How Will the STAR Market Transform China's Capital Market in 2019?

Editor’s Note: This article is republished from Guotai Junan Securities Research, authored by the GTJA Research Product Center. VCBeat has been authorized to repost it.

At its sixth meeting held on January 23, the Central Committee for Comprehensive Deepening Reform reviewed and approved the “Overall Implementation Plan for Establishing the Science and Technology Innovation Board (STAR Market) at the Shanghai Stock Exchange and Piloting the Registration-Based IPO System” and the “Implementation Opinions on Establishing the Science and Technology Innovation Board (STAR Market) at the Shanghai Stock Exchange and Piloting the Registration-Based IPO System,” marking another major milestone for the STAR Market, which has been under intensive preparation since last year.

Although the launch of the STAR Market is imminent, there remains considerable debate over how it will ultimately reshape China’s capital markets.

We have identified certain “clues” from the event commentaries and annual strategy reports issued by various research teams at Guotai Junan Securities, complemented by the in-depth research continuously advanced since last year by Guotai Junan’s IPO research team and its small- and mid-cap equity team, in an effort to provide the most appropriate answer to this question at the current stage.

Following the conclusion of the meeting of the Central Committee for Comprehensively Deepening Reforms, Guotai Junan’s non-banking financial sector team promptly released an analysis on the impact of the launch of the STAR Market on securities firms’ investment banking businesses.

Guotai Junan’s non-banking financial team believes that the establishment of the STAR Market on the Shanghai Stock Exchange and the pilot implementation of the registration-based IPO system were among the most significant measures to deepen capital market reforms in 2019, with the registration-based system holding even greater significance. The market-oriented pricing mechanism implied by the registration-based system will represent the most important transformation in the capital market. A series of supporting regulatory details will subsequently be introduced to ensure the swift implementation of the registration-based IPO system on the Shanghai Stock Exchange’s STAR Market.

The draft implementing rules for the supporting regulatory framework are expected to be released for public comment after the “Two Sessions,” with the first batch of companies listing on the STAR Market anticipated as early as the second quarter.

Under the registration-based IPO system of the STAR Market on the Shanghai Stock Exchange, the market-oriented pricing mechanism and the co-investment requirement for underwriters will impose new demands on investment banks’ pricing capabilities, sales capabilities, and capital strength. Meanwhile, underwriting fee rates for STAR Market listed companies are likely to be higher than those for traditional enterprises. This will prompt securities firms’ investment banking businesses to move beyond their traditional role as mere issuance channels, positively influencing the industry-wide pricing levels and practice quality of investment banking services. Such developments will help foster a more fair, orderly, and reasonable pricing mechanism, as well as a healthy competitive landscape within the industry.

Furthermore, the competitive landscape of investment banking will further concentrate among top-tier securities firms. The registration-based system on the STAR Market will bring certain incremental performance gains and synergistic value to the participating top-tier securities firms:

Underwriting and Sponsorship Revenue: As part of incremental reforms, the listing pace for the first batch of companies on the STAR Market will be controlled. The number of initial issuers is expected to range from 10 to 15, with a total issuance size under RMB 20 billion. Based on a 5% underwriting and sponsorship fee rate, this would generate RMB 1 billion in investment banking revenue. Compared with our estimated industry-wide investment banking revenue of approximately RMB 35 billion in 2018, this represents a 2.9% contribution. Its contribution to total industry revenue is expected to be below 0.5%, which is relatively limited.

Under the registration-based IPO system on the STAR Market, investment banks with strong pricing and distribution capabilities will gain greater influence in the allocation of new share offerings, thereby fostering stronger client stickiness with participating institutions and facilitating enhanced synergistic value.

Under the co-investment mechanism for underwriting institutions, investment banks will generate certain co-investment income; detailed rules, such as the co-investment ratio, remain to be clarified in subsequent drafts for public comment.

Financial Engineering

In its report “Five Major Annual Trading Strategies for 2019” by Guotai Junan Securities Research Institute, the Guotai Junan Financial Engineering Team stated that the launch of the STAR Market has exerted a divergent effect on existing ChiNext constituents: on one hand, it has led to a revaluation of certain companies with characteristics akin to those of STAR Market-listed firms; on the other hand, it has posed challenges to some traditional ChiNext companies.

Therefore, the stocks on the STAR Market that were viewed favorably in 2019 shared a pricing rationale centered on three aspects:

Under the registration-based system, listed companies are subject to more stringent information disclosure requirements. Consequently, publicly disclosed financial and non-financial metrics will serve as more critical references for investors. Specifically, factors such as corporate reputation, the proportion of R&D expenditure to total assets, the stage of R&D development, the actual rate of commercialization, the degree of market monopoly held by new technologies, as well as the number of existing and potential customers, may become important considerations in the valuation of companies listed on the STAR Market.

Drawing on the 13th Five-Year Plan for the Development of Strategic Emerging Industries and the Implementation Measures for Regulatory Work on the Domestic Issuance and Listing of Stocks or Depositary Receipts by Pilot Innovative Enterprises, the industries primarily covered include high-tech and strategic emerging sectors such as the Internet of Things (IoT), big data, cloud computing, artificial intelligence, software and integrated circuits, high-end equipment manufacturing, and biopharmaceuticals.

Initially, listed companies on the STAR Market are expected to be predominantly star enterprises from the primary market. Given the potentially limited supply, it is advisable to identify their respective industrial chains and uncover listed targets with distinctive industrial characteristics.

Non-bank Financial Services

Guotai Junan’s non-bank financial services team stated in its annual strategy report, titled “Waiting for Spring in Winter,” that the incremental reforms to the registration-based system on the STAR Market are of significant importance:

First, the market-based pricing mechanism is a fundamental change in the capital market, with an impact no less than that of the shareholding reform.

Second, this is not only a major transformation in the capital market that significantly impacts the competitive landscape of securities firms, but also reflects a deepening trend toward capitalization in investment banking, which places high demands on intermediaries’ pricing capabilities, sales capabilities, and capital strength.

Further policy-driven upside surprises in the securities industry are expected to persist, with leading brokerages poised to benefit more significantly.

Small and Mid-Cap

In its annual strategy report titled “Value Unfolds Along the Middle Path, Growth Leads to Drive Sci-Tech Innovation,” Guotai Junan’s Small- and Mid-Cap Team stated that, given the emphasis on stability in the short-term listing of companies on the STAR Market—with strict control over the number and pace of listings—the ChiNext board is poised to benefit first from the valuation uplift spurred by the launch of the STAR Market.

The launch of the ChiNext board will help in the short term

Enhancing the Valuation Level of the SME Board

As a pilot reform for incremental market expansion, Guotai Junan’s IPO team expects the STAR Market to differ from existing markets in three aspects: listing standards, investors, and institutional frameworks.

Company: Focusing on Sci-Tech Innovation Enterprises, Pursuing Differentiated Competition

The establishment of the STAR Market serves two primary purposes: first, it directs domestic enterprises’ attention toward scientific and technological innovation, stimulating their enthusiasm for R&D investment; second, it improves the financing chain for the development of technology-based enterprises by providing a financing platform that facilitates exits for private equity (PE), venture capital (VC), and other investors.

After bearing higher risks in the early stages, private equity (PE) and venture capital (VC) firms can achieve exit through listings on the STAR Market once companies enter a relatively stable and mature phase. This not only facilitates a shift in financing sources for technology enterprises but also enables PE and VC firms to recycle capital to support new startups, thereby unblocking the corporate financing chain and creating a positive virtuous cycle.

Support for science and technology and strategic emerging industries facilitates the transformation and upgrading of China's economy, enabling higher-quality development.

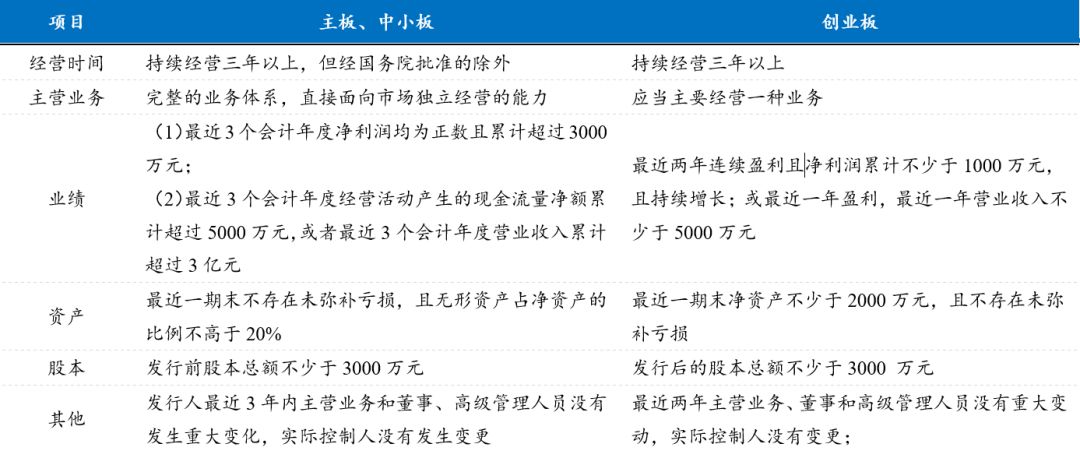

Currently, one of the listing requirements for the Main Board and the SME Board is that the net profit must be positive in each of the last three fiscal years, with a cumulative total exceeding RMB 30 million. For the ChiNext Board, listing requires either profitability in the most recent year with operating revenue of no less than RMB 50 million, or profitability in two consecutive years with a cumulative net profit of no less than RMB 10 million.

Both the Main Board and the ChiNext Board impose minimum profitability requirements, and in practice, due to the large number of companies waiting in line for listing, the actual financial metrics of these companies generally far exceed the minimum thresholds.

Although the National Equities Exchange and Quotations (NEEQ) system does not impose explicit profitability requirements, an imbalance between supply and demand has emerged due to the excessive number of listed companies and insufficient investor participation.

Main Board, SME Board, ChiNext

Profitability Requirements for Listed Companies

Data Source: China Securities Regulatory Commission, Guotai Junan Securities Research

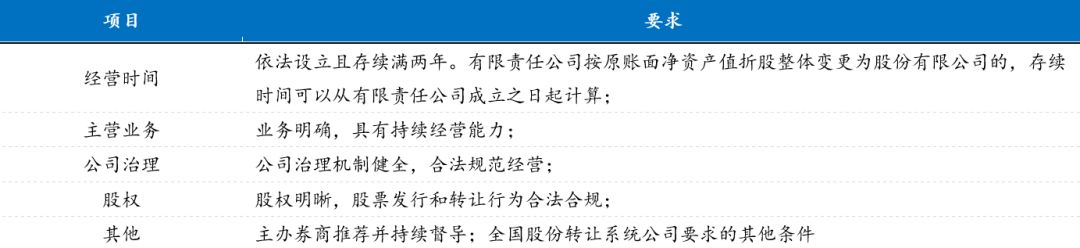

Listing requirements for companies on the NEEQ are relatively lenient.

Data Source: "Business Rules of the National Equities Exchange and Quotations (Trial)" and Guotai Junan Securities Research

Overall, the listing requirements for the Main Board and the ChiNext are excessively high, while those for the NEEQ are too low; therefore, the STAR Market is expected to strike a balance between the two.

Based on the public disclosures by the China Securities Regulatory Commission (CSRC) and the Shanghai Stock Exchange (SSE), as well as statements from relevant government officials, we believe that the listing requirements for companies on the STAR Market should be lower than those currently applicable to the ChiNext Board. (This assessment focuses on profitability criteria; if profitability is excluded, other metrics may be subject to stricter requirements than those of the ChiNext Board, serving as a compensation for the higher tolerance toward profitability indicators.)

In addition, certain changes may occur in aspects such as equity structure, which will significantly enhance inclusivity for companies that are not yet profitable and whose equity structures do not meet the listing requirements of the Main Board or the ChiNext Board.

In summary, in addition to the most basic requirements regarding operating history and corporate governance, we believe that the STAR Market may impose regulations on listed companies in the following areas:

1. Financial Indicators

De-emphasize profitability, adopt multiple optional criteria, focus on the trade-off between profitability and other metrics, or introduce indicators such as market capitalization and the ratio of R&D expenses to revenue.

There were four sets of listing standards prepared for the Strategic Emerging Industries Board, namely:

Market Capitalization + Cash Flow + Revenue

Market Capitalization + Revenue

Market Cap + Net Profit

Market Capitalization + Shareholders' Equity + Total Assets

It is anticipated that the overall framework of listing standards for the STAR Market will draw reference from the design of the Strategic Emerging Industries Board, adopting a multi-indicator optional system. The core principle is to de-emphasize profitability by offering multiple alternative criteria, whereby a relaxation in one standard is offset by heightened requirements in others.

If a company’s standard imposes profitability requirements, the revenue requirements may be lower; if a standard does not require profitability, it may impose higher requirements on revenue, market capitalization, and cash flow from operating activities.

Additionally, the listing standards for the STAR Market may incorporate metrics such as R&D investment to underscore the emphasis placed on scientific and technological innovation.

2. Industry Indicators

Regarding the company’s industry classification, we consider it to be primarily focused on technology and strategic emerging industries. Specifically, we may still refer to the definitions outlined in the “Implementation Measures for Regulatory Work on the Domestic Issuance of Stocks or Depositary Receipts and Listing by Pilot Innovative Enterprises”:

Pilot enterprises should align with national strategies, possess core technologies, and enjoy high market recognition. They must belong to high-tech industries and strategic emerging industries, such as the internet, big data, cloud computing, artificial intelligence, software and integrated circuits, high-end equipment manufacturing, and biomedicine.

It should be noted that, with future economic and social development, the listing standards for company industries on the STAR Market may be subject to subsequent revisions.

Overall, the STAR Market is positioned at a higher level than the NEEQ and should be considered on par with the ChiNext Board. However, its focus on technology and strategic emerging industries further accentuates its prominence.

Each of the three has its own positioning, with complementarity outweighing competition. Differentiated development will become the mainstream trend; however, a clear divergence among companies will exert pressure on the ChiNext Board, potentially leading to a downward shift in its medium- to long-term valuation levels (in the short term, increased attention toward the STAR Market may boost ChiNext’s valuation).

In the long run, for companies that meet the listing requirements of the ChiNext board, the ultimate choice between listing on the ChiNext board and the STAR Market will likely depend more on valuation differences.

Investors: Set reasonable entry thresholds to guide incremental capital into the market

The STAR Market is an incremental market that will feature greater inclusivity for listed companies while also undergoing institutional exploration (such as reforms to the registration-based IPO system, issuance pricing, price fluctuation limits, and delisting mechanisms). Consequently, it will be a market characterized by significant uncertainty in its early stages.

It is expected that the investor suitability requirements for the STAR Market will be relatively stringent. In the initial phase, participants should primarily consist of institutional investors and high-net-worth individual investors, while retail individual investors are encouraged to participate in the STAR Market through public mutual funds.

Regarding the requirements for individual investors, provisions may be made concerning investment experience, risk tolerance, and assets, with financial thresholds expected to be lower than those of the New Third Board.

For the STAR Market, a key task is to maintain market supply-demand equilibrium, fully draw on the experience of the New Third Board, and guide incremental capital into the market.

System: Comprehensive supporting reforms, with marketization as the direction and strengthened investor protection

China has initially established a multi-tiered capital market, comprising the Main Board (including the SME Board), the ChiNext Board, the New Third Board (NEEQ), and regional equity markets. However, each segment faces certain challenges: the listing thresholds for the ChiNext Board are relatively high, making it difficult for unprofitable companies to list; meanwhile, the New Third Board suffers from severe liquidity shortages due to an oversupply of listings resulting from its rapid expansion under the registration-based system.

The launch of the STAR Market has effectively addressed existing issues by positioning itself to serve the sci-tech innovation sector. Its overall listing thresholds are lower than those of the ChiNext Board but higher than those of the NEEQ, thereby not only alleviating the difficulties tech enterprises face in going public but also preventing a range of problems associated with excessive market expansion.

Furthermore, the STAR Market bears the mission of serving as a pilot for institutional reforms, undertaking comprehensive exploration of a package of systems including the registration-based IPO system. Companies may face a series of institutional reforms in their issuance and listing, trading, information disclosure, and delisting processes. In addition, corresponding supporting measures are required for investor protection and the supervision of listed companies.

1. Issuance Phase: Explore the registration-based system or adopt market-oriented pricing

Companies listing on the STAR Market will be subject to a registration-based system, which significantly lowers the threshold for initial public offerings. To avoid an overly rapid increase in the number of listed companies in the short term and prevent liquidity issues similar to those seen on the New Third Board, regulators are expected to appropriately control the pace of listings during the initial phase.

Meanwhile, the pricing of corporate IPOs is likely to be deregulated in favor of market-based pricing, making it difficult for the phenomenon of A-share companies experiencing multiple consecutive daily limit-ups after listing to recur. This places higher demands on investors’ pricing capabilities, thereby further accentuating the advantages of institutional investors.

2. Trading Phase: The daily price limit system may undergo reform, and information disclosure requirements will become more stringent

The implementation of the registration-based IPO system means that regulatory authorities will only review the legality and compliance of companies’ filing materials, without making judgments on the quality or merits of the enterprises, thereby significantly lowering the listing threshold. This necessitates strengthened oversight of listed companies in areas such as information disclosure, along with stringent crackdowns on certain irregularities currently present in China’s A-share market.

Meanwhile, the current 10% daily price limit for A-shares may be widened or even abolished.

3. Delisting Process: Strengthened enforcement, strict implementation of exit mechanisms to maintain market vitality.

The issuance process has adopted a registration-based system, so the exit mechanism must operate smoothly. Delisting policies must be strictly enforced to maintain a dynamic market with both entries and exits, ensuring survival of the fittest. This will prevent a substantial increase in the number of listed companies and a surge in stocks characterized by low prices, low market capitalization, and low trading volumes, which could lead to insufficient market liquidity.

1. The launch of the STAR Market may exceed expectations

Market expectations currently point to the establishment of the STAR Market in the first half of 2019. However, Guotai Junan’s IPO team believes that most institutional preparations and system testing were already completed during the first half of 2018 with the advancement of Chinese Depositary Receipts (CDRs) for innovative enterprises. The rapid approval of key companies, notably Foxconn Industrial Internet (11.850, +0.01, +0.08%), also helped streamline the regulatory authorities’ expedited review mechanism. At present, the main obstacles to be addressed lie in institutional experiments to liberalize pricing mechanisms and trading restrictions.

From 2009 to 2012, the ChiNext board underwent market-oriented IPO pricing, during which more than 800 new stocks were issued, with a total issuance scale exceeding RMB 1 trillion. The results were significant, and regulatory authorities accumulated certain experience in liberalizing pricing mechanisms. The draft for public consultation on the STAR Market and the pilot registration-based system is expected to be released soon, with breakthrough progress in the establishment of related systems and the board anticipated in the first quarter of 2018.

2. No definitive list yet, but criteria for candidate companies are becoming increasingly clear

Based on relevant information and our assessment, candidate companies are primarily expected to emerge from the high-tech sector. Key evaluation metrics include core business activities, revenue, net profit, R&D expenditure as a percentage of revenue, the number of granted invention patents, and industry ranking.

Candidate enterprises should hold a prominent position in their industry either globally or domestically. While profitability is not mandatory, they must achieve a certain scale of revenue. Additionally, they must meet specific criteria, including possessing independent intellectual property rights, maintaining an R&D investment ratio of no less than 3%, ensuring that scientific and technical personnel account for no less than 5% of the total workforce, and deriving no less than 40% of their revenue from high-tech enterprise products.

3. Pilot of the Registration-Based System: Limited Liquidity Shock

Currently, the registration-based IPO system widely adopted around the world generally allows companies to list once they meet the specified requirements. Regulatory authorities implement ex-post oversight, adhering to a lenient approach during the issuance and listing phase while enforcing strict supervision after listing.

The market’s interpretation of the implementation of the registration-based IPO system focuses on the significant expansion in the number of listed companies, which is expected to exert substantial pressure on market liquidity. However, we believe that such concerns are unlikely to materialize in the short term.

Meanwhile, we anticipate that the initial issuance scale on the STAR Market will remain within RMB 50 billion, with 20–50 companies going public, which will to some extent divert IPO volume from the traditional market.

We believe that, to avoid significant disruption to the existing market, the initial phase of the Science and Technology Innovation Board (STAR Market) will continue to prioritize registration-based review. Regulatory authorities will maintain stringent oversight over companies applying for listing via registration. Meanwhile, to mitigate substantial impact on the currently fragile market, the STAR Market adopts an incremental reform approach, ensuring that the overall number of listed companies remains controllable and the issuance pace continues in line with the prevailing style.

In terms of funding, due to the temporary suspension of Chinese Depository Receipts (CDRs), CDR strategic placement funds—originally designed to support new-economy enterprises listing in the domestic market—are highly likely to shift their focus to investments in the STAR Market once it is fully established. Meanwhile, we believe that entry barriers will inevitably be imposed during the initial phase of the STAR Market’s operation. If a threshold of RMB 500,000 or more is implemented, a large number of small and medium-sized investors may be excluded from participating in the STAR Market.

Based on statements from regulatory authorities, small and medium-sized investors are encouraged to participate in investments in the STAR Market through public mutual funds and other channels. Specifically, small and medium-sized investors who do not meet the eligibility thresholds cannot immediately sell their existing holdings via securities accounts to purchase STAR Market stocks; instead, they must invest indirectly by purchasing corresponding public fund products. Obstacles in the conversion process and cumbersome operational procedures will dampen the willingness of small and medium-sized investors to sell their existing holdings and switch to investing in STAR Market stocks.

In summary, before the conditions for implementing the registration-based system are fully mature in China, regulatory review will remain the primary standard for corporate listings. Regulatory authorities will retain decision-making power over the pace of issuance and the number of listings, and the establishment of the STAR Market will have a limited impact on the outflow of capital from the exchange-traded market.

4. Stronger Correlation Between the ChiNext and STAR Market

We believe that assessing the impact of a new sector’s launch on existing sectors should be based on two factors: the valuation level of the new sector and its correlation with existing sectors.

Valuation Levels of the New Sector

As the detailed implementation rules for the listing standards of the STAR Market have not yet been released, we merely speculate that companies listed on the STAR Market will undergo market-oriented bookbuilding, and the assessment criteria for listing conditions will be diversified. Considering the initial phase of the STAR Market’s operation, regulatory authorities may prioritize the listing of new economy enterprises with high visibility in the national economy and significant market share within their respective niche segments. Such companies typically exhibit characteristics of large revenue scales and high market capitalization, but with less pronounced profitability, leading to higher valuation metrics based on the Price-to-Earnings (P/E) ratio. Therefore, we believe that companies listed on the STAR Market will initially demonstrate features of elevated valuations.

Correlation of Existing Sectors

We selected biopharmaceutical and TMT companies with the highest correlation to STAR Market-listed enterprises within each sector as samples. It is evident that biopharmaceutical and TMT companies account for the largest proportion of both the number of listings and market capitalization on the ChiNext Board, reaching 42% and 46%, respectively. These figures are significantly higher than those on the SME Board (25% and 36%) and the Main Board (14% and 10%). This further suggests that if a substantial number of biopharmaceutical and TMT companies were to list on the STAR Market, the correlation between the ChiNext Board and the STAR Market would be the strongest.

Number and Market Capitalization of Biopharmaceutical and TMT Companies

Highest Weighting but Lowest Valuation on the ChiNext Board

Data source: Guotai Junan Securities Research, Wind

From the perspective of sector structure, the ChiNext Board exhibits the highest correlation with the STAR Market. However, in terms of valuation levels for biopharmaceutical and TMT companies, the ChiNext Board has the lowest valuations among the three domestic market segments. Consequently, if high valuation characteristics emerge during the initial listing phase on the STAR Market, it will inevitably exert a significant impact on the valuation system of the more closely correlated ChiNext Board.

5. The impact of the STAR Market on the market valuation system may depend more heavily on market conditions

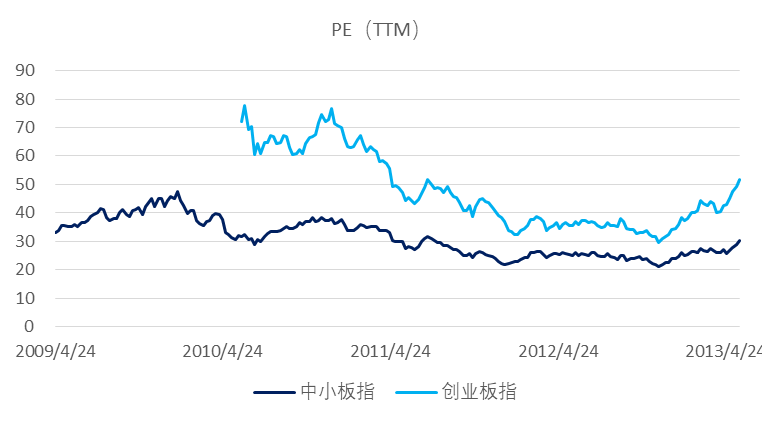

Compared to 2009, when the ChiNext board was launched, the introduction of the STAR Market has seen fundamental differences at the institutional level; nevertheless, we can still identify certain patterns from historical experience.

Two Distinct Characteristics Emerged After the Launch of the ChiNext Board in 2009:

The new board (ChiNext) will exhibit higher valuations, with pronounced premium characteristics;

The new board (ChiNext) demonstrates a significant leading effect after its listing, with valuation changes occurring earliest among the three boards, meaning it leads both rallies and declines.

From the perspective of market valuation levels before and after the launch of the ChiNext board

New sectors generally exhibit a leading role after their market listing.

Source: Guotai Junan Securities Research

It can also be observed that, driven by expectations of high valuations for the ChiNext Board, the SME Board, which exhibits a higher correlation with it, showed significant positive movement during the two-month window period prior to its listing, and subsequently moved in tandem with changes in ChiNext’s valuation.

Let us revisit the market environment surrounding the launch of the ChiNext board. In 2009, following the systemic risks of 2008, China’s capital market exhibited a strong positive wealth effect, with the Shanghai Composite Index rising from 1,800 points at the beginning of the year to over 3,400 points in August.

Optimistic or pessimistic market sentiment tends to amplify upward or downward price movements, respectively. The favorable market atmosphere in 2009 provided a conducive environment for the launch of the ChiNext board, while further reinforcing optimistic expectations regarding its high valuations. Consequently, under such circumstances, the SME Board, which exhibited a high correlation with the ChiNext board, benefited more significantly.

Currently, the ChiNext and STAR Market exhibit a strong correlation. However, it is important to note that high correlation can be either strongly positive or strongly negative. We tentatively attribute the primary factor influencing this directionality to market sentiment.

At this stage, the time window is relatively long. Whether the launch of the STAR Market will have a positive or negative impact on the existing market segments will still be determined by next year’s market environment. We propose two possible scenarios for its evolution:

If the STAR Market is launched relatively quickly in the first quarter or first half of this year, and market sentiment improves, creating a favorable environment for the STAR Market, we believe that the A-share market, dominated by the ChiNext Board, will exhibit a strong positive correlation in response. Valuation levels are expected to be revised upward due to event-driven stimuli.

The STAR Market was launched as scheduled in the first quarter or first half of this year. However, market sentiment remained subdued, and risk appetite stayed at a low level. The launch of the STAR Market may exert a short-term shock to market liquidity. Furthermore, as the market anticipates stronger policy support for the STAR Market, expectations for the ChiNext Board have been dampened. Consequently, the valuation level of the ChiNext Board will be negatively correlated with the launch of the STAR Market, leading to a certain degree of short-term impact.

It can be tentatively concluded that the existing ChiNext board is more sensitive to the launch of the STAR Market. However, regarding the impact of the STAR Market’s introduction on various existing boards, particularly the ChiNext board, we believe that shifts in market risk appetite are more significant. Therefore, we recommend closely monitoring developments related to the STAR Market while actively paying attention to changes in risk appetite.