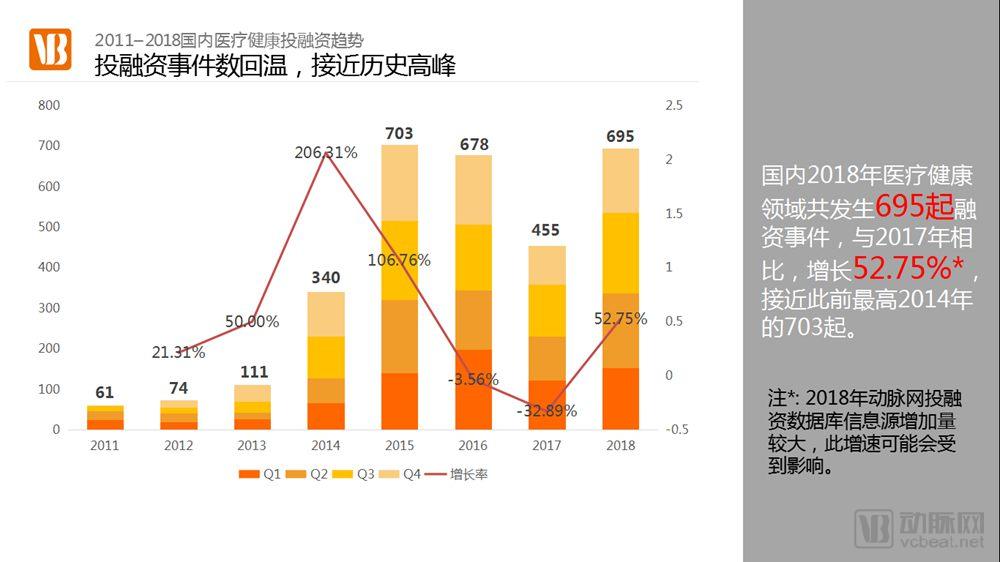

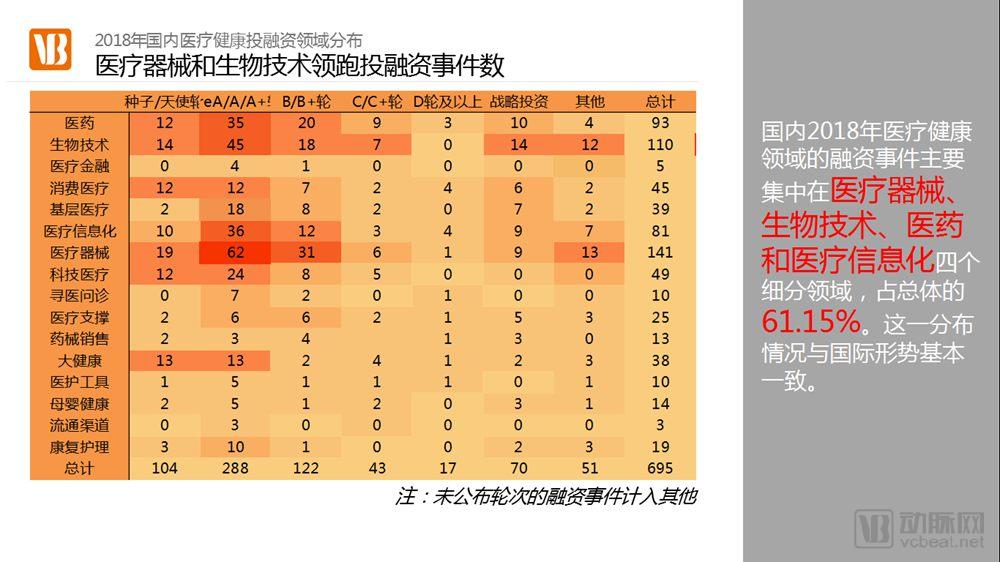

The number of domestic investment and financing events, after a significant decline in 2017, rebounded to 695 in 2018, just 8 short of the historical peak recorded in 2014.

The medical device industry played a significant role in this bottoming-out and rebound, while most industries also demonstrated an increase in the number of financing and investment events.

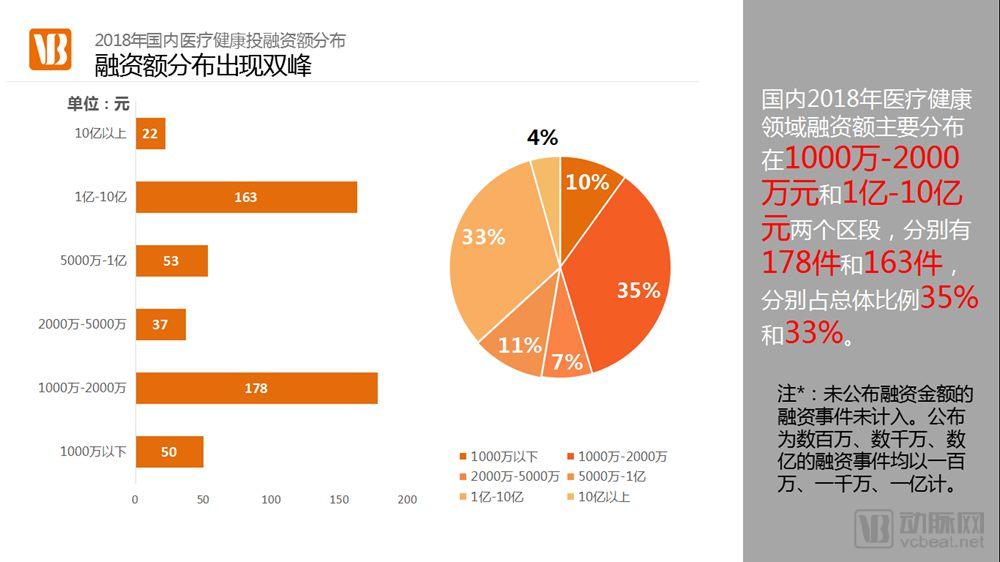

The distribution of domestic investment and financing amounts exhibits a bimodal curve, with peaks observed in the RMB 10 million–20 million and RMB 100 million–1 billion ranges.

Investment and financing deals valued between RMB 10 million and RMB 20 million occurred primarily during the angel to Series A stages. Beyond biotechnology, significant activity was observed in the subsectors of medical devices, healthcare informatization, and digital health. Last year, novel wearable devices and big data-based intelligent analytics attracted substantial funding, sparking another surge in investment and financing within the medical device and healthcare informatization segments.

The other peak, ranging from 100 million to 1 billion, exhibits greater diversity. Financing rounds are distributed across all stages, from angel rounds to Series E, and the investment sectors cover the vast majority of niche areas.

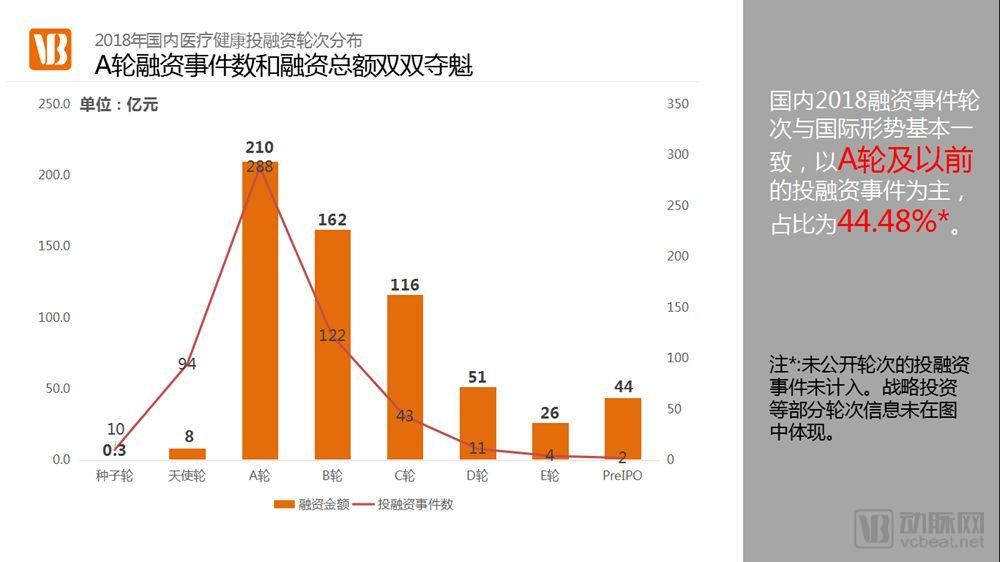

The landscape of domestic investment and financing rounds is largely consistent with the international trend, with nearly half of all deals occurring at Series A or earlier stages.

In 2018, domestic investment and financing activities were primarily concentrated in four sectors: medical devices, biotechnology, pharmaceuticals, and healthcare informatics. Among these, biotechnology, medical devices, and healthcare informatics largely maintained their historical development trends, with growth proceeding as expected, resulting in a steady but unspectacular performance.

In 2018, both the total investment and financing amount and the number of investment and financing events in the pharmaceutical industry experienced rapid growth, with growth rates reaching 210% and 245%, respectively. This sudden surge in the pharmaceutical sector was likely driven by national policies. Drug approval reforms and the “4+7” volume-based procurement program introduced new growth drivers for the entire pharmaceutical industry while also bolstering investor confidence. However, as the market environment gradually stabilized and the industry landscape settled, it became difficult for the pharmaceutical sector to sustain the high levels of financing seen in 2018. Investment and financing in the pharmaceutical industry are expected to decline slightly in 2019 and gradually return to previous levels in the following years.

The healthcare finance sector secured a total of RMB 8 billion in funding in 2018, with Ping An Health Insurance’s Series A round accounting for over 95% of this amount. In February 2018, Ping An Health Insurance raised USD 1.15 billion in its Series A financing, becoming a unicorn in the healthcare finance industry.

Ping An Health Insurance Technology is a member of the “Healthcare and Wellness” segment under Ping An Group. Its business primarily serves China’s medical insurance and health administration systems, commercial insurers, healthcare institutions, and the pharmaceutical distribution sector. Committed to building a technology-driven managed care service platform, Ping An Health Insurance Technology focuses on leveraging technology to advance product development and service innovation. Reportedly, the company is currently employing “cloud governance” as a strategic approach, driven by Ping An’s suite of advanced technologies—including biometric recognition, artificial intelligence, blockchain, cloud computing, and big data—to deploy applications across the healthcare sector, integrate medical services, pharmaceuticals, and medical insurance, and address the longstanding challenges facing these three interconnected domains.

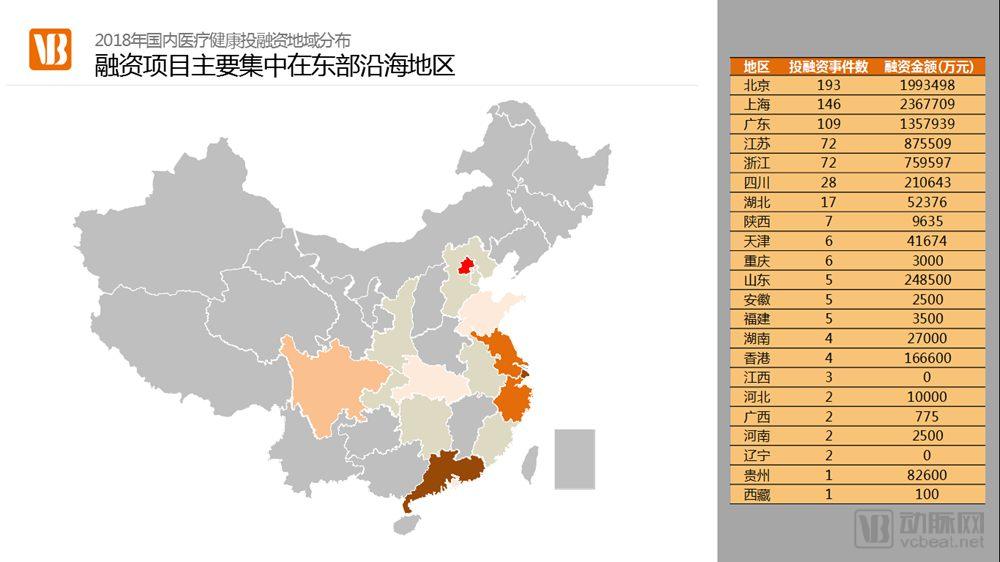

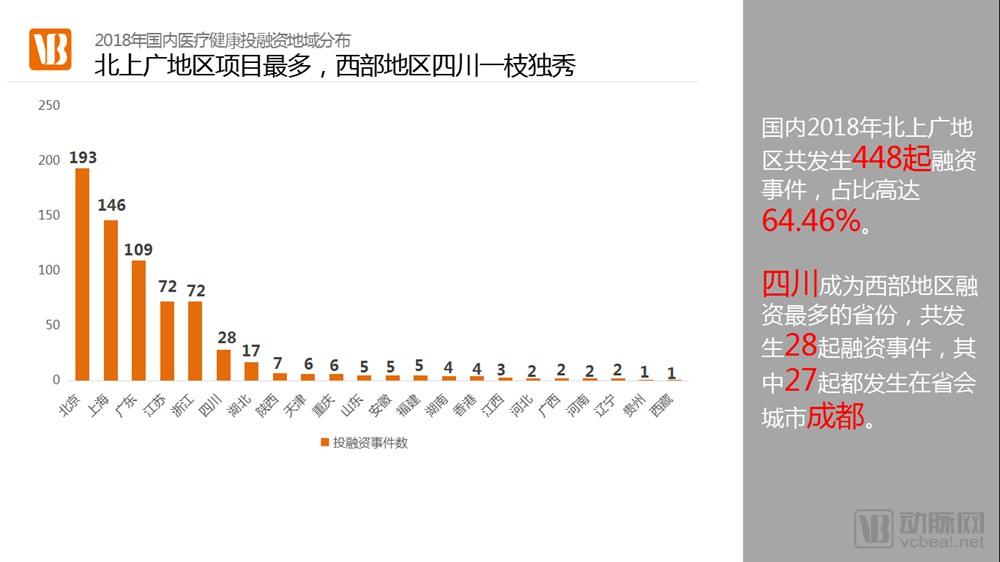

The eastern coastal regions remained the primary areas for domestic investment and financing activities in 2018, with Beijing, Shanghai, and Guangdong each recording total investment and financing amounts exceeding RMB 10 billion and more than 100 deal transactions. In addition to the eastern coastal regions,

Sichuan Province has emerged as the hub of healthcare in western China. Of the 28 investment and financing transactions that took place in Sichuan in 2018, 27 occurred in its provincial capital, Chengdu, featuring prominent companies such as 23Mofang and Leading Pharma.

Top 10 Domestic Financing Deals in 2018: All Exceeded $150 Million (Over RMB 1 Billion) Among them, HEC Pharm and Innovent Biologics have already been listed on the Hong Kong Stock Exchange, while CStone Pharmaceuticals has also submitted its IPO application to the Hong Kong Stock Exchange.

At the end of 2017, the Hong Kong Stock Exchange (HKEX) announced rules permitting pre-revenue and unprofitable biotechnology companies to list in Hong Kong. On August 31, 2018, the China Securities Regulatory Commission (CSRC) also stated that it would guide innovative enterprises in sectors such as biopharmaceuticals—those not yet profitable or with accumulated deficits—to list domestically. The gradual relaxation of listing requirements has made initial public offerings (IPOs) an increasingly attractive option for a growing number of biopharmaceutical companies. Consequently, it is expected that more biopharmaceutical firms will leverage large-scale financing as a springboard to pursue IPOs in the near future.

Top 10 Investors by Number of Financing Deals in China’s Healthcare Sector in 2018, Each Participating in More Than 10 Deals. Compared with the global landscape, top-tier investors in China have a relatively diversified focus. In addition to biotechnology and pharmaceuticals, sectors such as medical devices, consumer healthcare, and health tech have also attracted considerable investment interest.

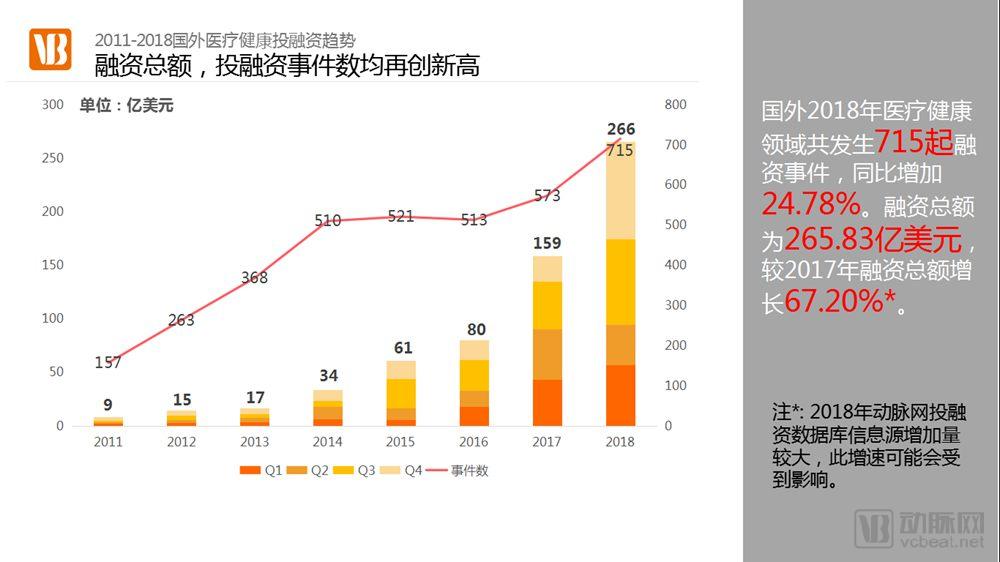

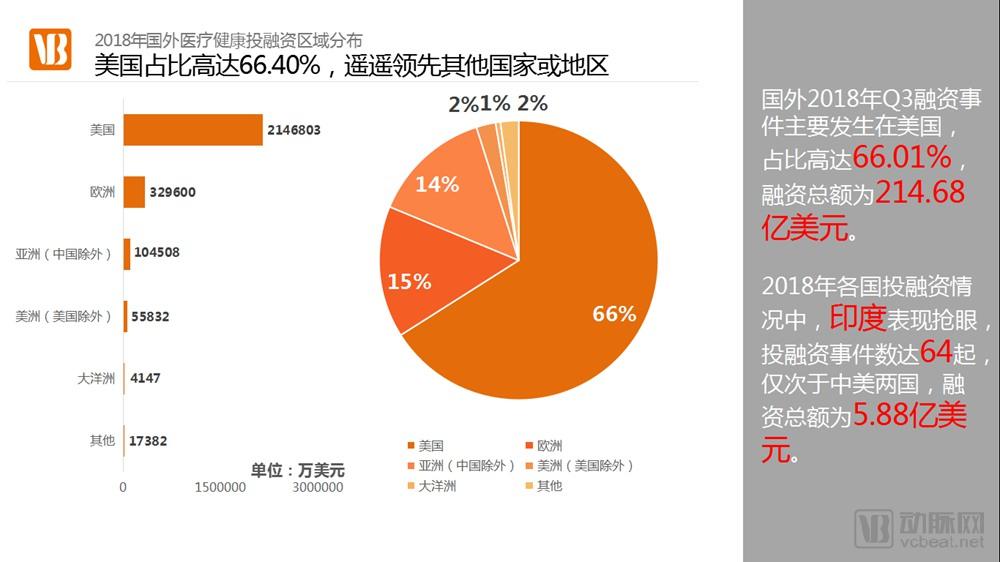

In 2018, a total of 715 financing and investment events occurred overseas, with the total amount raised reaching $26.583 billion.

Compared with 2017, both the number and total amount of overseas investment and financing activities have shown significant growth, with growth rates of 24.78% and 67.20%, respectively, maintaining the consistent trend of rapid expansion.

The United States remains the center of the global healthcare industry, with total financing and investment reaching $21.468 billion in 2018, accounting for 66.01% of all financing and investment deals in overseas markets. Europe and Asia (excluding China) follow closely behind.

Investment and financing activities in India’s healthcare sector have been increasing in recent years. In 2018, there were 64 such deals in India, second only to those in China and the United States. As the world’s second-most populous country, India is gradually unlocking its potential in healthcare and is poised to become the third-largest healthcare market globally, after China and the United States.

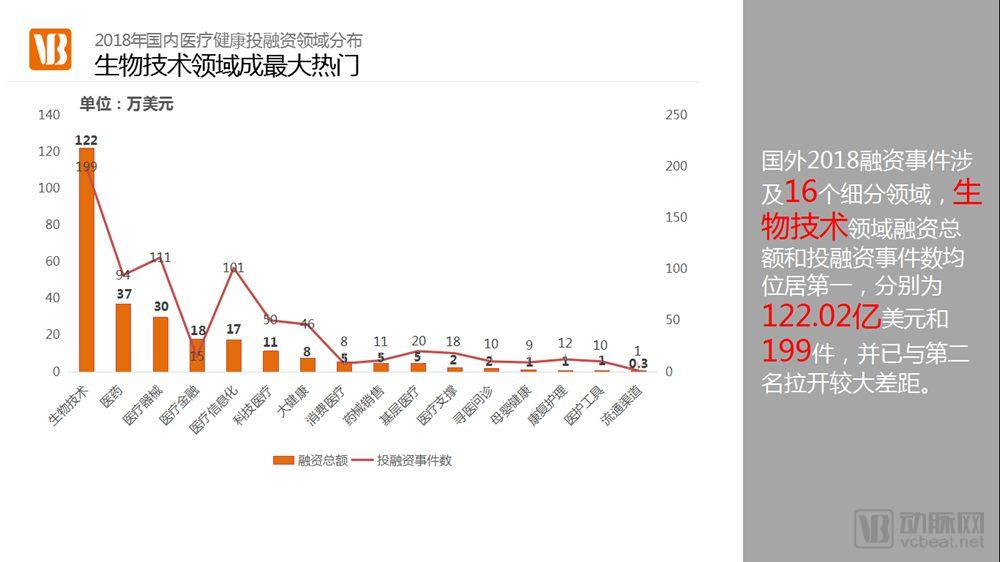

In 2018, the biotechnology sector emerged as the most prominent hotspot across all segments of the overseas market, maintaining a substantial lead. Total financing for the biotechnology sector in overseas markets reached $12.2 billion, accounting for 45.89% of the overall total and nearing half of the entire share.

Globally, the biotechnology industry has become the undisputed hottest sector in healthcare and is poised to maintain or even intensify its current momentum in the future. Compared with the technological gap between China and the United States in other high-tech industries, the disparity in biotechnology is relatively small, making it likely to emerge as a critical focal point in future Sino-U.S. technological competition.

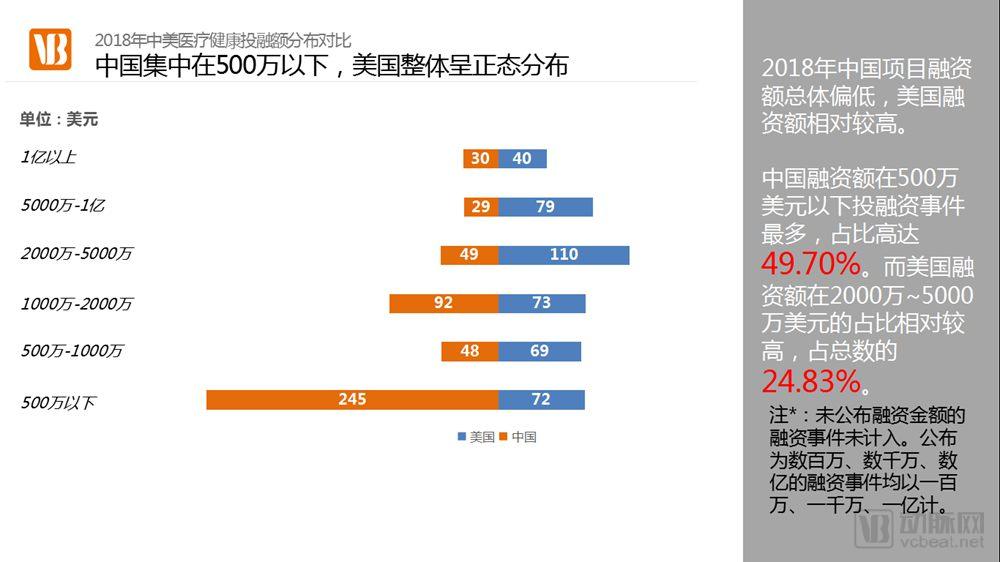

In 2018, a divergence began to emerge in the number of investment and financing deals between China and the United States, with China recording approximately 1.5 times as many deals as the U.S. However, in contrast, the total funding amount in the U.S. was about 1.75 times that of China, and the average deal size in the U.S. far exceeded that in China.

In China, financing and investment activities in the healthcare sector remain dominated by small-ticket deals under $5 million, with another minor peak observed in the $10–20 million range. In contrast, U.S. deals are significantly larger in size, exhibiting a normal distribution centered around $20–50 million.

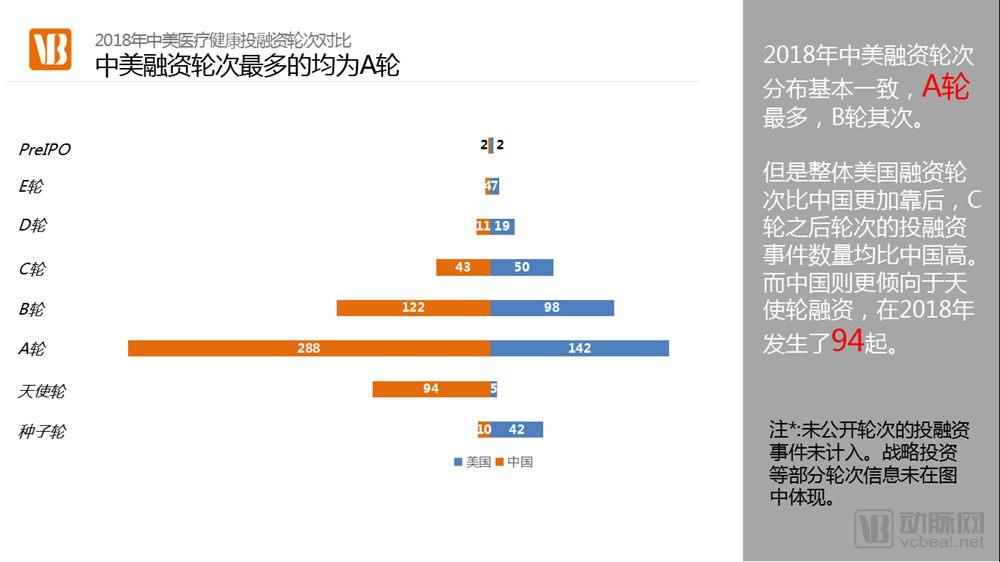

In 2018, Series A accounted for the highest number of investment and financing deals in the healthcare sector in both China and the United States. However, from a structural perspective, China’s investment rounds were relatively earlier-stage, whereas those in the U.S. tended to cluster at Series B and beyond.

Compared with China, the U.S. healthcare market is more mature, with leading enterprises having emerged in most subsectors. Consequently, its investment and financing trends have largely moved away from small-scale, dispersed early-stage investments, shifting instead toward later-stage financing characterized by larger ticket sizes and a more concentrated focus on key investment hotspots.

In terms of attention to specific sub-sectors, the United States trails slightly behind China in all areas except biotechnology and healthcare finance. Nevertheless, the strategic focus of both countries is largely aligned, with the majority of investment and financing activities concentrated in four key sub-sectors: pharmaceuticals, biotechnology, medical devices, and healthcare informatics.